The looming question of when will student loan crash has become a pressing concern for millions of borrowers, economists, and policymakers alike, as the staggering $1.7 trillion in U.S. student loan debt continues to weigh heavily on the economy. With rising defaults, increasing calls for debt forgiveness, and the precarious financial situations of many graduates, experts are debating whether the system is on the brink of collapse. Factors such as high tuition costs, limited job opportunities, and the burden of compounding interest have created a perfect storm, leaving many to wonder if the student loan bubble is unsustainable and when it might burst, potentially triggering widespread economic repercussions.

Explore related products

$8.34 $17.99

What You'll Learn

![]()

Economic Indicators Predicting Crash

The student loan market, a $1.7 trillion behemoth, is showing cracks under the weight of economic pressures. To predict a potential crash, economists scrutinize key indicators like delinquency rates, wage growth, and inflation. Delinquency rates, currently hovering around 10%, are a red flag. When borrowers consistently miss payments, it signals financial distress and increases the likelihood of defaults. Historically, a 15% delinquency rate has preceded significant market disruptions. Wage growth, stagnant for many borrowers, compounds the issue. If wages fail to outpace loan repayment obligations, borrowers are forced to choose between essentials and debt servicing, accelerating default risk. Inflation exacerbates this by eroding purchasing power, making fixed loan payments feel heavier. These indicators, when analyzed together, paint a picture of mounting vulnerability in the student loan sector.

Consider the role of unemployment rates as a predictive tool. A spike in unemployment directly correlates with loan defaults, as job loss eliminates income streams. During the 2008 financial crisis, unemployment surged to 10%, and student loan defaults followed suit. Today, while unemployment remains relatively low, underemployment—where borrowers work in jobs below their skill level—is a silent crisis. Underemployed graduates often struggle to meet repayment obligations, contributing to the delinquency rate. Monitoring unemployment trends, particularly in sectors employing recent graduates, is crucial. For instance, a downturn in tech or healthcare industries could disproportionately affect young borrowers, triggering a wave of defaults.

Another critical indicator is the federal policy landscape. Changes in loan forgiveness programs, interest rates, or repayment plans can either stabilize or destabilize the market. The Biden administration’s recent loan forgiveness initiatives, though limited, have provided temporary relief. However, legal challenges and political volatility threaten their longevity. If these programs expire without a sustainable alternative, millions of borrowers could face renewed financial strain. Additionally, the Federal Reserve’s interest rate hikes increase the cost of variable-rate loans, pushing more borrowers toward delinquency. Policymakers must tread carefully; abrupt changes could accelerate a crash, while strategic interventions might delay it.

Finally, the broader economic context cannot be ignored. A recession, characterized by declining GDP and consumer spending, would amplify the student loan crisis. During recessions, job opportunities shrink, wages stagnate, and borrowers default en masse. The 2020 pandemic recession temporarily paused loan payments, but such measures are unsustainable. If another recession hits, the student loan market could reach a tipping point. Investors and policymakers should watch leading indicators like consumer confidence and manufacturing activity. A downturn in these areas signals economic contraction, increasing the likelihood of a student loan crash. Proactive measures, such as income-driven repayment plans or expanded forgiveness programs, could mitigate risk, but timing is critical.

Does Wells Fargo Offer Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Government Policies Impacting Loans

Government policies have long been the invisible hand steering the student loan market, often determining its stability or vulnerability to collapse. One critical policy lever is interest rate regulation. When governments set artificially low interest rates on student loans, as seen in the U.S. with subsidized federal loans, borrowers benefit from reduced repayment burdens. However, this can create a moral hazard, encouraging excessive borrowing and inflating tuition costs as institutions capitalize on readily available funds. Conversely, high interest rates, like those on unsubsidized private loans, can lead to skyrocketing debt, increasing the likelihood of defaults and systemic strain. Striking the right balance is essential, but political and economic pressures often skew this equilibrium, setting the stage for potential market instability.

