The highly anticipated student loan forgiveness case is set to reach the Supreme Court, with millions of borrowers eagerly awaiting a decision that could significantly impact their financial futures. The case, which challenges the Biden administration's plan to cancel up to $20,000 in student debt for eligible borrowers, has sparked intense debate and legal battles. As the highest court in the land prepares to hear oral arguments, the question on everyone's mind is: when will the Supreme Court finally address this pivotal case? With the fate of student loan forgiveness hanging in the balance, borrowers, advocates, and policymakers alike are closely monitoring the court's schedule, anticipating a hearing date that could bring much-needed clarity and resolution to this contentious issue.

| Characteristics | Values |

|---|---|

| Case Name | Biden v. Nebraska and Department of Education v. Brown |

| Hearing Date | February 28, 2023 |

| Decision Date | June 30, 2023 |

| Outcome | The Supreme Court ruled 6-3 against the Biden administration's student loan forgiveness program, deeming it unconstitutional. |

| Key Issue | Whether the Biden administration had the authority to cancel up to $20,000 in student loan debt per borrower under the HEROES Act. |

| Majority Opinion | Written by Chief Justice John Roberts, joined by Justices Alito, Thomas, Gorsuch, Kavanaugh, and Coney Barrett. |

| Dissenting Opinion | Written by Justice Elena Kagan, joined by Justices Sotomayor and Jackson. |

| Impact | The ruling blocked the forgiveness of approximately $430 billion in student loan debt for over 40 million borrowers. |

| Current Status | The program remains halted, and borrowers are required to resume payments starting in October 2023. |

| Alternative Relief | The Biden administration has proposed alternative measures, such as income-driven repayment plans and targeted debt relief for specific groups. |

Explore related products

What You'll Learn

![]()

Case Timeline Overview

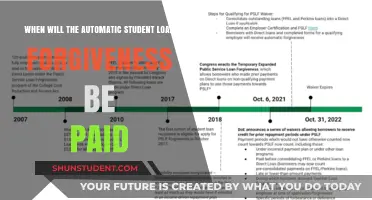

The Supreme Court's involvement in the student loan forgiveness case began in earnest in February 2022, when the Biden administration announced its plan to cancel up to $20,000 in federal student loan debt for eligible borrowers. This initiative, aimed at providing financial relief to millions of Americans, quickly became a focal point of legal and political debate. The case timeline is marked by a series of strategic legal challenges, appeals, and procedural milestones that have shaped its trajectory toward the nation’s highest court. Understanding this timeline is crucial for borrowers and observers alike, as it clarifies when and how the Supreme Court’s decision might impact student loan forgiveness.

The first significant step occurred in October 2022, when six Republican-led states filed a lawsuit in Missouri, arguing that the debt relief program overstepped executive authority and violated the Administrative Procedure Act. This challenge was swiftly followed by another lawsuit from two individual borrowers in Texas, who claimed they were unfairly excluded from the program. These cases highlighted the program’s vulnerabilities to legal scrutiny and set the stage for expedited appeals. By November 2022, the Supreme Court had already intervened, declining to lift a lower court’s injunction blocking the program but agreeing to hear oral arguments in February 2023. This decision underscored the urgency and complexity of the issue, as millions of borrowers awaited clarity on their financial futures.

The oral arguments, held on February 28, 2023, were a pivotal moment in the case timeline. Justices probed the legal basis for the debt relief program, questioning its scope, authority, and potential economic implications. Observers noted sharp divisions among the justices, with conservative members expressing skepticism about the program’s legality and their liberal counterparts emphasizing the executive branch’s authority during national emergencies. This exchange provided critical insights into the Court’s likely reasoning and foreshadowed a decision that could have far-reaching consequences for both borrowers and the Biden administration.

