The maximum interest rate on student loans is a critical factor for borrowers, as it directly impacts the total cost of repayment over time. In the United States, federal student loans typically have fixed interest rates set by Congress, which are generally lower than private loan rates and vary depending on the type of loan and the year it was disbursed. For instance, undergraduate Direct Subsidized and Unsubsidized Loans for the 2023-2024 academic year carry a rate of 5.5%, while PLUS Loans for parents and graduate students are at 8.05%. Private student loans, on the other hand, have variable or fixed rates determined by the lender, often based on the borrower’s creditworthiness, and can exceed 12% or more. Understanding these limits is essential for students and families to make informed financial decisions and explore options like income-driven repayment plans or refinancing to manage debt effectively.

| Characteristics | Values |

|---|---|

| Maximum Interest Rate (Federal Undergraduate Loans) | 7.05% (for loans first disbursed on or after July 1, 2023, and before July 1, 2024) |

| Maximum Interest Rate (Federal Graduate Loans) | 8.55% (for loans first disbursed on or after July 1, 2023, and before July 1, 2024) |

| Maximum Interest Rate (Federal PLUS Loans) | 9.55% (for loans first disbursed on or after July 1, 2023, and before July 1, 2024) |

| Interest Rate Type | Fixed (for federal loans) |

| Rate Determination | Based on 10-year Treasury note yield + margin (set by Congress) |

| Private Student Loans | Variable (typically 1% - 12% or more, depending on creditworthiness) |

| Rate Variability | Fixed or variable (private loans); fixed (federal loans) |

| Repayment Terms | 10-25 years (federal); varies (private) |

| Borrower Protections | Income-driven repayment, deferment, forbearance (federal loans only) |

| Latest Update | Rates updated annually based on May Treasury note auction |

Explore related products

What You'll Learn

![]()

Federal vs. Private Loan Rates

When considering student loans, understanding the difference between federal and private loan rates is crucial, especially in terms of the maximum interest rates borrowers might face. Federal student loans, which are issued by the U.S. Department of Education, have interest rates set by Congress and are typically fixed for the life of the loan. As of recent data, federal undergraduate loans have a maximum interest rate capped at 8.25% for Direct Subsidized and Unsubsidized Loans for undergraduate students. Graduate and professional students face a higher cap, with Direct Unsubsidized Loans reaching a maximum of 9.5%, and Direct PLUS Loans, which are available to graduate students and parents, capped at 10.5%. These rates are determined annually based on the 10-year Treasury note index, plus a fixed margin, ensuring they remain relatively stable and predictable.

In contrast, private student loans, offered by banks, credit unions, and other financial institutions, have interest rates that vary widely based on the borrower’s creditworthiness, the lender’s policies, and market conditions. Unlike federal loans, private loans do not have a statutory maximum interest rate, meaning rates can theoretically climb much higher. While some private loans may offer competitive rates lower than federal loans for borrowers with excellent credit, others can exceed 12% or more, especially for those with poor credit or no cosigner. Additionally, private loans often have variable interest rates, which can fluctuate over time, potentially increasing the overall cost of the loan.

One key advantage of federal loans is their borrower protections and repayment options, which are not guaranteed with private loans. Federal loans offer income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options, making them a safer choice for many borrowers. Private loans, on the other hand, rarely provide such flexibility, and their terms are strictly determined by the lender. This lack of protections means borrowers must carefully consider their ability to repay private loans, especially at higher interest rates.

Another important factor is the role of credit history in determining rates. Federal student loans do not require a credit check (except for PLUS Loans), making them accessible to students regardless of their credit profile. Private loans, however, heavily rely on credit scores and income levels, often requiring a cosigner for students with limited credit history. This can result in significantly higher rates for borrowers with less-than-ideal credit, further widening the gap between federal and private loan costs.