Another policy area with profound implications is loan forgiveness programs. Initiatives like the U.S. Public Service Loan Forgiveness (PSLF) program aim to alleviate debt for borrowers in public service roles. While well-intentioned, these programs can inadvertently incentivize borrowers to accumulate larger debts, assuming future forgiveness. Moreover, their implementation often suffers from bureaucratic inefficiencies, leaving many eligible borrowers unable to access relief. This mismatch between promise and delivery erodes trust in the system and exacerbates financial stress, contributing to the fragility of the loan market. Without robust oversight and reform, such programs may accelerate the conditions leading to a crash.

Income-driven repayment (IDR) plans represent a third policy tool with dual-edged effects. By capping monthly payments at a percentage of discretionary income, IDR plans provide immediate relief to struggling borrowers. However, they also extend repayment terms, often resulting in borrowers paying more over time due to accruing interest. This can create a debt trap, particularly for low-income earners, who may never fully repay their loans. While IDR plans reduce short-term default risks, they also mask underlying affordability issues, delaying the reckoning until the system reaches a breaking point. Policymakers must address the root causes of unaffordable education rather than relying on bandaid solutions like IDR.

Finally, the role of government in accrediting and regulating educational institutions cannot be overlooked. Lax accreditation standards allow low-quality, for-profit schools to proliferate, saddling students with debt for degrees that offer little economic value. The 2016 collapse of ITT Tech, a for-profit college chain, left thousands of students with worthless degrees and insurmountable debt, highlighting the systemic risks of inadequate oversight. Stronger regulations and accountability measures could prevent such institutions from exploiting the loan system, reducing the likelihood of a broader crash. However, political resistance from vested interests often hinders such reforms, leaving the market vulnerable to future shocks.

In sum, government policies wield immense power over the stability of the student loan market. Interest rate regulation, loan forgiveness programs, income-driven repayment plans, and accreditation standards each play a role in shaping borrower behavior and systemic risk. While these policies aim to support education access, their unintended consequences—moral hazard, bureaucratic inefficiencies, debt traps, and regulatory failures—can collectively push the system toward collapse. Addressing these issues requires a holistic approach, balancing borrower relief with market sustainability, to avert a crash and ensure the long-term viability of student financing.

Student Nurse Loans: Forgiveness Eligibility Explained for Aspiring Nurses

You may want to see also

Explore related products

![]()