Following the oral arguments, the Court’s typical timeline for issuing a decision came into focus. Historically, the Supreme Court delivers opinions on argued cases by the end of its term in late June or early July. For the student loan forgiveness case, this meant a decision was expected by June 2023. However, the Court’s workload and the case’s complexity introduced uncertainty, leaving borrowers in a state of limbo. Practical tips for borrowers during this waiting period included staying informed through official channels, avoiding scams promising immediate debt relief, and preparing financially for potential outcomes, such as resumed payments if the program were struck down.

In conclusion, the case timeline overview reveals a meticulously orchestrated legal journey, from initial challenges to Supreme Court intervention. Each step has been marked by strategic maneuvers, procedural rigor, and high-stakes implications. For borrowers, understanding this timeline is not just about tracking dates but about navigating uncertainty with informed preparedness. As the nation awaits the Supreme Court’s decision, the timeline serves as a reminder of the intricate balance between executive action, judicial review, and the lives of millions affected by student loan debt.

Do You Qualify for Federal Student Loan Forgiveness? Find Out Now

You may want to see also

Explore related products

![]()

Legal Arguments Summary

The Supreme Court's decision to hear the student loan forgiveness case hinges on critical legal arguments centered around constitutional authority, statutory interpretation, and separation of powers. At the heart of the debate is whether the Biden administration overstepped its bounds under the Higher Education Relief Opportunities for Students (HEROES) Act of 2003. Proponents argue that the Act grants the Secretary of Education broad discretion to modify student loans during national emergencies, such as the COVID-19 pandemic. They contend that forgiving up to $20,000 in debt per borrower falls within this authority, as it provides necessary relief to millions of Americans burdened by educational debt.

Opponents, however, challenge this interpretation, asserting that the HEROES Act does not authorize such sweeping debt cancellation. They argue that the administration’s action constitutes an unlawful exercise of power, bypassing congressional approval and violating the Appropriations Clause of the Constitution. This clause requires that public funds be spent only as authorized by Congress, and critics claim that forgiving trillions in debt without explicit legislative approval undermines this principle. The legal question thus becomes whether the executive branch can unilaterally implement such a significant policy change.

Another key argument revolves around standing—whether the plaintiffs challenging the policy have a legal right to sue. States like Texas and Missouri, along with other challengers, argue that the debt forgiveness harms them by reducing revenue from student loan servicers or violating administrative procedures. However, the administration counters that these claims are speculative and insufficient to establish standing. The Court’s decision on standing will determine whether the case proceeds or is dismissed, shaping the future of student loan policy.

Practically, borrowers should monitor these arguments closely, as the Court’s ruling will directly impact their financial obligations. If the policy is upheld, eligible borrowers with incomes below $125,000 (or $250,000 for married couples) could see significant debt reduction. Conversely, a ruling against the administration would likely reinstate payments and interest accrual, potentially exacerbating financial strain. Borrowers should prepare by reviewing their loan balances, exploring alternative repayment plans, and staying informed through official channels like the Department of Education’s website.

In conclusion, the legal arguments in this case are complex and far-reaching, with implications for executive power, constitutional law, and millions of Americans’ financial futures. The Supreme Court’s decision will not only resolve a contentious policy dispute but also set precedents for the limits of administrative authority in addressing national crises. Borrowers, policymakers, and legal scholars alike await the ruling, which will shape the intersection of law and economic relief for years to come.

Forgiving All Student Loans: Economic Impact, Social Justice, and Future Implications

You may want to see also

Explore related products

$15.3 $18

![]()

Key Parties Involved

The Supreme Court's decision to hear the student loan forgiveness case hinges on the actions and interests of several key parties, each with distinct stakes and strategies. At the forefront are the Biden administration and the Department of Education, who championed the loan forgiveness program under the HEROES Act, aiming to alleviate financial burdens for millions of borrowers. Their legal team must navigate constitutional and statutory arguments to defend the program's legality. Conversely, six Republican-led states (Arkansas, Iowa, Kansas, Missouri, Nebraska, and South Carolina) have challenged the initiative, arguing it oversteps executive authority and harms state-based loan servicers. Their success could dismantle the program, setting a precedent for limiting federal power.

