The question of whether student debt forgiveness will be automatic has become a pressing concern for millions of borrowers in the United States. As discussions around debt relief policies intensify, many are left wondering if eligible individuals will receive forgiveness without needing to apply or take additional steps. While some proposals suggest streamlined processes, such as automatic forgiveness for those meeting specific criteria, others may require borrowers to actively apply or provide documentation. The outcome will likely depend on the final legislation or executive action, leaving borrowers eagerly awaiting clarity on how and when relief might be implemented.

| Characteristics | Values |

|---|---|

| Automatic Forgiveness Eligibility | Not automatic for all borrowers; depends on specific programs and criteria |

| Income-Driven Repayment (IDR) Forgiveness | Automatic after 20-25 years of qualifying payments, depending on the plan |

| Public Service Loan Forgiveness (PSLF) | Requires application; not automatic, even after 10 years of qualifying payments |

| Biden Administration's One-Time Forgiveness (2022) | Automatic for borrowers with income below certain thresholds (e.g., $125,000 individual, $250,000 married) |

| Loan Type Eligibility | Only federal student loans are eligible for automatic forgiveness programs |

| Notification to Borrowers | Borrowers may receive notifications, but must often take action to confirm eligibility |

| Tax Implications | Forgiveness may be tax-free depending on the program and state laws |

| Current Status (as of 2023) | Programs like IDR and PSLF are active; Biden's one-time forgiveness is paused due to legal challenges |

| Future Changes | Potential for policy changes, but no guarantees of broader automatic forgiveness |

| Private Loans | Not eligible for federal automatic forgiveness programs |

Explore related products

What You'll Learn

![]()

Eligibility criteria for automatic student debt forgiveness

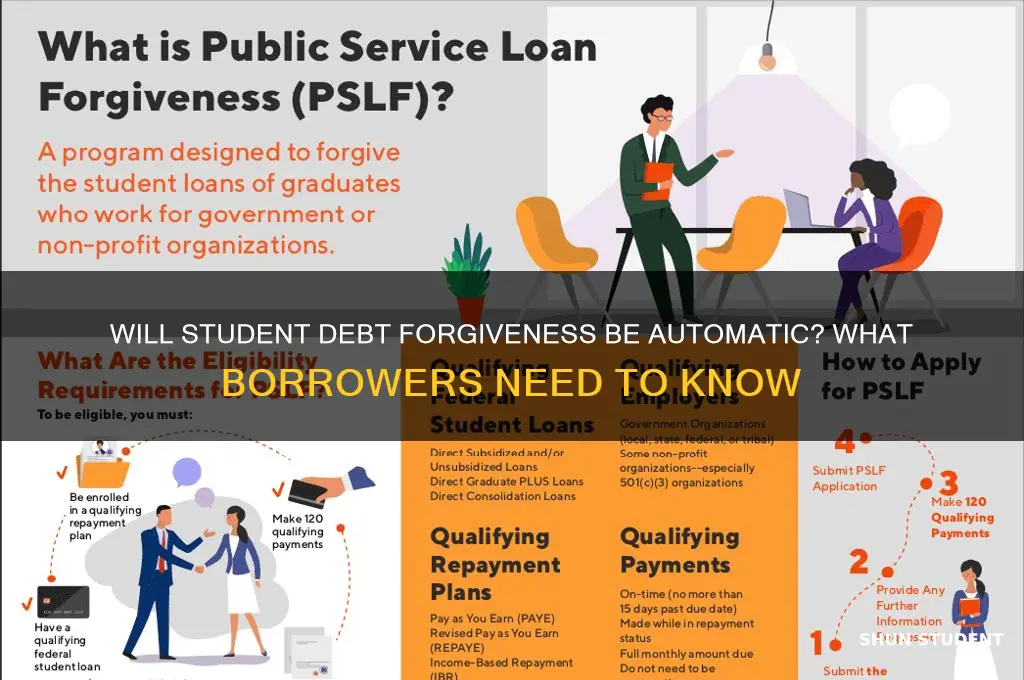

Automatic student debt forgiveness hinges on specific eligibility criteria, which vary depending on the program or policy in question. For instance, the Public Service Loan Forgiveness (PSLF) program requires borrowers to make 120 qualifying payments while working full-time for a government or nonprofit organization. This example underscores the importance of understanding the precise conditions that trigger automatic forgiveness. Without meeting these criteria, borrowers may miss out on relief, even if they believe they qualify.

