The question of when the $10,000 student loan forgiveness will be applied has been a pressing concern for millions of borrowers since its announcement as part of the Biden administration’s debt relief plan. While the initiative aimed to provide financial relief to eligible borrowers, its implementation has faced significant legal challenges, including lawsuits that temporarily halted the program. As of now, the timeline for when the $10,000 forgiveness will be applied remains uncertain, pending the resolution of ongoing court battles and potential legislative actions. Borrowers are advised to stay informed through official channels, such as the Department of Education, for updates on the program’s status and next steps.

| Characteristics | Values |

|---|---|

| Announcement Date | August 24, 2022 |

| Eligible Borrowers | Recipients of federal student loans with income below $125,000 (individual) or $250,000 (married/head of household) |

| Loan Forgiveness Amount | $10,000 (additional $10,000 for Pell Grant recipients) |

| Loan Types Covered | Federal student loans held by the U.S. Department of Education |

| Application Process | Initially required application (now automatic for most eligible borrowers) |

| Implementation Status | On hold due to legal challenges (as of October 2023) |

| Legal Challenges | Blocked by Supreme Court ruling in June 2023 |

| Current Status | Program is not active; no debt relief has been applied |

| Alternative Relief | Payment pause ended on October 1, 2023; new SAVE repayment plan available |

| Future Outlook | Uncertain; depends on legislative or administrative action |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for the $10k student loan forgiveness and what are the requirements

- Application Process: Steps to apply for the $10k student loan forgiveness program

- Timeline Updates: Expected dates for $10k forgiveness implementation and disbursement

- Loan Types Covered: Which federal student loans are eligible for the $10k forgiveness

- Impact on Borrowers: How $10k forgiveness affects monthly payments and overall debt burden

![]()

Eligibility Criteria: Who qualifies for the $10k student loan forgiveness and what are the requirements?

The $10,000 student loan forgiveness initiative, part of the Biden administration's broader debt relief plan, hinges on specific eligibility criteria. To qualify, borrowers must meet income thresholds: individuals earning less than $125,000 annually or married couples filing jointly with incomes under $250,000 are eligible. These figures are based on adjusted gross income (AGI) from either 2020 or 2021 tax returns, allowing flexibility for those whose financial situations may have shifted due to the pandemic. This income-based approach ensures relief targets those most in need, balancing fiscal responsibility with equitable support.

Beyond income, the type of loan held is critical. Only federal student loans owned by the Department of Education qualify, including Direct Loans, subsidized and unsubsidized Stafford Loans, Parent PLUS Loans (if held by the student), and consolidated loans under the Direct Consolidation Loan program. Notably, Federal Family Education Loans (FFEL) and Perkins Loans not held by the Department of Education are ineligible unless consolidated into a Direct Loan before the application deadline. Borrowers with private loans or ineligible federal loans are excluded, underscoring the program’s focus on federally managed debt.

Pell Grant recipients receive special consideration under this plan. Those who received a Pell Grant in college are eligible for up to $20,000 in forgiveness, double the standard $10,000. This distinction acknowledges the financial challenges faced by low-income students, who often rely heavily on Pell Grants to fund their education. To confirm Pell Grant status, borrowers can check their Student Aid Report or log into their Federal Student Aid account, ensuring they maximize their potential relief.

Finally, borrowers must navigate the application process carefully. While the Department of Education has streamlined the application, requiring only basic personal and financial information, accuracy is paramount. Errors in income reporting or loan type selection can delay or disqualify applications. Borrowers should gather their tax returns, loan statements, and Pell Grant documentation beforehand. Additionally, staying informed through official channels is crucial, as updates and deadlines may shift due to legal challenges or administrative adjustments. Proactive preparation and attention to detail will ensure eligible borrowers secure the relief they deserve.

When Will Student Loan Forgiveness Checks Arrive? Key Dates Explained

You may want to see also

Explore related products

![]()

Application Process: Steps to apply for the $10k student loan forgiveness program

The $10,000 student loan forgiveness program, part of the Biden administration’s broader debt relief initiative, has generated significant interest. For eligible borrowers, understanding the application process is crucial to securing this financial relief. While the program’s rollout has faced legal challenges, the steps to apply remain clear for those who qualify. Here’s a detailed guide to navigating the application process effectively.

Step 1: Confirm Eligibility

Before applying, verify that you meet the program’s criteria. Borrowers with federal student loans held by the U.S. Department of Education, including Direct Loans and Federal Family Education Loans (FFELP) held by the Department, are eligible. Additionally, your annual income must fall below $125,000 (individual) or $250,000 (married couples) based on 2020 or 2021 tax returns. Pell Grant recipients may qualify for up to $20,000 in forgiveness. Double-check your loan type and income status using the Federal Student Aid website to avoid unnecessary delays.