In summary, while federal student loans offer capped interest rates and robust borrower protections, private loans come with variable and potentially much higher rates, depending on individual financial circumstances. Borrowers should exhaust federal loan options before turning to private loans, as federal loans generally provide more favorable terms and long-term financial security. Understanding these differences is essential for making informed decisions about financing education and managing student debt effectively.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Current Federal Interest Rate Caps

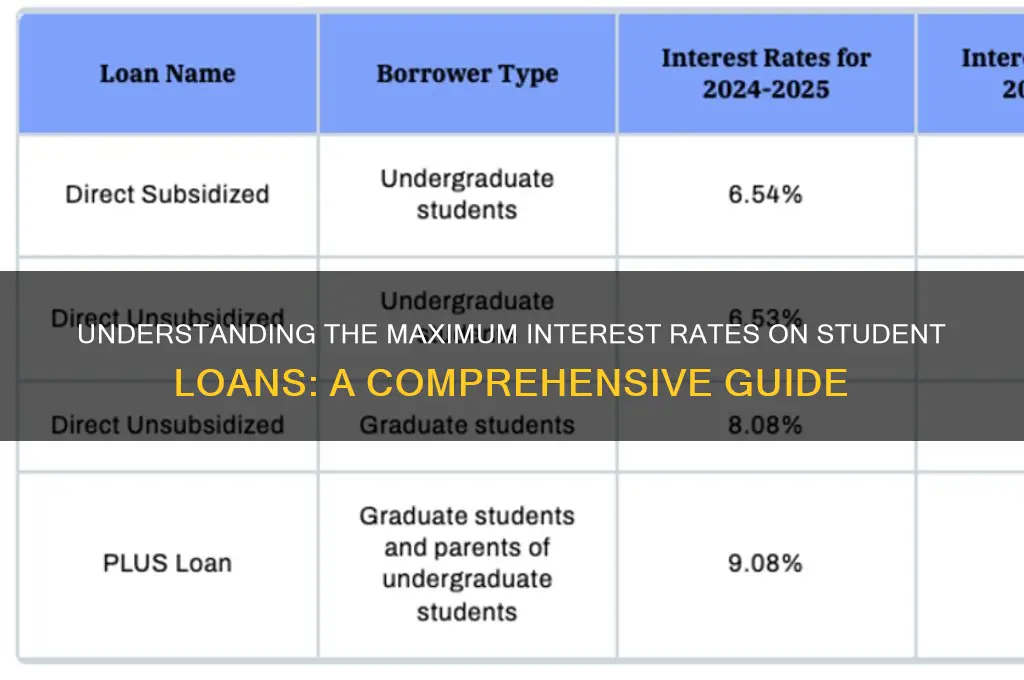

As of the most recent updates, the federal government has implemented specific interest rate caps on student loans to protect borrowers from excessively high interest rates. These caps are part of a broader effort to make higher education more accessible and manageable for students and their families. The Current Federal Interest Rate Caps for student loans are determined annually, based on the 10-year Treasury note auction held each May, plus a fixed margin depending on the type of loan and the borrower's educational level.

For Undergraduate Direct Subsidized Loans and Direct Unsubsidized Loans, the current interest rate cap is set at 8.25%. This rate applies to loans first disbursed on or after July 1, 2023, and before July 1, 2024. It’s important to note that these loans are subsidized by the government, meaning the government pays the interest while the borrower is in school, during the grace period, and in certain deferment periods. For Graduate and Professional Direct Unsubsidized Loans, the interest rate cap is higher, currently set at 9.5%. These loans are not subsidized, so interest accrues while the borrower is in school.

Direct PLUS Loans, which are available to graduate students and parents of dependent undergraduate students, have an even higher interest rate cap of 10.5%. These loans require a credit check and are designed to cover any remaining costs not met by other financial aid. Despite the higher cap, PLUS Loans offer fixed interest rates for the life of the loan, providing predictability for borrowers. It’s crucial for borrowers to understand these caps, as they directly impact the total cost of repayment over the life of the loan.

The federal government also enforces aggregate loan limits to prevent borrowers from accumulating unsustainable debt. For instance, dependent undergraduate students can borrow up to $31,000 in total, with no more than $23,000 in subsidized loans. Independent undergraduates and dependent students whose parents are ineligible for PLUS Loans have higher limits, up to $57,500, with the same $23,000 subsidized cap. Graduate and professional students can borrow up to $138,500, including any undergraduate loans, with no more than $65,500 in subsidized loans.

