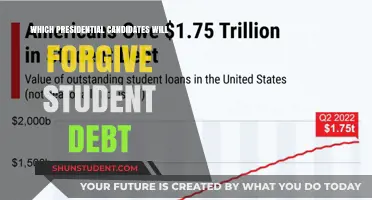

The topic of which president will forgive student loans has become a central issue in American politics, as millions of borrowers grapple with the burden of escalating debt. With student loan debt surpassing $1.7 trillion, many are looking to the federal government for relief. President Joe Biden has already taken steps to address this crisis, including pausing loan payments during the COVID-19 pandemic and implementing targeted forgiveness programs for specific groups, such as public service workers. However, broader, large-scale forgiveness remains a contentious issue, with debates over its feasibility, cost, and fairness. As the 2024 election approaches, both Biden and potential Republican candidates are under pressure to outline clear plans, making this a defining policy question for the next administration.

Explore related products

What You'll Learn

![]()

Biden's Loan Forgiveness Plan

President Biden's loan forgiveness plan has been a focal point in the ongoing debate about student debt relief. Announced in August 2022, the plan promises to cancel up to $20,000 in federal student loans for eligible borrowers. This initiative targets individuals earning less than $125,000 annually ($250,000 for married couples), with an additional $10,000 in relief for Pell Grant recipients. The plan aims to alleviate financial burdens for millions, but its implementation has faced legal challenges and political scrutiny.

Analyzing the plan’s impact reveals both its potential and limitations. For instance, while $20,000 in forgiveness can significantly reduce debt for some, it falls short for borrowers with six-figure balances. Critics argue it doesn’t address the root causes of rising tuition costs or future borrowing. Proponents, however, highlight its immediate relief for low- and middle-income earners, particularly those with Pell Grants, who often come from disadvantaged backgrounds. The plan also includes a pause on student loan payments until legal disputes are resolved, providing temporary financial breathing room.

To navigate this plan effectively, borrowers should take specific steps. First, verify eligibility by checking annual income thresholds and loan types (only federal loans qualify). Second, ensure contact information is updated with the Department of Education to receive notifications. Third, consider consolidating private loans into federal programs if possible, though this may not be feasible for all. Caution is advised against relying solely on forgiveness; continue making payments if financially able to avoid accruing interest once the pause ends.

Comparatively, Biden’s approach differs from previous administrations’ efforts. Obama’s income-driven repayment plans and Trump’s payment pauses during the pandemic were temporary fixes. Biden’s plan, however, seeks to provide direct, one-time relief while addressing equity concerns through Pell Grant provisions. Yet, it contrasts with more radical proposals like universal free college or full debt cancellation, which some advocates argue are necessary for systemic change.

In conclusion, Biden’s loan forgiveness plan represents a significant, albeit partial, step toward addressing the student debt crisis. Its success hinges on legal outcomes and future policy actions. Borrowers should stay informed, take proactive measures, and explore additional relief options like income-driven repayment plans. While not a panacea, the plan offers tangible benefits for millions, marking a pivotal moment in the broader conversation about education affordability.

Can All Student Loans Be Forgiven? Exploring the Possibility and Impact

You may want to see also

Explore related products

![]()

Eligibility Criteria for Forgiveness

The eligibility criteria for student loan forgiveness are a complex web of requirements, varying significantly depending on the program and the president's policies. Under President Biden's administration, for instance, the Public Service Loan Forgiveness (PSLF) program has been expanded, offering a pathway to debt relief for borrowers who work in qualifying public service jobs. To be eligible, individuals must make 120 qualifying payments while working full-time for a government or non-profit organization. This equates to approximately 10 years of consistent payments, a substantial commitment that demands careful planning and adherence to the program's rules.

A critical aspect of eligibility is the type of loan and repayment plan. Only Direct Loans are eligible for PSLF, and borrowers must be enrolled in an income-driven repayment (IDR) plan. These plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), adjust monthly payments based on income and family size, making them more manageable for those in public service careers. For example, a single borrower earning $40,000 annually with $50,000 in student debt could see their monthly payment reduced from $500 to around $200 under an IDR plan, making the 120 qualifying payments more attainable.

