The question of which company will take over federal student loans under the DeVos administration has sparked significant debate and concern among borrowers and policymakers alike. During her tenure as Secretary of Education, Betsy DeVos implemented several changes to the federal student loan system, including the rollback of borrower protections and the privatization of certain loan servicing functions. Speculation has arisen regarding which private companies might be positioned to take on a larger role in managing federal student loans, potentially shifting the landscape of student debt repayment and raising questions about accountability, transparency, and the long-term impact on borrowers.

Explore related products

What You'll Learn

- Navient's role in federal student loan servicing under DeVos' leadership

- Impact of DeVos policies on loan forgiveness programs for borrowers

- Federal Student Aid (FSA) oversight changes during DeVos' tenure

- DeVos' stance on privatizing federal student loan servicing contracts

- Consequences of DeVos' policies on student loan debt collection practices

![]()

Navient's role in federal student loan servicing under DeVos' leadership

Under Betsy DeVos's leadership as Secretary of Education, Navient, one of the largest federal student loan servicers, faced heightened scrutiny and legal challenges. DeVos's decision to roll back Obama-era regulations aimed at protecting borrowers from predatory practices sparked controversy, particularly regarding Navient’s role. During her tenure, the Department of Education ceased sharing information with the Consumer Financial Protection Bureau (CFPB), which had been investigating Navient for alleged misconduct, including mismanaging payments and steering borrowers into costlier repayment plans. This move effectively shielded Navient from federal oversight, raising questions about DeVos’s commitment to borrower protection.

Analyzing Navient’s operations during this period reveals a pattern of borrower complaints and legal battles. For instance, in 2017, the CFPB and several states sued Navient for systemic failures in loan servicing, accusing the company of violating consumer protection laws. Despite these allegations, DeVos’s Department of Education continued to award Navient contracts, citing a lack of evidence to terminate their role as a servicer. This decision underscored a broader shift in policy priorities, favoring servicers over borrowers and prioritizing cost-cutting over accountability.

From a practical standpoint, borrowers dealing with Navient under DeVos’s leadership faced significant challenges. Many reported difficulties accessing income-driven repayment plans, receiving inaccurate billing statements, and experiencing delays in processing payments. To navigate these issues, borrowers were advised to document all communications with Navient, verify payment allocations, and file complaints with the Federal Student Aid Ombudsman if necessary. Additionally, exploring loan consolidation or switching servicers became a strategic move for some, though options were limited due to DeVos’s policies.

Comparatively, DeVos’s approach to Navient contrasted sharply with previous administrations. While the Obama administration sought to hold servicers accountable and improve borrower outcomes, DeVos’s tenure marked a retreat from these efforts. This shift had tangible consequences: Navient remained a dominant player in the student loan servicing market, despite ongoing litigation and widespread criticism. Borrowers, particularly those with limited financial literacy, were left vulnerable to mismanagement and predatory practices, highlighting the need for stronger regulatory frameworks.

In conclusion, Navient’s role in federal student loan servicing under DeVos’s leadership exemplifies the tension between industry interests and borrower protections. DeVos’s policies not only shielded Navient from accountability but also perpetuated systemic issues in loan servicing. For borrowers, this era underscored the importance of vigilance, advocacy, and proactive measures to safeguard their financial well-being. As the student loan landscape continues to evolve, the lessons from this period serve as a cautionary tale about the consequences of prioritizing servicers over the millions of Americans burdened by student debt.

Tim Walz's Daughter and Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Impact of DeVos policies on loan forgiveness programs for borrowers

Betsy DeVos' tenure as Secretary of Education under the Trump administration brought significant changes to federal student loan policies, particularly regarding loan forgiveness programs. One of her most notable actions was the overhaul of the Borrower Defense to Repayment (BDR) program, which was designed to provide debt relief to students defrauded by predatory colleges. DeVos tightened eligibility criteria, slowed processing times, and reduced the amount of relief granted, leaving thousands of borrowers in limbo. For instance, while the Obama administration approved over $550 million in BDR claims in its final year, DeVos' Department of Education approved only $12 million in her first two years. This drastic reduction highlights the immediate impact of her policies on borrowers seeking relief.

