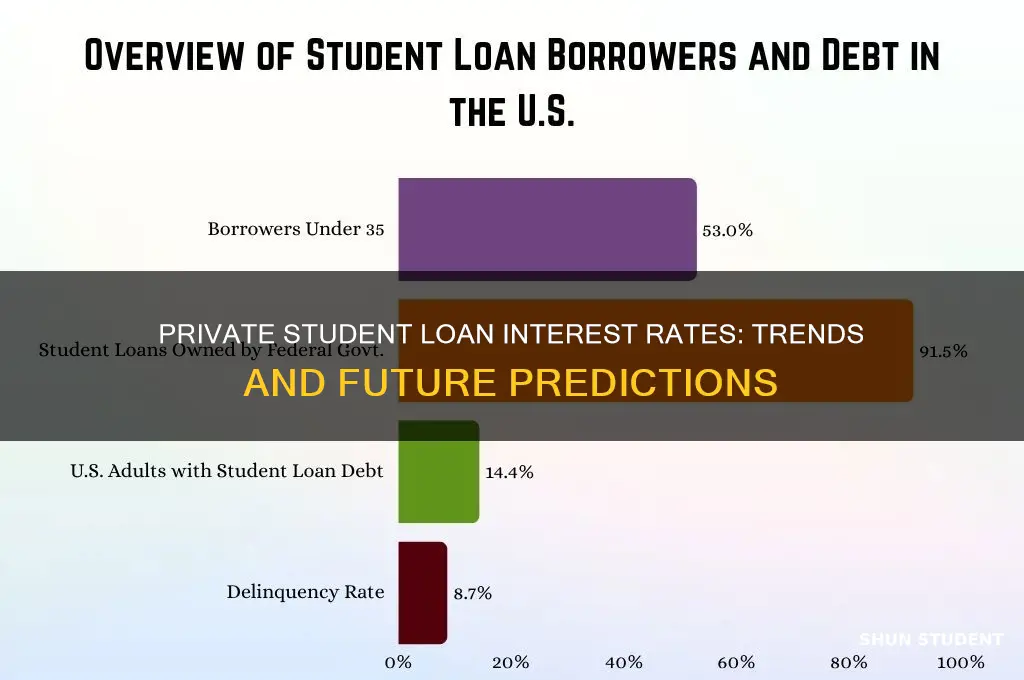

As the economic landscape continues to evolve, borrowers and financial experts alike are closely monitoring the trajectory of private student loan interest rates. Influenced by factors such as Federal Reserve policies, inflation trends, and market competition, these rates have seen fluctuations in recent years. With the Federal Reserve's ongoing efforts to manage inflation through interest rate hikes, private lenders are adjusting their terms accordingly, potentially leading to higher borrowing costs for students. However, increased competition among lenders and the introduction of more flexible repayment options may temper these increases. As a result, prospective borrowers must stay informed and compare offers to secure the most favorable terms in this dynamic environment.

Explore related products

What You'll Learn

![]()

Economic Indicators Impacting Rates

The trajectory of private student loan interest rates is intricately tied to broader economic indicators that influence lending costs and market conditions. One of the most significant factors is the Federal Reserve’s monetary policy, particularly changes to the federal funds rate. When the Fed raises rates to combat inflation or stabilize the economy, private lenders often follow suit, increasing the cost of borrowing for student loans. Conversely, during periods of economic downturn or low inflation, the Fed may lower rates, which can lead to more favorable terms for private student loans. Borrowers should closely monitor Fed announcements and economic forecasts to anticipate potential shifts in loan rates.

Another critical economic indicator is inflation, which erodes the purchasing power of money over time. Lenders factor inflation into their interest rate calculations to ensure they maintain profitability. High inflation typically leads to higher interest rates, as lenders demand compensation for the diminished value of future repayments. For private student loans, this means borrowers may face steeper rates in inflationary environments. Conversely, low or stable inflation can create a more favorable borrowing climate. Tracking inflation metrics, such as the Consumer Price Index (CPI), can provide insights into where private student loan rates might be headed.

Unemployment rates also play a pivotal role in shaping private student loan interest rates. High unemployment levels can signal economic uncertainty, prompting lenders to perceive higher risk in lending. As a result, they may increase interest rates to offset potential defaults. For students and recent graduates, a weak job market can exacerbate the challenge of securing affordable loans. Conversely, a robust job market with low unemployment can lead to more competitive lending rates, as lenders feel more confident in borrowers’ ability to repay. Economic reports, such as the Bureau of Labor Statistics’ monthly jobs data, are essential tools for understanding this dynamic.

