The Student Loan Interest Paid Federal Form, officially known as Form 1098-E, is a crucial document for borrowers who have paid interest on qualified student loans during the tax year. Issued by lenders, this form reports the total amount of interest paid, which can be claimed as a deduction on federal income tax returns, potentially reducing taxable income. Understanding and properly utilizing Form 1098-E is essential for eligible taxpayers to maximize their tax benefits while managing student loan debt.

Explore related products

What You'll Learn

- Eligibility Criteria: Who can claim the student loan interest deduction on federal tax forms

- Deduction Limits: Maximum amount of student loan interest deductible annually on federal taxes

- Form 1098-E: Purpose and details of the form for reporting student loan interest payments

- Income Phaseouts: Income thresholds affecting eligibility for the student loan interest deduction

- Filing Instructions: How to correctly report student loan interest on federal tax returns

![]()

Eligibility Criteria: Who can claim the student loan interest deduction on federal tax forms

The student loan interest deduction is a valuable tax benefit for individuals who have taken out loans to finance their education or that of their dependents. To claim this deduction on federal tax forms, specifically on Schedule 1 of Form 1040, taxpayers must meet certain eligibility criteria. First and foremost, the taxpayer must have paid interest on a qualified student loan during the tax year. A qualified student loan is one taken out solely to pay for education expenses, such as tuition, fees, room and board, books, and other necessary supplies, for the taxpayer, their spouse, or dependents. The loan must have been used for attendance at an eligible educational institution, which includes most accredited colleges, universities, and vocational schools.

One of the key eligibility requirements is that the taxpayer must be legally obligated to pay the interest on the student loan. This means that if a parent took out a loan for their child’s education, only the parent can claim the deduction, not the child, unless the child is the one legally responsible for repaying the loan. Additionally, the taxpayer’s filing status plays a crucial role in determining eligibility. For example, if married, the couple must file a joint return to claim the deduction. Those who file as "married filing separately" are not eligible for this deduction.

Income limits are another critical factor in determining eligibility for the student loan interest deduction. The deduction is phased out for taxpayers with modified adjusted gross income (MAGI) above certain thresholds. As of the latest guidelines, the phase-out begins at $70,000 for single filers and $140,000 for married couples filing jointly, with the deduction completely phased out at $85,000 for single filers and $170,000 for married couples filing jointly. Taxpayers whose MAGI exceeds these limits are not eligible to claim the deduction.

The taxpayer or their spouse must also have been enrolled in an eligible course of study at least half-time during the academic period when the loan was issued. This requirement ensures that the loan was directly related to education expenses. Furthermore, the loan must have been taken out from a qualified lender, such as a bank, credit union, or the federal government. Loans from related parties, such as family members, do not qualify for this deduction.

Lastly, the student loan interest deduction is only available for interest payments made during the tax year, not for the repayment of the loan principal. Taxpayers must have received a Form 1098-E from their lender, which reports the amount of interest paid during the year. If the taxpayer did not receive this form but still paid interest, they should contact their lender to obtain the necessary documentation. Meeting all these eligibility criteria allows taxpayers to claim the student loan interest deduction, potentially reducing their taxable income by up to $2,500, depending on their income level and the amount of interest paid.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Deduction Limits: Maximum amount of student loan interest deductible annually on federal taxes

The student loan interest deduction is a valuable tax benefit for borrowers who are repaying qualifying education loans. This deduction allows taxpayers to reduce their taxable income by the amount of interest paid on eligible student loans during the tax year. However, it’s important to understand that this deduction is subject to certain limits, including a maximum annual amount that can be claimed. For the most recent tax years, the maximum amount of student loan interest deductible annually on federal taxes is $2,500. This limit applies regardless of the actual amount of interest paid, meaning if you paid more than $2,500 in interest, you can only deduct up to that cap.

The $2,500 maximum deduction is not indexed for inflation, so it remains constant unless adjusted by legislation. This means that as interest rates or loan balances increase, the proportion of interest that can be deducted may decrease relative to the total interest paid. Additionally, the deduction is phased out for taxpayers with higher incomes, further limiting its availability for some borrowers. For single filers, the phaseout begins at a modified adjusted gross income (MAGI) of $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phaseout starts at $140,000 and ends at $170,000.

