The phase-out for the student loan interest deduction is a critical aspect of tax planning for borrowers, as it determines eligibility based on income thresholds. For tax year 2023, single filers with modified adjusted gross income (MAGI) between $75,000 and $90,000, and married couples filing jointly with MAGI between $155,000 and $185,000, face a gradual reduction in the deduction. Once income exceeds these ranges, the deduction is completely eliminated. This rule ensures that higher-income earners receive less or no benefit, while targeting relief toward those with greater financial need. Understanding these limits is essential for maximizing tax savings and managing student loan repayment strategies effectively.

| Characteristics | Values |

|---|---|

| Deduction Type | Above-the-line deduction (reduces taxable income) |

| Maximum Deduction Amount | $2,500 per year |

| Phase-Out Begins (Single Filers) | $75,000 in Modified Adjusted Gross Income (MAGI) |

| Phase-Out Ends (Single Filers) | $90,000 in MAGI (deduction completely phased out) |

| Phase-Out Begins (Married Filing Jointly) | $150,000 in MAGI |

| Phase-Out Ends (Married Filing Jointly) | $180,000 in MAGI (deduction completely phased out) |

| Eligible Loans | Student loans used for qualified higher education expenses |

| Eligible Expenses | Tuition, fees, room, board, books, supplies, and equipment |

| Tax Year Applicability | Current tax rules (as of latest data, typically updated annually) |

| Filing Status Impact | Phase-out ranges differ based on filing status (single, married filing jointly) |

| Dependency Status | Cannot claim the deduction if someone else claims you as a dependent |

| Refundable Credit | No, it is a non-refundable deduction |

| Income Calculation | Based on Modified Adjusted Gross Income (MAGI) |

| Loan Repayment Status | Applies to interest paid during the tax year on qualifying loans |

| Carryover Provision | No carryover of unused interest to future tax years |

Explore related products

What You'll Learn

![]()

Income Limits for Eligibility

The phase-out for the student loan interest deduction is directly tied to income limits, which determine eligibility for this tax benefit. For tax year 2023, single filers can claim the full deduction if their modified adjusted gross income (MAGI) is below $70,000, while the phase-out begins at $70,000 and completely phases out at $85,000. For married couples filing jointly, the full deduction is available if their MAGI is below $140,000, with the phase-out starting at $140,000 and ending at $170,000. These income thresholds are crucial because they dictate whether a taxpayer can claim the deduction in full, partially, or not at all. Understanding these limits is essential for maximizing tax savings related to student loan interest payments.

For taxpayers whose income falls within the phase-out range, the deduction is gradually reduced based on their MAGI. The reduction is calculated using a formula that prorates the deduction based on how far into the phase-out range the taxpayer's income falls. For example, a single filer with a MAGI of $80,000—midway through the phase-out range—would be eligible for 50% of the maximum deduction. This prorated approach ensures that the benefit is tapered off rather than eliminated abruptly, providing some relief to taxpayers whose incomes are slightly above the lower threshold.

It's important to note that taxpayers with incomes above the upper limits of the phase-out range ($85,000 for single filers and $170,000 for married filing jointly) are not eligible for the student loan interest deduction. This means that higher-income earners cannot claim this tax benefit, regardless of the amount of student loan interest they have paid during the year. As such, careful income planning may be necessary for those nearing these thresholds to optimize their eligibility for the deduction.

Married couples filing separately are not eligible for the student loan interest deduction, regardless of their income level. This restriction underscores the importance of considering tax filing status when planning for student loan interest deductions. Couples in this filing category may need to explore alternative strategies, such as prepaying deductible expenses or contributing to retirement accounts, to offset their tax liability.

Lastly, taxpayers should be aware that the income limits for the student loan interest deduction are not adjusted for inflation annually, unlike some other tax provisions. This means that over time, more taxpayers may find themselves exceeding the income thresholds and losing eligibility for the deduction. Staying informed about current income limits and planning accordingly can help taxpayers make the most of this tax benefit while it remains available to them.

Understanding Typical Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Gradual Reduction Process

The gradual reduction process for the student loan interest deduction phase-out is a mechanism designed to limit the tax benefit for higher-income earners. This process ensures that the deduction is targeted towards individuals who may need it most, rather than providing a blanket benefit across all income levels. For tax year 2023, the phase-out begins for taxpayers with a modified adjusted gross income (MAGI) of $70,000 if single, or $140,000 if married filing jointly. Understanding this threshold is the first step in comprehending how the gradual reduction process works. Once a taxpayer’s income exceeds these limits, the deduction begins to decrease incrementally.

The reduction is calculated based on the amount by which the taxpayer’s income surpasses the initial threshold. For every dollar of income above the $70,000 (single) or $140,000 (married filing jointly) mark, the eligible interest deduction is reduced by $1. This continues until the deduction is completely phased out at a MAGI of $85,000 for single filers and $170,000 for married filers. For example, a single taxpayer earning $75,000 would see their deduction reduced by $5,000, as their income exceeds the threshold by that amount. This linear reduction ensures a fair and gradual decrease in benefits as income rises.

