Student loan borrowers are eagerly anticipating a potential drop in interest rates, a move that could significantly ease the financial burden of repayment. With the Federal Reserve’s recent shifts in monetary policy and ongoing economic fluctuations, there is growing speculation about when and by how much student loan rates might decrease. Historically, federal student loan interest rates are tied to the 10-year Treasury note yield, which has shown signs of decline in response to broader economic conditions. As borrowers await the annual rate reset, typically occurring in July, many are hopeful that lower rates will translate to reduced monthly payments and long-term savings, providing much-needed relief in an era of rising living costs.

| Characteristics | Values |

|---|---|

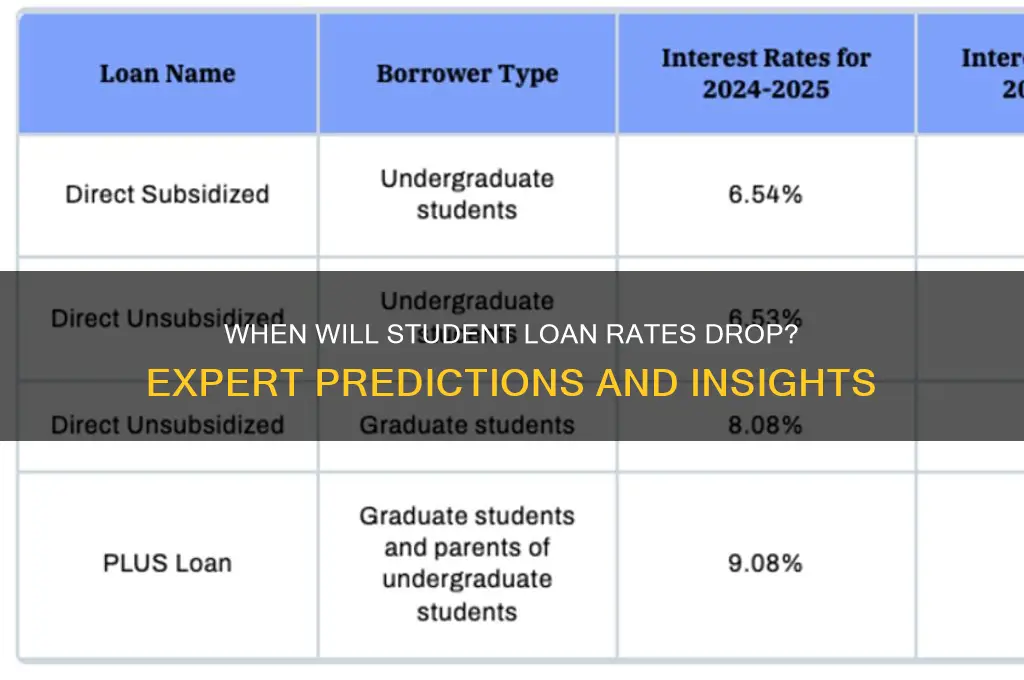

| Current Federal Student Loan Rates | 5.5% for undergraduate loans (2023-2024 academic year) |

| Next Federal Rate Adjustment | July 1, 2024 (rates are set annually based on May Treasury auctions) |

| Factors Influencing Rate Changes | 10-year Treasury note yield, federal legislation, economic conditions |

| Historical Trends | Rates have fluctuated; lowest in 2020-2021 (2.75%), highest in 2006 (6.8%) |

| Private Loan Rates | Variable (typically 4.5%–12%+ depending on credit and market conditions) |

| Potential Rate Drop Scenarios | Economic recession, federal policy changes, or Treasury yield decline |

| Payment Resumption Impact | Rates unlikely to drop immediately post-payment resumption (Oct 2023) |

| Refinancing Opportunities | Private refinancing may offer lower rates for eligible borrowers |

| Inflation Influence | High inflation may delay rate drops unless offset by policy changes |

| Expert Predictions | No significant drop expected in 2024 unless Treasury yields decrease sharply |