It’s crucial to note that the student loan interest deduction is an "above-the-line" deduction, meaning it can be claimed even if you don’t itemize deductions on your tax return. This makes it accessible to a broader range of taxpayers. However, the deduction cannot exceed the actual amount of interest paid during the year, and it must be for a qualified education loan used for eligible educational expenses. Loans from family members or qualified employer plans generally do not qualify for this deduction.

To claim the deduction, taxpayers must receive a Form 1098-E from their loan servicer, which reports the amount of interest paid during the year. If the form is not provided, borrowers can still claim the deduction if they have documentation of the interest paid. The deduction is reported on IRS Form 1040, Schedule 1, line 21, and then transferred to Form 1040. Understanding these limits and requirements ensures that borrowers maximize their tax benefits while staying compliant with federal tax laws.

Lastly, it’s important to consider how the student loan interest deduction interacts with other tax benefits, such as the American Opportunity Credit or Lifetime Learning Credit. Taxpayers cannot claim the deduction for interest on a loan for which the proceeds were used to pay qualified education expenses if they also claim a tuition tax credit for the same student in the same year. This rule prevents double-dipping but requires careful planning to optimize tax savings. By staying informed about deduction limits and eligibility rules, borrowers can effectively manage their student loan interest payments and reduce their tax liability.

Understanding the Phase-Out of Student Loan Interest Deduction: What You Need to Know

You may want to see also

Explore related products

![]()

Form 1098-E: Purpose and details of the form for reporting student loan interest payments

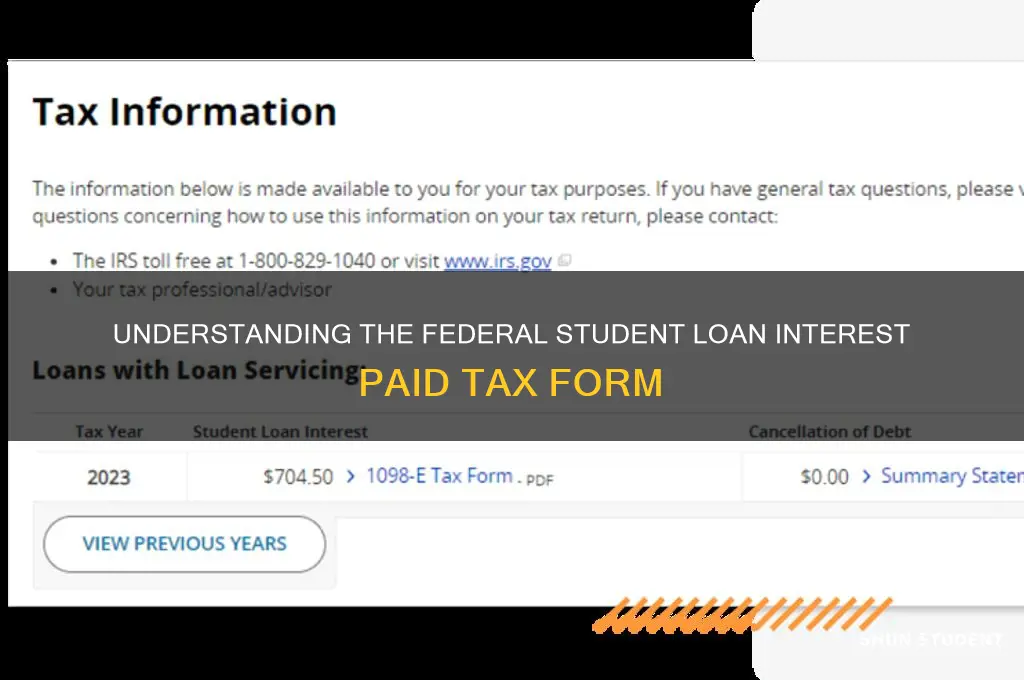

Form 1098-E is a crucial document used for reporting student loan interest payments made during the tax year. Its primary purpose is to provide both the borrower and the Internal Revenue Service (IRS) with accurate information regarding the amount of interest paid on qualified student loans. This form is essential for taxpayers who wish to claim the Student Loan Interest Deduction, a tax benefit that allows eligible borrowers to deduct up to $2,500 of the interest paid on their student loans, depending on their income and filing status. By reporting this information, Form 1098-E ensures compliance with tax regulations and helps borrowers maximize their potential deductions.