Borrowers should also be aware of income-driven repayment (IDR) plans, which can further mitigate the impact of interest rates by capping monthly payments at a percentage of discretionary income. These plans can extend the repayment period but may result in more interest paid over time. Understanding the interplay between interest rate caps, loan limits, and repayment options is essential for managing student loan debt effectively.

Lastly, it’s worth noting that private student loans are not subject to federal interest rate caps and often come with variable rates that can exceed federal limits significantly. Borrowers are strongly encouraged to exhaust federal loan options before considering private loans due to the added protections and benefits provided by federal programs. Staying informed about Current Federal Interest Rate Caps and other loan terms is key to making educated financial decisions.

Understanding Maximum Student Loan Interest Adjustment: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Private Lender Rate Variability

One of the primary drivers of private lender rate variability is the borrower’s credit profile. Lenders assess credit scores, income, debt-to-income ratios, and other financial indicators to gauge the risk of lending. Borrowers with excellent credit and stable income may qualify for lower interest rates, while those with poor or limited credit history could face significantly higher rates, sometimes reaching the maximum limits set by the lender. This can result in maximum interest rates ranging from 10% to 15% or even higher, depending on the lender’s policies and the borrower’s financial situation.

Another factor contributing to rate variability is the type of loan and repayment terms offered by private lenders. Variable-rate loans, for instance, may start with lower interest rates than fixed-rate loans but can increase over time based on market interest rate benchmarks, such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. This means the maximum interest rate a borrower could pay on a variable-rate loan is not only determined by the lender’s initial offer but also by future economic conditions. In contrast, fixed-rate loans provide stability but may start at a higher rate, with maximums often capped by the lender’s internal policies.

Market competition and lender-specific strategies also play a significant role in private lender rate variability. Some lenders may offer competitive rates to attract borrowers with strong credit profiles, while others might focus on higher-risk borrowers and charge premium rates to offset potential defaults. Additionally, lenders may impose maximum interest rate caps, but these caps can vary widely across institutions. For example, one lender might cap rates at 18%, while another may allow rates to climb as high as 25% for certain borrowers. This underscores the importance of shopping around and comparing offers from multiple lenders.

Lastly, economic conditions and regulatory environments influence private lender rate variability. During periods of economic uncertainty or rising interest rates, private lenders may increase their rates to protect against inflation and higher borrowing costs. Conversely, in a low-interest-rate environment, lenders might offer more competitive terms. Borrowers should remain aware of these macroeconomic factors, as they can impact the maximum interest rates available at any given time. Understanding these dynamics is essential for making informed decisions and securing the most favorable terms when taking out private student loans.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

![]()

Historical Trends in Student Loan Rates

The interest rates on student loans have fluctuated significantly over the past few decades, reflecting broader economic conditions and shifts in federal policy. In the 1980s and early 1990s, student loan rates were relatively high, often exceeding 7% for undergraduate loans. These rates were tied to the prevailing market conditions, with the federal government setting fixed rates that remained unchanged for the life of the loan. For instance, in 1988, the interest rate for subsidized Stafford loans was 7.0%, while unsubsidized loans carried rates as high as 10.0%. These high rates were a response to the inflationary pressures of the era, which peaked in the early 1980s.

The 1990s and early 2000s saw a gradual decline in student loan interest rates, driven by legislative changes and a more stable economic environment. The Higher Education Amendments of 1992 introduced variable interest rates tied to the 91-day Treasury bill, allowing rates to adjust annually based on market conditions. This change led to a reduction in rates, with undergraduate loans dropping to around 5.0% by the mid-1990s. However, rates began to rise again in the early 2000s, reaching a peak of 6.8% for subsidized Stafford loans in 2006. This increase was partly due to the rising cost of education and the growing demand for student loans.

The 2008 financial crisis marked a turning point in student loan interest rates, as the federal government took steps to make borrowing more affordable during the economic downturn. The Health Care and Education Reconciliation Act of 2010 eliminated subsidized loans for graduate and professional students, but it also introduced a new income-driven repayment plan and lowered rates for undergraduate borrowers. By 2013, interest rates were tied to the 10-year Treasury note, with caps to prevent excessive increases. For example, undergraduate subsidized and unsubsidized loans had a maximum rate of 8.25%, while graduate unsubsidized loans were capped at 9.5%, and PLUS loans at 10.5%.

