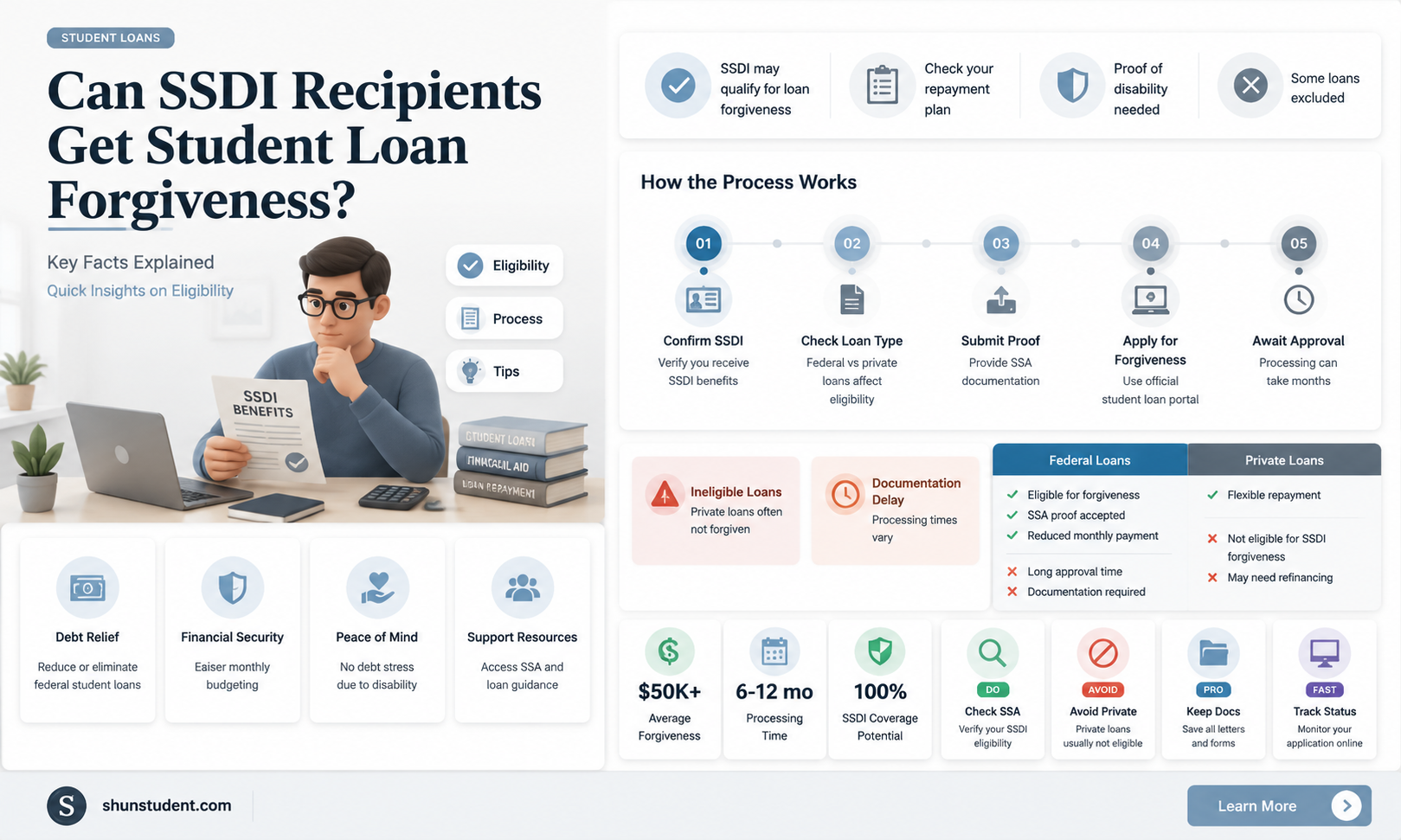

Many individuals on Social Security Disability Insurance (SSDI) wonder if their student loans can be forgiven due to their disability status. The good news is that the Total and Permanent Disability (TPD) discharge program offers federal student loan forgiveness for borrowers who are unable to work due to a permanent disability. To qualify, SSDI recipients must provide documentation from the Social Security Administration (SSA) confirming their eligibility for disability benefits. Additionally, private student loans may have different policies, often requiring separate applications or proof of disability. Understanding these options can provide significant financial relief for those facing long-term disabilities.