The details included on Form 1098-E are specific and structured to provide clear information. The form includes the borrower’s name, address, and taxpayer identification number (usually a Social Security Number), as well as the lender’s name and federal identification number. The most critical piece of information is the total amount of interest paid on the student loan during the tax year, which is reported in Box 1. Additionally, if the borrower paid any fees treated as interest, these amounts are also included. It’s important to note that only interest payments on qualified student loans—those used for higher education expenses—are reported on this form. Personal loans or loans for non-educational purposes are not eligible.

Who receives Form 1098-E and when it is issued are key aspects of its function. Lenders or loan servicers are required to send this form to borrowers by January 31 of the year following the tax year in which the interest was paid. For example, if interest was paid in 2023, the borrower should receive Form 1098-E by January 31, 2024. Borrowers who paid at least $600 in student loan interest during the year will receive this form. If a borrower does not receive the form but believes they qualify, they should contact their loan servicer to request it. The IRS also receives a copy of Form 1098-E, ensuring that the reported interest payments align with the borrower’s tax return.

How to use Form 1098-E for tax purposes is straightforward but requires attention to detail. When filing taxes, borrowers should refer to the amount reported in Box 1 of Form 1098-E to claim the Student Loan Interest Deduction. This deduction is reported on Schedule 1 (Form 1040), line 21, and is then transferred to Form 1040. It’s important to ensure eligibility for the deduction, as income limits and other restrictions apply. For instance, the deduction phases out for taxpayers with modified adjusted gross incomes above certain thresholds. Borrowers who are claimed as dependents on someone else’s tax return cannot claim this deduction.

In summary, Form 1098-E plays a vital role in the tax process for student loan borrowers by accurately reporting interest payments and enabling them to claim potential deductions. Understanding its purpose, details, and usage ensures that borrowers can take full advantage of available tax benefits while maintaining compliance with IRS regulations. By keeping track of this form and using it correctly, borrowers can effectively manage their tax obligations related to student loan interest payments.

Understanding Income Limits for Claiming Student Loan Interest Deductions

You may want to see also

Explore related products

![1099 NEC Forms 2024, 50 Pack 4 Part Laser Tax Forms Kit Pack of Federal/State Copy's, 1096's –Great for QuickBooks and Accounting Software, [NO Envelopes] 2024 1099-NEC, 50 Pack](https://m.media-amazon.com/images/I/81BpoWshMvL._AC_UY218_.jpg)

![]()

Income Phaseouts: Income thresholds affecting eligibility for the student loan interest deduction

The student loan interest deduction is a valuable tax benefit for borrowers who are repaying eligible education loans. However, not all borrowers qualify for this deduction, as it is subject to income phaseouts. Income phaseouts refer to the income thresholds that determine whether a taxpayer is eligible to claim the student loan interest deduction and, if eligible, the amount they can deduct. These phaseouts are designed to limit the benefit to lower- and middle-income borrowers, gradually reducing or eliminating the deduction as income rises.

For tax year 2023, the income phaseouts for the student loan interest deduction are based on the taxpayer's modified adjusted gross income (MAGI). Single filers with a MAGI above $70,000 and joint filers with a MAGI above $145,000 begin to phase out of eligibility. The deduction is completely phased out for single filers with a MAGI above $85,000 and joint filers with a MAGI above $175,000. It's important to note that these thresholds are adjusted annually for inflation, so borrowers should verify the current year's limits when filing their taxes. Taxpayers whose income falls within the phaseout range can claim a partial deduction, calculated based on where their income falls within the specified thresholds.

The phaseout calculation reduces the maximum deductible amount of $2,500 proportionally as income increases within the phaseout range. For example, a single filer with a MAGI of $75,000—midway through the phaseout range—would be eligible for half of the maximum deduction, or $1,250. This proportional reduction continues until the deduction is fully phased out at the upper income limit. Borrowers should use the worksheet provided in the IRS instructions for Form 1040 or tax software to accurately calculate their eligible deduction based on their income level.