To determine eligibility, borrowers must first identify the type of loans they hold, as not all loans qualify for automatic forgiveness. Federal Direct Loans, for example, are eligible for PSLF, while Federal Family Education Loans (FFEL) and Perkins Loans may require consolidation into a Direct Loan to qualify. This step is critical, as incorrect loan types can disqualify borrowers from automatic forgiveness. Checking the National Student Loan Data System (NSLDS) can help borrowers confirm their loan types and ensure they meet this foundational requirement.

Income-driven repayment (IDR) plans also play a pivotal role in automatic forgiveness eligibility. Under these plans, borrowers’ monthly payments are capped based on their income and family size, and any remaining balance is forgiven after 20–25 years of qualifying payments. However, borrowers must recertify their income and family size annually to remain eligible. Failure to do so can result in disqualification, even if all other criteria are met. This highlights the need for proactive management of repayment plans to ensure continuous eligibility.

Another key criterion is the borrower’s employment status and history. For programs like PSLF, consistent employment in a qualifying public service role is mandatory. Borrowers must submit an Employment Certification Form (ECF) periodically to verify their eligibility. Incomplete or inaccurate forms can delay or derail the forgiveness process. Keeping detailed records of employment and payments is essential, as these documents serve as proof of eligibility when forgiveness is applied for automatically.

Finally, borrowers should be aware of potential policy changes that could expand or restrict automatic forgiveness eligibility. For example, recent initiatives like the Fresh Start program aim to help defaulted borrowers regain eligibility for forgiveness programs. Staying informed about such updates through official channels like the Department of Education’s Federal Student Aid website can ensure borrowers take advantage of all available opportunities. Proactive engagement with these criteria and resources is the key to securing automatic student debt forgiveness.

Discover Student Loans: Are They Eligible for Forgiveness?

You may want to see also

Explore related products

![]()

Process for verifying income and loan types

Income verification is a critical step in determining eligibility for student debt forgiveness, as it ensures that relief is targeted toward borrowers who meet specific financial thresholds. The process typically involves submitting documentation such as tax returns, pay stubs, or employer certifications to confirm annual earnings. For example, under the Public Service Loan Forgiveness (PSLF) program, borrowers must provide proof of income through the Annual Certification and Application form, which is cross-referenced with IRS data. Similarly, income-driven repayment (IDR) plans require borrowers to recertify their income annually to adjust payment amounts, a process that may be streamlined but not eliminated under recent forgiveness initiatives.

Loan type verification is equally essential, as not all student loans qualify for forgiveness programs. Federal Direct Loans, for instance, are generally eligible, while Federal Family Education Loans (FFEL) and Perkins Loans held by private lenders often require consolidation into a Direct Loan to qualify. Borrowers must review their loan portfolios using tools like the National Student Loan Data System (NSLDS) to identify eligible loans. For example, the one-time student debt relief plan announced in 2022 explicitly excluded privately held FFEL loans, leaving many borrowers to navigate consolidation processes to access forgiveness.

The interplay between income verification and loan type assessment complicates the question of whether forgiveness will be automatic. While some programs, like the automatic PSLF waiver implemented in 2021, temporarily relaxed certain verification requirements, most initiatives still demand active participation from borrowers. For instance, the IDR Account Adjustment, which counts previously ineligible repayment periods toward forgiveness, requires borrowers to ensure their loan types and payment histories are accurately recorded. Automation in these cases is limited to backend processing, not the borrower’s responsibility to provide accurate data.

Practical tips for navigating this process include regularly updating contact information with loan servicers to receive notifications about required documentation and using the IRS Data Retrieval Tool to expedite income verification. Borrowers should also proactively consolidate ineligible loans into Direct Loans if pursuing forgiveness programs that exclude certain loan types. While the push for more automated forgiveness processes continues, the current reality demands vigilance and proactive engagement from borrowers to ensure they meet all eligibility criteria.

