Navigating the complexities of student loan repayment often involves understanding and managing interest, a critical component that can significantly impact overall debt. One essential aspect of this process is locating and utilizing the student loan interest form, typically known as Form 1098-E. This document is provided by lenders and serves as a crucial tax deduction tool for borrowers, allowing them to claim a portion of the interest paid on their student loans as a deduction on their federal income tax return. Knowing where to find this form—whether through online accounts, mailed statements, or direct communication with loan servicers—is vital for maximizing financial benefits and ensuring compliance with tax regulations.

| Characteristics | Values |

|---|---|

| Form Name | Form 1098-E (Student Loan Interest Statement) |

| Purpose | Reports the amount of interest paid on qualified student loans for tax purposes. |

| Issuer | Lender or loan servicer |

| Recipient | Borrower who paid student loan interest |

| Deadline for Issuance | January 31st (for the previous tax year) |

| Filing Requirement | Not required to file with the IRS; used for tax deductions (Form 1040) |

| Deduction Limit | Up to $2,500 per year (subject to income phase-out limits) |

| Eligibility | Interest paid on qualified education loans for higher education expenses |

| Where to Find | Mailed by the lender or available online via the lender's portal |

| IRS Reference | IRS Topic No. 456 |

| Tax Year Applicability | 2023 (latest data as of October 2023) |

| Income Phase-Out Range | $75,000 to $90,000 (single) / $150,000 to $180,000 (married filing jointly) |

| Electronic Availability | Yes, if provided by the lender |

| Retention Period | Keep with tax records for at least 3 years |

Explore related products

What You'll Learn

![]()

IRS Form 1098-E: Student Loan Interest Statement

IRS Form 1098-E, officially titled the Student Loan Interest Statement, is a crucial document for taxpayers who have paid interest on qualified student loans during the tax year. This form is provided by the lender or loan servicer and reports the amount of interest paid, which may be eligible for a tax deduction. Understanding where to find and how to use Form 1098-E is essential for maximizing potential tax benefits related to student loan interest. If you’re searching for "where is student loan interest form," Form 1098-E is the specific document you need to locate.

To find Form 1098-E, start by checking your email or physical mailbox in January or early February, as lenders are required to send this form to borrowers by January 31st if at least $600 in interest was paid during the tax year. If you haven’t received it by mid-February, log into your student loan account online or contact your loan servicer directly to request a copy. Many lenders also provide access to Form 1098-E through their online portals. If you’re unsure who your loan servicer is, visit the National Student Loan Data System (NSLDS) to retrieve this information.

Once you have Form 1098-E, review Box 1, which shows the total amount of interest paid on your qualified student loans during the year. This figure is critical for claiming the student loan interest deduction on your federal tax return. To claim the deduction, you’ll need to meet certain eligibility criteria, such as having a modified adjusted gross income (MAGI) below specific limits and using the loan solely for qualified education expenses. The deduction can reduce your taxable income by up to $2,500, depending on your income and filing status.

