Understanding when interest is charged on student loans is crucial for borrowers to manage their debt effectively. Typically, interest on federal student loans begins accruing as soon as the loan is disbursed, though subsidized loans may offer a grace period during which the government covers the interest while the borrower is in school or in deferment. For unsubsidized loans, interest starts immediately and can capitalize, adding to the principal balance if not paid during periods like in-school deferment or grace periods. Private student loans vary widely, with some requiring interest payments while in school and others deferring payments until after graduation. Knowing these timelines helps borrowers plan for repayment, minimize long-term costs, and avoid unnecessary debt accumulation.

| Characteristics | Values |

|---|---|

| Interest Accrual During School | Interest accrues on unsubsidized loans while the borrower is in school. Subsidized loans do not accrue interest during this period. |

| Grace Period | Interest accrues on unsubsidized loans during the grace period (typically 6 months after leaving school). Subsidized loans do not accrue interest during this period. |

| Deferment | Interest accrues on unsubsidized loans during deferment. Subsidized loans do not accrue interest during this period. |

| Forbearance | Interest accrues on both subsidized and unsubsidized loans during forbearance. |

| Repayment Period | Interest accrues on all loans during the repayment period unless payments cover the interest. |

| Capitalization | Unpaid interest on unsubsidized loans may capitalize (added to the principal balance) during specific periods, such as at the end of the grace period or deferment. |

| Loan Type | Subsidized: No interest while in school, grace period, or deferment. Unsubsidized: Interest accrues at all times unless paid by the borrower. |

| Interest Rates | Rates vary by loan type and disbursement date. As of 2023, undergraduate subsidized/unsubsidized loans have a fixed rate of 5.5%, while graduate unsubsidized loans are at 7.05%. |

| Private Student Loans | Interest accrual terms vary by lender; typically accrues immediately after disbursement. |

Explore related products

What You'll Learn

![]()

Interest Accrual During School

Understanding when interest accrues on student loans is crucial for borrowers, especially during their time in school. Interest Accrual During School refers to the accumulation of interest on student loans while the borrower is still enrolled in an academic program. This period is significant because it directly impacts the total amount repaid over the life of the loan. For most federal student loans, such as Direct Subsidized Loans, the government pays the interest while the borrower is in school at least half-time, during the grace period after leaving school, and during deferment periods. This means that for subsidized loans, the borrower is not responsible for the interest that accrues during these times, and the loan balance remains unchanged.

However, not all student loans offer this benefit. For Direct Unsubsidized Loans, interest begins accruing as soon as the loan is disbursed, even while the borrower is still in school. This means that if the borrower does not make payments on the interest during this period, it will be capitalized—added to the principal balance of the loan—once repayment begins. Capitalization increases the total amount of the loan, leading to higher overall interest costs over time. Therefore, borrowers with unsubsidized loans are strongly encouraged to pay the accruing interest while in school, if possible, to minimize the long-term financial burden.

Private student loans operate differently and often have less favorable terms regarding interest accrual during school. Many private lenders require interest payments while the borrower is still enrolled, and failing to make these payments can result in capitalization, similar to unsubsidized federal loans. Some private loans may offer deferment options, but interest still accrues during this time and is typically capitalized when repayment begins. Borrowers should carefully review the terms of their private loans to understand their obligations and explore options like interest-only payments to manage costs effectively.

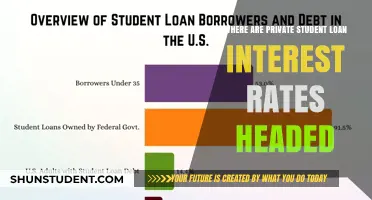

For borrowers with both subsidized and unsubsidized loans, it’s essential to track which loans are accruing interest during school. The U.S. Department of Education provides tools like the National Student Loan Data System (NSLDS) to help borrowers monitor their loan details. Additionally, contacting the loan servicer can provide clarity on which loans require immediate attention. Proactive management of interest accrual during school can save borrowers thousands of dollars in the long run.

Lastly, students should consider their financial situation and explore strategies to minimize interest accrual. For instance, making small monthly payments on unsubsidized loans or private loans can prevent capitalization and reduce the overall loan balance. Some students may also qualify for grants or scholarships that can reduce reliance on loans altogether. By staying informed and taking proactive steps, borrowers can better manage their student loans and avoid unnecessary financial strain after graduation.

Uniting Passions: The Power of Shared Interests Among Students

You may want to see also

Explore related products

![]()

Grace Period Rules

The grace period is a crucial aspect of understanding when interest is charged on student loans, offering borrowers a temporary reprieve from repayment obligations. This period typically begins after a student graduates, leaves school, or drops below half-time enrollment. For most federal student loans, including Direct Subsidized and Unsubsidized Loans, the grace period lasts for six months. During this time, borrowers are not required to make payments on their loans, providing a financial buffer as they transition from school to the workforce. However, it’s important to note that not all loans offer a grace period, such as some private student loans, which may require immediate repayment after graduation or even while still in school.