Step 2: Gather Required Documentation

While the application itself is straightforward, having key documents ready streamlines the process. Ensure your Social Security Number (SSN), contact information, and Federal Student Aid (FSA) ID are accessible. If you’re unsure about your loan servicer or balance, log into your account on StudentAid.gov. For income verification, have your 2020 or 2021 tax returns handy, as the Department of Education may cross-reference your application with IRS data.

Step 3: Complete the Application

Once the application portal reopens (following legal resolutions), visit the official Department of Education website to submit your request. The form is designed to be user-friendly, requiring basic personal and financial information. Be precise and honest in your responses, as inaccuracies can lead to delays or denials. After submission, you’ll receive a confirmation email with a reference number—keep this for future inquiries.

Cautions and Tips

Beware of scams targeting borrowers seeking debt relief. The application is free, and no third-party services are required. Avoid sharing sensitive information unless you’re on the official government website. If you encounter technical issues, use the FSA’s help desk for assistance. Finally, monitor your email and loan servicer account for updates on your application status. Patience is key, as processing times may vary.

Applying for the $10,000 student loan forgiveness program requires preparation and attention to detail. By confirming eligibility, gathering documents, and submitting an accurate application, you maximize your chances of approval. Stay informed about program updates and remain vigilant against fraud. While the process may seem daunting, taking these steps ensures you’re on track to receive the financial relief you deserve.

Is One-Time Student Loan Forgiveness Application Available Now?

You may want to see also

Explore related products

![]()

Timeline Updates: Expected dates for $10k forgiveness implementation and disbursement

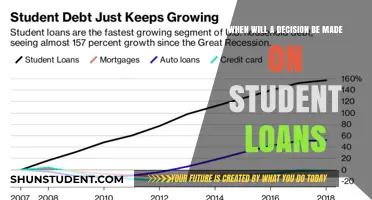

The Biden administration's student loan forgiveness plan has been a beacon of hope for millions of borrowers, but the timeline for its implementation has been anything but straightforward. Initially announced in August 2022, the program promised up to $10,000 in forgiveness for eligible borrowers, with an additional $10,000 for Pell Grant recipients. However, legal challenges have delayed its rollout, leaving borrowers in a state of uncertainty. As of late 2023, the Supreme Court’s decision to strike down the program has effectively halted its progress, but legislative efforts and alternative pathways are being explored to revive or replace it.

Analyzing the timeline, the first phase was expected to begin within weeks of the announcement, with borrowers submitting applications through a streamlined online portal. The Department of Education had projected that disbursement would start by early 2023, prioritizing those with existing income-driven repayment plans or verified incomes. However, the legal battles, particularly the Supreme Court case *Biden v. Nebraska*, brought the process to a standstill. Borrowers who applied before the court’s injunction in November 2022 had their applications held in limbo, with no clear indication of when or if they would be processed.

Instructively, borrowers should monitor updates from the Department of Education and trusted financial news sources for any revival of the program. If a new forgiveness plan emerges, it’s crucial to act swiftly. Prepare by ensuring your contact information is up-to-date with your loan servicer and gathering necessary documentation, such as proof of Pell Grant eligibility or income verification. Additionally, consider enrolling in income-driven repayment plans to reduce monthly payments while awaiting forgiveness.

Comparatively, the timeline for student loan forgiveness contrasts sharply with other debt relief programs. For instance, the Public Service Loan Forgiveness (PSLF) program operates on a clear, albeit lengthy, 10-year timeline. In contrast, the $10,000 forgiveness plan was designed for rapid implementation, but legal hurdles have transformed it into a protracted process. This highlights the importance of legislative stability in crafting effective relief measures.

Descriptively, the emotional toll of this delay cannot be overstated. Borrowers who planned their finances around the promise of forgiveness now face renewed anxiety as payments resume after the pandemic-related pause. For many, the $10,000 relief represented a lifeline, offering a chance to invest in homes, start families, or pursue careers without the burden of crushing debt. The uncertainty surrounding its implementation has left them in financial and emotional limbo, underscoring the need for a swift and decisive resolution.

Student Loan Case Decision Timeline: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Loan Types Covered: Which federal student loans are eligible for the $10k forgiveness?

The $10,000 federal student loan forgiveness plan, part of broader debt relief initiatives, specifically targets certain loan types. Understanding which loans qualify is crucial for borrowers seeking to maximize this opportunity. Not all federal student loans are eligible, and the criteria hinge on the loan’s origination, type, and holder. For instance, Direct Loans, including subsidized and unsubsidized Stafford Loans, PLUS Loans, and Consolidation Loans held by the Department of Education, are covered. However, loans not held by the Department of Education, such as those in the Federal Family Education Loan (FFEL) program or Perkins Loans owned by schools, are generally excluded unless consolidated into a Direct Loan before the application deadline.