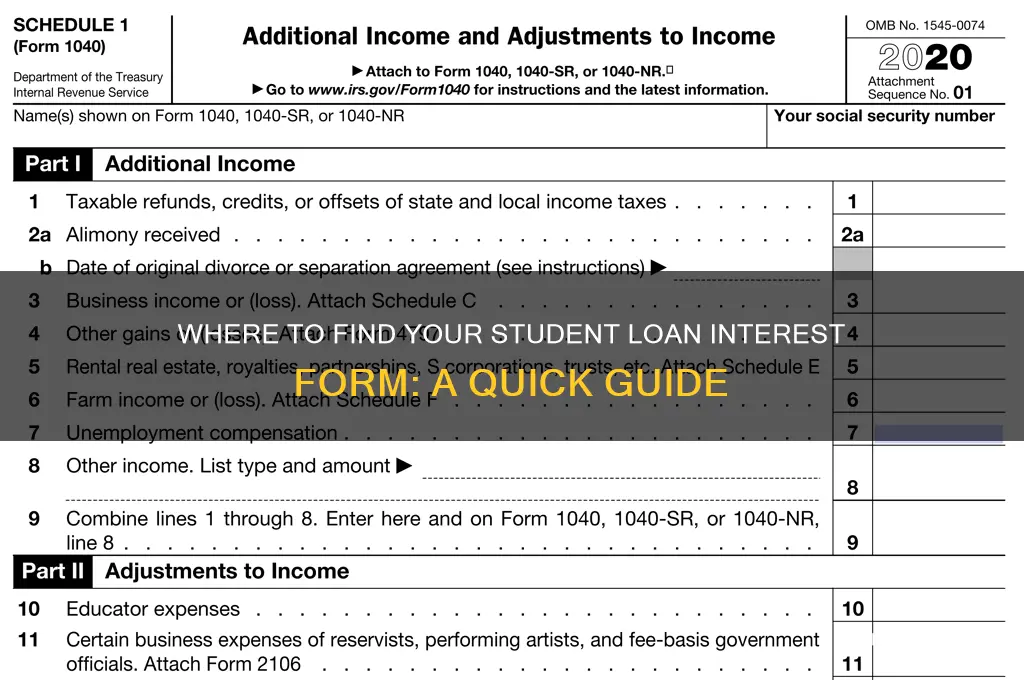

When filing your taxes, you’ll report the interest from Form 1098-E on Schedule 1 of Form 1040. Even if you don’t itemize deductions, you can still claim the student loan interest deduction as an adjustment to income. Ensure you keep a copy of Form 1098-E with your tax records in case the IRS requests verification. If you paid less than $600 in interest and didn’t receive Form 1098-E, you can still claim the deduction if you have documentation of the interest paid, such as monthly statements or an annual summary from your loan servicer.

In summary, IRS Form 1098-E is the key document for reporting student loan interest payments on your tax return. If you’re wondering "where is student loan interest form," it’s typically sent by your lender or accessible through your loan account. By understanding how to locate, review, and use Form 1098-E, you can take full advantage of potential tax savings related to your student loan interest payments. Always consult the IRS guidelines or a tax professional if you have questions about eligibility or filing procedures.

Understanding When Student Loan Interest Accrues and Increases Principal Balance

You may want to see also

Explore related products

![]()

Where to Find Form 1098-E Online

If you're looking for Form 1098-E, the document that reports the amount of student loan interest you've paid during the tax year, there are several places you can find it online. This form is crucial for claiming the student loan interest deduction on your federal tax return, so knowing where to locate it is essential. Here’s a detailed guide to help you find Form 1098-E online.

First, check your student loan servicer’s website. Most loan servicers, such as Navient, Nelnet, or Great Lakes, provide access to tax documents, including Form 1098-E, through their online portals. Log in to your account, navigate to the tax or document section, and look for the option to download or view your 1098-E. Servicers typically make these forms available by January 31st of the following year, so ensure you check after this date if you don’t see it immediately.

If you’re unable to find the form on your loan servicer’s website, consider checking your email inbox. Many servicers send Form 1098-E electronically, so search for emails from your loan provider with subject lines like “Your Tax Form is Available” or “1098-E Statement.” If you opted for paperless communications, the form may have been sent to the email address associated with your loan account.

Another option is to visit the IRS website. While the IRS doesn’t provide your specific 1098-E, they offer a blank version of the form and instructions for filling it out. If you’re unable to obtain the form from your servicer, you can use the interest paid information from your loan statements to manually complete the form. However, this should be a last resort, as using the official form from your servicer is more accurate and convenient.

Lastly, if you’ve refinanced your student loans, check with your new loan provider. When you refinance, the original servicer may no longer be responsible for issuing Form 1098-E. Instead, the new lender will provide the form. Log in to your new account or contact their customer service to ensure you receive the correct document.