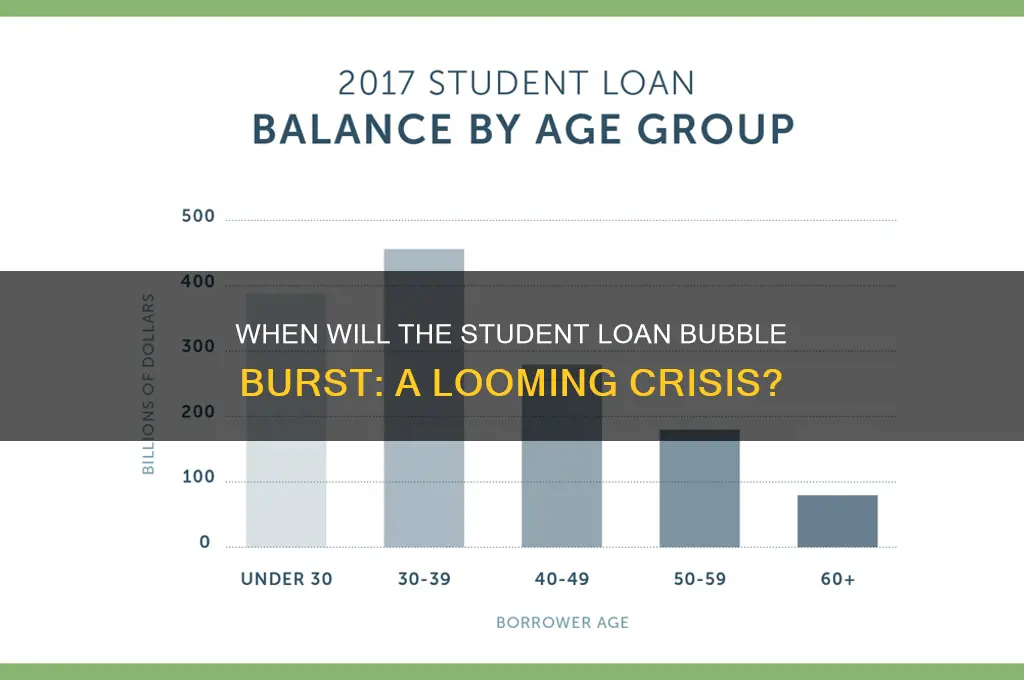

Student Debt Bubble Risks

The student debt bubble, now exceeding $1.7 trillion in the U.S., mirrors the housing crisis of 2008 in its potential for systemic collapse. Unlike mortgages, student loans are rarely dischargeable in bankruptcy, trapping borrowers in a cycle of debt. This rigidity amplifies the risk: as defaults rise, lenders face losses, and the government, which backs 92% of these loans, shoulders the burden. The question isn’t if the bubble will burst, but when—and what triggers it.

Consider the mechanics of this bubble. Tuition costs have outpaced inflation by 200% since the 1980s, fueled by easy access to federal loans. Colleges, knowing students can borrow unlimited amounts, raise prices without restraint. Meanwhile, wages for college graduates have stagnated, leaving borrowers with debt-to-income ratios that rival mortgage payments. For example, a borrower with $30,000 in debt and a $40,000 salary spends 25% of their income on payments—a level unsustainable in economic downturns.

The risks extend beyond individual borrowers. A collapse would ripple through the economy. Reduced consumer spending, delayed homeownership, and lower retirement savings are immediate consequences. For instance, a 2021 study found that student debt reduces homeownership rates by 15% among 25-35-year-olds. If defaults spike, lenders tighten credit, stifling economic growth. The government, already strained by pandemic spending, would face a bailout dilemma: forgive debt and inflame taxpayers, or let defaults spiral and cripple consumer confidence.

To mitigate personal risk, borrowers should prioritize high-interest debt and explore income-driven repayment plans. Refinancing with private lenders can lower rates but forfeits federal protections. For policymakers, capping loan amounts tied to expected earnings for specific degrees could curb reckless borrowing. Colleges must also be held accountable by linking federal funding to graduate employment rates. Without these measures, the bubble’s burst is inevitable—and its fallout will reshape education and finance for decades.

Will Biden Forgive Student Loans? Analyzing the Possibility and Impact

You may want to see also

Explore related products

![]()

Historical Loan Market Crashes

The student loan market, while not identical to housing or subprime lending, shares vulnerabilities with historical loan crashes. Consider the 2008 financial crisis. Securitization of subprime mortgages, bundled into complex financial instruments, created a house of cards. When defaults surged, the entire system collapsed. Student loans, increasingly securitized and held by both private lenders and the government, exhibit similar risk concentration. Over $1.7 trillion in outstanding student debt, much of it held by borrowers with limited income mobility, raises parallels to the subprime bubble.

History also warns of the dangers of unchecked lending growth. The savings and loan crisis of the 1980s saw deregulation and risky investments lead to widespread bank failures. Student lending, particularly in the for-profit college sector, mirrors this pattern. Aggressive recruitment tactics, inflated promises of job placement, and easy access to federal loans created a boom-and-bust cycle. Institutions like Corinthian Colleges and ITT Tech collapsed, leaving students with worthless degrees and insurmountable debt.

A comparative analysis reveals another red flag: income-driven repayment plans. While designed to provide relief, these plans often result in negative amortization, where interest accrues faster than payments. This echoes the "teaser rate" mortgages of the mid-2000s, which lured borrowers with low initial payments before resetting to unaffordable levels. For student loans, this means a growing portion of borrowers are effectively insolvent, unable to reduce their principal balance over decades.