To determine eligibility, borrowers should first identify their loan type through their Federal Student Aid account or by contacting their loan servicer. Direct Loans, the most common type, are automatically eligible for the $10,000 forgiveness. Borrowers with FFEL or Perkins Loans can still qualify by consolidating them into a Direct Consolidation Loan, but timing is critical. Consolidation must be completed before the forgiveness application deadline to ensure eligibility. This process can take several weeks, so borrowers should act promptly to avoid missing out.

Income plays a significant role in eligibility, with the $10,000 forgiveness available to individuals earning less than $125,000 annually or households earning under $250,000. Pell Grant recipients may qualify for an additional $10,000 in forgiveness, totaling $20,000. This distinction highlights the importance of checking Pell Grant status, as it significantly increases the potential relief. Borrowers can verify their Pell Grant status on their Student Aid Report or by logging into their Federal Student Aid account.

For practical steps, borrowers should gather documentation, including tax returns and loan statements, to confirm income and loan type. Applying for forgiveness is typically done through the loan servicer or a dedicated Department of Education portal. While the process is designed to be straightforward, borrowers should remain vigilant for updates, as legal challenges or policy changes could impact timelines. Staying informed through official channels ensures borrowers are prepared when the application window opens.

In summary, eligibility for the $10,000 student loan forgiveness hinges on loan type, holder, and borrower income. Direct Loans are automatically covered, while FFEL and Perkins Loans require consolidation. Pell Grant recipients stand to gain additional relief, making it essential to verify this status. By taking proactive steps to understand and prepare, borrowers can position themselves to benefit fully from this opportunity.

Is Student Loan Forgiveness Live? Latest Updates and What You Need to Know

You may want to see also

Explore related products

$14.95

![]()

Impact on Borrowers: How $10k forgiveness affects monthly payments and overall debt burden

The $10,000 student loan forgiveness initiative, once implemented, will immediately reduce the principal balance for eligible borrowers, directly impacting their monthly payments and overall debt burden. For those on income-driven repayment plans, a lower principal means recalculated payments based on the adjusted balance, potentially resulting in lower monthly obligations. For instance, a borrower with a $30,000 loan at a 5% interest rate and a 10-year term could see their monthly payment drop from $318 to $212 after $10,000 forgiveness, freeing up $106 monthly for other financial priorities.

Consider the psychological and financial relief this reduction provides. Borrowers with smaller balances may see their loans eliminated entirely, achieving debt-free status sooner than anticipated. For example, a borrower with $12,000 in loans could have $10,000 forgiven, leaving only $2,000 to repay. If they continue making their original $120 monthly payment, they could clear the remaining balance in just 16 months, compared to the original 10-year timeline. This accelerated payoff not only saves on interest but also removes the mental weight of long-term debt.

However, the impact varies depending on the repayment plan and loan type. Borrowers on standard 10-year plans may not see a change in monthly payments if their servicer applies the forgiveness to reduce the number of payments rather than the monthly amount. For instance, a borrower with $25,000 in loans might still pay $288 monthly but finish their repayment 3 years and 4 months earlier. Understanding how your servicer applies the forgiveness is crucial to managing expectations and budgeting effectively.

To maximize the benefits, borrowers should take proactive steps. First, ensure your loans qualify for forgiveness by confirming eligibility criteria, such as federal loan types and income thresholds. Second, review your repayment plan options post-forgiveness. Switching to an income-driven plan could further lower monthly payments, especially if your income has decreased. Lastly, allocate the savings strategically—whether toward high-interest debt, emergency funds, or retirement accounts—to build long-term financial stability.

In summary, the $10,000 forgiveness initiative offers tangible relief by reducing monthly payments, shortening repayment timelines, and alleviating overall debt stress. However, its impact hinges on individual loan structures and borrower actions. By understanding these dynamics and taking informed steps, borrowers can transform this policy into a cornerstone of their financial recovery and future planning.

Forgiving Student Loan Debt: Inflationary Impact or Economic Boost?

You may want to see also

Frequently asked questions

The $10,000 student loan forgiveness application process began in October 2022, but it was halted due to legal challenges. If the program resumes, eligible borrowers will receive forgiveness once their applications are processed, typically within several weeks to months after approval.

Eligibility for the $10,000 forgiveness depends on income limits: single filers earning under $125,000 and married couples filing jointly earning under $250,000 in 2020 or 2021. Borrowers with federal student loans held by the Department of Education qualify.

Most federal student loan borrowers will need to submit an application for the $10,000 forgiveness, though some data (like income) may be automatically verified. Check the Federal Student Aid website for updates on the application process.

No, the $10,000 student loan forgiveness applies only to federal student loans held by the Department of Education. Private loans are not eligible for this program.