| Characteristics | Values |

|---|---|

| Eligibility for Student Loan Forgiveness | Individuals receiving Social Security Disability Insurance (SSDI) benefits may qualify for Total and Permanent Disability (TPD) discharge of federal student loans. |

| Application Process | Borrowers must submit an application for TPD discharge, providing documentation of their SSDI eligibility. |

| Documentation Required | Proof of SSDI benefits, such as a Notice of Award from the Social Security Administration (SSA). |

| Loan Types Eligible | Federal student loans, including Direct Loans, FFEL Program loans, and Perkins Loans. |

| Private Loans | Private student loans are not eligible for TPD discharge based on SSDI eligibility. |

| Monitoring Period | After approval, a 3-year monitoring period begins, during which the borrower must not earn above the poverty guideline or receive a new federal student loan. |

| Tax Implications | Forgiven amounts may be considered taxable income, though exceptions apply under the American Rescue Plan Act through 2025. |

| Reinstatement of Loans | If the monitoring period requirements are violated, loans may be reinstated. |

| Frequency of Review | No periodic reviews after the 3-year monitoring period ends. |

| Impact on Credit Score | TPD discharge is reported to credit bureaus but does not negatively impact credit score. |

| Appeal Process | Borrowers can appeal denials by providing additional evidence of eligibility. |

| Recent Updates | Streamlined processes for SSDI recipients to apply for TPD discharge, reducing paperwork. |

Explore related products

What You'll Learn

![]()

SSDI and Loan Discharge Eligibility

Receiving Social Security Disability Insurance (SSDI) benefits can be a crucial lifeline for individuals unable to work due to a disability. However, the financial burden of student loans often persists, raising the question: can these loans be discharged for SSDI recipients? The answer lies in understanding the specific eligibility criteria and application process for Total and Permanent Disability (TPD) discharge.

Here's a breakdown:

Qualifying for TPD Discharge: The Department of Education offers TPD discharge for federal student loans, including Direct Loans, Perkins Loans, and FFEL Loans. To qualify, you must provide documentation proving your total and permanent disability. This typically involves submitting a physician's certification or a notice of award for SSDI benefits. Importantly, simply receiving SSDI doesn't automatically guarantee TPD discharge. The Social Security Administration's (SSA) definition of disability for SSDI purposes may differ slightly from the Department of Education's criteria for TPD.

The Application Process: Applying for TPD discharge involves submitting an application to the Department of Education's TPD Servicer. This application requires detailed information about your disability, including medical documentation or your SSA notice of award. The process can be lengthy, so starting early and gathering all necessary documentation is crucial.

Post-Discharge Monitoring: Even after a successful TPD discharge, borrowers enter a three-year monitoring period. During this time, you must meet certain conditions, such as not earning above the poverty line and not receiving a new federal student loan. Failure to comply with these conditions can result in loan reinstatement.

Private Loans and State Variations: It's important to note that TPD discharge only applies to federal student loans. Private student loans are not eligible for this program. Additionally, some states offer their own loan forgiveness programs for individuals with disabilities, so exploring state-specific options is recommended.

VA Student Loan Forgiveness: What Veterans Need to Know

You may want to see also

Explore related products

![]()

Total and Permanent Disability Verification

For individuals receiving Social Security Disability Insurance (SSDI), the prospect of student loan forgiveness hinges on a critical process: Total and Permanent Disability (TPD) verification. This isn’t automatic; borrowers must actively apply and provide evidence of their eligibility. The U.S. Department of Education requires documentation from the Social Security Administration (SSA) confirming that the borrower’s disability is expected to last continuously for at least 60 months or result in death. Once approved, federal student loans—including Direct Loans, Perkins Loans, and FFEL Program loans—are discharged, freeing the borrower from repayment obligations.

The TPD verification process begins with the SSA notifying the Department of Education of borrowers who meet the disability criteria. However, borrowers can also initiate the process themselves by submitting SSA documentation or a physician’s certification. The physician’s certification must confirm the borrower’s inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. This route is particularly useful for those who haven’t yet received an SSA disability determination.