It’s important to note that the phase-out range is fixed and does not adjust annually for inflation, unlike some other tax provisions. This means that as incomes rise over time, more taxpayers may find themselves subject to the phase-out rules. Taxpayers should carefully calculate their MAGI to determine where they fall within the phase-out range. MAGI includes income from wages, salaries, and other sources, with certain adjustments, so it may differ from a taxpayer’s standard AGI. Accurate calculation is crucial to avoid overclaiming the deduction.

Taxpayers nearing or within the phase-out range can employ strategies to manage their MAGI and maximize their deduction. For instance, contributing to retirement accounts or making other pre-tax deductions can lower MAGI and potentially keep the taxpayer below the phase-out threshold. Additionally, understanding the timing of income recognition can be beneficial. If possible, deferring bonuses or other income to the following tax year may help maintain eligibility for the full deduction in the current year.

In summary, the gradual reduction process for the student loan interest deduction is a structured mechanism that limits the benefit for higher-income earners. By understanding the income thresholds, calculating MAGI accurately, and employing strategic financial planning, taxpayers can navigate the phase-out rules effectively. This ensures that the deduction remains a valuable tool for those who need it most while maintaining fairness in the tax system.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Tax Filing Status Impact

The phase-out for the student loan interest deduction is a critical aspect of tax planning, and your tax filing status plays a significant role in determining eligibility and the extent of the phase-out. For single filers, the phase-out begins at a modified adjusted gross income (MAGI) of $70,000 and is completely phased out at $85,000. This means that as your income increases within this range, the amount of student loan interest you can deduct gradually decreases. For example, if your MAGI is $75,000, you would only be eligible for a partial deduction, while at $85,000 or above, you would not qualify for the deduction at all. Understanding this threshold is essential for single filers to maximize their tax benefits.

For married couples filing jointly, the phase-out rules are different and can significantly impact the deduction. The phase-out range for joint filers starts at a MAGI of $140,000 and is completely phased out at $170,000. This wider range provides married couples with more flexibility, but it also means that careful income planning is necessary to retain the deduction. For instance, if a couple’s combined MAGI is $155,000, they would still qualify for a partial deduction, but at $170,000 or higher, the deduction would be eliminated. Married couples should consider strategies such as deferring income or contributing to retirement accounts to stay within the eligible income range.

Married individuals filing separately face stricter limitations when it comes to the student loan interest deduction. Regardless of income level, those who file separately are not eligible for the deduction. This filing status completely disqualifies taxpayers from claiming the deduction, making it a less advantageous option for couples with student loan debt. If both spouses have student loans, filing separately could result in a significant loss of potential tax savings. Therefore, it’s crucial for married couples to weigh the pros and cons of their filing status in relation to this deduction.

Head of household filers have a phase-out range similar to single filers but with slightly different thresholds. The phase-out begins at a MAGI of $70,000 and is fully phased out at $85,000. This filing status is often used by unmarried individuals who financially support dependents, and it offers a middle ground between single and joint filing statuses. For head of household filers, understanding the phase-out rules is key to optimizing their tax situation, especially if they are managing both student loan payments and dependent care expenses.

In summary, your tax filing status directly influences the phase-out rules for the student loan interest deduction, affecting both eligibility and the amount you can deduct. Single and head of household filers face the same phase-out range, while married couples filing jointly have a broader income threshold. However, married individuals filing separately are excluded from the deduction entirely. By carefully considering your filing status and income level, you can strategically plan to maximize this valuable tax benefit. Always consult a tax professional to ensure you’re making the most informed decisions based on your unique financial situation.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Phase-Out Thresholds for 2023

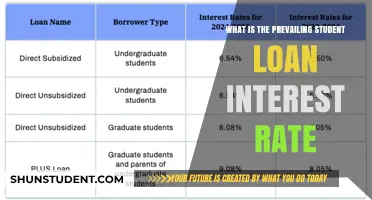

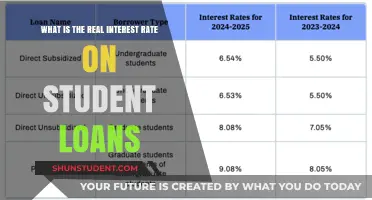

The phase-out thresholds for the student loan interest deduction in 2023 are crucial for borrowers to understand, as they determine eligibility for this tax benefit. For the tax year 2023, the phase-out begins for taxpayers with modified adjusted gross incomes (MAGIs) exceeding certain thresholds. Single filers start experiencing the phase-out once their MAGI surpasses $75,000, while the deduction is completely phased out at $90,000. This means that if a single taxpayer earns more than $90,000, they are no longer eligible to claim the student loan interest deduction. It’s important to note that these figures are adjusted periodically to account for inflation, ensuring they remain relevant to current economic conditions.

