The question of whether student loan forgiveness will be based on Adjusted Gross Income (AGI) has become a central point of discussion as policymakers and borrowers alike seek clarity on potential relief programs. AGI, a key metric used by the IRS to determine tax liabilities, could serve as a basis for eligibility in student loan forgiveness initiatives, ensuring that relief is targeted toward those with the greatest financial need. While no definitive framework has been established, proposals and existing programs, such as income-driven repayment plans, often consider AGI to assess borrowers' ability to repay their loans. As debates continue over the fairness and feasibility of broad-scale forgiveness, tying eligibility to AGI could balance the need for relief with fiscal responsibility, though critics argue it may exclude some borrowers who still face significant financial strain.

| Characteristics | Values |

|---|---|

| Basis for Forgiveness Eligibility | Adjusted Gross Income (AGI) is a key factor in determining eligibility for student loan forgiveness under certain programs, such as the Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans. |

| Income Thresholds | For IDR plans, monthly payments are capped at a percentage of discretionary income, which is calculated based on AGI. Forgiveness typically occurs after 20-25 years of qualifying payments, depending on the plan. |

| PSLF AGI Consideration | While AGI does not directly determine PSLF eligibility, it influences the borrower's ability to make qualifying payments under an IDR plan, which is often a prerequisite for PSLF. |

| Tax Implications | Forgiven amounts under IDR plans may be considered taxable income, though the American Rescue Plan Act of 2021 temporarily exempts forgiven student loans from federal taxation through 2025. |

| Recent Policy Updates | As of the latest data, there is no broad-based student loan forgiveness program explicitly tied to AGI, but AGI remains crucial for IDR plan calculations and PSLF eligibility. |

| Biden Administration's Plan | The Biden administration's targeted loan forgiveness initiatives (e.g., $10,000 to $20,000 for eligible borrowers) were not directly based on AGI but had income caps for eligibility ($125,000 for individuals, $250,000 for couples). These plans are currently paused due to legal challenges. |

| State-Specific Programs | Some state-based forgiveness programs may consider AGI or income thresholds, but these vary widely and are not standardized. |

| Future Legislation | Proposals for broader forgiveness based on AGI or income are under discussion but have not been enacted as of the latest data. |

Explore related products

What You'll Learn

![]()

AGI Thresholds for Eligibility

Adjusted Gross Income (AGI) thresholds are a critical factor in determining eligibility for student loan forgiveness programs, particularly those tied to income-driven repayment plans or targeted relief initiatives. For instance, the Biden administration’s 2022 student loan forgiveness plan proposed canceling up to $20,000 in debt for borrowers earning below $125,000 (individuals) or $250,000 (married couples) based on 2020 or 2021 tax returns. These thresholds were designed to target relief toward lower- and middle-income borrowers, ensuring that higher earners did not benefit disproportionately. Understanding how AGI is calculated—by subtracting certain deductions from gross income—is essential, as it directly impacts eligibility.

From a practical standpoint, borrowers should review their tax filings to confirm their AGI, as this figure is not always intuitive. For example, contributions to retirement accounts or student loan interest payments can lower AGI, potentially qualifying someone for forgiveness who might otherwise exceed the threshold. Additionally, married couples filing jointly must consider their combined income, which can complicate eligibility if one spouse earns significantly more. Proactive steps, such as consulting a tax professional or using IRS tools to estimate AGI, can help borrowers determine their standing before applying for relief.

Critics argue that AGI thresholds, while well-intentioned, may exclude borrowers who face high living costs in expensive urban areas or carry substantial non-student debt. For instance, a borrower earning $130,000 in San Francisco might struggle with affordability despite exceeding the forgiveness threshold. This highlights the tension between creating a universal standard and accounting for regional economic disparities. Policymakers could address this by adjusting thresholds based on cost-of-living indices or introducing exceptions for borrowers with high debt-to-income ratios.

Comparatively, AGI-based eligibility differs from means-testing in other social programs, such as Medicaid or SNAP, which often consider household size and assets. Student loan forgiveness programs have thus far relied solely on income, which may overlook borrowers with modest earnings but significant financial obligations. Incorporating additional criteria, such as household size or local living costs, could create a more nuanced approach. However, this would also increase administrative complexity, potentially delaying relief for those in urgent need.

In conclusion, AGI thresholds serve as a straightforward yet imperfect tool for determining student loan forgiveness eligibility. Borrowers must carefully assess their financial situation, leveraging deductions to lower their AGI if possible. Meanwhile, policymakers should consider refining these thresholds to better reflect economic realities, ensuring that relief reaches those who need it most without undue complexity. As student debt continues to burden millions, the fairness and efficacy of AGI-based eligibility will remain a central issue in the debate over loan forgiveness.

