The student loan freeze, implemented as a financial relief measure during the COVID-19 pandemic, has been a critical lifeline for millions of borrowers, temporarily pausing payments, interest accrual, and collections. However, as the economic landscape evolves, borrowers are increasingly asking: *When will the student loan freeze end?* The answer hinges on government decisions, with extensions already granted multiple times since the initial freeze in March 2020. As of now, the freeze is set to expire on a specific date, but policymakers continue to weigh factors such as inflation, unemployment rates, and broader economic recovery before making a final announcement. Borrowers are advised to stay informed and prepare for the resumption of payments, as the end of the freeze will likely bring significant changes to their financial obligations.

| Characteristics | Values |

|---|---|

| Current Status | The student loan payment freeze ended on October 1, 2023. |

| Duration of Freeze | The freeze was in place for over three years due to the COVID-19 pandemic and legal battles over student loan forgiveness. |

| Reason for Freeze | Initially implemented as part of COVID-19 relief measures, later extended due to legal challenges to the Biden administration's loan forgiveness plan. |

| Interest Accrual During Freeze | Interest did not accrue on eligible federal student loans during the freeze period. |

| Next Steps for Borrowers | Borrowers must resume payments starting October 2023. New repayment plans and forgiveness programs may be available. |

| Loan Forgiveness Updates | The Biden administration's broad loan forgiveness plan was blocked by the Supreme Court in June 2023. Targeted forgiveness programs remain in effect. |

| Resources for Borrowers | Borrowers can visit studentaid.gov for updates on repayment options, forgiveness programs, and loan servicer information. |

Explore related products

What You'll Learn

![]()

Current Freeze End Date

The current student loan freeze, implemented as a relief measure during the COVID-19 pandemic, has been extended multiple times, leaving borrowers in a state of uncertainty. As of the latest update, the freeze is set to expire on December 31, 2022, unless further action is taken by the federal government. This date marks the end of the pause on federal student loan payments, interest accrual, and collections, a policy that has provided financial breathing room for millions of Americans. However, with the deadline approaching, borrowers are advised to prepare for the resumption of payments to avoid potential financial strain.

Analyzing the implications of this end date, it’s clear that the transition back to regular payments will require careful planning. Borrowers should start by reviewing their loan balances, monthly payment amounts, and repayment plans. The Department of Education has encouraged individuals to update their contact information with their loan servicers to ensure they receive important notifications. Additionally, exploring options like income-driven repayment plans or loan consolidation could help manage payments more effectively once the freeze ends. Proactive steps taken now can mitigate the shock of resumed payments in January 2023.

From a persuasive standpoint, extending the freeze beyond December 31, 2022, could provide further relief to borrowers still recovering from the economic impacts of the pandemic. Advocacy groups argue that many individuals are not yet financially stable enough to resume payments, particularly with rising inflation and housing costs. However, policymakers must balance this need with the long-term sustainability of the student loan system. Borrowers should stay informed about potential legislative changes and consider reaching out to their representatives to voice their concerns.

Comparatively, the end of the student loan freeze contrasts sharply with other pandemic-era relief measures, such as stimulus checks and expanded unemployment benefits, which have already expired. This makes the freeze’s end date particularly significant, as it represents one of the last remaining financial safeguards for many Americans. Unlike other forms of debt, student loans cannot be discharged through bankruptcy, adding to the urgency of addressing this issue. Borrowers must prioritize understanding their options and taking action before the freeze lifts.

Practically speaking, here are actionable steps borrowers can take before December 31, 2022: log into your loan servicer’s website to confirm your payment due date and amount, set aside funds in a savings account to ease the transition, and explore refinancing options if you have private loans. For federal loan holders, consider enrolling in auto-pay to secure a small interest rate reduction. Finally, mark your calendar for early January to ensure your first payment is made on time. Preparation is key to avoiding delinquency and maintaining financial stability.