For married couples filing jointly, the phase-out thresholds are higher but follow a similar structure. In 2023, the phase-out begins when the combined MAGI exceeds $155,000, and the deduction is entirely eliminated once income reaches $185,000. This broader range reflects the assumption that married couples may have higher combined incomes while still benefiting from the deduction. Understanding these thresholds is essential for joint filers to plan their finances and maximize potential tax savings related to student loan interest payments.

Taxpayers filing as head of household also have specific phase-out thresholds for 2023. The phase-out starts at a MAGI of $75,000, similar to single filers, but the deduction is fully phased out at $90,000. This category is designed for individuals who are unmarried and pay more than half the cost of maintaining a home for themselves and a qualifying dependent. While the thresholds align with those for single filers, head of household filers should carefully assess their MAGI to determine eligibility for the deduction.

It’s critical for borrowers to calculate their MAGI accurately, as this figure directly impacts eligibility for the student loan interest deduction. The MAGI is determined by taking the adjusted gross income (AGI) and adding back certain deductions or exclusions, such as foreign earned income or housing exclusions. Once the MAGI is calculated, taxpayers can compare it to the 2023 phase-out thresholds to gauge their eligibility. For those nearing the phase-out limits, exploring other tax strategies or deductions may help offset the loss of this particular benefit.

Lastly, borrowers should be aware that the student loan interest deduction is capped at $2,500 per year, regardless of the actual interest paid. Even if a taxpayer’s MAGI falls within the eligible range, the deduction cannot exceed this limit. Additionally, the deduction is considered "above-the-line," meaning it can be claimed even if the taxpayer does not itemize deductions. By staying informed about the 2023 phase-out thresholds and how they apply to individual circumstances, borrowers can make informed decisions to optimize their tax situation.

Understanding Student Loan Interest Rates: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

$78.99 $84.99

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![]()

Elimination Criteria Explained

The phase-out for the student loan interest deduction is a critical aspect of understanding who qualifies for this tax benefit and to what extent. The elimination criteria are primarily based on the taxpayer's modified adjusted gross income (MAGI), which determines whether the deduction is fully available, partially available, or completely phased out. For single filers, the phase-out begins at a MAGI of $70,000 and is completely eliminated at $85,000. For married couples filing jointly, the phase-out starts at $140,000 and ends at $170,000. These income thresholds are crucial because they directly dictate eligibility, ensuring that the deduction primarily benefits taxpayers within specific income brackets.

The elimination criteria are structured to gradually reduce the deduction as income rises within the phase-out range. For example, if a single filer has a MAGI of $75,000, they would be eligible for a partial deduction, calculated based on the proportion of their income within the phase-out range. The formula reduces the deduction by the amount their income exceeds the lower threshold ($70,000) divided by the width of the phase-out range ($15,000). This proportional reduction ensures a fair transition from full eligibility to complete ineligibility as income increases.

Taxpayers with a MAGI above the upper limits of the phase-out range ($85,000 for single filers and $170,000 for married couples) are not eligible for the student loan interest deduction. This criterion is absolute, meaning no deduction is available regardless of the amount of student loan interest paid. The rationale behind this elimination is to target the deduction toward individuals and families with moderate incomes, who are more likely to benefit from the financial relief it provides.

It’s important to note that the elimination criteria apply only to the student loan interest deduction and do not affect other education-related tax benefits, such as the American Opportunity Credit or the Lifetime Learning Credit. Taxpayers should carefully assess their MAGI and understand how it impacts their eligibility for this specific deduction. Additionally, the phase-out ranges are not adjusted annually for inflation, so taxpayers must monitor their income levels to determine eligibility each tax year.

Lastly, the elimination criteria highlight the importance of strategic tax planning for individuals with student loans. Taxpayers nearing the phase-out thresholds may consider strategies to reduce their MAGI, such as contributing to retirement accounts or timing income and deductions, to maximize their eligibility for the student loan interest deduction. Understanding these criteria empowers taxpayers to make informed financial decisions and optimize their tax benefits.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Frequently asked questions

The phase-out for the student loan interest deduction begins at a modified adjusted gross income (MAGI) of $70,000 for single filers and $140,000 for married couples filing jointly. The deduction is completely phased out at $85,000 for single filers and $170,000 for married couples filing jointly.

The deduction is phased out gradually as income rises within the specified ranges. For every $1,000 of income above the phase-out threshold, the deduction is reduced by $1,000 until it is fully eliminated at the upper income limit.

Taxpayers with MAGI within the phase-out range may still qualify for a partial deduction, depending on how much their income exceeds the lower threshold. Those above the upper income limit are not eligible for the deduction.

No, the phase-out ranges differ by filing status. Single filers and married couples filing jointly have separate income thresholds, while married filing separately are not eligible for the deduction at any income level.

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)