Oregon's Tax Implications for Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![Reproductions by the Collotype Process of Some of the Works in the Loan Exhibition of Pictures, Held in the Art Gallery of the Corporation of London, at the Guildhall, 1892 : 1892 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Impact of AGI on Forgiveness Amounts

Adjusted Gross Income (AGI) plays a pivotal role in determining eligibility and forgiveness amounts for student loan relief programs. For instance, under the Public Service Loan Forgiveness (PSLF) program, AGI indirectly influences repayment plans like income-driven repayment (IDR), which can reduce monthly payments and ultimately the forgiven amount. Borrowers with lower AGI often qualify for lower payments, potentially extending their repayment term but minimizing the taxable forgiven sum. Conversely, higher AGI borrowers may face larger payments, shortening their repayment period but increasing the forgiven amount at the end of the term.

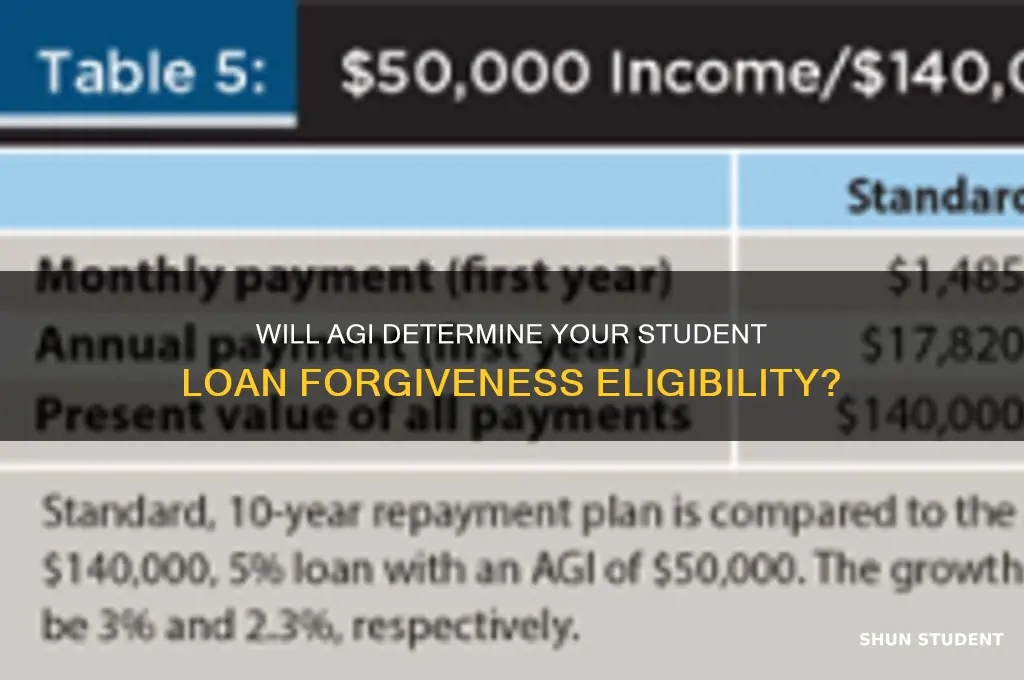

Consider the mechanics of income-driven repayment plans, which cap monthly payments at a percentage of discretionary income (typically 10-20% of AGI above the poverty line). For example, a borrower earning $40,000 annually with $100,000 in debt might pay $200 monthly under an IDR plan, compared to $1,000 under a standard plan. Over 20-25 years, the IDR plan could result in $48,000-$60,000 in payments, with the remaining $40,000-$52,000 forgiven. AGI fluctuations during this period—due to raises, bonuses, or side income—can recalibrate payments annually, directly impacting the final forgiveness amount.

To maximize forgiveness based on AGI, borrowers should strategically manage their income reporting. For instance, deferring bonuses or contributing to pre-tax retirement accounts (e.g., 401(k) or IRA) can lower AGI, reducing IDR payments. Married borrowers may file taxes separately to exclude a spouse’s income from AGI calculations, though this could disqualify them from certain deductions. However, this tactic is not universally beneficial; it may increase overall tax liability or limit access to other financial aid programs.