The yield on U.S. Treasury bonds is another key indicator that influences private student loan rates. Lenders often benchmark their rates against Treasury yields, which reflect the risk-free rate of return. When Treasury yields rise, private loan rates tend to follow, as lenders adjust their pricing to remain competitive with government securities. Conversely, falling Treasury yields can lead to lower borrowing costs for students. Monitoring Treasury auctions and economic forecasts can help borrowers gauge the direction of private student loan rates.

Lastly, economic growth projections impact lender sentiment and, consequently, interest rates. Strong GDP growth typically signals a healthy economy, encouraging lenders to offer more competitive rates to attract borrowers. However, if economic growth slows or contracts, lenders may become more risk-averse, leading to higher rates or stricter lending criteria. Economic reports from institutions like the Federal Reserve or the International Monetary Fund (IMF) provide valuable insights into growth trends and their potential impact on private student loan rates. By staying informed about these indicators, borrowers can make more strategic decisions about when and how to secure financing for their education.

Where to Deduct Student Loan Interest on Your Tax Return

You may want to see also

Explore related products

![]()

Federal Reserve Policy Influence

The Federal Reserve's monetary policy decisions have a significant and direct influence on private student loan interest rates, making it a critical factor to consider when predicting future trends. As the central banking system of the United States, the Federal Reserve's primary tools for implementing monetary policy include adjusting the federal funds rate, open market operations, and forward guidance. When the Federal Reserve raises or lowers the federal funds rate, it creates a ripple effect throughout the economy, impacting various interest rates, including those for private student loans.

One of the key ways the Federal Reserve influences private student loan interest rates is through its control of short-term interest rates. Private lenders often base their student loan interest rates on benchmarks such as the London Interbank Offered Rate (LIBOR) or the Prime Rate, both of which are closely tied to the federal funds rate. When the Federal Reserve raises the federal funds rate, these benchmarks tend to increase, leading to higher interest rates on private student loans. Conversely, when the Federal Reserve lowers the federal funds rate, these benchmarks decrease, potentially resulting in lower interest rates for borrowers. As of recent trends, the Federal Reserve's actions to combat inflation have led to a series of rate hikes, which have contributed to rising private student loan interest rates.

Moreover, the Federal Reserve's forward guidance plays a crucial role in shaping market expectations and, consequently, private student loan interest rates. Forward guidance refers to the Federal Reserve's communication about its future monetary policy plans. When the Federal Reserve signals that it intends to maintain a tight monetary policy or continue raising rates, lenders may anticipate higher borrowing costs and adjust their private student loan interest rates accordingly. This can create a sense of certainty or uncertainty in the market, influencing the pricing of private student loans. Borrowers should closely monitor the Federal Reserve's statements and economic projections to gauge the potential direction of private student loan interest rates.

In addition to its direct impact on short-term interest rates, the Federal Reserve's policies also affect long-term interest rates, which are relevant for fixed-rate private student loans. The Federal Reserve's large-scale asset purchases, also known as quantitative easing, can put downward pressure on long-term interest rates, including those for private student loans. However, as the Federal Reserve begins to reduce its balance sheet or engage in quantitative tightening, long-term interest rates may rise, leading to higher fixed rates for private student loans. Understanding the Federal Reserve's balance sheet policies and their potential effects on the yield curve is essential for predicting the trajectory of private student loan interest rates.

The Federal Reserve's influence on private student loan interest rates is further amplified by its role in shaping overall economic conditions. When the Federal Reserve pursues a tight monetary policy, it can slow down economic growth, reduce inflation, and increase unemployment. In such an environment, lenders may become more risk-averse, leading to stricter lending standards and higher interest rates for private student loans. Conversely, a accommodative monetary policy can stimulate economic growth, increase inflation, and reduce unemployment, potentially resulting in more favorable lending conditions and lower interest rates for borrowers. As the Federal Reserve navigates the delicate balance between controlling inflation and supporting economic growth, its policies will continue to have a profound impact on the private student loan market, making it essential for borrowers to stay informed about monetary policy developments.