Explore related products

What You'll Learn

![]()

Federal Reserve Interest Rate Cuts

The Federal Reserve's interest rate decisions are a critical factor in determining when student loan rates might drop. When the Fed cuts its benchmark interest rate, it typically leads to lower borrowing costs across the economy, including for student loans. However, the relationship isn’t always direct, as student loan rates are influenced by both federal and private lending structures. For federal student loans, rates are set annually by Congress based on the 10-year Treasury note auction in May, plus a fixed markup. This means a Fed rate cut won’t immediately lower existing federal loan rates, but it could indirectly influence future rates if it drives down Treasury yields.

To understand the timeline, consider the Fed’s monetary policy actions. When the Fed cuts rates, it aims to stimulate economic activity by making borrowing cheaper. Historically, this has led to lower yields on Treasury bonds, which could reduce the cost of new federal student loans issued after the next May auction. For example, during the 2020 economic downturn, the Fed slashed rates to near zero, contributing to historically low Treasury yields and, subsequently, lower federal student loan rates for the 2020-2021 academic year. However, this effect isn’t immediate—borrowers with existing fixed-rate loans won’t see a change, and private loan rates may respond more quickly to market conditions.

If you’re a borrower awaiting lower rates, monitor the Fed’s announcements and economic indicators like inflation and unemployment. The Fed typically cuts rates during economic slowdowns or recessions, so periods of economic uncertainty could signal an opportunity for future rate reductions. For private student loans, refinancing is a practical strategy when rates drop. Compare offers from multiple lenders, and consider using a cosigner or improving your credit score to secure the lowest possible rate. Keep in mind that refinancing federal loans into private ones means losing access to income-driven repayment plans and loan forgiveness programs.

A cautionary note: while Fed rate cuts can create a favorable environment for lower student loan rates, they aren’t a guarantee. Federal loan rates are locked in for the life of the loan, so timing is crucial if you’re considering borrowing or refinancing. Additionally, private lenders may not pass on the full benefit of lower rates, so shop around for the best terms. Finally, stay informed about legislative changes—proposals to tie student loan rates more closely to market conditions or cap them could reshape the landscape entirely. By staying proactive and understanding these dynamics, you can position yourself to take advantage of rate drops when they occur.

When Will My Student Loan Be Disbursed? A Clear Timeline Guide

You may want to see also

Explore related products

![]()

Economic Recession Impact on Rates

Economic recessions often trigger a chain reaction in financial markets, and student loan rates are no exception. During a downturn, central banks typically lower interest rates to stimulate borrowing and spending. This monetary policy shift can directly influence the cost of student loans, particularly those tied to federal benchmarks like the 10-year Treasury note. For instance, during the 2008 recession, federal student loan rates dropped significantly as the Federal Reserve slashed its target rate to near zero. Borrowers with variable-rate loans saw immediate relief, while fixed-rate loans became more attractive for refinancing. Understanding this mechanism is crucial for predicting when rates might drop again.

However, the relationship between recession and student loan rates isn’t linear. While lower federal rates can reduce borrowing costs, private lenders may tighten credit standards during economic uncertainty, offsetting some benefits. For example, during the 2020 recession, federal student loan rates hit historic lows, but private lenders raised eligibility requirements and reduced loan limits. Borrowers with lower credit scores or unstable incomes found it harder to secure favorable terms, even as rates dropped. This highlights the importance of monitoring both macroeconomic trends and lender behavior during a recession.

Another critical factor is the government’s response to economic crises. In times of recession, policymakers often introduce stimulus measures to alleviate financial strain on households. For instance, the CARES Act of 2020 paused federal student loan payments and set interest rates to 0% for a limited time. Such interventions can provide immediate relief but are temporary and dependent on political will. Borrowers should stay informed about legislative proposals, such as the possibility of extended payment pauses or interest rate caps, which could signal further drops in student loan rates.

