Understanding where to find information about your student loan interest is crucial for managing your finances effectively. Student loan interest rates and details are typically outlined in your loan agreement, which you received when you first took out the loan. Additionally, you can access this information through your loan servicer’s website or online portal by logging in with your credentials. Federal student loan borrowers can visit the National Student Loan Data System (NSLDS) for a comprehensive overview of their loans, including interest rates. For private loans, check your lender’s website or contact their customer service directly. Knowing your interest rate helps you plan payments, explore repayment options, and potentially save money through strategies like interest capitalization avoidance or refinancing.

| Characteristics | Values |

|---|---|

| Source of Information | Federal Student Aid (FSA) website, MyFederalStudentAid account |

| Account Access | Requires FSA ID to log in |

| Interest Rate Type | Fixed or variable depending on loan type and disbursement date |

| Loan Types Covered | Direct Subsidized, Direct Unsubsidized, Direct PLUS, Direct Consolidation |

| Interest Accrual | Daily, based on unpaid principal balance |

| Interest Capitalization | Occurs when unpaid interest is added to the principal balance |

| Repayment Plans | Standard, Graduated, Income-Driven, etc., affecting interest accrual |

| Deferment/Forbearance | Interest may or may not accrue depending on loan type and status |

| Tax Deductibility | Student loan interest may be tax-deductible up to certain limits |

| Loan Servicers | MOHELA, Aidvantage, Nelnet, etc., provide interest rate details |

| Interest Rate Updates | Rates are updated annually for new loans based on federal regulations |

| Historical Rates | Available on the Federal Student Aid website for past years |

| Interest Calculator Tools | Available on FSA and loan servicer websites |

| Notification of Rates | Provided in loan disclosure statements and annual loan summaries |

| Interest Assistance Programs | Public Service Loan Forgiveness (PSLF) may include interest benefits |

| Private Loans | Interest rates and details vary by lender, not managed by FSA |

Explore related products

What You'll Learn

- Federal vs. Private Loans: Understand differences in interest rates and repayment terms for federal and private loans

- Interest Accrual Periods: Learn when interest starts accruing on subsidized vs. unsubsidized loans

- Repayment Plan Impact: Explore how income-driven or standard plans affect interest accumulation

- Loan Servicer Resources: Check your loan servicer’s portal for current interest rate details

- Interest Capitalization: Discover when unpaid interest is added to your loan balance

![]()

Federal vs. Private Loans: Understand differences in interest rates and repayment terms for federal and private loans