Michigan Teacher Loan Forgiveness: What Educators Need to Know

You may want to see also

Explore related products

![]()

Timeline for debt relief implementation

The timeline for student debt relief implementation is a critical aspect of understanding whether forgiveness will be automatic. Based on recent announcements and historical examples, the process is expected to unfold in phases, each with distinct milestones. Initially, eligible borrowers will receive notifications outlining their qualification status, likely through email or postal mail. This phase could begin as early as 60 to 90 days after the policy is finalized, depending on administrative readiness. Borrowers should monitor their accounts and official government communications during this period to ensure they don’t miss crucial updates.

Once notifications are sent, the application phase will commence, though this step may be bypassed for certain borrowers. For instance, those with income-driven repayment plan histories or existing Department of Education records may qualify for automatic forgiveness. Others, particularly those with private loans serviced by federal contractors or incomplete records, may need to submit applications. This phase is projected to last 3 to 6 months, with a staggered rollout to prevent system overloads. Borrowers should prepare by gathering documentation, such as tax returns or loan statements, to streamline the process if required.

After applications are processed, debt relief will be applied to accounts, a step expected to take 4 to 8 weeks per borrower. During this time, loan servicers will update balances and notify borrowers of the changes. It’s essential to verify these adjustments independently by logging into accounts or contacting servicers directly. Errors, such as incorrect forgiveness amounts or overlooked loans, should be reported immediately to avoid long-term complications.

Finally, the post-implementation phase will focus on appeals and corrections. Borrowers who believe they were wrongly denied forgiveness or received insufficient relief will have a designated window, likely 60 to 90 days, to contest decisions. This phase underscores the importance of retaining all communications and documentation related to the process. While the timeline aims for efficiency, borrowers should remain proactive and informed to navigate potential delays or discrepancies.

Loan Forgiveness: Boosting Opportunities for Privileged Students in Education

You may want to see also

Explore related products

$9.99 $12.99

$14.95 $14.95

![]()

Required documentation for borrowers

Borrowers seeking student debt forgiveness often assume the process will be seamless, but the reality is far more nuanced. While some forgiveness programs may automatically apply to eligible borrowers, others require active participation and documentation. Understanding what paperwork is needed—and why—can mean the difference between approval and denial. For instance, income-driven repayment (IDR) plans often mandate annual income verification, typically through tax returns or pay stubs, to adjust monthly payments and track progress toward forgiveness. Similarly, Public Service Loan Forgiveness (PSLF) applicants must submit an Employment Certification Form (ECF) periodically and a final PSLF application to prove eligibility. Each program has its own rules, but the common thread is clear: documentation is not optional.

Consider the PSLF program, which requires borrowers to work full-time for a qualifying employer while making 120 eligible payments. To ensure compliance, borrowers must submit the ECF annually or when switching employers. This form verifies employment and payment eligibility, serving as a critical checkpoint. Missing even one submission can reset the clock on forgiveness eligibility. For IDR plans, borrowers must provide proof of income annually to recalculate payments. This often involves submitting tax returns, pay stubs, or other income documentation. Failure to do so can result in being placed on a standard repayment plan, derailing progress toward forgiveness. These examples underscore the importance of staying organized and proactive in gathering and submitting required documents.

From a practical standpoint, borrowers should treat documentation as an ongoing responsibility rather than a one-time task. Create a dedicated folder—physical or digital—to store all loan-related documents, including payment histories, employment certifications, and correspondence with loan servicers. Set calendar reminders for annual deadlines, such as IDR recertification or PSLF form submissions. For PSLF applicants, keep a running list of employers and dates of employment to streamline the ECF process. If self-employed or experiencing income fluctuations, gather additional documentation, such as profit-and-loss statements or bank statements, to support income claims. Being over-prepared is better than risking delays or disqualification due to missing paperwork.