Practical steps can maximize the benefits of recession-driven rate drops. First, borrowers with variable-rate loans should monitor market indicators like the Federal Funds Rate and Treasury yields to anticipate changes. Second, those with fixed-rate loans should explore refinancing options when rates fall, but beware of origination fees that could negate savings. Finally, maintaining a strong credit profile and stable income improves access to the best terms, even during economic downturns. By combining awareness of economic trends with strategic action, borrowers can position themselves to capitalize on lower rates when they occur.

COVID-19 Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Legislative Changes in Loan Policies

Student loan interest rates are not set in stone; they are subject to legislative changes that can significantly impact borrowers. One of the most direct ways rates can drop is through federal legislation. For instance, the Bipartisan Student Loan Certainty Act of 2013 tied federal student loan rates to the 10-year Treasury note, creating a variable but market-aligned structure. This act demonstrated how policy shifts can directly influence borrowing costs, offering a precedent for future changes.

To advocate for lower rates, borrowers should track bills like the Student Loan Refinancing Act, which periodically resurfaces in Congress. This legislation aims to allow borrowers to refinance existing loans at current, lower rates, potentially saving thousands over the life of the loan. Practical steps include contacting representatives, signing petitions, and supporting organizations like the Student Borrower Protection Center, which push for such reforms. Remember, legislative change often requires sustained public pressure.

Comparatively, state-level initiatives also play a role. For example, Minnesota’s Refinance Authority allows residents to refinance both federal and private loans at lower rates, bypassing federal gridlock. While this doesn’t directly drop federal rates, it highlights how localized policies can provide relief. Borrowers in states without such programs can lobby for similar measures, using Minnesota’s model as a template.

A cautionary note: legislative changes often move slowly and are subject to political climates. For instance, the Public Service Loan Forgiveness (PSLF) program faced years of bureaucratic hurdles before recent reforms streamlined it. Borrowers should stay informed but also explore interim solutions like income-driven repayment plans, which cap payments at a percentage of income, indirectly mitigating rate impacts.

In conclusion, while federal and state legislative changes offer the most direct path to lowering student loan rates, they require proactive engagement. Track relevant bills, support advocacy groups, and explore existing programs like refinancing or PSLF. Combining these strategies maximizes the chance of benefiting from policy shifts when they occur.

Discover Eligible Fields for Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Inflation Trends and Loan Costs

The Federal Reserve's interest rate hikes since 2022 have directly influenced student loan rates, which are tied to the 10-year Treasury note. As inflation surged past 8% in mid-2022, the Fed responded aggressively, raising rates from near-zero to over 5% by mid-2023. This tightening cycle has pushed undergraduate federal loan rates to 5.5% for the 2023-2024 academic year, up from 3.73% in 2021-2022. Private loan rates, often variable and tied to the Prime Rate, have climbed even higher, averaging 10-12% for borrowers with fair credit. To mitigate costs, borrowers should prioritize refinancing high-interest private loans when inflation shows sustained decline, as this could signal a Fed pivot to rate cuts.

Historical inflation trends suggest a cyclical pattern: periods of high inflation (e.g., the 1980s and 2020s) are followed by corrective monetary policy, eventually easing borrowing costs. For instance, after peaking at 18.6% in 1980, inflation fell to 3.2% by 1983, prompting the Fed to lower rates and reduce loan costs. Similarly, if current inflation (3.4% as of April 2024) stabilizes near the Fed’s 2% target, student loan rates could drop in 2025-2026. Borrowers aged 25-34, who hold 40% of all student debt, should monitor the Consumer Price Index (CPI) monthly and prepare to refinance when the 10-year Treasury note falls below 3%, a likely precursor to lower federal and private rates.