One of the key rules of the grace period is how it affects interest accrual. For Direct Subsidized Loans, the government pays the interest during the grace period, meaning the loan balance remains unchanged. In contrast, for Direct Unsubsidized Loans, interest begins accruing immediately after graduation, even during the grace period. If borrowers choose not to pay this accruing interest, it will be capitalized—added to the principal balance—once the grace period ends, increasing the total amount to be repaid. Understanding this distinction is essential for managing loan costs effectively.

Another important rule pertains to the use of the grace period. While it provides a break from payments, borrowers can still make voluntary payments during this time, which can help reduce the overall cost of the loan by lowering the principal or accrued interest. Additionally, borrowers should be aware that entering the grace period does not automatically enroll them in an income-driven repayment plan or other repayment options. Proactive communication with the loan servicer is necessary to explore repayment strategies before the grace period ends.

It’s also critical to know that the grace period is a one-time benefit for each loan. If a borrower returns to school at least half-time before the grace period ends, the full six-month grace period will be reinstated when they leave school again. However, if the grace period expires and the borrower fails to make payments, the loan may enter default, leading to severe financial consequences. Therefore, staying informed about the grace period’s end date and preparing for repayment is vital.

Lastly, private student loans often have different grace period rules, which vary by lender. Some private loans may offer a grace period similar to federal loans, while others may require immediate repayment or provide no grace period at all. Borrowers with private loans should carefully review their loan agreements to understand the terms, including when interest begins to accrue and when payments are due. Being aware of these differences ensures borrowers can plan accordingly and avoid unexpected financial burdens.

Student Loan Interest Waived: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

In-School Deferment Impact

In-school deferment is a critical provision for student loan borrowers, allowing them to temporarily pause their loan payments while enrolled in an eligible school at least half-time. This deferment period significantly impacts when and how interest accrues on student loans, depending on the loan type. For federal subsidized loans, the government covers the interest during in-school deferment, meaning the borrower’s loan balance remains unchanged. This benefit is a major advantage, as it prevents the loan from growing while the borrower focuses on their education. However, for federal unsubsidized loans, interest begins accruing immediately, even during deferment. If the borrower does not make payments on this accruing interest, it is capitalized (added to the principal balance) once the deferment period ends, increasing the total amount to be repaid.

The impact of in-school deferment on interest charges highlights the importance of understanding the type of loan a borrower holds. For unsubsidized loans, the deferment period can lead to higher overall costs due to interest capitalization. Borrowers can mitigate this by paying the accruing interest while in school, even if they are not required to make full payments. This proactive approach prevents the loan balance from growing and reduces the long-term cost of the loan. In contrast, subsidized loans offer a financial reprieve during deferment, as no interest accrues, making them a more borrower-friendly option.

Another aspect of in-school deferment impact is its influence on repayment strategies. Borrowers with unsubsidized loans may consider making interest payments during deferment as part of their financial planning. This strategy not only minimizes the loan’s growth but also reduces the burden once repayment begins. For subsidized loan holders, the absence of interest accrual allows them to focus solely on their studies without the added stress of increasing debt. However, it is essential for all borrowers to remain aware of their loan terms and the end date of their deferment period to prepare for repayment.

In-school deferment also affects borrowers’ eligibility for other benefits, such as loan forgiveness programs or income-driven repayment plans. For example, the deferment period counts toward the service requirements for Public Service Loan Forgiveness (PSLF), provided the borrower is working full-time in qualifying employment. Additionally, understanding the interest accrual during deferment helps borrowers make informed decisions about consolidating or refinancing their loans in the future. Consolidation can simplify repayment but may affect interest rates and deferment eligibility, so careful consideration is necessary.

Lastly, the in-school deferment impact extends to the borrower’s financial literacy and long-term financial health. By understanding how interest accrues during deferment, borrowers can develop better financial habits and make strategic decisions about their student loans. For instance, knowing the difference between subsidized and unsubsidized loans can guide borrowers in choosing the most suitable financial aid options. Additionally, staying informed about the deferment end date and repayment terms ensures a smoother transition into loan repayment, reducing the risk of default or financial strain. In summary, in-school deferment plays a pivotal role in managing student loan interest, and its impact varies based on loan type, borrower actions, and long-term financial planning.

Student Loan Interest Resumes: Key Dates and What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Capitalization of Interest

Interest capitalization on student loans is a critical concept borrowers must understand, as it directly impacts the total cost of repayment. Capitalization of interest occurs when unpaid interest is added to the principal balance of the loan, increasing the total amount owed. This process is particularly relevant for student loans because interest often accrues while the borrower is still in school or during grace periods, and if not paid, it capitalizes. For federal student loans, interest capitalization typically happens at the end of the grace period, after a deferment period, or when a loan is placed in forbearance. For private student loans, the terms of capitalization vary by lender, so borrowers should carefully review their loan agreements.