Another layer of complexity arises with the recent limited-time waiver for PSLF, which temporarily relaxes some rules. This waiver allows past payments on any federal loan, regardless of the repayment plan, to count toward forgiveness. It also permits consolidation of non-Direct Loans into the Direct Loan program, opening up eligibility for many previously excluded borrowers. However, this waiver has a strict deadline, emphasizing the need for prompt action and careful review of one's loan history to maximize the benefits.

For those considering loan forgiveness, a strategic approach is essential. Start by verifying your loan type and employment eligibility through the Federal Student Aid website. Keep meticulous records of your payments and employment certification forms, as these are crucial for demonstrating compliance with the program's requirements. Additionally, stay informed about policy changes, as presidential administrations may introduce new initiatives or modify existing ones, potentially expanding or restricting eligibility criteria.

In summary, navigating the eligibility criteria for student loan forgiveness requires a detailed understanding of program specifics, strategic planning, and proactive management of your loans and employment documentation. By focusing on these elements, borrowers can position themselves to take full advantage of available forgiveness opportunities, potentially alleviating a significant financial burden.

Will AES Student Loans Qualify for Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Impact on Federal Budget

Student loan forgiveness, while a lifeline for millions, carries a hefty price tag for the federal budget. Estimates suggest broad-scale forgiveness could cost upwards of $1 trillion over a decade. This isn't a one-time hit; it's a structural shift in spending priorities, potentially crowding out other critical areas like infrastructure, healthcare, or education funding.

Cares Act Student Loan Forgiveness: Step-by-Step Application Guide

You may want to see also

Explore related products

$14.95 $14.95

![]()

Private vs. Federal Loan Forgiveness

The distinction between private and federal student loans is critical when considering loan forgiveness, as each type operates under vastly different rules and eligibility criteria. Federal student loans, backed by the U.S. Department of Education, offer several forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) plans. These programs are designed to alleviate financial burden for borrowers who meet specific requirements, such as working in public service or maintaining low income relative to debt. For instance, PSLF forgives the remaining balance after 120 qualifying payments for those employed full-time by a government or nonprofit organization. In contrast, private student loans, issued by banks, credit unions, or other financial institutions, rarely offer forgiveness options. Borrowers with private loans must rely on lender-specific policies or negotiate directly with their lender, often with limited success.

Analyzing the landscape of presidential policies reveals that federal loan forgiveness initiatives are more likely to be influenced by executive action. For example, President Biden’s administration has implemented targeted forgiveness measures, such as the $10,000 to $20,000 debt cancellation plan (currently paused due to legal challenges) and expansions to IDR plans. These actions exclusively impact federal loans, leaving private loan borrowers without similar relief. This disparity underscores the importance of understanding loan type when anticipating or advocating for forgiveness. Private loan borrowers may need to explore alternative strategies, such as refinancing at lower interest rates or seeking employer-based repayment assistance programs.

From a practical standpoint, borrowers should prioritize identifying their loan type and researching available options. Federal loan holders can take proactive steps like consolidating loans into a Direct Consolidation Loan to qualify for PSLF or enrolling in an IDR plan to cap monthly payments at a manageable percentage of their income. Private loan holders, however, should focus on improving their financial position through budgeting, increasing income, or negotiating with lenders for temporary forbearance or reduced interest rates. For example, a borrower with $30,000 in private loans at 8% interest might save thousands by refinancing to a 5% rate, even if forgiveness remains out of reach.

Persuasively, the debate over private vs. federal loan forgiveness highlights the need for systemic reform to address the broader student debt crisis. While federal forgiveness programs provide a safety net for some, their complexity and limitations leave many borrowers confused or ineligible. Private loans, often taken out due to gaps in federal aid, exacerbate financial strain without recourse. Policymakers must consider expanding forgiveness opportunities for private loans or regulating lenders to offer more flexible repayment terms. Until then, borrowers must navigate this bifurcated system with diligence, leveraging every available resource to manage their debt effectively.

