The issue of student debt forgiveness has become a pivotal topic in the 2024 presidential election, with millions of Americans burdened by trillions of dollars in educational loans. As candidates vie for the presidency, their stances on forgiving student debt are under intense scrutiny, as this policy could significantly impact voters, particularly younger demographics. Some candidates advocate for broad forgiveness plans, ranging from partial to full cancellation, while others propose targeted relief or alternative solutions like income-driven repayment reforms. Understanding which candidates support debt forgiveness—and to what extent—is crucial for voters prioritizing this issue, as it reflects broader economic and social equity concerns in the United States.

Explore related products

What You'll Learn

![]()

Biden's Student Debt Relief Plan

President Biden's Student Debt Relief Plan has been a cornerstone of his administration's efforts to address the burgeoning student debt crisis in the United States. Announced in August 2022, the plan aimed to provide targeted relief to millions of borrowers, offering up to $20,000 in debt cancellation for Pell Grant recipients and up to $10,000 for other federal student loan borrowers. This initiative was designed to alleviate financial strain on individuals and families, particularly those from low- and middle-income backgrounds, by reducing or eliminating their student loan burdens. The plan also included a pause on federal student loan payments, which has been extended multiple times, providing additional breathing room for borrowers during economic uncertainty.

Analytically, Biden's plan stands out for its focus on equity. By offering higher relief amounts to Pell Grant recipients, the administration acknowledged the disproportionate impact of student debt on lower-income borrowers. Pell Grants are typically awarded to students from families with annual incomes below $50,000, making this targeted approach a strategic effort to address systemic inequalities. However, the plan faced legal challenges, with critics arguing it overstepped executive authority. The Supreme Court’s June 2023 ruling struck down the program, halting its implementation and leaving millions in limbo. This outcome underscores the complexities of implementing large-scale debt relief through executive action.

From a practical standpoint, borrowers should stay informed about alternative relief options. The Biden administration has since expanded income-driven repayment (IDR) plans and streamlined the Public Service Loan Forgiveness (PSLF) program. For example, the Saving on a Valuable Education (SAVE) plan caps monthly payments at 5% of discretionary income for undergraduate loans, compared to 10% under previous plans. Borrowers can also pursue PSLF by working full-time for qualifying employers, such as government or nonprofit organizations, for 10 years. These alternatives, while not as immediate as direct debt cancellation, offer pathways to manageable repayment or eventual forgiveness.

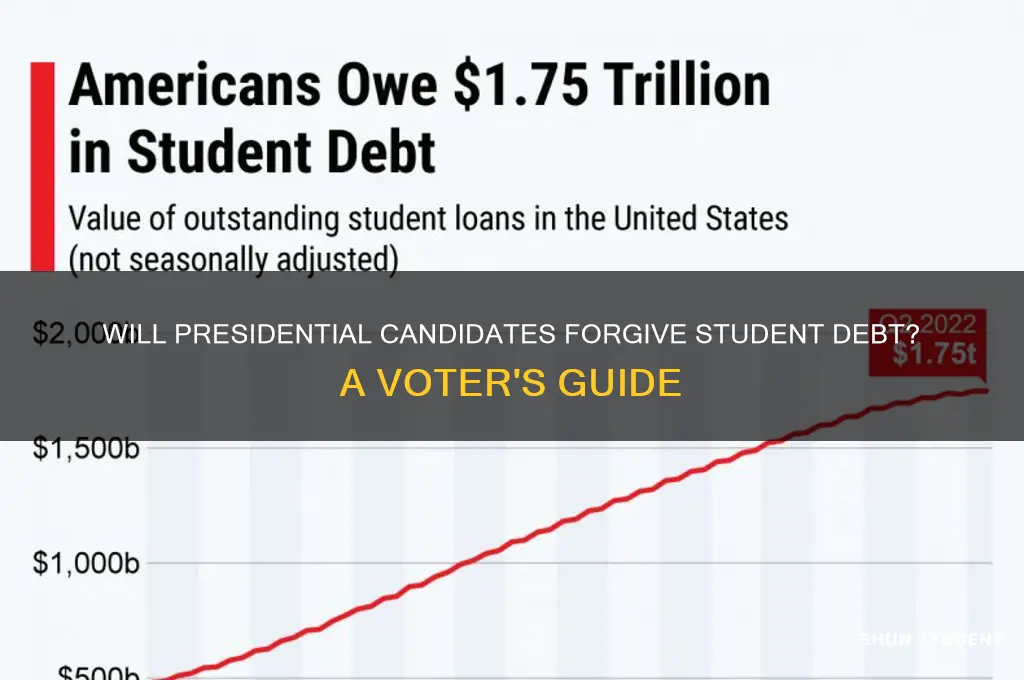

Persuasively, Biden’s plan highlights the moral imperative of addressing student debt as a societal issue. With over 43 million Americans holding $1.7 trillion in student loans, the crisis stifles economic mobility, delays homeownership, and discourages entrepreneurship. While the plan’s legal defeat was a setback, it sparked a national conversation about the role of government in higher education financing. Advocates argue that comprehensive reform, including lowering college costs and increasing institutional accountability, is essential to prevent future generations from falling into debt traps.