To mitigate crash risks, policymakers must learn from past mistakes. First, transparency in loan terms and institutional outcomes is critical. Borrowers need clear information about graduation rates, default risks, and post-graduation earnings. Second, accountability measures for predatory lenders and low-quality institutions must be enforced. Finally, refinancing options and debt forgiveness programs, while politically contentious, could prevent a systemic collapse by addressing the underlying burden. Ignoring these lessons risks repeating history, with devastating consequences for borrowers and the broader economy.

Student Loan Freeze End Date: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Consequences for Borrowers & Economy

The student loan crisis has reached a tipping point, with over 45 million Americans collectively owing nearly $1.7 trillion. If this debt bubble bursts, the consequences will be far-reaching, impacting individual borrowers and the broader economy in profound ways. For borrowers, the immediate effects could include damaged credit scores, reduced access to future financing, and a significant decline in overall financial stability. A crash would likely trigger a wave of defaults, as millions of borrowers, already struggling under the weight of their loans, find themselves unable to meet their obligations. This scenario would not only devastate personal creditworthiness but also limit opportunities for homeownership, entrepreneurship, and other wealth-building activities.

From an economic perspective, a student loan crash could act as a catalyst for a broader financial downturn. Consumer spending, which drives about two-thirds of U.S. economic activity, would likely contract as borrowers redirect their income toward debt repayment or default. This reduction in spending could ripple through industries such as retail, housing, and automotive, leading to job losses and business closures. Additionally, the banking sector, which holds a significant portion of student loan debt, could face severe liquidity issues. If defaults surge, banks may tighten lending standards, further restricting credit availability and stifling economic growth.

To mitigate these risks, policymakers must consider targeted interventions. For instance, expanding income-driven repayment plans could provide immediate relief to borrowers, reducing the likelihood of widespread defaults. Similarly, implementing loan forgiveness programs for specific sectors or income brackets could alleviate financial pressure while stimulating economic activity. Borrowers, meanwhile, should proactively explore options like refinancing at lower interest rates or consolidating loans to manage their debt more effectively. Financial literacy programs could also empower individuals to make informed decisions about borrowing and repayment.

A comparative analysis of historical debt crises, such as the 2008 housing market collapse, reveals that swift and decisive action is critical to minimizing long-term damage. Just as the government intervened to stabilize the housing market, a similar approach may be necessary to prevent a student loan crash from derailing the economy. However, unlike the housing crisis, student debt is not backed by tangible assets, making it more challenging to address. This unique characteristic underscores the need for innovative solutions, such as public-private partnerships or alternative funding models for higher education, to prevent future crises.

In conclusion, the consequences of a student loan crash would be severe and multifaceted, affecting borrowers' financial futures and the overall health of the economy. By understanding these potential outcomes and taking proactive steps, both individuals and policymakers can work to avert disaster. For borrowers, this means staying informed and exploring all available options to manage debt. For the economy, it requires bold, forward-thinking policies that address the root causes of the crisis while providing immediate relief. The time to act is now, before the debt bubble bursts and the damage becomes irreversible.

Candidates Pushing for Student Loan Forgiveness: Who Supports Debt Relief?

You may want to see also

Frequently asked questions

It’s impossible to predict an exact date for a student loan market crash, as it depends on economic factors like unemployment rates, government policies, and borrower defaults.

A crash could be triggered by widespread borrower defaults, economic recession, changes in government loan forgiveness policies, or a collapse in higher education enrollment.

No, the impact would vary based on loan type (federal vs. private), repayment status, and individual financial situations. Federal loan borrowers might have more protections.

Stay informed about policy changes, explore repayment or forgiveness programs, build an emergency fund, and reduce other debts to improve financial stability.

Unlikely. While some borrowers might benefit from forgiveness programs, a crash would more likely lead to policy changes, restructuring, or increased financial strain rather than complete debt erasure.