DeVos also targeted the Public Service Loan Forgiveness (PSLF) program, which promises debt forgiveness to borrowers who work in public service and make 120 qualifying payments. Her department introduced stricter verification processes and denied applications for minor technicalities, such as incorrect payment counts or loan type mismatches. A 2019 Government Accountability Office report revealed that only 1% of PSLF applicants had their loans forgiven under DeVos' leadership, compared to 27% in the program’s early years. This suggests a deliberate effort to limit access to forgiveness, burdening public servants with unsustainable debt.

Another area affected by DeVos' policies was income-driven repayment (IDR) plans, which tie monthly payments to borrowers' earnings and promise forgiveness after 20–25 years. Her department failed to properly track qualifying payments, leading to widespread confusion and miscalculations. For example, a 2021 audit found that 98% of borrowers in IDR plans had not received credit for payments that should have counted toward forgiveness. This systemic failure exacerbated financial strain for low-income borrowers, who were promised relief but faced bureaucratic hurdles instead.

DeVos' policies also reflected a broader ideological shift away from borrower protection and toward industry interests. Her rollback of gainful employment rules, which held for-profit colleges accountable for graduates' debt-to-earnings ratios, allowed predatory institutions to continue operating without oversight. This decision, combined with her resistance to automatic loan discharges for disabled borrowers, signaled a prioritization of profit over people. The cumulative effect of these policies was a student loan system increasingly hostile to borrowers, with forgiveness programs rendered nearly inaccessible.

For borrowers navigating this landscape, practical steps include meticulously documenting all payments and communications with loan servicers, especially for PSLF and IDR plans. Advocacy groups like the Student Borrower Protection Center offer resources to challenge denials and hold servicers accountable. Additionally, staying informed about legislative efforts to reverse DeVos-era policies, such as the proposed expansion of PSLF under the Biden administration, can provide hope for future relief. While DeVos' legacy complicates the path to forgiveness, proactive measures and collective action remain essential tools for borrowers seeking justice.

Public Service Loan Forgiveness: Are Applications Finally Getting Approved?

You may want to see also

Explore related products

![]()

Federal Student Aid (FSA) oversight changes during DeVos' tenure

During Betsy DeVos's tenure as Secretary of Education, Federal Student Aid (FSA) oversight underwent significant changes, many of which sparked controversy and debate. One of the most notable shifts was the rollback of Obama-era regulations aimed at holding predatory for-profit colleges accountable. DeVos's Department of Education delayed and ultimately rescinded the "gainful employment" rule, which cut federal funding to career education programs whose graduates struggled to repay student loans. This move was criticized for prioritizing the interests of for-profit institutions over student protections, leaving vulnerable borrowers at risk of exploitation.

Another key change was DeVos's restructuring of the FSA office itself. She appointed high-ranking officials with ties to the student loan industry, raising concerns about conflicts of interest. For instance, the hiring of Robert Eitel, a former executive at for-profit college operator Career Education Corporation, as a senior advisor drew scrutiny. Critics argued that such appointments undermined FSA's ability to act as an impartial watchdog, instead aligning it more closely with industry interests than those of borrowers.

DeVos also halted investigations into predatory lending practices and scaled back enforcement actions against fraudulent institutions. For example, the Department of Education stopped approving debt relief claims for students defrauded by Corinthian Colleges and other for-profit schools. This decision left thousands of borrowers in limbo, unable to access the loan forgiveness they were legally entitled to under the "borrower defense to repayment" program. Advocacy groups and lawmakers accused DeVos of abandoning her duty to protect students, instead shielding companies from accountability.