A comparative analysis of AGI-based forgiveness reveals disparities across demographics. Lower-income borrowers, particularly those in public service or nonprofit roles, often benefit most from AGI-driven IDR plans, as their payments remain low relative to their debt. Conversely, high-earning borrowers in fields like law or medicine may face larger forgiven amounts but could incur significant tax liabilities, as forgiven debt is treated as taxable income. For example, a physician with $300,000 in debt and an AGI of $250,000 might see $200,000 forgiven after 25 years, resulting in a $50,000 tax bill—a critical consideration when planning for forgiveness.

In conclusion, AGI is a double-edged sword in student loan forgiveness. While it enables lower monthly payments for many, it also dictates the ultimate forgiven amount and potential tax consequences. Borrowers must weigh their current financial flexibility against future liabilities, leveraging strategies like income optimization and tax planning to navigate this complex landscape effectively. Understanding the interplay between AGI and forgiveness amounts is essential for anyone seeking to minimize their student debt burden.

Will Democrats Deliver on Student Loan Forgiveness Promises?

You may want to see also

Explore related products

![]()

AGI Verification Process Explained

The AGI verification process is a critical step in determining eligibility for student loan forgiveness programs, particularly those tied to income-driven repayment plans. Adjusted Gross Income (AGI) serves as the financial benchmark for assessing a borrower’s ability to repay loans, making its accurate verification essential. This process involves cross-referencing the income reported on federal tax returns with the information provided in loan applications. Borrowers must submit their most recent tax transcripts or use the IRS Data Retrieval Tool to ensure consistency, as discrepancies can delay approval or result in ineligibility.

For example, if a borrower claims an AGI of $40,000 on their loan application but their tax return shows $50,000, the higher figure will be used to calculate repayment terms. This could disqualify them from certain forgiveness programs with strict income caps. To avoid such pitfalls, borrowers should double-check their tax filings and ensure all deductions, credits, and income sources are accurately reported. Practical tip: File taxes early and retain copies of all financial documents to streamline the verification process.

One common misconception is that AGI verification is a one-time event. In reality, borrowers enrolled in income-driven repayment plans must recertify their AGI annually to maintain eligibility. Failure to update this information can lead to payment increases or even default. For instance, a borrower whose income rises significantly after a job change must report the new AGI promptly to avoid penalties. This recurring requirement underscores the importance of staying organized and proactive in managing student loan obligations.

Comparatively, the AGI verification process for student loan forgiveness differs from other federal aid programs, such as Pell Grants, which often rely on Expected Family Contribution (EFC). While EFC considers assets and family size, AGI focuses solely on taxable income. This distinction means borrowers with high assets but low income may still qualify for loan forgiveness based on their AGI. Understanding these nuances can help borrowers maximize their eligibility and plan their finances strategically.

In conclusion, the AGI verification process is a cornerstone of student loan forgiveness programs, demanding precision and vigilance from borrowers. By familiarizing themselves with the steps, maintaining accurate records, and staying informed about annual recertification requirements, borrowers can navigate this process effectively. While it may seem daunting, a proactive approach ensures financial stability and increases the likelihood of qualifying for much-needed relief.

Maximize Student Loan Forgiveness: Strategies to Erase Your Debt Fast

You may want to see also

Explore related products

![]()

Tax Implications of AGI-Based Forgiveness

Adjusted Gross Income (AGI) serves as a critical metric in determining eligibility for student loan forgiveness programs, but its role extends beyond mere qualification—it directly influences the tax implications borrowers face. When forgiveness is tied to AGI, the forgiven amount may be considered taxable income, depending on the program’s structure. For instance, under the Public Service Loan Forgiveness (PSLF) program, forgiven debt is tax-free, but other programs, like income-driven repayment plans, often treat forgiven balances as taxable income unless explicitly excluded by law. This distinction underscores the importance of understanding how AGI-based forgiveness interacts with tax liabilities.

Consider the mechanics: if a borrower’s AGI falls within a certain threshold, they may qualify for partial or full loan forgiveness. However, if the forgiven amount is taxable, it increases their AGI for that tax year, potentially pushing them into a higher tax bracket or reducing eligibility for other tax credits. For example, a borrower with an AGI of $50,000 who receives $30,000 in taxable forgiveness could see their AGI rise to $80,000, triggering higher taxes and possibly disqualifying them from credits like the Earned Income Tax Credit (EITC). This cascading effect highlights the need for strategic planning when navigating AGI-based forgiveness.