One common scenario where interest capitalization occurs is at the end of the grace period for federal student loans. Most federal loans offer a six-month grace period after graduation, leaving school, or dropping below half-time enrollment. During this time, interest accrues on unsubsidized loans but not on subsidized loans. If the borrower does not pay the accrued interest during the grace period, it is capitalized and added to the principal balance when the repayment period begins. This increases the total amount of interest that will accrue over the life of the loan, as interest is now charged on a higher principal amount.

Another instance of interest capitalization is when a borrower exits a deferment or forbearance period. Deferment allows borrowers to temporarily pause payments under specific conditions, such as returning to school or experiencing economic hardship, while forbearance is a discretionary pause granted by the lender. During deferment, interest may or may not accrue depending on the loan type—interest on subsidized loans is paid by the government, but it accrues on unsubsidized loans. In forbearance, interest always accrues. If this accrued interest is not paid by the borrower, it capitalizes at the end of the deferment or forbearance period, increasing the loan’s principal balance.

For income-driven repayment (IDR) plans, interest capitalization can occur if the monthly payment is insufficient to cover the accruing interest. IDR plans calculate payments based on the borrower’s income and family size, and sometimes these payments are lower than the monthly interest accrual. When this happens, the unpaid interest is capitalized annually, adding to the principal balance. This can lead to a situation known as "negative amortization," where the loan balance grows despite making regular payments. Borrowers on IDR plans should be aware of this risk and consider paying extra toward interest to prevent capitalization.

To minimize the impact of interest capitalization, borrowers should explore strategies such as making interest payments while in school, during grace periods, or while in deferment or forbearance. For federal loans, choosing an income-driven plan with a payment that covers at least the accruing interest can prevent capitalization. Additionally, borrowers may consider refinancing private loans to secure a lower interest rate or better terms, though this option is not available for federal loans and comes with the loss of federal benefits. Understanding when and how interest capitalizes empowers borrowers to make informed decisions and manage their student loan debt more effectively.

When Do Student Loan Interest Charges Begin? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Plan Effects

Interest on student loans is a critical factor that can significantly impact the total amount repaid over time. The timing and conditions under which interest accrues depend largely on the type of loan and the repayment plan chosen. Repayment Plan Effects play a pivotal role in determining when and how much interest is charged, influencing the overall cost of the loan. For instance, income-driven repayment plans often result in lower monthly payments but may extend the loan term, allowing more time for interest to accrue. Conversely, standard repayment plans typically have higher monthly payments but shorter terms, reducing the total interest paid.

One of the most direct Repayment Plan Effects is observed in subsidized vs. unsubsidized federal loans. For subsidized loans, the government pays the interest while the borrower is in school, during the grace period, and in certain deferment periods. However, for unsubsidized loans, interest begins accruing immediately after disbursement, regardless of the repayment plan. Choosing a repayment plan that does not cover this accruing interest can lead to capitalization, where unpaid interest is added to the principal balance, increasing the total amount owed. This effect is particularly pronounced in plans like the Income-Based Repayment (IBR) or Pay As You Earn (PAYE), where payments may not cover the accruing interest on unsubsidized loans.

Another critical aspect of Repayment Plan Effects is the impact of forbearance or deferment periods. While these options allow borrowers to temporarily pause payments, interest continues to accrue on unsubsidized loans and all private loans. Repayment plans that frequently utilize these options, such as those with flexible payment terms, can lead to substantial interest growth over time. For example, a borrower in a long-term forbearance period under a Graduated Repayment Plan may face a significantly higher balance once payments resume due to compounded interest.

Private student loans also exhibit distinct Repayment Plan Effects compared to federal loans. Private lenders often offer variable interest rates, which can fluctuate based on market conditions. Repayment plans with extended terms or low initial payments may expose borrowers to higher interest costs if rates rise. Additionally, private loans rarely offer income-driven repayment options, leaving borrowers with fewer tools to manage interest accrual. Selecting a repayment plan with fixed payments and a shorter term can mitigate the risk of escalating interest charges on private loans.

Finally, the choice of repayment plan can influence the eligibility for loan forgiveness programs, which in turn affects interest charges. For instance, borrowers enrolled in income-driven repayment plans may qualify for loan forgiveness after 20–25 years, but the forgiven amount could be taxable as income. During the repayment period, interest continues to accrue, and the total forgiven amount may include a significant portion of accrued interest. Understanding these Repayment Plan Effects is essential for borrowers to make informed decisions that minimize interest costs and align with their financial goals.

When Does Interest Begin on Your Student Loan?

You may want to see also

Frequently asked questions

Interest typically begins accruing on student loans as soon as the loan is disbursed, unless it’s a subsidized federal loan, in which case the government pays the interest while the borrower is in school, during the grace period, and in certain deferment periods.

For unsubsidized federal loans and most private loans, interest is charged while the borrower is in school. For subsidized federal loans, interest is not charged during this period.

For unsubsidized federal loans, interest continues to accrue during the grace period (usually 6 months after graduation). For subsidized federal loans, interest does not accrue during the grace period.

Interest is typically charged daily, based on the outstanding principal balance of the loan. It is then capitalized (added to the principal) at certain points, such as when the loan enters repayment or after a deferment or forbearance period ends.