In conclusion, the divide between private and federal loan forgiveness is stark, with federal borrowers having access to structured relief programs and private borrowers largely left to fend for themselves. Understanding this distinction empowers individuals to make informed decisions, whether by pursuing federal forgiveness pathways or strategizing to mitigate private loan burdens. As presidential policies continue to evolve, staying informed and advocating for equitable solutions will remain essential for all student loan borrowers.

Why Do I Keep Getting Calls About Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness Expansion

The Public Service Loan Forgiveness (PSLF) program has long been a beacon of hope for borrowers committed to careers in public service, offering the promise of debt relief after a decade of qualifying payments. However, its complex requirements and administrative hurdles have left many eligible borrowers frustrated and disqualified. Recognizing these challenges, recent expansions to the program aim to streamline access and extend forgiveness to a broader range of public servants. These changes reflect a growing acknowledgment of the critical role public service plays in society and the financial burdens faced by those who choose these careers.

One of the most significant updates to the PSLF program is the temporary waiver introduced in 2021, which allowed borrowers to receive credit for past payments that were previously deemed ineligible due to technicalities, such as having the wrong loan type or repayment plan. This waiver, extended through October 31, 2023, has provided a lifeline to thousands of borrowers, many of whom were on the verge of disqualification. For example, teachers, nurses, and nonprofit workers who had made years of payments under graduated or extended repayment plans suddenly found those payments qualifying toward forgiveness. To take advantage of this opportunity, borrowers must consolidate their loans into a Direct Loan and submit a PSLF form before the deadline, ensuring their years of service are not in vain.

Beyond the temporary waiver, the Biden administration has proposed long-term reforms to simplify the PSLF program and make it more accessible. These include automating payment tracking, reducing documentation burdens, and expanding the definition of qualifying employment to include more public service roles. For instance, part-time workers and those employed by religious organizations may soon be eligible, addressing gaps that previously excluded deserving borrowers. Such reforms aim to align the program’s structure with its original intent: rewarding public servants for their dedication to communities while alleviating the financial strain of student debt.

Critics argue that these expansions could strain federal resources, as forgiving billions in student loans shifts the financial burden from borrowers to taxpayers. However, proponents counter that investing in public service careers strengthens societal infrastructure, from education and healthcare to social services. Moreover, the economic benefits of loan forgiveness—such as increased consumer spending and reduced default rates—can offset initial costs. For borrowers, the key takeaway is clear: stay informed about program changes, ensure your loans and employment qualify, and take proactive steps to maximize your chances of forgiveness.

In practical terms, borrowers should regularly certify their employment using the PSLF Help Tool, maintain records of payments and employer certifications, and consider switching to an income-driven repayment plan to lower monthly obligations. Additionally, those nearing the 120-payment threshold should verify their payment count with their loan servicer to avoid surprises. While the PSLF expansion represents a significant step forward, its success hinges on borrowers’ ability to navigate its requirements effectively. By staying engaged and leveraging available resources, public servants can turn the promise of loan forgiveness into a reality.

Private Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Frequently asked questions

The President of the United States has limited authority to forgive student loans through executive action, primarily for federal loans. However, widespread loan forgiveness typically requires congressional approval.

Yes, President Biden has implemented targeted student loan forgiveness programs, including relief for borrowers under the Public Service Loan Forgiveness (PSLS) program and those defrauded by for-profit colleges. He also proposed broader forgiveness, but it faces legal challenges.

Future presidents may pursue student loan forgiveness depending on their policies and political priorities. However, any action would depend on legal authority, congressional support, and public opinion.

A president cannot unilaterally forgive all student loans without congressional approval. Broad forgiveness would require legislative action or a significant expansion of executive authority, which is legally contentious.

President Barack Obama introduced the Pay As You Earn (PAYE) repayment plan and expanded loan forgiveness programs, but widespread forgiveness as a policy goal gained momentum under President Biden.