Interest paid on student loans is a critical aspect of the repayment process, as it significantly impacts the total cost of borrowing. When students or graduates make loan payments, a portion typically goes toward the interest accrued on the principal balance, while the remainder reduces the principal itself. The allocation of these payments depends on the loan’s terms and the repayment plan chosen. For federal student loans, interest may be deductible on federal taxes, up to a certain limit, providing a potential financial benefit to borrowers. Understanding where and how interest is applied is essential for managing student loan debt effectively and minimizing long-term financial burden.

Explore related products

What You'll Learn

![]()

Tax Deductibility of Student Loan Interest

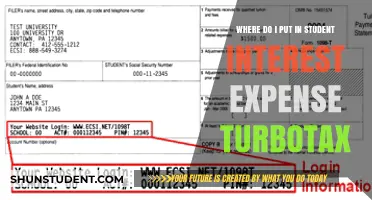

The interest paid on student loans can be a significant financial burden for many borrowers, but there is a silver lining: it may be tax-deductible. The Tax Deductibility of Student Loan Interest is a provision that allows eligible taxpayers to claim a deduction for the interest paid on qualified student loans, potentially reducing their taxable income and overall tax liability. This benefit is particularly valuable for recent graduates and individuals with substantial student loan debt, as it provides a measure of financial relief during the repayment process. To take advantage of this deduction, it's essential to understand the eligibility criteria, limitations, and reporting requirements set forth by the Internal Revenue Service (IRS).

To qualify for the student loan interest deduction, the loan must have been taken out solely to pay for qualified higher education expenses, such as tuition, fees, room and board, and other necessary educational costs. The deduction is available for interest paid on both federal and private student loans, provided that the loans meet the IRS's criteria. Additionally, the taxpayer must be legally obligated to pay the interest, and the loan must be used for the taxpayer, their spouse, or their dependent. It's worth noting that the deduction is phased out for taxpayers with higher incomes, meaning that the amount of deductible interest decreases as income increases. For the tax year 2023, the phase-out begins at $70,000 for single filers and $140,000 for married couples filing jointly.

The maximum amount of student loan interest that can be deducted is $2,500 per year, although this limit may be reduced based on the taxpayer's income and filing status. To claim the deduction, taxpayers must receive a Form 1098-E from their loan servicer, which reports the total interest paid during the tax year. If the taxpayer doesn't receive this form, they can still claim the deduction by obtaining the interest information from their loan servicer and reporting it on their tax return. The student loan interest deduction is claimed as an adjustment to income, meaning that taxpayers can take advantage of it even if they don't itemize their deductions. This makes it a valuable tax break for many borrowers, as it can be combined with other tax credits and deductions to maximize savings.

When reporting the student loan interest deduction, taxpayers should use the IRS Form 1040 or Form 1040-SR, and attach Schedule 1 if necessary. It's crucial to keep accurate records of all student loan payments and interest charges, as the IRS may request documentation to verify the deduction. Furthermore, taxpayers should be aware that the student loan interest deduction cannot be claimed for loans that have been consolidated or refinanced, unless the consolidation or refinancing was done to pay for qualified education expenses. By understanding the rules and requirements surrounding the Tax Deductibility of Student Loan Interest, borrowers can make informed decisions about their finances and potentially save hundreds or even thousands of dollars on their tax bill.

In addition to the federal tax deduction, some states also offer their own student loan interest deductions or credits. Taxpayers should check with their state's tax agency to determine if they are eligible for any additional benefits. It's also essential to stay informed about changes to tax laws and regulations, as these can impact the availability and amount of the student loan interest deduction. By staying up-to-date and taking advantage of all available tax breaks, borrowers can minimize the financial burden of student loan repayment and achieve greater financial stability. Ultimately, the Tax Deductibility of Student Loan Interest is a valuable tool for managing student loan debt, and understanding its nuances can help taxpayers make the most of this important benefit.

Where to File Student Loan Interest: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Federal vs. Private Loan Interest Payments

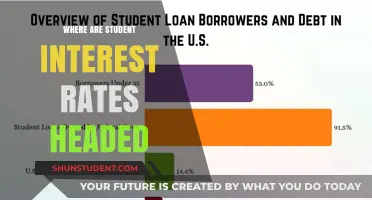

When it comes to understanding where interest paid on student loans goes, it’s essential to distinguish between federal and private loans, as their structures and implications differ significantly. Federal student loans are funded by the U.S. Department of Education and come with fixed interest rates set by Congress. The interest paid on these loans primarily returns to the federal government, which then allocates the funds to various programs, including education and deficit reduction. For example, a portion of the interest may be used to subsidize future loans or support initiatives like Pell Grants for low-income students. Federal loans also offer borrower protections, such as income-driven repayment plans and loan forgiveness programs, which can affect how interest accrues and is paid over time.