One common pitfall borrowers face is the three-year monitoring period following TPD discharge. During this time, borrowers must not earn above the poverty guideline for their family size, take out additional federal student loans, or receive a new SSA disability review determining they’ve medically improved. Violating these conditions can reinstate the loan, making it crucial to understand and adhere to the rules. For example, a single borrower in 2023 must ensure their annual earnings remain below $13,590 to avoid jeopardizing their discharge.

Comparatively, TPD verification is more streamlined for SSDI recipients than for those relying solely on physician certification. SSDI beneficiaries often face fewer hurdles because the SSA has already determined their eligibility for disability benefits. However, the process still requires attention to detail, such as ensuring the SSA shares the necessary data with the Department of Education. Borrowers should regularly check their status on the TPD Service website and respond promptly to any requests for additional information.

In conclusion, Total and Permanent Disability verification is a lifeline for SSDI recipients burdened by student loans, but it demands proactive engagement. By understanding the documentation requirements, monitoring period restrictions, and differences in application routes, borrowers can navigate the process effectively. This isn’t just about paperwork—it’s about reclaiming financial freedom in the face of significant challenges.

Track Your Student Loan Forgiveness Application: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Application Process for Loan Forgiveness

For those on Social Security Disability Insurance (SSDI), the Total and Permanent Disability (TPD) discharge program offers a lifeline to eliminate federal student loan debt. However, the application process is nuanced and requires careful attention to detail. To initiate the process, borrowers must first confirm their eligibility, which typically involves receiving a notice from the Social Security Administration (SSA) stating that their disability review will occur within five to seven years. Once eligibility is established, the borrower or their representative can apply for TPD discharge through the U.S. Department of Education’s online portal or by submitting a paper application. This step is critical, as failure to apply means the loans remain in repayment status, accruing interest and potentially leading to default.

The application itself demands specific documentation, including the SSA notice of award for SSDI benefits or a physician’s certification of permanent disability. Borrowers must also provide their loan account numbers and personal identifying information. A common pitfall is incomplete submissions, which delay approval. For instance, omitting the physician’s certification when SSA documentation is unavailable can halt the process. To avoid this, applicants should double-check the required forms and ensure all fields are accurately filled. Additionally, keeping copies of submitted documents is essential for follow-up inquiries.

After submission, the review period begins, during which borrowers are placed in a temporary forbearance to halt payments and collections. This period typically lasts 120 days but can extend if additional information is requested. During this time, it’s crucial to monitor communications from the loan servicer or the Department of Education. Approved applicants receive a notification confirming the discharge, while denied applicants have the right to appeal. Notably, discharged loans may be subject to tax, though under the American Rescue Plan Act of 2021, TPD discharges are tax-free through December 31, 2025.

A lesser-known aspect of the process is the three-year post-discharge monitoring period, during which borrowers must provide annual documentation of their earnings to ensure they remain eligible. Failure to comply can result in loan reinstatement. For SSDI recipients, this often involves submitting SSA benefit statements or physician certifications. Proactive management of this period is key, as overlooking deadlines can undo the entire discharge. Borrowers should mark their calendars and set reminders to avoid missing submissions.

In summary, the application process for TPD discharge is a structured yet intricate journey requiring diligence and organization. From confirming eligibility to navigating post-discharge monitoring, each step demands attention to detail. By understanding the requirements and potential pitfalls, SSDI recipients can maximize their chances of successfully eliminating their student loan debt and achieving financial relief.

Kentucky's Tax Rules: Student Loan Forgiveness Implications Explained

You may want to see also

Explore related products

![]()

Tax Implications of Forgiven Loans

Forgiven student loans, while a financial relief, often come with a hidden cost: taxes. The IRS generally considers forgiven debt as taxable income, meaning you may owe taxes on the amount discharged. This rule applies to student loans forgiven under certain programs, including those tied to Social Security Disability Insurance (SSDI) eligibility. Understanding these tax implications is crucial to avoid unexpected financial burdens.

For instance, if you qualify for Total and Permanent Disability (TPD) discharge through SSDI, the forgiven loan amount is typically reported to the IRS as income. This can push you into a higher tax bracket, increasing your overall tax liability. However, there are exceptions. The American Rescue Act of 2021 temporarily excludes forgiven student loans due to death or disability from taxable income through 2025. This provision offers significant relief, but it’s essential to stay updated on legislative changes, as tax laws can evolve.