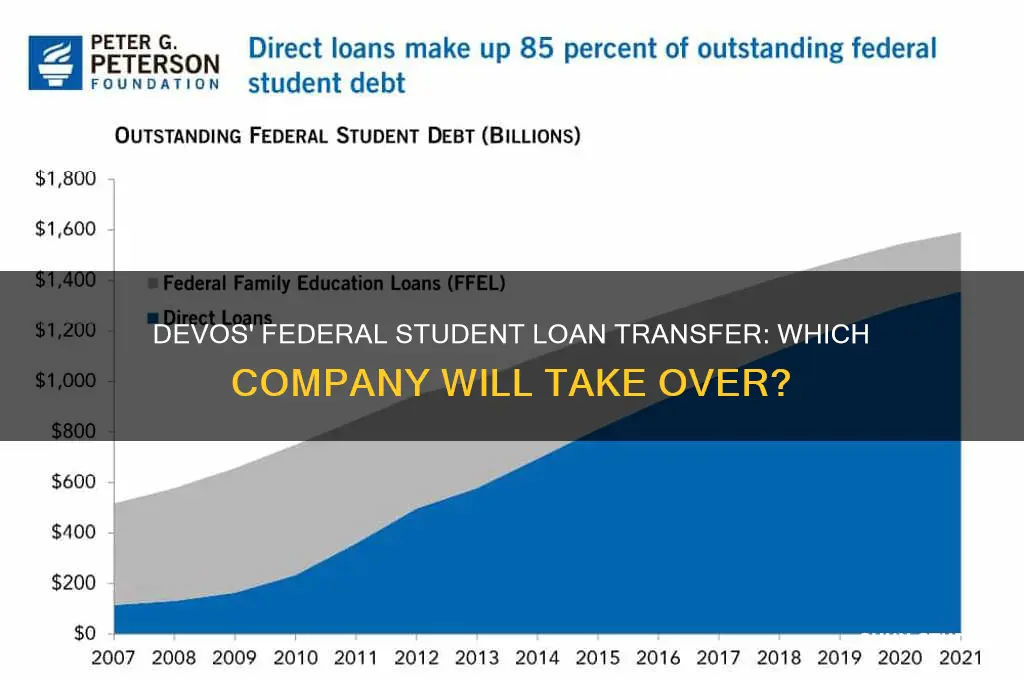

A comparative analysis reveals that DeVos's approach to FSA oversight marked a stark departure from her predecessors. While previous administrations sought to strengthen borrower protections and hold institutions accountable, DeVos's policies often favored deregulation and industry interests. This shift had tangible consequences: student loan debt continued to soar, reaching $1.7 trillion by the end of her tenure, while borrower protections were systematically dismantled. The takeaway is clear—DeVos's changes to FSA oversight prioritized institutional profit over student welfare, leaving a legacy of weakened accountability and heightened risk for borrowers.

To navigate this landscape, borrowers must take proactive steps. First, stay informed about changes to federal student loan policies and protections. Second, explore alternative repayment plans or loan forgiveness programs that may still be available. Finally, advocate for stronger oversight and accountability in the student loan industry, as DeVos's tenure underscored the need for systemic reform to protect future generations of students.

Navigating Student Debt Forgiveness: Where and How to Apply Now

You may want to see also

Explore related products

![]()

DeVos' stance on privatizing federal student loan servicing contracts

Betsy DeVos, during her tenure as Secretary of Education, championed the privatization of federal student loan servicing contracts, arguing that market competition would improve efficiency and borrower experience. Her stance aligned with broader Trump administration efforts to reduce the federal government’s role in education and financial services. DeVos criticized the existing system, managed by companies like Navient and FedLoan Servicing, for poor customer service and borrower confusion, suggesting private sector innovation could address these issues. However, critics argued that privatization risked prioritizing profit over borrower welfare, potentially exacerbating student debt challenges.

To understand DeVos’s approach, consider her 2017 decision to halt Obama-era regulations aimed at holding loan servicers accountable for misconduct. She framed this as removing unnecessary red tape, but it also cleared the path for private companies to operate with less oversight. DeVos’s Department of Education sought to streamline the loan servicing process by consolidating contracts under fewer vendors, a move she claimed would simplify operations. For instance, in 2019, the department awarded a major contract to Missouri Higher Education Loan Authority (MOHELA), signaling a shift toward fewer, larger private servicers.

