The return of student loan payments has been a pressing concern for millions of borrowers since the pandemic-era pause on federal student loan payments began in March 2020. Initially intended as a temporary relief measure, the payment freeze has been extended multiple times, most recently until August 30, 2022, due to ongoing economic challenges and legal battles surrounding student debt forgiveness. As the deadline approaches, borrowers are anxiously awaiting clarity on when payments will resume, what changes to expect in repayment plans, and how the Biden administration’s proposed debt relief measures might impact their financial obligations. With the potential for widespread economic implications, the return of student loan payments remains a critical issue for both individual borrowers and the broader economy.

Explore related products

What You'll Learn

- Payment Restart Date: Official date when student loan payments are scheduled to resume after pause

- Interest Accrual: When interest will start accumulating on loans post-pause period

- Repayment Plan Options: Available plans for borrowers to manage payments effectively upon restart

- Relief Programs: Updates on forgiveness or relief programs affecting payment obligations

- Notification Process: How borrowers will be informed about payment resumption details

![]()

Payment Restart Date: Official date when student loan payments are scheduled to resume after pause

The Payment Restart Date is a critical milestone for millions of student loan borrowers, marking the end of the pandemic-related pause on federal student loan payments. As of the latest updates, the official date set for payments to resume is October 1, 2023. This date is not arbitrary; it follows a series of extensions since the initial pause began in March 2020. Borrowers should mark this date on their calendars and prepare financially, as interest will also begin accruing again after a long hiatus.

Analyzing the implications, the Payment Restart Date is more than just a deadline—it’s a call to action. Borrowers have had over three years of reprieve, during which they could redirect funds toward savings, debt repayment, or other financial goals. Now, they must reassess their budgets to accommodate monthly loan payments. For example, if a borrower was paying $300 monthly before the pause, they should ensure that amount is factored back into their expenses. Tools like budgeting apps or financial planners can help ease this transition.

From a practical standpoint, borrowers should take specific steps to prepare for the Payment Restart Date. First, verify your loan servicer and update your contact information to ensure you receive important notifications. Second, review your repayment plan options—if your financial situation has changed, you may qualify for income-driven repayment or other adjustments. Third, consider making a small payment before October 1 to reacquaint yourself with the process and avoid potential technical glitches on the platform.

Comparatively, the Payment Restart Date differs from previous pauses in its finality. While earlier extensions were tied to ongoing pandemic conditions, this date is tied to legislative action, specifically the expiration of the COVID-19 national emergency. This means borrowers should not expect another extension unless there is significant policy change. Unlike past pauses, this resumption also coincides with the rollout of new loan forgiveness programs, such as the SAVE Plan, which could alter repayment strategies for eligible borrowers.

In conclusion, the Payment Restart Date is a definitive turning point for student loan borrowers. It demands proactive planning, from budgeting adjustments to exploring new repayment options. By understanding this date’s significance and taking concrete steps, borrowers can navigate the transition smoothly and avoid financial strain. October 1, 2023, is not just a deadline—it’s an opportunity to regain control of your financial future.

Department of Education's Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Interest Accrual: When interest will start accumulating on loans post-pause period

Interest on student loans will resume its relentless march forward as soon as the payment pause ends. This means that for most federal student loan borrowers, interest will begin accruing again on September 1, 2023, with payments due starting in October. Understanding this timeline is crucial, as it directly impacts the total cost of your loan and your monthly payment obligations.

Mark your calendars: the interest-free grace period is ending.

The restart of interest accrual isn’t just a date to remember—it’s a call to action. Borrowers should use the remaining months of the pause to strategize. Consider making interest-only payments during this time to prevent capitalization, where unpaid interest is added to the principal balance. For example, if you have a $30,000 loan at 5% interest, paying just $125 monthly (the accrued interest) can save you hundreds in the long run. This proactive approach keeps your loan balance from ballooning when full payments resume.

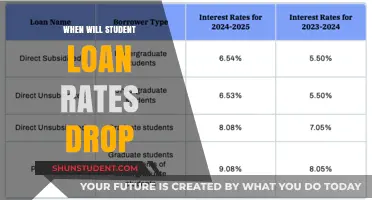

Not all loans are created equal when it comes to interest accrual. Subsidized federal loans, typically offered to undergraduate students with demonstrated financial need, do not accrue interest during the pause or while in school. Unsubsidized loans, however, accrue interest from the moment they are disbursed. Private loans follow their own rules, often starting interest accrual immediately, regardless of enrollment status. Knowing which type of loan you have is essential for planning. For instance, if you have unsubsidized or private loans, the pause’s end will hit harder, as interest has likely been building since day one.