Can Native Americans Get Student Loan Forgiveness? Exploring Options

You may want to see also

Explore related products

![]()

Government Announcements on Extensions

The timing and nature of government announcements regarding student loan freeze extensions have historically been influenced by economic indicators, political priorities, and public pressure. For instance, during the COVID-19 pandemic, extensions were announced in response to widespread unemployment and financial hardship, with the U.S. Department of Education pausing federal student loan payments in March 2020 and extending the freeze multiple times since. These announcements typically come via official press releases, social media updates, or statements from key figures like the Secretary of Education, often just weeks or days before the current freeze is set to expire. Borrowers should monitor trusted sources such as the Federal Student Aid website or reputable financial news outlets to stay informed, as delays in announcements can create uncertainty and stress.

Analyzing past patterns reveals that extensions are frequently tied to broader economic relief measures. For example, the American Rescue Plan Act of 2021 included provisions that indirectly supported the continuation of the student loan freeze by addressing related financial burdens. Governments often frame these extensions as temporary solutions to immediate crises, yet they can also serve as political tools to garner public support. Borrowers should note that while extensions provide short-term relief, they do not typically reduce the principal balance or interest accrued, except in cases like the 0% interest rate applied during the pandemic freeze. Understanding this distinction is crucial for long-term financial planning.

To maximize the benefits of a freeze extension, borrowers should take proactive steps during the reprieve period. For federal loan holders, this could mean redirecting monthly payments toward high-interest private debt or building an emergency fund. For those in income-driven repayment plans, it’s an opportunity to recertify income or explore loan forgiveness programs like Public Service Loan Forgiveness (PSLF). Private loan borrowers, who are often excluded from government freezes, should negotiate with lenders for reduced interest rates or deferment options. A practical tip: use online calculators to estimate how different repayment strategies could impact your financial outlook post-freeze.

Comparatively, the communication strategies of different governments highlight varying levels of transparency and borrower support. In the U.K., for instance, the Student Loans Company provides clear timelines and eligibility criteria for repayment pauses, whereas U.S. announcements have sometimes been criticized for their last-minute nature and lack of long-term guidance. Borrowers in countries with less structured communication should advocate for clearer policies by engaging with student loan advocacy groups or contacting their representatives. Regardless of location, the key takeaway is that staying proactive and informed is essential, as extensions are rarely permanent solutions but rather temporary measures requiring strategic financial management.

ITT Tech Loan Forgiveness: A Step-by-Step Guide to Debt Relief

You may want to see also

Explore related products

![]()