A comparative analysis reveals that while some programs, like automatic forgiveness for certain federal employees under the American Rescue Plan, require minimal effort, most demand active participation. For example, borrowers in IDR plans must recertify income annually, while PSLF applicants must submit multiple forms over a decade. This highlights the need for borrowers to understand their specific program requirements. Unlike automatic processes, which rely on government databases to identify eligible borrowers, most forgiveness programs place the onus on the individual to prove eligibility. This distinction is crucial, as assuming automation can lead to costly oversights.

In conclusion, required documentation is the backbone of student debt forgiveness programs, ensuring accountability and compliance. Borrowers must approach this task with diligence, treating it as an integral part of their repayment strategy. By staying informed, organized, and proactive, they can navigate the process with confidence, maximizing their chances of achieving forgiveness. Remember: in the world of student loans, the devil is in the details—and the paperwork.

Can Native Americans Get Student Loan Forgiveness? Exploring Options

You may want to see also

Explore related products

![]()

Impact on credit scores and taxes

Student debt forgiveness, if implemented, could significantly alter the financial landscape for millions of borrowers. One critical aspect often overlooked is its impact on credit scores and taxes. While forgiveness may seem like an outright benefit, its effects on these areas are nuanced and require careful consideration.

Credit Scores: A Double-Edged Sword

Debt forgiveness can positively influence credit scores by reducing overall debt burden, which accounts for 30% of your FICO score. For instance, if $10,000 in student loans is forgiven, your credit utilization ratio decreases, potentially boosting your score. However, the process isn’t automatic. If the forgiven debt is reported as "settled for less than the full balance," it could temporarily lower your score. Lenders may view this as a negative mark, similar to a delinquency. To mitigate this, borrowers should monitor their credit reports post-forgiveness and dispute inaccuracies promptly. Additionally, maintaining timely payments on other debts during this period is crucial to offset any potential dip.

Tax Implications: The Hidden Cost

Forgiven student debt is often treated as taxable income by the IRS, unless specifically exempted by legislation like the American Rescue Plan Act (which excludes forgiven student loans from taxation through 2025). For example, if $50,000 in debt is forgiven, it could push you into a higher tax bracket, resulting in a substantial tax bill. Borrowers should calculate their potential tax liability using IRS Form 1099-C, which reports canceled debt. Proactive strategies, such as setting aside funds or exploring tax credits like the Lifetime Learning Credit, can help offset this burden. Consulting a tax professional is advisable to navigate these complexities effectively.

Practical Steps for Borrowers

To maximize benefits and minimize drawbacks, borrowers should take specific actions. First, verify if the forgiveness program includes tax exemptions. Second, request a detailed breakdown of how the forgiven debt will be reported to credit bureaus. Third, consider refinancing remaining debt at lower interest rates to further improve financial health. For those with private loans, negotiate with lenders for favorable terms, as private debt forgiveness is less standardized. Finally, stay informed about policy changes, as legislative updates can alter both credit and tax implications.

Long-Term Takeaway

While student debt forgiveness can provide immediate relief, its impact on credit scores and taxes demands strategic planning. Understanding these effects empowers borrowers to make informed decisions, ensuring that forgiveness serves as a stepping stone to financial stability rather than a temporary reprieve. By addressing both credit and tax considerations, individuals can fully leverage the benefits of debt forgiveness while avoiding unintended consequences.

Is Obama's Department Forgiving Student Loans? Facts and Updates

You may want to see also

Frequently asked questions

It depends on the specific forgiveness program. Some programs, like Public Service Loan Forgiveness (PSLF), require borrowers to apply, while others, such as targeted relief under certain executive actions, may be automatic for eligible borrowers.

If forgiveness is automatic, you will likely receive a notification from your loan servicer or the Department of Education. Check your account regularly and ensure your contact information is up to date.

In most cases, if forgiveness is automatic, no action is required. However, it’s always a good idea to monitor your loan status and stay informed about updates from official sources.

No, automatic forgiveness typically applies only to federal student loans. Private loans are not eligible for federal forgiveness programs unless specifically stated in legislation or executive action.

Contact your loan servicer or the Department of Education to inquire about your eligibility and status. Keep records of your communications and any documentation that supports your case.