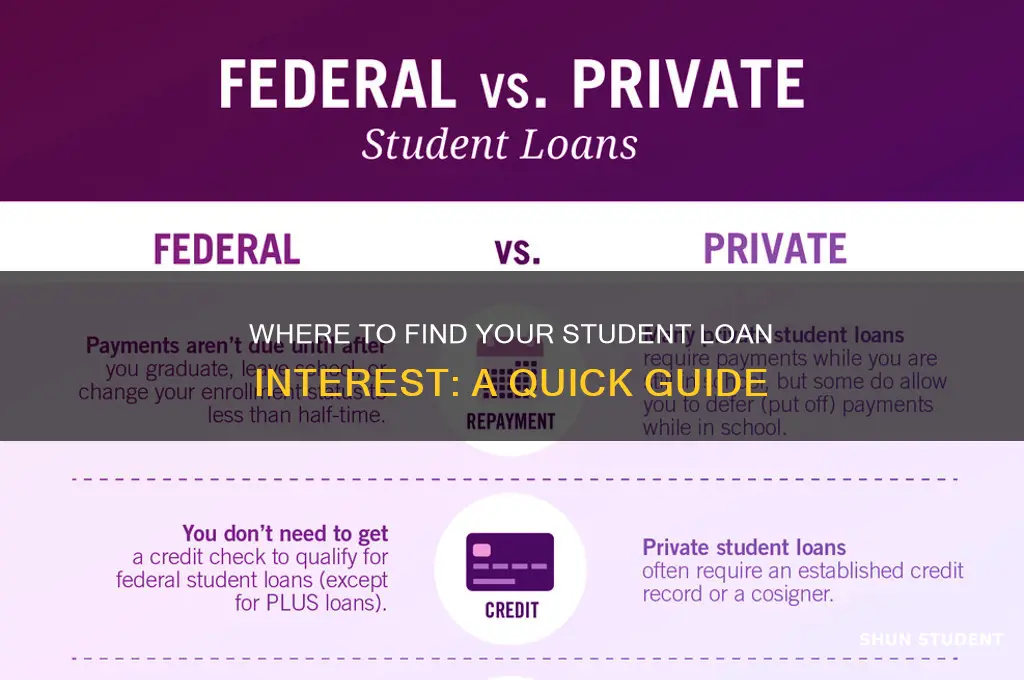

When navigating the complexities of student loans, understanding the differences between federal and private loans is crucial, especially regarding interest rates and repayment terms. Federal student loans are funded by the U.S. Department of Education and offer fixed interest rates set by Congress, which remain consistent for the life of the loan. For the 2023-2024 academic year, undergraduate federal loans have an interest rate of 5.5%, while graduate loans are at 7.05%, and PLUS loans are at 8.05%. These rates are generally lower than private loans and are determined without consideration of your credit history. To find your federal student loan interest rate, log into your account on the Federal Student Aid website (studentaid.gov), where all loan details, including interest rates, are listed under your loan breakdown.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions. Their interest rates can be fixed or variable, meaning they may fluctuate over time based on market conditions. Private loan rates are heavily influenced by your credit score and financial history, often resulting in higher rates than federal loans for borrowers with less-than-stellar credit. Variable rates may start lower but can increase, potentially making repayment more expensive. To locate your private student loan interest rate, check your loan agreement or log into your lender’s online portal, where interest rates and repayment terms are typically outlined in detail.

Repayment terms also differ significantly between federal and private loans. Federal loans offer a variety of repayment plans, including income-driven repayment (IDR) plans, which cap monthly payments based on your income and family size. These plans can provide flexibility, especially for borrowers with lower incomes. Federal loans also come with options for deferment or forbearance, allowing you to temporarily pause payments under certain conditions. Private loans, however, rarely offer such flexible repayment options. Repayment terms are strictly defined by the lender, and deferment or forbearance options are limited or unavailable. Always review your private loan agreement to understand your repayment obligations.

Another key difference is the availability of borrower protections and benefits. Federal loans provide access to loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), which forgives remaining debt after 10 years of qualifying payments for eligible borrowers. Additionally, federal loans offer deferment and forbearance options without additional fees. Private loans typically do not offer these protections or benefits, making them riskier for borrowers. To understand your interest and repayment terms, carefully review your loan agreements and contact your lender directly if you have questions.

In summary, federal loans generally offer lower, fixed interest rates, flexible repayment plans, and borrower protections, making them a safer option for most students. Private loans, while sometimes necessary to cover gaps in funding, come with higher interest rates, less flexible terms, and fewer protections. To find your student loan interest rate, check the Federal Student Aid website for federal loans or your lender’s portal for private loans. Understanding these differences will help you make informed decisions about managing your student loan debt effectively.

Deducting Student Loan Interest: Finding the Right Line on Form 1040

You may want to see also

Explore related products

![]()

Interest Accrual Periods: Learn when interest starts accruing on subsidized vs. unsubsidized loans

Understanding when interest begins to accrue on your student loans is crucial for managing your debt effectively. The interest accrual period varies significantly between subsidized and unsubsidized loans, and knowing these differences can help you make informed decisions about repayment. For subsidized loans, the federal government pays the interest while you are enrolled in school at least half-time, during the grace period after leaving school (typically six months), and during any approved deferment periods. This means interest does not start accruing until after these periods end, providing a significant financial benefit to borrowers.

On the other hand, unsubsidized loans begin accruing interest as soon as the loan is disbursed. This includes while you are still in school, during the grace period, and throughout any deferment or forbearance periods. Since the interest is not covered by the government, it capitalizes (added to the principal balance) if not paid during these times, increasing the total amount you owe over the life of the loan. To find out when interest starts accruing on your specific loans, check your loan agreement or log into your loan servicer’s website, where details about your loan type and accrual periods are typically listed.

For both loan types, understanding the accrual period is essential for budgeting and planning. If you have unsubsidized loans, consider making interest payments while in school or during grace periods to prevent capitalization and reduce long-term costs. For subsidized loans, take advantage of the interest-free periods, but remain aware of when the accrual begins to avoid unexpected expenses. Your loan servicer or the National Student Loan Data System (NSLDS) can provide detailed information about your loan status and accrual timelines.