A key takeaway from DeVos’s strategy is her belief in private companies’ ability to outperform federal entities in servicing loans. She pointed to examples like Great Lakes Educational Loan Services, which had a reputation for better borrower support before its contract ended in 2021. However, this approach overlooked systemic issues, such as servicers’ financial incentives to minimize costs, which could undermine borrower assistance. For instance, a 2018 Government Accountability Office report found that servicers often failed to inform borrowers about income-driven repayment plans, a problem privatization did not inherently solve.

Borrowers navigating DeVos’s privatized landscape should take proactive steps to protect themselves. First, monitor communications from servicers closely, as transitions between companies (e.g., from FedLoan to MOHELA) often led to lost paperwork or payment errors. Second, use third-party tools like the Consumer Financial Protection Bureau’s complaint database to report issues. Finally, consider refinancing with private lenders if terms are favorable, though this forfeits federal protections like loan forgiveness. DeVos’s legacy in this area underscores the need for vigilance in a system increasingly tilted toward private interests.

Student Loan Payments Resume: What Borrowers Need to Know Now

You may want to see also

Explore related products

![]()

Consequences of DeVos' policies on student loan debt collection practices

Betsy DeVos' tenure as Secretary of Education saw significant shifts in federal student loan debt collection practices, with far-reaching consequences for borrowers. One key change was the rollback of Obama-era regulations that held loan servicers accountable for fair and transparent practices. Under DeVos, companies like Navient and FedLoan Servicing faced fewer restrictions, leading to increased reports of mismanagement, incorrect billing, and aggressive collection tactics. This environment allowed servicers to prioritize profits over borrower welfare, exacerbating financial strain for millions of students.

Consider the case of Navient, which faced a 2017 lawsuit from the Consumer Financial Protection Bureau (CFPB) for systematically steering borrowers into costly repayment plans. DeVos' Department of Education not only refused to cooperate with the CFPB but also halted investigations into similar servicer misconduct. This hands-off approach emboldened collectors, leaving borrowers with limited recourse against predatory practices. For instance, borrowers in income-driven repayment plans often found themselves incorrectly billed or pushed into default due to servicer errors, resulting in wage garnishments and damaged credit scores.

DeVos' policies also expanded the role of private collection agencies in federal student loan debt recovery. These agencies, operating under contracts worth hundreds of millions of dollars, were incentivized to maximize collections through aggressive tactics like frequent calls, threats of legal action, and excessive fees. Unlike federal servicers, these agencies were not bound by the same borrower protections, creating a Wild West scenario for debt collection. Borrowers, particularly those from low-income backgrounds, faced disproportionate harm, as they often lacked the resources to challenge these practices or navigate complex repayment options.

A critical takeaway is the long-term impact on financial stability and mental health. Studies show that aggressive debt collection correlates with increased stress, anxiety, and even depression among borrowers. DeVos' policies, by enabling such practices, contributed to a cycle of financial insecurity that hindered borrowers' ability to build wealth, purchase homes, or invest in their futures. For example, a 2020 survey found that 40% of student loan borrowers delayed major life decisions due to debt-related stress, a statistic that underscores the human cost of these policy changes.

To mitigate these consequences, borrowers should proactively document all communications with servicers and collection agencies, ensuring a paper trail for disputes. Utilizing resources like the Student Loan Ombudsman or nonprofit counseling services can also provide guidance in navigating repayment options and challenging unfair practices. While DeVos' policies created a challenging landscape, informed and assertive action remains a borrower's best defense against predatory debt collection.

Will AGI Determine Your Student Loan Forgiveness Eligibility?

You may want to see also

Frequently asked questions

There is no single company taking over federal student loans under Betsy DeVos. Federal student loans are managed by loan servicers contracted by the U.S. Department of Education, and changes in administration do not typically involve a complete takeover by one company.

No, Betsy DeVos did not privatize federal student loans to a specific company. Federal student loans remain government-owned, and servicers are contracted to manage them, not own them.

No, federal student loans were not transferred to a new company under DeVos’s leadership. Loan servicers may change periodically, but the loans remain under the oversight of the U.S. Department of Education.