Lastly, it is crucial for borrowers to recognize that the Federal Reserve's policy influence on private student loan interest rates is not the only factor at play. Other factors, such as market competition, lender risk appetite, and individual creditworthiness, also contribute to the determination of private student loan interest rates. However, given the Federal Reserve's significant role in shaping the overall interest rate environment, its policies remain a critical consideration for borrowers seeking to understand where private student loan interest rates are headed. By staying informed about Federal Reserve actions and their potential implications, borrowers can make more strategic decisions regarding their student loan financing, potentially saving thousands of dollars in interest costs over the life of their loans.

When Did Student Loan Interest Rates Rise? A Timeline Explained

You may want to see also

Explore related products

![]()

Market Competition Trends

The private student loan market is experiencing a shift in dynamics, primarily driven by increasing market competition, which is likely to influence interest rate trends in the coming years. As traditional lenders face growing pressure from fintech companies and online lending platforms, borrowers can expect more competitive interest rates and flexible repayment options. These new entrants are leveraging technology to streamline the loan application process, offer personalized rates, and provide transparent terms, thereby attracting a significant portion of the borrower market. This heightened competition is forcing established lenders to reevaluate their pricing strategies, potentially leading to a downward pressure on interest rates to remain attractive to prospective students.

One notable trend is the rise of peer-to-peer (P2P) lending platforms and online marketplaces that connect borrowers directly with individual or institutional investors. These platforms often offer lower interest rates compared to traditional banks due to reduced overhead costs and risk-based pricing models. As more students become aware of these alternatives, they are increasingly opting for private loans from non-traditional sources, compelling conventional lenders to adapt. This shift in borrower behavior is expected to contribute to a more competitive interest rate environment, where lenders must continuously innovate to stay relevant.

Another factor shaping market competition is the growing emphasis on borrower benefits and incentives. Lenders are now offering perks such as interest rate discounts for consistent on-time payments, cashback rewards, and flexible repayment plans to differentiate themselves. For instance, some lenders provide interest rate reductions for borrowers who sign up for automatic payments or complete a financial literacy course. These value-added features not only attract borrowers but also create a competitive landscape where interest rates are just one aspect of the overall loan package. As a result, students are likely to see more tailored loan products with competitive rates in the near future.

Furthermore, economic conditions and federal policy changes are indirectly influencing market competition in the private student loan sector. With federal student loan interest rates often serving as a benchmark, private lenders must remain competitive, especially when federal rates are low. Additionally, economic uncertainties may prompt lenders to adjust their risk assessments, potentially leading to more conservative lending practices or, conversely, more aggressive marketing to secure a larger market share. Borrowers should monitor these macroeconomic factors as they could impact the interest rate environment and the competitive strategies employed by lenders.

In summary, the private student loan market is becoming increasingly competitive, driven by the entry of fintech companies, P2P lending platforms, and innovative borrower incentives. This competition is expected to push interest rates downward and encourage lenders to offer more attractive terms. As students explore their financing options, they should stay informed about these market trends to make educated decisions. The evolving landscape suggests that private student loan interest rates are likely to remain competitive, benefiting borrowers who are willing to compare offers from multiple lenders.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Inflation and Rate Projections

The trajectory of private student loan interest rates is intricately tied to broader economic factors, particularly inflation and the Federal Reserve’s monetary policy. Inflation, as measured by the Consumer Price Index (CPI), has been a dominant force in recent years, driving up the cost of living and influencing borrowing costs. When inflation rises, lenders typically increase interest rates to protect the real value of the loans they issue. For private student loans, which are not subsidized by the government, this means borrowers often face higher rates as lenders adjust to the inflationary environment. As of the latest data, inflation has shown signs of cooling but remains above the Federal Reserve’s target of 2%, suggesting that interest rates may continue to reflect this elevated economic pressure.

The Federal Reserve’s actions play a critical role in shaping private student loan rates. The Fed has been raising the federal funds rate aggressively since 2022 to combat inflation, and these hikes have a ripple effect on all consumer lending, including private student loans. Most private student loans are tied to the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR), both of which are influenced by Fed policy. As the Fed continues to signal a "higher for longer" interest rate environment, borrowers can expect private student loan rates to remain elevated. Projections from economic analysts suggest that while the pace of rate increases may slow, a significant drop in rates is unlikely until inflation is firmly under control.

Economic forecasts for 2024 and beyond indicate that inflation will gradually return to the Fed’s target range, but this process is expected to be gradual. As a result, private student loan interest rates are unlikely to see a sharp decline in the near term. Borrowers should anticipate rates to stabilize at higher levels compared to the pre-pandemic era. Fixed-rate private student loans, in particular, may remain less attractive due to their higher upfront rates, while variable-rate loans could offer some relief if inflation continues to moderate. However, variable rates carry the risk of increasing further if economic conditions shift unexpectedly.