Another key factor to consider is the grace period after graduation or leaving school. For both subsidized and unsubsidized federal loans, this period typically lasts six months before repayment begins. However, interest accrual differs: subsidized loans remain interest-free during this time, while unsubsidized loans continue to accrue interest. Knowing these timelines allows you to prepare financially and explore options like consolidating loans or enrolling in income-driven repayment plans to manage accruing interest effectively.

Finally, if you’re unsure about your loan type or accrual period, contact your loan servicer directly. They can provide personalized information and guide you on how to locate interest details in your account. Additionally, tools like the NSLDS or your school’s financial aid office can help clarify whether your loans are subsidized or unsubsidized. By staying informed about interest accrual periods, you can take proactive steps to minimize the impact of interest on your student loan debt.

Key Questions to Ask Grad Students in Your PI's Lab

You may want to see also

Explore related products

![]()

Repayment Plan Impact: Explore how income-driven or standard plans affect interest accumulation

When it comes to managing student loan interest, understanding the impact of your repayment plan is crucial. The two primary categories of repayment plans—income-driven plans and standard plans—have distinct effects on how interest accumulates over time. Income-driven plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), adjust your monthly payments based on your income and family size. These plans often result in lower monthly payments, especially if your income is modest. However, because the payments may not cover the full amount of interest accruing each month, unpaid interest can capitalize, meaning it is added to your principal balance. This can lead to a larger overall loan balance over time, increasing the total interest paid.

On the other hand, standard repayment plans typically require fixed monthly payments over a 10-year period. With these plans, borrowers often pay more each month but benefit from paying off the loan faster and minimizing interest accumulation. Since the payments are designed to cover both principal and interest, there is less likelihood of interest capitalization. For borrowers with stable, higher incomes, standard plans can be a more cost-effective option in the long run, as they reduce the total interest paid by shortening the loan term.

Income-driven plans, while beneficial for those with lower incomes or high debt-to-income ratios, can lead to significant interest growth if the payments do not cover the accruing interest. For example, if your monthly interest accrual is $100 but your income-driven payment is only $50, the remaining $50 in interest may capitalize, increasing your loan balance. Over time, this can result in a phenomenon known as "negative amortization," where your loan balance grows instead of shrinks. Borrowers on income-driven plans should monitor their loan balances and consider making extra payments toward interest whenever possible to mitigate this effect.

To find information about your student loan interest and how your repayment plan is impacting it, log in to your loan servicer’s website or the Federal Student Aid portal. Look for details on your current balance, interest rate, and payment allocation. Many servicers provide breakdowns of how each payment is applied to interest and principal. Additionally, tools like the Loan Simulator on the Federal Student Aid website can help you compare how different repayment plans affect interest accumulation over time. Understanding these details is essential for making informed decisions about managing your student loan debt.

Ultimately, the choice between an income-driven plan and a standard plan depends on your financial situation and long-term goals. If minimizing total interest paid is a priority and your budget allows for higher monthly payments, a standard plan may be more advantageous. However, if affordability is a concern and you need lower monthly payments, an income-driven plan can provide relief, though you should be prepared for potential interest capitalization. Regularly reviewing your loan details and exploring options like refinancing or extra payments can help you navigate the impact of your repayment plan on interest accumulation.

Student Loan Interest Waived: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Loan Servicer Resources: Check your loan servicer’s portal for current interest rate details

If you're looking to find your student loan interest rate, one of the most direct and reliable methods is to check your loan servicer's portal. Your loan servicer is the company that handles the billing and other services on your student loan. They are a crucial resource for understanding the specifics of your loan, including the current interest rate. Most loan servicers provide an online portal where you can access detailed information about your loan, make payments, and view important documents. Here’s how you can utilize this resource effectively.

To begin, log in to your loan servicer’s website using your credentials. If you haven’t created an account yet, you’ll need to register with your personal information, such as your name, Social Security number, and loan account number. Once logged in, navigate to the dashboard or account summary section. This area typically displays an overview of your loan, including the principal balance, interest rate, and payment status. Look for a section labeled "Loan Details" or "Interest Rate Information" to find the current interest rate applied to your student loan. This rate is crucial as it determines how much interest accrues on your loan over time.

If you’re having trouble locating the interest rate on the dashboard, explore the menu options for a more detailed breakdown. Many loan servicer portals have a "Statements" or "Documents" section where you can download monthly statements or annual loan summaries. These documents often include a clear breakdown of your interest rate, along with other important terms of your loan. Additionally, some servicers provide a "Help" or "FAQ" section that explains how to find specific information, including interest rates, on their platform.