In recent years, student loan interest rates have continued to reflect economic trends, with rates reaching historic lows during the COVID-19 pandemic. For the 2020-2021 academic year, undergraduate loans carried a rate of 2.75%, the lowest in decades. However, rates have begun to rise again as the Federal Reserve has increased interest rates to combat inflation. As of the 2023-2024 academic year, undergraduate loans have a rate of 5.5%, while graduate unsubsidized loans are at 7.05%, and PLUS loans are at 8.05%. These increases highlight the ongoing sensitivity of student loan rates to broader economic conditions.

Looking at the historical trends, it is clear that the maximum interest rate on student loans has been influenced by a combination of legislative changes, economic conditions, and federal policy decisions. While rates have generally trended downward since the 1980s, they remain subject to fluctuation based on market dynamics. Borrowers must stay informed about these trends, as they directly impact the cost of education and the long-term financial burden of student loans. Understanding these historical patterns can help students and families make more informed decisions about financing their education.

Explore related products

$16.53 $22.99

![]()

Impact of Credit Score on Rates

When considering the maximum interest rate on student loans, it's essential to understand how credit scores play a pivotal role in determining the rates borrowers receive. Lenders, whether they are private institutions or government-backed programs, assess the creditworthiness of applicants to gauge the risk associated with lending. A higher credit score generally indicates a lower risk to the lender, which can lead to more favorable interest rates for the borrower. Conversely, a lower credit score may result in higher interest rates, as lenders compensate for the perceived increased risk of default.

The impact of a credit score on student loan rates is particularly significant in the realm of private student loans. Private lenders often have a wide range of interest rates, and these rates can vary dramatically based on the borrower's credit history. For instance, a borrower with an excellent credit score (typically above 750) might secure a loan with an interest rate at the lower end of the spectrum, sometimes even below the maximum rates advertised. On the other hand, individuals with fair or poor credit scores (below 650) may face interest rates nearing the maximum limit, which can significantly increase the overall cost of the loan.

Federal student loans, while generally more forgiving in terms of credit requirements, also consider credit history for certain types of loans. For example, PLUS loans, which are available to graduate students and parents of dependent undergraduate students, do require a credit check. Borrowers with adverse credit histories may still be eligible for these loans but could face higher interest rates or additional fees. However, it's important to note that federal student loan interest rates are typically fixed and set by Congress, so they do not fluctuate as widely as private loan rates based on individual credit scores.

Improving one's credit score before applying for a student loan can be a strategic move to secure better rates. This can be achieved by paying bills on time, reducing outstanding debt, and correcting any inaccuracies on credit reports. For students with limited credit history, having a co-signer with a strong credit profile can also help in obtaining a loan with a lower interest rate. Co-signers provide additional security to the lender, often resulting in more favorable loan terms.

In summary, the impact of a credit score on student loan interest rates is profound, especially in the private loan market. Borrowers with higher credit scores are likely to benefit from lower interest rates, reducing the long-term cost of their education financing. Understanding this relationship and taking steps to improve creditworthiness can be crucial for students and their families when navigating the complexities of student loan borrowing. By being proactive about credit health, borrowers can position themselves to access the most competitive rates available.

Frequently asked questions

The maximum interest rate on federal student loans varies by loan type and year. For example, for the 2023-2024 academic year, undergraduate Direct Subsidized and Unsubsidized Loans have a fixed rate of 5.5%, while Graduate PLUS Loans are capped at 8.05%.

Private student loan interest rates are not federally regulated and can vary widely based on the lender, creditworthiness, and market conditions. There is no legal maximum, but rates typically range from 3% to 12% or higher, depending on the borrower’s financial profile.

For federal student loans, interest rates are fixed for the life of the loan, meaning they do not change. However, private student loans may have variable interest rates, which can fluctuate based on market indices like the LIBOR or Prime Rate, potentially increasing or decreasing over time.