Borrowers themselves form a critical yet often voiceless party. Representing over 40 million individuals, their collective interest lies in debt relief, but their direct involvement in the case is limited. Advocacy groups like the Student Borrower Protection Center and American Federation of Teachers have stepped in to amplify their concerns, filing amicus briefs and mobilizing public support. These groups highlight the economic and social benefits of forgiveness, framing it as a matter of equity and opportunity.

The Supreme Court justices play a pivotal role, with their ideological leanings likely shaping the outcome. Conservative justices may scrutinize the program’s scope and constitutionality, while liberal justices could emphasize its public interest. The Court’s decision will not only determine the fate of the program but also clarify the boundaries of executive action in times of national emergency.

Finally, loan servicers and financial institutions have a vested interest, though their involvement is indirect. State-affiliated servicers, as argued by the plaintiff states, claim financial harm from reduced loan volumes. Private lenders, meanwhile, may benefit from the program’s failure, as borrowers revert to traditional repayment plans. Understanding these dynamics reveals the case’s broader implications for the student loan industry and federal policy.

In sum, the case is a high-stakes clash of interests, with each party’s actions and arguments shaping the future of student loan forgiveness. Borrowers, states, the administration, and the Court are locked in a battle that transcends legal technicalities, touching on fundamental questions of power, equity, and economic policy.

Federal Employees and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Potential Outcomes Impact

The Supreme Court’s decision on the student loan forgiveness case could reshape the financial landscape for millions of borrowers, with ripple effects across the economy. If the Court upholds the forgiveness program, an estimated 40 million borrowers could see up to $20,000 in debt relief, significantly reducing their monthly obligations. This would free up disposable income, potentially boosting consumer spending in sectors like housing, retail, and education. Conversely, a ruling against forgiveness could leave borrowers with unchanged debt burdens, increasing the risk of defaults and delinquencies, which could strain credit markets and dampen economic growth.

Consider the psychological impact of these outcomes. For borrowers, debt forgiveness would alleviate long-term financial stress, improving mental health and overall well-being. Studies show that high debt levels correlate with anxiety and depression, particularly among younger adults. A favorable ruling could empower borrowers to pursue career changes, start businesses, or invest in their futures without the weight of student loans. Conversely, a rejection of the program might deepen feelings of financial insecurity, delaying major life milestones like homeownership or starting a family.

From a policy perspective, the Court’s decision will set a precedent for executive authority in financial relief programs. If the forgiveness plan is upheld, it could embolden future administrations to use similar measures to address economic crises. However, a ruling against it might limit the government’s ability to act swiftly in emergencies, potentially leaving vulnerable populations without critical support. This outcome would also reignite debates about the role of Congress in authorizing large-scale debt relief, shifting the focus back to legislative solutions.

Practical tips for borrowers awaiting the decision include preparing for both scenarios. Those anticipating forgiveness should avoid making extra payments until the ruling is final, as forgiven amounts could be refunded. Conversely, borrowers should budget for resumed payments if the program is struck down, exploring options like income-driven repayment plans or refinancing at lower interest rates. Staying informed through official channels, such as the Department of Education, is crucial to avoid scams targeting uncertain borrowers.

Finally, the broader societal impact cannot be overlooked. Debt forgiveness could reduce wealth inequality, particularly for Black and Latino borrowers, who disproportionately carry higher student loan burdens. This could narrow racial wealth gaps and foster greater economic mobility. Conversely, a rejection of the program might exacerbate existing inequalities, perpetuating cycles of debt and limiting opportunities for marginalized communities. The Court’s decision will not only affect individual borrowers but also shape the nation’s approach to education financing and economic equity for years to come.