To navigate these complexities, consider consulting a tax professional. They can help determine if your forgiven loans qualify for exclusion under current laws or if you’ll need to plan for the tax impact. Additionally, keep detailed records of all loan discharge documentation and IRS communications. If you’re unsure whether your forgiven loans are taxable, review IRS Publication 4302, which outlines specific guidelines for disabled taxpayers.

Another practical tip is to explore tax credits or deductions that may offset the additional tax burden. For example, the Earned Income Tax Credit (EITC) or the Child Tax Credit could reduce your overall tax liability. If you’re on SSDI, your income is likely limited, making these credits particularly valuable. Proactively planning for tax season can turn a potential financial setback into a manageable situation.

In summary, while forgiven student loans through SSDI can provide much-needed relief, the tax implications require careful attention. Stay informed about current tax laws, seek professional advice, and leverage available credits to minimize your tax burden. By taking these steps, you can ensure that loan forgiveness remains a financial benefit rather than a hidden liability.

Unlock Debt-Free Future: UK Student Loan Forgiveness Guide

You may want to see also

Explore related products

![]()

Reinstatement Risks After Loan Discharge

Student loan discharge due to a permanent disability, such as qualifying for Social Security Disability Insurance (SSDI), offers significant relief, but it’s not without potential pitfalls. One critical risk borrowers face is reinstatement of their discharged loans, which can occur under specific circumstances. Understanding these risks is essential for maintaining financial stability after discharge.

The primary trigger for reinstatement is earning income above the poverty guideline threshold during the three-year monitoring period following discharge. For example, in 2023, the poverty guideline for a single individual in the contiguous U.S. is $13,590. If your annual earnings exceed this amount, the U.S. Department of Education may reinstate your loans. This includes income from employment, self-employment, or certain benefits like unemployment compensation. To avoid this, monitor your income closely and consider consulting a financial advisor to structure your earnings within the allowed limits.

Another reinstatement risk arises from failure to submit required documentation during the monitoring period. Borrowers must provide annual earnings documentation to the loan servicer or risk having their loans reinstated. For instance, if you miss the deadline for submitting proof of income, even if your earnings are below the threshold, your loans could be reactivated. Set reminders for submission deadlines and keep detailed records of all communications with your loan servicer to protect yourself.

A lesser-known but equally important risk is regaining the ability to engage in substantial gainful activity (SGA). If the Social Security Administration (SSA) determines you are no longer disabled and can work at the SGA level, your loans may be reinstated. For 2023, the SGA amount is $1,470 per month for non-blind individuals and $2,460 for blind individuals. Regularly review SSA guidelines and consult with a disability attorney if you anticipate changes in your disability status.

Finally, tax implications can indirectly lead to reinstatement. While discharged student loans are typically not taxable, certain circumstances, such as a change in disability status or failure to meet monitoring requirements, could result in tax liabilities. These financial strains might push borrowers to seek income that exceeds the poverty threshold, triggering reinstatement. Stay informed about tax laws and consider working with a tax professional to navigate potential pitfalls.

In summary, while student loan discharge via SSDI provides relief, borrowers must remain vigilant to avoid reinstatement. Monitor income, submit required documentation, stay informed about disability status changes, and manage tax implications proactively. By understanding and mitigating these risks, you can safeguard your financial freedom after discharge.

Student Loan Forgiveness: A Catalyst for Economic Growth and Recovery

You may want to see also

Frequently asked questions

No, student loans are not automatically forgiven upon SSDI approval. However, SSDI recipients may qualify for a Total and Permanent Disability (TPD) discharge by applying through their loan servicer or the U.S. Department of Education.

To apply for a TPD discharge, submit an application to your loan servicer or the U.S. Department of Education. You can provide documentation of your SSDI approval, which simplifies the process, or complete a physician’s certification of your disability.

Most federal student loans, including Direct Loans, FFEL Loans, and Perkins Loans, qualify for TPD discharge. Private student loans, however, do not qualify and are not forgiven through SSDI.

As of recent legislation, student loan forgiveness due to TPD is tax-free through 2025. However, tax laws may change, so consult a tax professional for the most current information.

Yes, if your disability status changes and you are no longer eligible for SSDI, your student loans could be reinstated. You will be given a three-year monitoring period during which you must confirm your continued eligibility for SSDI or risk loan reinstatement.