The psychological impact of interest accrual can’t be overlooked. Seeing your loan balance grow due to compounding interest can feel demoralizing, especially if you’re already struggling financially. To combat this, focus on actionable steps: enroll in income-driven repayment plans, explore loan forgiveness programs, or refinance private loans at lower rates. For borrowers aged 22–35, who hold the majority of student debt, starting early with these strategies can significantly reduce long-term financial stress. Remember, interest accrual is a silent but powerful force—address it head-on before it snowballs.

Biden's Power to Veto Student Loan Forgiveness: Legal Limits Explained

You may want to see also

Explore related products

![]()

Repayment Plan Options: Available plans for borrowers to manage payments effectively upon restart

As student loan payments resume, borrowers face a critical decision: selecting a repayment plan that aligns with their financial situation. The federal government offers several options, each with distinct advantages and eligibility criteria. Understanding these plans is essential for managing debt effectively and avoiding default.

Income-Driven Repayment (IDR) Plans stand out for their flexibility. These plans—including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE)—cap monthly payments at a percentage of discretionary income, typically 10-20%. For instance, a borrower earning $40,000 annually with $30,000 in loans might pay as little as $200 monthly under REPAYE. After 20-25 years of consistent payments, any remaining balance is forgiven, though borrowers may owe taxes on the forgiven amount. Caution: IDR plans require annual recertification of income and family size, and lower payments may extend the loan term, increasing total interest paid.

Standard Repayment Plans offer simplicity and cost-effectiveness. Payments are fixed over a 10-year term, ensuring the loan is fully paid off within a decade. For example, a borrower with $30,000 in loans at 5% interest would pay approximately $318 monthly. This plan is ideal for those with stable, higher incomes seeking to minimize interest. However, the higher monthly payments may strain borrowers with limited cash flow.

Graduated and Extended Repayment Plans provide alternatives for borrowers needing lower initial payments. Graduated plans start with smaller payments that increase every two years, while Extended plans stretch repayment over 25 years, reducing monthly costs. For instance, a borrower with $40,000 in debt might pay $250 monthly under an Extended plan versus $400 under Standard. These options offer immediate relief but result in higher total interest paid. Borrowers should weigh short-term affordability against long-term costs.

Selecting the right repayment plan requires careful consideration of income, debt load, and financial goals. Tools like the Federal Student Aid Loan Simulator (studentaid.gov) can help borrowers compare plans and estimate monthly payments. Additionally, borrowers should explore options like Public Service Loan Forgiveness (PSLF) if they work in qualifying public service roles. Proactive planning and regular reviews of repayment strategies can ensure borrowers stay on track and avoid financial hardship when payments restart.

Who's Blocking Student Loan Forgiveness and Why It Matters

You may want to see also

Explore related products

![]()

Relief Programs: Updates on forgiveness or relief programs affecting payment obligations

The Biden administration's recent extension of the student loan payment pause through August 30, 2023, has provided temporary relief for millions of borrowers. However, as this deadline approaches, attention turns to the various relief programs that could further alleviate financial burdens. Among these, updates on forgiveness and relief initiatives are critical for borrowers navigating their repayment obligations.

One significant development is the expansion of the Public Service Loan Forgiveness (PSLF) program. Previously criticized for its complex requirements and low approval rates, recent reforms have made it more accessible. Borrowers now have until October 31, 2023, to consolidate their loans and receive credit for past payments, even if they were previously deemed ineligible. This one-time adjustment has already resulted in over $11 billion in forgiveness for 175,000 borrowers. For those in qualifying public service roles, this update could mean substantial savings and earlier debt-free status.

Another key initiative is the Fresh Start program, designed for borrowers in default. Launched in 2022, it allows defaulted borrowers to re-enter repayment in good standing, removing the default from their credit reports and restoring access to federal aid. This program is particularly impactful as it addresses the long-term consequences of default, such as wage garnishment and collection fees. Borrowers should take advantage of this opportunity before it expires, as it provides a rare chance to reset their financial standing.