A comparative analysis of inflation-adjusted loan costs reveals that real interest rates (nominal rate minus inflation) are currently punitive. For example, a 5.5% federal loan rate with 3.4% inflation yields a 2.1% real rate, higher than the 0.5% real rate seen in 2020. This erodes affordability, especially for low-income borrowers. To counteract this, consider income-driven repayment plans, which cap payments at 10-20% of discretionary income, or explore employer-sponsored repayment assistance programs. Additionally, locking in fixed-rate private loans during inflationary peaks can provide long-term savings if rates later decline.

Persuasively, policymakers must address the structural link between inflation and loan costs to prevent generational debt traps. For instance, indexing federal loan rates to inflation rather than Treasury yields could stabilize costs during economic volatility. Until such reforms, borrowers should adopt proactive strategies: avoid deferment (which accrues interest), pay above the minimum to reduce principal faster, and leverage tax deductions for up to $2,500 in annual student loan interest. By understanding inflation’s role in rate fluctuations, borrowers can time refinancing opportunities and minimize lifetime interest payments.

Will Student Loan Forgiveness Be Taxed? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Private Lender Competition Effects

The intensity of competition among private lenders directly influences student loan interest rates, creating a dynamic market where borrowers can benefit from strategic timing and informed decision-making. As traditional federal loan rates fluctuate, private lenders often adjust their offerings to attract a larger share of borrowers, especially those with strong credit profiles or cosigners. For instance, during periods of economic uncertainty, lenders may lower rates to maintain loan volumes, while in booming economies, they might increase rates to maximize profits. Understanding these patterns allows borrowers to anticipate when private loan rates might drop, positioning them to secure more favorable terms.

To leverage private lender competition effectively, borrowers should monitor market trends and compare offers from multiple lenders. Tools like loan comparison platforms and rate-tracking websites can provide real-time insights into prevailing rates and promotional offers. For example, lenders often introduce limited-time rate discounts or cashback incentives to outpace competitors. Borrowers who time their applications to coincide with these promotions can save significantly over the life of their loans. Additionally, maintaining a high credit score or securing a creditworthy cosigner can further enhance negotiating power, as lenders compete more aggressively for low-risk borrowers.

A cautionary note: while private lender competition can drive rates down, it also introduces variability and risk. Unlike federal loans, private loans typically lack income-driven repayment plans or forgiveness options, making them less flexible in times of financial hardship. Borrowers should carefully assess their long-term financial stability before opting for private loans, even if rates appear attractive. A practical tip is to prioritize federal loans first, exhausting all available options before turning to private lenders. This ensures access to borrower protections while still allowing for strategic use of private loans when rates are favorable.

Finally, the ripple effects of private lender competition extend beyond individual borrowers, shaping the broader student loan landscape. As lenders vie for market share, they may innovate with products like variable-rate loans tied to economic indices or loyalty programs offering rate reductions for timely payments. Borrowers who stay informed about these developments can capitalize on emerging opportunities. For instance, a borrower with a variable-rate loan might benefit from a dropping prime rate, while another might earn rate reductions through consistent on-time payments. By understanding and engaging with these competitive dynamics, borrowers can navigate the student loan market more effectively, turning private lender competition into a tool for financial advantage.

How $1,500 in Student Loan Interest Impacts Your Tax Return

You may want to see also

Frequently asked questions

Student loan rates are tied to the 10-year Treasury note and are set annually by Congress. Rates typically adjust each May based on market conditions. A drop in rates depends on economic factors like inflation, Federal Reserve policies, and government decisions. There is no guaranteed timeline, but rates may decrease if the economy stabilizes or interest rates decline.

A: The government can implement policies to lower interest rates for existing loans, but this is rare and depends on legislative action. Historically, rate reductions have been applied to new loans rather than retroactively. Borrowers should monitor federal announcements and consider refinancing options if rates drop.

A: Stay informed about economic trends and federal student loan policies. Consider refinancing private loans if rates drop, but be cautious with federal loans, as refinancing them into private loans may result in losing federal benefits. Additionally, explore income-driven repayment plans or loan forgiveness programs to manage payments effectively.