Impact on Repayment Plans

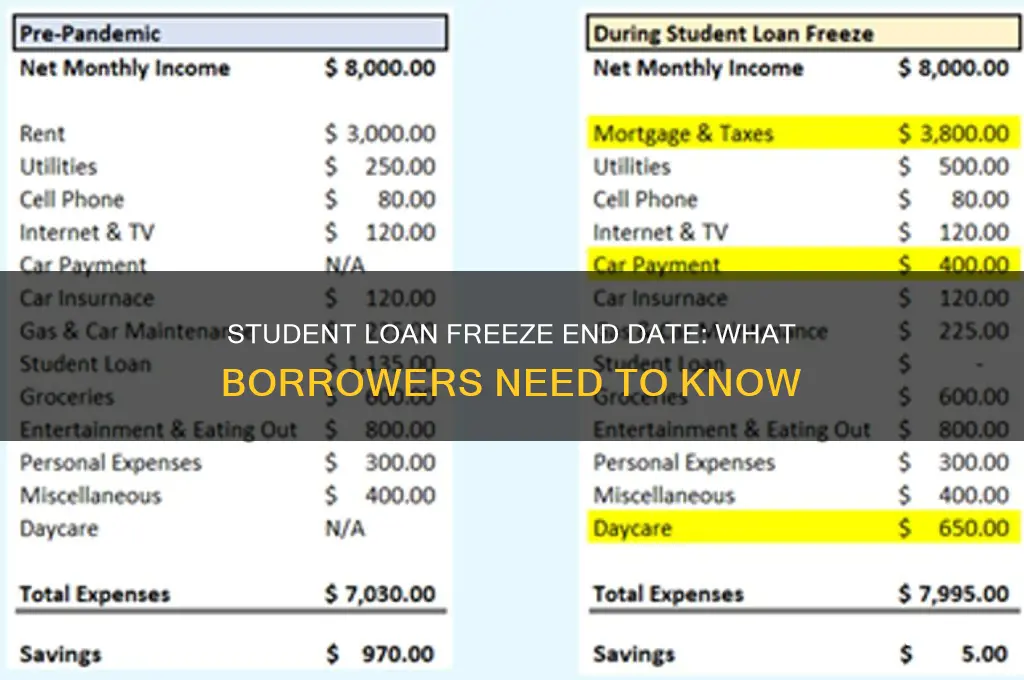

The end of the student loan freeze will force borrowers to reassess their repayment strategies, particularly those who have grown accustomed to the financial breathing room provided by the pause. For many, this means recalibrating budgets to accommodate monthly payments that may have been redirected to savings, debt reduction, or other expenses over the past few years. The sudden resumption of payments could strain household finances, especially for those with variable income or high-interest debt. Borrowers must act proactively by reviewing their current financial situation and exploring repayment options that align with their post-freeze reality.

Analyzing the impact on income-driven repayment (IDR) plans reveals a critical juncture for borrowers. During the freeze, many paused payments still counted toward IDR forgiveness timelines, effectively shortening the path to loan discharge. However, the end of the freeze may disrupt this progress, particularly if borrowers fail to recertify their income or update their plan details promptly. For example, a borrower earning $40,000 annually with $50,000 in loans could see their monthly payment jump from $0 to $200 under a standard plan, but an IDR plan might reduce it to $100 or less. The key takeaway? Borrowers on IDR plans must recertify their income immediately to avoid being switched to a less favorable repayment structure.

Persuasively, the freeze’s end underscores the importance of refinancing as a strategic tool for certain borrowers. Those with high credit scores (700+) and stable incomes may benefit from refinancing private loans at lower interest rates, potentially saving thousands over the loan term. For instance, refinancing a $30,000 loan from 7% to 4% could reduce monthly payments by $50 and save over $5,000 in interest. However, federal loan borrowers should proceed cautiously, as refinancing strips access to IDR plans and forgiveness programs. This option is best suited for those confident in their ability to repay without federal protections.

Comparatively, the freeze’s end highlights disparities in borrower preparedness. Younger borrowers (ages 22–30) may struggle more than older cohorts due to lower earnings and higher debt-to-income ratios. For example, a recent graduate with $35,000 in loans and an entry-level salary of $45,000 faces a steeper challenge than a mid-career professional with similar debt but a $70,000 income. Lenders and policymakers must address these inequities by offering targeted resources, such as financial literacy workshops or extended grace periods for recent graduates. Without such measures, the repayment restart risks exacerbating existing economic divides.

Descriptively, the transition period will be marked by confusion and stress for many borrowers. Servicers will be inundated with inquiries, potentially leading to delays in processing changes to repayment plans. Borrowers should anticipate this by logging into their accounts well before the freeze ends to update contact information, review payment due dates, and explore options like autopay (which often includes a 0.25% interest rate reduction). Practical tips include setting aside a "restart fund" equivalent to 2–3 months of expected payments and enrolling in servicer notifications to stay informed about deadlines. Proactive steps today can mitigate the chaos of tomorrow.

Are Navient Student Loans Forgivable? Exploring Options for Borrowers

You may want to see also

Explore related products

![]()

Economic Factors Influencing the Freeze

The student loan freeze, implemented as a temporary relief measure during the COVID-19 pandemic, has been extended multiple times, leaving borrowers and economists alike speculating about its end date. While political and social factors play a role, economic considerations are at the forefront of this decision-making process. One critical factor is the current inflation rate, which has been hovering around 8% in the United States as of 2023. High inflation erodes the purchasing power of borrowers, making it harder for them to resume payments without significant financial strain. For instance, a borrower earning $50,000 annually in 2019 would need to earn approximately $54,000 in 2023 just to maintain the same standard of living, assuming an average annual inflation rate of 3%. This economic reality pressures policymakers to extend the freeze until inflation stabilizes.

Another economic factor is the labor market’s recovery trajectory. While unemployment rates have dropped to pre-pandemic levels, job quality and wage growth remain uneven. Industries like hospitality and retail, which employ many recent graduates, have seen slower wage increases compared to tech or finance. A borrower working in hospitality might earn 10-15% less than their pre-pandemic peers, making it difficult to allocate funds for student loan payments. Policymakers must weigh the risk of resuming payments against the potential for widespread defaults, which could destabilize the financial system. For example, if 10% of the 45 million student loan borrowers default, it could result in a loss of $100 billion for lenders, triggering a ripple effect across the economy.