To mitigate these tax implications, borrowers should explore programs that explicitly exclude forgiven debt from taxable income, such as PSLF or temporary provisions like the Taxpayer Certainty and Disaster Tax Relief Act of 2020, which excluded forgiven student loans from taxation through 2025. Additionally, maintaining detailed records of AGI and loan forgiveness amounts can help borrowers accurately report their tax liabilities and avoid penalties. Consulting a tax professional can provide tailored advice, especially for those with complex financial situations or multiple sources of income.

A comparative analysis reveals that AGI-based forgiveness programs often trade immediate relief for long-term tax consequences. While income-driven repayment plans offer lower monthly payments and potential forgiveness after 20–25 years, the tax bill on forgiven debt can offset the benefits. In contrast, programs like PSLF provide tax-free forgiveness after 10 years of qualifying payments, making them more advantageous for eligible borrowers. This trade-off emphasizes the need to weigh short-term savings against future tax obligations when selecting a forgiveness strategy.

In practice, borrowers can take proactive steps to minimize tax burdens. For instance, timing forgiveness to coincide with a year of lower income can reduce the impact of increased AGI. Alternatively, setting aside funds in a tax-advantaged account, such as a Health Savings Account (HSA) or retirement plan, can offset higher tax liabilities. By understanding the interplay between AGI, forgiveness, and taxation, borrowers can make informed decisions that align with their financial goals and avoid unexpected tax surprises.

Loan Forgiveness: Boosting Opportunities for Privileged Students in Education

You may want to see also

Explore related products

![]()

AGI Changes and Recertification Requirements

Adjusted Gross Income (AGI) plays a pivotal role in determining eligibility for various student loan forgiveness programs, particularly income-driven repayment (IDR) plans. Recent changes to AGI calculations and recertification requirements have introduced both opportunities and challenges for borrowers. For instance, the exclusion of certain types of income, such as Social Security benefits for some borrowers, can lower AGI, potentially reducing monthly payments under IDR plans. However, these adjustments also necessitate careful attention to recertification deadlines, as failure to update AGI information annually can result in payment increases or even disqualification from forgiveness programs.

To navigate these changes effectively, borrowers must understand the recertification process. This involves submitting updated income and family size information to the loan servicer each year. The Department of Education typically sends reminders 90, 60, and 30 days before the recertification deadline, but it’s the borrower’s responsibility to ensure timely submission. Pro tip: Set a personal reminder two months in advance to gather necessary documents, such as tax returns or pay stubs, and avoid last-minute stress. Missing the deadline can lead to a recalculation of payments based on 100% of the federal poverty guideline, significantly increasing monthly costs.

One critical aspect of AGI changes is the inclusion or exclusion of spousal income for married borrowers on IDR plans. Depending on the tax filing status (joint or separate), spousal income may factor into the AGI calculation, affecting payment amounts. For example, filing jointly often results in a higher AGI, while filing separately may exclude spousal income but limit eligibility for certain repayment plans. Borrowers should weigh these options carefully, potentially consulting a tax professional to determine the most advantageous filing strategy for their financial situation.

Finally, the interplay between AGI and student loan forgiveness underscores the importance of staying informed about policy updates. For instance, the Biden administration’s proposed changes to IDR plans aim to cap payments at 5% of discretionary income (down from 10-20%) for undergraduate loans, with forgiveness after 10 years for balances under $12,000. Such reforms would hinge on AGI calculations, making accurate recertification more critical than ever. Borrowers should monitor federal announcements and utilize tools like the Federal Student Aid website to stay ahead of changes that could impact their path to forgiveness.

VA Student Loan Forgiveness: Tax Implications and What You Need to Know

You may want to see also

Frequently asked questions

Yes, some student loan forgiveness programs, such as the Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans, consider AGI when determining eligibility and payment amounts.

AGI is used to calculate your discretionary income, which determines your monthly payment under income-driven repayment plans. Lower AGI typically results in lower payments and may qualify you for forgiveness after 20–25 years of payments.

Yes, AGI is a key factor in determining eligibility for one-time forgiveness programs. For example, borrowers with AGI below certain thresholds (e.g., $125,000 for individuals or $250,000 for married couples) may qualify for up to $10,000 or $20,000 in forgiveness.

Yes, AGI can change annually based on your income, deductions, and credits. If your AGI increases or decreases, it may impact your eligibility for forgiveness programs or your monthly payments under income-driven plans.

For some programs, AGI determines eligibility but not the forgiveness amount. For example, under the one-time forgiveness program, eligible borrowers receive a fixed amount ($10,000 or $20,000) regardless of AGI, as long as they meet the income threshold. However, AGI affects payment amounts under IDR plans, which can influence the total forgiven after 20–25 years.