It's crucial for taxpayers to understand that the student loan interest deduction is an "above-the-line" deduction, meaning it can be claimed even if the taxpayer does not itemize deductions. However, the income phaseouts make it unavailable to higher-income earners. Additionally, married couples filing separately are not eligible for this deduction, regardless of their income level. Borrowers should also ensure that the interest they are deducting was paid on a qualified education loan used for eligible higher education expenses, as outlined in IRS guidelines.

To claim the student loan interest deduction, borrowers must receive a Form 1098-E from their loan servicer, which reports the amount of interest paid during the tax year. This form is essential for accurately reporting the deduction on the federal tax return. Taxpayers who do not receive a Form 1098-E but have paid eligible interest can still claim the deduction by manually calculating the amount and ensuring it meets IRS criteria. Understanding the income phaseouts and eligibility rules is key to maximizing this tax benefit while avoiding errors that could trigger an IRS audit.

Understanding the Latest Interest Rate Changes for Student Loans

You may want to see also

Explore related products

![]()

Filing Instructions: How to correctly report student loan interest on federal tax returns

When filing your federal tax returns, correctly reporting student loan interest paid can help you claim a valuable deduction. The form you’ll need is Form 1098-E, Student Loan Interest Statement, which is provided by your loan servicer if you paid $600 or more in interest during the tax year. This form details the amount of interest you paid, which is eligible for the student loan interest deduction. If you don’t receive Form 1098-E but still paid interest, you can contact your loan servicer to obtain the necessary information. Ensure you have this form or the interest amount before starting your tax return.

To report student loan interest on your federal tax return, you’ll use Schedule 1 (Form 1040), which is an additional form attached to your main tax return (Form 1040). On Schedule 1, look for Line 21, labeled "Student loan interest deduction." Enter the total amount of interest you paid during the tax year, as reported on Form 1098-E or provided by your loan servicer. This amount will then transfer to your Form 1040, reducing your taxable income. It’s important to note that the student loan interest deduction is an "above-the-line" deduction, meaning you can claim it even if you don’t itemize deductions.

Before claiming the deduction, ensure you meet the eligibility criteria. The interest must have been paid on a qualified student loan used for higher education expenses, such as tuition, fees, room, and board. Additionally, your income must fall within certain limits, as the deduction is phased out for higher-income taxpayers. For example, in 2023, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $75,000 and is completely phased out at $90,000. For married filing jointly, the phaseout range is $150,000 to $180,000. Verify your eligibility to avoid errors.

If you’re using tax software or working with a tax professional, the process of reporting student loan interest is typically streamlined. Most tax software programs will prompt you to enter the interest amount from Form 1098-E, and they’ll automatically calculate the deduction for you. However, it’s still crucial to double-check the entered amount for accuracy. If filing manually, carefully transfer the interest amount from Form 1098-E to Schedule 1 and then to Form 1040. Mistakes in reporting can delay your refund or trigger an IRS inquiry.

Finally, keep all documentation related to your student loan interest payments, including Form 1098-E and any correspondence with your loan servicer. These records are essential in case the IRS requests verification of your deduction. By following these filing instructions and ensuring accuracy, you can correctly report your student loan interest on your federal tax return and maximize your potential tax savings. Always consult the IRS instructions or a tax professional if you have questions about your specific situation.

Understanding the Refundable Student Loan Interest Amount: A Comprehensive Guide

You may want to see also

Frequently asked questions

The Student Loan Interest Paid Federal Form, officially known as Form 1098-E, is a tax document that reports the amount of interest you paid on qualified student loans during the tax year. It is provided by the lender or loan servicer and is used to claim the student loan interest deduction on your federal tax return.

You are eligible to receive Form 1098-E if you paid $600 or more in interest on a qualified student loan during the tax year. The form is typically sent to you by your loan servicer or lender by January 31st of the following year.

You can use the information from Form 1098-E to claim the student loan interest deduction on your federal tax return. This deduction can reduce your taxable income, potentially lowering your tax liability. You’ll report the interest paid on Schedule 1 (Form 1040) and then transfer the amount to your Form 1040.

If you paid $600 or more in student loan interest and did not receive Form 1098-E by early February, contact your loan servicer or lender to request it. If they cannot provide the form, you can still claim the deduction by using your loan statements or online account to verify the amount of interest paid and report it on your tax return.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)