For prospective borrowers, understanding these projections is crucial for making informed decisions. Refinancing existing private student loans may be less appealing in the current high-rate environment, but locking in a fixed rate now could provide long-term stability if rates rise further. Additionally, borrowers should closely monitor economic indicators such as CPI reports and Fed announcements, as these will signal potential shifts in private loan rates. Financial experts advise comparing offers from multiple lenders and considering factors like repayment terms and borrower protections to mitigate the impact of higher rates.

In summary, inflation and the Federal Reserve’s monetary policy are the primary drivers of private student loan interest rates. While inflation is easing, it remains above target, keeping borrowing costs elevated. The Fed’s commitment to maintaining higher rates until inflation is fully tamed suggests that private student loan rates will not see significant decreases soon. Borrowers should stay informed, compare options, and strategize their financing decisions to navigate this challenging economic landscape effectively.

Maximize Your Tax Savings: Understanding Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Borrower Credit Score Effects

The trajectory of private student loan interest rates is closely tied to broader economic trends, such as Federal Reserve rate changes and market conditions. However, one of the most significant factors influencing the interest rate a borrower receives is their credit score. Borrower credit score effects are profound and multifaceted, directly impacting the cost of borrowing and the terms of the loan. Lenders use credit scores to assess the risk associated with lending to an individual, and higher scores generally translate to lower interest rates. As private student loan interest rates continue to fluctuate, understanding how credit scores affect these rates is crucial for borrowers seeking the most favorable terms.

A high credit score, typically above 720, positions borrowers to secure the lowest available interest rates on private student loans. Lenders view these individuals as low-risk, making them eligible for prime rates that can save thousands of dollars over the life of the loan. Conversely, borrowers with fair or poor credit scores (below 670) often face significantly higher interest rates, as lenders compensate for the perceived risk of default. In a rising interest rate environment, the disparity between rates offered to high- and low-credit-score borrowers tends to widen, making credit score optimization even more critical. Borrowers with lower scores may also struggle to qualify for loans without a cosigner, further limiting their options.

For borrowers with limited or no credit history, such as many students, the impact of credit score on private loan rates can be particularly challenging. Lenders often require a cosigner to mitigate risk, but this can also lead to higher rates if the cosigner’s credit score is not optimal. Building or improving credit before applying for a private student loan can significantly reduce borrowing costs. Simple steps like paying bills on time, reducing credit card balances, and avoiding new debt can help boost a credit score over time. As interest rates trend upward, proactive credit management becomes an essential strategy for minimizing loan expenses.

Another aspect of borrower credit score effects is the potential for rate reductions through refinancing. As borrowers improve their credit scores post-graduation, they may qualify for lower interest rates by refinancing their private student loans. This is especially relevant in a rising rate environment, where locking in a lower rate can provide long-term savings. However, refinancing is typically only an option for those with strong credit profiles, highlighting the importance of maintaining a good credit score throughout the loan term. Borrowers with poor credit may find themselves locked into high-interest loans with limited opportunities for improvement.

Lastly, the relationship between credit scores and private student loan rates underscores the need for financial literacy among borrowers. Understanding how credit behavior impacts loan terms empowers students to make informed decisions. For instance, missing payments or maxing out credit cards can quickly damage a credit score, leading to higher rates on future loans. As private student loan interest rates are expected to rise in response to economic conditions, borrowers must prioritize credit health to secure the best possible terms. In essence, a borrower’s credit score is not just a number—it’s a key determinant of their financial future in the student loan landscape.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Frequently asked questions

Private student loan interest rates are primarily influenced by the Federal Reserve’s monetary policy, economic conditions, inflation, and market competition among lenders. Additionally, individual borrower creditworthiness and cosigner involvement can impact the specific rate offered.

As of now, private student loan interest rates are expected to remain volatile, largely dependent on broader economic trends. If the Federal Reserve continues to raise benchmark rates to combat inflation, private loan rates may increase. However, if economic conditions stabilize or improve, rates could moderate or slightly decrease.

Borrowers can prepare by improving their credit scores, securing a cosigner with strong credit, and shopping around for lenders offering competitive rates. Refinancing existing loans when rates are favorable and staying informed about economic trends can also help mitigate the impact of rising interest rates.