In contrast, private student loans are offered by banks, credit unions, and other financial institutions. The interest paid on these loans goes directly to the lender, which is typically a for-profit entity. Private lenders use the interest income to generate revenue, cover operational costs, and fund additional loans. Unlike federal loans, private loans often have variable interest rates, which can fluctuate based on market conditions, potentially increasing the total cost of borrowing. Additionally, private loans rarely offer the same borrower protections as federal loans, making it harder for borrowers to manage interest payments during financial hardship.

One key difference in federal vs. private loan interest payments is how interest accrues during periods of non-payment. For federal loans, certain types (e.g., subsidized Direct Loans) do not accrue interest while the borrower is in school or during grace periods. Unsubsidized federal loans, however, do accrue interest during these times, which is capitalized (added to the principal balance) if not paid. Private loans, on the other hand, almost always accrue interest immediately, even while the borrower is in school, which can significantly increase the total amount repaid over time.

Another critical aspect is the tax treatment of interest payments. Borrowers who pay interest on federal or private student loans may be eligible to deduct up to $2,500 of interest paid annually on their federal tax returns, provided they meet certain income requirements. However, this deduction applies only to qualified education loans, and the rules can differ slightly between federal and private loans. For instance, the lender must provide a Form 1098-E to the borrower and the IRS, which is more straightforward with federal loans due to their standardized reporting processes.

Finally, the long-term financial impact of interest payments varies between federal and private loans. Federal loans often provide more flexibility in repayment options, such as income-driven plans that cap monthly payments based on earnings, potentially reducing the burden of interest over time. Private loans, however, typically require full payments shortly after graduation, leaving less room for financial adjustment. Understanding these differences is crucial for borrowers to make informed decisions about managing their student loan interest payments effectively.

Calculating Monthly Interest on a $7,500 Student Loan: A Guide

You may want to see also

Explore related products

![]()

Interest Capitalization on Student Loans

For federal student loans, interest capitalization rules vary based on the loan type. Subsidized Direct Loans do not capitalize interest while the borrower is in school, during the grace period, or in deferment. However, unsubsidized Direct Loans, PLUS Loans, and private student loans often capitalize interest in these situations. For instance, if a borrower postpones payments through a deferment or forbearance, the unpaid interest may be added to the principal balance when the repayment period resumes. This means the borrower will pay interest on a larger amount, increasing the total cost of the loan.

Private student loans generally have stricter interest capitalization policies compared to federal loans. Many private lenders capitalize interest more frequently, such as monthly or at the end of a forbearance period. Borrowers with private loans should carefully review their loan agreements to understand when and how interest capitalization occurs. Additionally, some private lenders may capitalize interest immediately when payments are missed, further escalating the loan balance. This makes it crucial for borrowers to stay current on their payments or explore options like interest-only payments during periods of financial hardship.

To minimize the impact of interest capitalization, borrowers can take proactive steps. One effective strategy is making interest payments while in school, during grace periods, or while loans are in deferment or forbearance. By paying the interest as it accrues, borrowers can prevent it from being added to the principal balance. Another approach is to choose income-driven repayment plans for federal loans, which may limit interest capitalization in certain cases. Borrowers should also consider refinancing private loans to secure a lower interest rate or more favorable terms, though this may come with trade-offs like losing federal benefits.

Understanding interest capitalization is essential for managing student loan debt effectively. Borrowers should familiarize themselves with their loan terms, monitor interest accrual, and explore strategies to reduce capitalization. By staying informed and taking proactive measures, borrowers can avoid unnecessary increases in their loan balances and save money over time. Regular communication with loan servicers and financial advisors can also provide valuable guidance tailored to individual circumstances. Ultimately, addressing interest capitalization early can lead to more manageable repayment and long-term financial stability.

When Did Student Loan Interest Rates Increase? A Timeline

You may want to see also

Explore related products

![]()

Interest Rates for Different Loan Types

Interest rates on student loans can vary significantly depending on the type of loan, the lender, and the borrower’s financial situation. Federal student loans typically offer fixed interest rates set by the U.S. Congress, which remain the same for the life of the loan. For the 2023-2024 academic year, undergraduate Direct Subsidized and Unsubsidized Loans carry an interest rate of 5.5%, while graduate Unsubsidized Loans are at 7.05%, and PLUS Loans for parents and graduate students are at 8.05%. These rates are generally lower than private loans and come with borrower protections like income-driven repayment plans and loan forgiveness options. The interest on federal loans is paid to the U.S. Department of Education, which uses the funds to support the federal student loan program and other educational initiatives.

Private student loans, on the other hand, are offered by banks, credit unions, and other financial institutions, and their interest rates can be fixed or variable. Variable rates may start lower but can fluctuate over time based on market conditions, potentially increasing the cost of the loan. Fixed rates remain consistent but are often higher initially. Private loan interest rates are determined by the borrower’s creditworthiness, with those having higher credit scores qualifying for lower rates. The interest paid on private loans goes directly to the lending institution, which profits from the loan. Borrowers should carefully compare private loan offers, as terms and rates can vary widely, and these loans typically lack the flexible repayment options available with federal loans.