Another useful feature of loan servicer portals is the ability to contact customer support directly. If you’re unable to find the interest rate information on your own, reach out to your loan servicer’s customer service team. They can guide you through the portal or provide the information directly. Most servicers offer multiple contact methods, such as live chat, email, or phone support, making it convenient to get the assistance you need. Remember to have your account information ready when you contact them to expedite the process.

Lastly, it’s a good practice to regularly check your loan servicer’s portal for updates, especially if you have multiple loans or if your interest rate is variable. Variable interest rates can change periodically based on market conditions, so staying informed ensures you’re aware of any adjustments that may affect your payments. By familiarizing yourself with your loan servicer’s portal, you’ll have a valuable tool at your disposal for managing your student loan effectively and understanding the costs associated with it.

Student Loan Interest Resumes: Key Dates and What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Interest Capitalization: Discover when unpaid interest is added to your loan balance

Interest capitalization is a critical concept for student loan borrowers to understand, as it directly impacts the total amount you’ll repay over the life of your loan. In simple terms, interest capitalization occurs when unpaid interest is added to your loan’s principal balance, causing your debt to grow. This process typically happens under specific circumstances, such as when your grace period ends, when a deferment or forbearance period concludes, or if you fail to make payments on an unsubsidized loan while in school. To find information about your student loan interest and whether capitalization has occurred, log into your loan servicer’s website or your Federal Student Aid account. Here, you can review your loan details, including the interest rate, accrued interest, and any instances where interest has been capitalized.

For federal student loans, interest capitalization is more likely to occur during periods when payments are not required, such as during grace periods, deferment, or forbearance. For example, if you have an unsubsidized Direct Loan and you choose not to pay the interest while in school, that interest will capitalize when you graduate or drop below half-time enrollment. Similarly, if you postpone payments through deferment or forbearance, any unpaid interest will be added to your principal balance when the payment pause ends. Private student loans may also capitalize interest, but the terms vary by lender, so it’s essential to review your loan agreement carefully. To avoid unnecessary capitalization, consider paying at least the monthly interest accrual while in school or during periods of non-payment.

To locate specific details about interest capitalization on your student loan, start by checking your loan statements or account summary. Federal loan borrowers can access this information through their MyFederalStudentAid account or their loan servicer’s portal. Look for terms like "capitalized interest" or "interest added to principal" in your loan activity. If you’re unsure, contact your loan servicer directly to request a breakdown of your loan balance, including any capitalized interest. Understanding when and why interest was added to your principal can help you make informed decisions about repayment strategies, such as paying more than the minimum to reduce the impact of capitalization.

Preventing interest capitalization can save you money in the long run. One effective strategy is to make interest payments while in school, even if they’re not required. For federal loans, you can also explore income-driven repayment plans or loan forgiveness programs that may reduce the likelihood of capitalization. If you’re in a deferment or forbearance, ask your servicer about the option to pay the interest during this time to avoid capitalization when payments resume. For private loans, discuss capitalization terms with your lender and explore refinancing options that may offer better terms.

In summary, interest capitalization occurs when unpaid interest is added to your loan balance, increasing the total amount you owe. To find details about your student loan interest and capitalization, review your loan statements, log into your loan servicer’s portal, or contact your servicer directly. Understanding when and why capitalization happens—such as after grace periods, deferment, or forbearance—can help you take proactive steps to minimize its impact. By staying informed and exploring strategies to prevent capitalization, you can manage your student loan debt more effectively and save money over time.

Interest-Free Student Loans: A Historical Overview of Their Inception

You may want to see also

Frequently asked questions

You can find your student loan interest rate on your loan agreement, through your loan servicer's website, or by logging into your account on the Federal Student Aid website if it’s a federal loan.

Student loan interest typically accrues daily, based on the outstanding principal balance of your loan.

You can view the total interest accrued on your student loan by checking your loan statement from your loan servicer or by reviewing your account details online.

Yes, many loan servicers and financial websites offer student loan interest calculators to help you estimate how much interest will accrue over the life of your loan.

Information about the tax-deductibility of student loan interest can be found on the IRS website or by consulting a tax professional. Generally, you may be eligible for a deduction if you meet certain criteria.