In summary, the best places to find Form 1098-E online are your student loan servicer’s website, your email inbox, or directly from your new lender if you’ve refinanced. Always ensure you have this form before filing your taxes to take full advantage of the student loan interest deduction.

Zero Payments on Student Loans: Does Interest Still Accrue?

You may want to see also

Explore related products

![]()

Loan Servicer’s Role in Providing Form 1098-E

Loan servicers play a crucial role in the process of providing Form 1098-E, which is the official document used to report student loan interest paid during the tax year. When a borrower makes payments toward their student loans, a portion of those payments typically goes toward interest, especially in the early years of repayment. The Internal Revenue Service (IRS) allows taxpayers to deduct up to $2,500 of student loan interest paid during the year, provided they meet certain eligibility criteria. This is where the loan servicer’s responsibility comes into play, as they are required to issue Form 1098-E to borrowers who have paid at least $600 in interest during the tax year.

The primary responsibility of loan servicers is to accurately track and report the interest paid by borrowers. Throughout the year, servicers maintain detailed records of each payment, distinguishing between principal and interest amounts. By January 31 of the following year, servicers must mail or electronically provide Form 1098-E to eligible borrowers. This form includes essential information such as the borrower’s name, address, taxpayer identification number, and the total amount of interest paid. It is critical for servicers to ensure the accuracy of this information, as errors can lead to complications for borrowers when filing their taxes.

Borrowers who are unsure where to find their Form 1098-E should first contact their loan servicer. Most servicers provide access to this form through online portals, where borrowers can log in to their accounts and download the document. For those who prefer physical copies, servicers typically mail the form to the address on file. If a borrower has not received Form 1098-E by early February, they should reach out to their servicer directly to request a copy. It is important to note that not all borrowers will receive this form; only those who have paid at least $600 in interest are eligible.

In cases where a borrower has multiple student loans serviced by different companies, they may receive separate Form 1098-E documents from each servicer. Borrowers should ensure they collect all relevant forms to accurately report their total interest paid when filing taxes. Loan servicers are not responsible for consolidating this information across different providers, so it is the borrower’s duty to gather and sum up the interest amounts from all forms received.

Lastly, loan servicers must also be prepared to address borrower inquiries regarding Form 1098-E. This includes clarifying eligibility criteria, explaining the information provided on the form, and resolving any discrepancies. Servicers should have dedicated customer service channels to assist borrowers with questions or issues related to their student loan interest reporting. By fulfilling these responsibilities, loan servicers ensure that borrowers have the necessary documentation to take advantage of potential tax benefits associated with their student loan payments.

Understanding Student Loan Interest Accrual: When Does It Begin?

You may want to see also

Explore related products

![]()

Tax Deduction Eligibility for Student Loan Interest

When it comes to tax deductions for student loan interest, understanding eligibility criteria is crucial for borrowers seeking to maximize their tax benefits. The first step in this process is to locate the necessary form, which is typically the IRS Form 1098-E. This form is specifically designed for reporting student loan interest received by the lender during the tax year. Borrowers should receive this form from their loan servicer by January 31st of the following year, either by mail or electronically, depending on their communication preferences. If you haven't received it by early February, it's advisable to contact your loan servicer directly to request a copy.

To be eligible for the student loan interest deduction, you must meet certain requirements set by the Internal Revenue Service (IRS). Firstly, the interest you're claiming must be on a qualified student loan, which is a loan taken out solely to pay for eligible education expenses. These expenses generally include tuition, fees, room and board, books, supplies, and other necessary costs for enrollment or attendance at an eligible educational institution. It's important to note that the loan must be used for the borrower's own education or for a dependent, such as a child or spouse. Consolidated loans also qualify, as long as the original loans were used for eligible educational expenses.