Can SSDI Recipients Get Student Loan Forgiveness? Key Facts Explained

You may want to see also

Explore related products

![]()

Public Reaction Updates

The public’s anticipation surrounding the Supreme Court’s hearing of the student loan forgiveness case has sparked a wave of reactions across social media, news outlets, and community forums. From fervent debates to organized advocacy, the discourse reflects a deeply divided yet highly engaged populace. Proponents of loan forgiveness highlight the economic relief it would provide to millions, while critics argue it oversteps executive authority and burdens taxpayers. This polarization has fueled a surge in petitions, hashtags, and grassroots campaigns, each vying for attention and influence ahead of the Court’s decision.

Analyzing the tone of public reactions reveals a striking generational divide. Younger demographics, particularly those aged 18–35, dominate online conversations with hashtags like #CancelStudentDebt, emphasizing the moral imperative of alleviating financial strain. In contrast, older generations often express skepticism, framing the issue as a matter of fiscal responsibility and fairness to those who repaid loans without assistance. This age-based split underscores broader societal tensions around economic equity and the role of government intervention.

Practical tips for staying informed and engaged include following trusted legal analysts on platforms like Twitter or subscribing to newsletters from organizations like the Student Borrower Protection Center. For those directly affected, tracking updates through the Department of Education’s Federal Student Aid website ensures access to accurate, actionable information. Engaging in local town halls or virtual forums can also amplify individual voices and foster collective action, turning passive concern into active advocacy.

Comparatively, the public reaction to this case mirrors responses to other landmark Supreme Court hearings, such as those on healthcare or voting rights. The intensity of engagement reflects the issue’s direct impact on millions of lives, with personal stories often taking center stage. For instance, viral testimonials from borrowers detailing the crippling effects of debt have humanized the debate, swaying public opinion in favor of forgiveness. Conversely, counter-narratives emphasizing personal responsibility and the rule of law have resonated with those wary of expansive executive power.

In conclusion, the public reaction to the Supreme Court’s impending hearing on student loan forgiveness is a dynamic, multifaceted phenomenon. By understanding its nuances—generational divides, practical engagement strategies, and historical parallels—individuals can navigate the discourse more effectively. Whether advocating for change or critiquing its implications, staying informed and actively participating ensures that the public’s voice remains a driving force in this pivotal moment.

Will Graduated Payment Student Loans Qualify for Loan Forgiveness?

You may want to see also

Frequently asked questions

The Supreme Court heard oral arguments in the student loan forgiveness case on February 28, 2023.

The case challenges the Biden administration's plan to forgive up to $20,000 in federal student loan debt for eligible borrowers under the Higher Education Relief Opportunities for Students (HEROES) Act.

The Supreme Court typically issues decisions by the end of its term in late June or early July, so a ruling is expected by then.

The program is being challenged by several Republican-led states and conservative groups, who argue that the administration overstepped its authority in implementing the forgiveness plan.

Student loan payments were set to resume 60 days after the case is resolved or by June 30, 2023, whichever comes first, but this timeline may change based on the Court’s decision.

![GolbinBox Magnetic for iPhone 13 Case & iPhone 14 Case, Compatible with MagSafe, [Soft Anti-Scratch Microfiber Lining], Slim Liquid Silicone Shockproof Protective Phone Case 6.1 inch, Chalk Pink](https://m.media-amazon.com/images/I/71g7XAqc5XL._AC_UY218_.jpg)

![Miracase Magnetic for iPhone 15 Pro Max Case 6.7'' [Compatible with Magsafe] Full-Body Drop Proof Bumper Phone Case for iPhone 15 Pro Max with Built-in 9H Tempered Glass Screen Protector,Black](https://m.media-amazon.com/images/I/714xw16BTrL._AC_UY218_.jpg)

![The Case for Christ [DVD]](https://m.media-amazon.com/images/I/91y-W9Vz4HL._AC_UY218_.jpg)

![Spigen for iPhone 17 Pro Max Case, Ultra Hybrid MagFit [TPU Covered Camera Control] [Anti-Yellowing] [Compatible with Magsafe] - Frost Black](https://m.media-amazon.com/images/I/61zbspkFCJL._AC_UY218_.jpg)