Comparatively, the Income-Driven Repayment (IDR) Account Adjustment stands out as a broader relief measure. This initiative reviews past payments to ensure borrowers receive credit toward forgiveness, even if they were on the wrong plan or experienced servicing errors. For example, months spent in forbearance may now count toward the 20- or 25-year forgiveness threshold. This adjustment is automatic for most borrowers, but those with older loans should verify their payment counts through their servicer to maximize benefits.

While these programs offer substantial relief, borrowers must remain proactive. For instance, those pursuing PSLF should submit their employment certification form annually to ensure uninterrupted progress. Similarly, Fresh Start participants should enroll in an affordable repayment plan immediately to avoid reverting to default. Practical tips include setting up automatic payments to avoid missed deadlines and regularly monitoring loan balances through the Federal Student Aid website.

In conclusion, the landscape of student loan relief is evolving rapidly, with targeted programs addressing specific borrower needs. By staying informed and taking advantage of these updates, borrowers can significantly reduce their financial strain and move closer to achieving debt freedom.

How to Apply for Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Notification Process: How borrowers will be informed about payment resumption details

Borrowers awaiting news on student loan payment resumption will receive notifications through multiple channels, ensuring clarity and accessibility. The U.S. Department of Education, in collaboration with loan servicers, will employ a tiered communication strategy. Direct emails and physical mailers will be sent to all borrowers, detailing their specific payment restart date, monthly amount, and available repayment plans. These communications will also include a personalized link to the borrower’s online account for further details and resources. For those who prefer digital updates, text message alerts will provide concise reminders and deadlines, linking to more comprehensive information.

Analyzing past communication failures during payment pauses reveals the importance of redundancy in this process. In 2020, many borrowers missed critical updates due to outdated contact information or overlooked emails. To address this, servicers will cross-reference multiple databases to verify borrower details before sending notifications. Additionally, a dedicated hotline will be established for borrowers to confirm their information, ensuring no one is left in the dark. This multi-channel approach aims to minimize confusion and maximize engagement, particularly among borrowers who may have relocated or changed contact details during the payment pause.

Persuasively, the success of this notification process hinges on borrower action. Upon receiving their notice, borrowers must log into their accounts to review their repayment options, such as income-driven plans or temporary hardship forbearance. Proactive engagement is critical, as failure to update contact information or select a repayment plan could result in automatic enrollment in the standard plan, potentially leading to higher monthly payments. The Department of Education will emphasize this in all communications, using clear, action-oriented language to encourage borrowers to take immediate steps.

Comparatively, this notification process stands in stark contrast to the 2020 payment pause rollout, which was criticized for its lack of transparency and inconsistent messaging. This time, servicers will provide a step-by-step guide within each communication, outlining what borrowers need to do and by when. For instance, borrowers will be instructed to update their income information for income-driven plans at least 30 days before their payment restart date. This structured approach aims to reduce anxiety and provide a clear path forward, ensuring borrowers feel supported during the transition.

Descriptively, the notifications themselves will be designed with simplicity and urgency in mind. Emails will feature bold subject lines like “Action Required: Your Student Loan Payments Resume [Date],” while physical mailers will include a bright, eye-catching envelope to ensure they’re not mistaken for junk mail. Text alerts will be concise, stating, “Your student loan payments restart on [date]. Log in now to prepare: [link].” These design choices reflect an understanding of borrower behavior, prioritizing clarity and immediacy to drive engagement. By combining thoughtful design with actionable content, the notification process aims to leave no borrower unprepared for the resumption of payments.

When Can You Expect Your 10K Student Loan Forgiveness?

You may want to see also

Frequently asked questions

Student loan payments are set to resume in October 2023, following the end of the payment pause implemented during the COVID-19 pandemic.

As of now, there are no plans for another extension. The current pause is scheduled to end in September 2023, with payments restarting in October.

Review your loan details, update your contact information with your loan servicer, explore repayment plans, and consider setting aside funds to ease the transition when payments resume.

Yes, interest will resume accruing on most federal student loans starting in September 2023, when the payment pause ends.

Yes, you can explore loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness. Check eligibility and apply before payments resume to potentially reduce your balance.