The IRS has specific guidelines regarding who can claim the deduction. You must be legally obligated to pay the interest on the loan, and your filing status plays a significant role. If you're married, you and your spouse cannot file separate returns and still claim this deduction. Additionally, your income level is a critical factor. For tax year 2023, the deduction is gradually reduced (phased out) if your modified adjusted gross income (MAGI) is between $70,000 and $85,000 ($140,000 and $170,000 if filing a joint return). If your MAGI is above these thresholds, you cannot claim the deduction. It's essential to calculate your MAGI accurately to determine your eligibility.

Another key aspect of eligibility is the time period during which the interest was paid. You can only deduct interest that you actually paid during the tax year, not the amount that accrued. If you made payments under an income-driven repayment plan, the interest that was paid on your behalf by the government may not be deductible. Furthermore, if you prepaid interest in a previous tax year, you generally cannot deduct that amount again in the current year. Understanding these timing rules is vital to ensure you're claiming the correct amount.

Lastly, the educational institution attended with the loan proceeds must be eligible. This includes most accredited universities, colleges, and vocational schools. The school must participate in the Department of Education's student aid programs. If you're unsure about the eligibility of your institution, you can verify it using the Department of Education's database. Keeping detailed records of your loan documents, payment statements, and Form 1098-E is essential for substantiating your deduction in case of an IRS inquiry. By carefully reviewing these eligibility criteria, borrowers can confidently navigate the process of claiming the student loan interest deduction on their tax returns.

Understanding the Federal Student Loan Interest Paid Tax Form

You may want to see also

Explore related products

![]()

What to Do If Form 1098-E Is Missing

If you're expecting Form 1098-E, which reports the amount of student loan interest you paid during the tax year, but haven't received it, don't panic. There are several steps you can take to locate the form or obtain the necessary information for your tax return. First, contact your loan servicer directly. Lenders are required to send Form 1098-E to borrowers who paid at least $600 in student loan interest during the year. If you haven't received it by early February, reach out to your loan servicer's customer service department via phone or email. They can verify whether the form was mailed, provide a copy, or explain any delays.

If contacting your loan servicer doesn't resolve the issue, check your online account portal. Many loan servicers upload tax documents, including Form 1098-E, to their online platforms. Log in to your account and look for a "Tax Documents" or "Statements" section. You may be able to download a digital copy of the form directly from the website. This is often the quickest way to access the information you need without waiting for a physical copy.

In cases where the form is still missing, review your loan statements for the tax year. Even without Form 1098-E, you can calculate the interest paid by examining your monthly or annual loan statements. Add up the interest payments made throughout the year to determine the total. While this method requires more effort, it ensures you have the correct amount to claim on your tax return. Keep these statements as proof in case of an audit.

If all else fails, contact the IRS for guidance. The IRS can provide advice on how to proceed if you're unable to obtain Form 1098-E. You may need to file your taxes using the interest amount from your records and include a note explaining the situation. The IRS can also help you request a copy of the form if it was filed electronically by your lender. Be prepared to provide your loan account details and tax identification information when reaching out.

Finally, consider filing for an extension if you're unable to gather the necessary information in time for the tax deadline. Filing Form 4868 grants you an additional six months to submit your return. This gives you more time to track down Form 1098-E or compile your loan statements. However, remember that an extension to file does not extend the deadline to pay any taxes owed, so estimate and pay any expected tax liability to avoid penalties.

Understanding When Your Student Loan Accrues Interest: A Comprehensive Guide

You may want to see also

Frequently asked questions

The student loan interest form, typically Form 1098-E, is usually provided by your loan servicer. You can access it through your online account or request it directly from them. It is also often mailed to you by January 31st each year.

If you haven’t received Form 1098-E by mid-February, contact your loan servicer to request a copy. You can also log into your loan account online to download it. If you’re unable to obtain it, you can still report the interest paid using other documentation, such as your loan statements.

While having Form 1098-E is helpful, it’s not mandatory to file your taxes. You can still claim the student loan interest deduction using the total interest paid, which can be found on your loan statements or by contacting your loan servicer. However, the form ensures accuracy and simplifies the process.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)