Subsidized vs. Unsubsidized federal loans also differ in how interest accrues. For Direct Subsidized Loans, the government pays the interest while the borrower is in school at least half-time, during the grace period after leaving school, and during deferment periods. This means no interest is added to the loan balance during these times, making subsidized loans more affordable. In contrast, Direct Unsubsidized Loans accrue interest from the time the loan is disbursed, and the borrower is responsible for paying it. If the borrower chooses not to pay the interest while in school, it is capitalized (added to the principal balance), increasing the total cost of the loan over time.

PLUS Loans, available to graduate students and parents of dependent undergraduates, have higher interest rates compared to other federal loans. While they offer the same fixed-rate structure, the higher rate reflects the greater risk associated with these loans. Borrowers should consider whether the higher cost is justified by their financial needs and ability to repay. Interest payments on PLUS Loans also go to the Department of Education, supporting the federal loan program.

Understanding the tax implications of student loan interest is also important. For federal and private loans, borrowers may be eligible to deduct up to $2,500 in student loan interest paid annually on their federal tax return, provided they meet certain income requirements. This deduction reduces taxable income, offering a financial benefit. However, it does not reduce the total interest paid to the lender, which remains a cost of borrowing. Borrowers should consult a tax professional to determine their eligibility for this deduction.

In summary, interest rates for student loans vary by loan type, with federal loans offering fixed rates and borrower protections, while private loans provide variable or fixed rates based on creditworthiness. Subsidized federal loans offer interest-free periods, whereas unsubsidized and private loans accrue interest immediately. Understanding these differences is crucial for managing loan costs effectively and making informed borrowing decisions.

Understanding Student Loan Interest Accrual: When Does It Begin?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Repayment Plans Affecting Interest Accrual

When considering where interest paid on student loans goes, it’s crucial to understand how different repayment plans affect interest accrual. Repayment plans dictate not only how much you pay monthly but also how interest accumulates over time. For federal student loans, the repayment plan you choose can significantly impact the total interest paid over the life of the loan. For instance, income-driven repayment (IDR) plans often result in lower monthly payments but may lead to higher interest accrual if payments don’t cover the full interest amount, causing capitalization. Conversely, standard repayment plans typically have higher monthly payments but minimize interest accrual by ensuring the loan is paid off in a shorter timeframe.

Income-Driven Repayment (IDR) plans are designed to make loan payments more manageable based on income and family size. However, these plans often result in interest accrual exceeding the monthly payment, especially for borrowers with high loan balances and low incomes. When payments fail to cover the accruing interest, the unpaid interest is capitalized, meaning it’s added to the principal balance. This increases the total amount of interest paid over time, as interest is then calculated on a higher principal. Borrowers on IDR plans should be aware that while these plans offer flexibility, they may pay more in interest in the long run.

Standard repayment plans, on the other hand, are structured to pay off loans in 10 years with fixed monthly payments. These plans ensure that borrowers pay less in interest overall because the loan is repaid more quickly. Each payment covers both principal and interest, reducing the balance steadily. For borrowers who can afford higher monthly payments, standard plans are the most cost-effective option, as they minimize interest accrual and capitalization. This plan is ideal for those seeking to pay off their loans as quickly as possible while minimizing the total cost.

Graduated and extended repayment plans offer alternatives to standard plans but come with trade-offs regarding interest accrual. Graduated plans start with lower payments that increase every two years, while extended plans stretch repayment over 25 years. Both options lower monthly payments but extend the repayment period, allowing more time for interest to accrue. Borrowers on these plans often end up paying significantly more in interest over the life of the loan compared to standard plans. These plans are best for borrowers who need lower initial payments but should be used cautiously to avoid excessive interest costs.

Lastly, deferment and forbearance options temporarily pause or reduce loan payments but can negatively impact interest accrual. For unsubsidized loans, interest continues to accrue during deferment and forbearance, and unpaid interest is capitalized when the repayment period resumes. This increases the loan balance and the total interest paid over time. Borrowers should consider these options only as a last resort and explore other repayment plans to minimize interest capitalization. Understanding how each repayment plan affects interest accrual is essential for managing student loan debt effectively and ensuring that payments align with long-term financial goals.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Frequently asked questions

The interest paid on federal student loans goes to the U.S. Department of Education, which uses the funds to support various federal programs, including education initiatives and deficit reduction.

The interest paid on private student loans goes to the lender, which is typically a bank, credit union, or financial institution. These lenders use the interest to cover operational costs, generate profit, and fund additional loans.

The interest paid on refinanced student loans goes to the new lender that provided the refinancing, such as a private bank or financial institution. This interest is used similarly to private loan interest, supporting the lender’s operations and profitability.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)