The national debt and budget deficit also influence the freeze’s timeline. As of 2023, the U.S. national debt exceeds $31 trillion, with the budget deficit projected to reach $1.4 trillion. Extending the student loan freeze costs the government approximately $5 billion per month in forgone revenue. While this is a small fraction of the overall budget, it adds to the fiscal burden, especially as lawmakers debate spending priorities. A persuasive argument for ending the freeze would be to redirect these funds toward infrastructure or healthcare, but this must be balanced against the economic hardship borrowers would face.

Lastly, the Federal Reserve’s monetary policy plays a subtle yet significant role. Rising interest rates, aimed at curbing inflation, increase the cost of borrowing across the economy, including for student loans. If the freeze ends while interest rates are high, borrowers with variable-rate loans could see their monthly payments increase by 20-30%. For example, a borrower with a $30,000 loan at a 5% interest rate might see their monthly payment rise from $318 to $400 if rates increase to 7%. This could exacerbate financial stress and reduce consumer spending, a key driver of economic growth. Policymakers must consider whether the economy can withstand such a shock.

In conclusion, the decision to end the student loan freeze is deeply intertwined with economic indicators like inflation, labor market health, fiscal constraints, and monetary policy. Each factor presents a unique challenge, requiring a delicate balance between fiscal responsibility and borrower welfare. As these economic conditions evolve, so too will the timeline for resuming student loan payments, making it essential for borrowers to stay informed and prepare for potential changes.

Denied Student Loan Forgiveness? Common Reasons and How to Appeal

You may want to see also

Explore related products

![]()

Post-Freeze Repayment Adjustments

The end of the student loan freeze will trigger a cascade of repayment adjustments, leaving borrowers navigating a complex financial landscape. This transition demands proactive planning and strategic decision-making to avoid pitfalls and optimize repayment terms.

Understanding your specific loan type is paramount. Federal loans, for instance, may offer income-driven repayment plans that cap monthly payments at a percentage of your discretionary income. These plans can provide crucial breathing room for borrowers facing financial strain post-freeze.

Assessing Your Financial Reality:

Before the freeze lifts, conduct a thorough financial audit. Calculate your monthly income, essential expenses, and discretionary spending. This realistic budget will reveal how much you can comfortably allocate towards loan repayment. Online budgeting tools and financial advisors can provide valuable guidance during this process.

Remember, overcommitting to repayments can lead to financial strain and potential default. Aim for a sustainable repayment plan that balances loan obligations with your overall financial well-being.

Exploring Repayment Options:

Don't settle for the standard repayment plan. Federal loans offer a variety of options tailored to different financial situations. Income-driven plans, as mentioned earlier, adjust payments based on your earnings. Graduated repayment plans start with lower payments that gradually increase over time, while extended repayment plans stretch the repayment period, lowering monthly payments but potentially increasing overall interest paid.

Proactive Communication is Key:

Don't wait until the last minute to contact your loan servicer. Reach out well before the freeze ends to discuss your options and understand any changes to your repayment terms. Be prepared to provide updated financial information and explore all available resources.

Building a Financial Cushion:

Anticipate potential financial bumps post-freeze. Aim to build a small emergency fund to cover unexpected expenses without derailing your repayment plan. Even a modest savings buffer can provide peace of mind and prevent reliance on high-interest debt.

Volunteering with BSA: Can It Help Forgive Your Student Loans?

You may want to see also

Frequently asked questions

The end date of the student loan freeze depends on government policies and announcements. As of the latest updates, borrowers should check official sources like the Department of Education or Federal Student Aid for the most accurate information.

Yes, student loan payments will typically resume the month following the end of the freeze. Borrowers should prepare to restart payments and consider updating their contact information with their loan servicers.

Some borrowers may receive a short grace period (e.g., 30 days) after the freeze ends to adjust to resuming payments. However, this depends on the specific terms announced by the government or loan servicers.

To prepare, update your contact information with your loan servicer, review your repayment plan, explore options like income-driven repayment, and set aside funds to resume payments. Stay informed about any policy changes or extensions.