Comparatively, Biden’s approach differs from proposals by other candidates, such as Senator Elizabeth Warren’s call for $50,000 in universal debt cancellation. While more expansive, such plans face similar political and legal hurdles. Biden’s targeted relief, though limited, demonstrated a pragmatic attempt to balance fiscal responsibility with immediate borrower needs. Its legacy lies in its ambition to reframe student debt as a policy priority, even if its execution fell short. Borrowers must now navigate a patchwork of existing programs, underscoring the need for continued advocacy and legislative action to achieve lasting solutions.

Student Loan Forgiveness: Analyzing the Odds of Debt Relief in 2023

You may want to see also

Explore related products

![]()

Candidates Supporting Full Debt Forgiveness

Student debt has become a defining issue for millions of Americans, and some presidential candidates have responded with bold proposals for full debt forgiveness. Among them, Senator Elizabeth Warren stands out with her plan to cancel up to $50,000 in student loan debt for 95% of borrowers, funded by a tax on wealth exceeding $50 million. This proposal targets systemic inequality by addressing both the financial burden and the racial wealth gap, as Black and Latino borrowers are disproportionately affected by student debt. Warren’s plan also includes tuition-free public college to prevent future debt accumulation, making it a comprehensive solution.

Another candidate advocating for full forgiveness is Senator Bernie Sanders, whose plan goes even further by canceling all $1.6 trillion in outstanding student debt. Sanders argues that this move would stimulate the economy by freeing up disposable income for millions of Americans, enabling them to buy homes, start businesses, and invest in their futures. His proposal is funded by a tax on Wall Street speculation, framing it as a redistribution of wealth from financial institutions to working-class families. Critics argue the cost is prohibitive, but Sanders counters that it’s a moral imperative to undo decades of policy that saddled students with unmanageable debt.

Former Secretary of Housing and Urban Development Julián Castro also supports full debt forgiveness, though his plan is less expansive than Warren’s or Sanders’. Castro proposes canceling debt for borrowers earning up to $250,000 annually, with partial forgiveness for those earning above that threshold. His plan includes a $5,000 grant for low-income students to cover non-tuition expenses, addressing the hidden costs of higher education. While narrower in scope, Castro’s approach balances fiscal responsibility with targeted relief, appealing to moderate voters concerned about the cost of broader forgiveness.

These candidates’ proposals reflect a growing consensus that student debt is not just a personal financial issue but a national crisis requiring bold action. Full forgiveness would provide immediate relief to millions, but it’s not without challenges. Critics worry about moral hazard, inflationary pressures, and fairness to those who’ve already paid off their loans. However, proponents argue that the long-term economic benefits—increased consumer spending, reduced defaults, and greater social mobility—outweigh the costs. For borrowers drowning in debt, these plans offer a lifeline, but their success hinges on political will and public support.

Will Student Debt Be Forgiven? Exploring the Possibility and Challenges

You may want to see also

Explore related products

![]()

Partial Forgiveness Proposals by Candidates

Several presidential candidates have proposed partial student debt forgiveness plans, recognizing the financial strain on borrowers while balancing fiscal responsibility. These proposals often target specific groups or debt thresholds, aiming to provide relief without blanket cancellation. For instance, some candidates suggest forgiving up to $10,000 in federal student loans per borrower, a figure that could eliminate debt entirely for roughly one-third of borrowers, according to federal data. This approach addresses the most vulnerable borrowers while avoiding the higher costs of universal forgiveness.

Analyzing these proposals reveals a strategic focus on equity. Candidates often tie partial forgiveness to income-driven repayment plans or public service requirements, ensuring relief reaches those most in need. For example, one plan proposes forgiving $50,000 in debt for borrowers earning under $100,000 annually, with a sliding scale for higher incomes. This tiered system aims to prevent high earners from benefiting disproportionately, a common critique of broader forgiveness plans. However, critics argue that such income caps could create administrative complexities and unintended consequences.

A persuasive argument for partial forgiveness lies in its potential to stimulate the economy. By reducing debt burdens for millions, borrowers could redirect funds toward consumer spending, homeownership, or entrepreneurship. Studies suggest that forgiving $10,000 per borrower could increase GDP by tens of billions of dollars annually. This economic boost could offset a portion of the program’s cost, making it a more viable option than full forgiveness, which carries a significantly higher price tag. Policymakers must weigh these benefits against long-term fiscal implications.

Comparatively, partial forgiveness proposals differ from full cancellation in their political feasibility. While full forgiveness appeals to progressive voters, it faces staunch opposition from conservatives and moderates concerned about cost and fairness. Partial plans, by contrast, offer a middle ground that could attract bipartisan support. For instance, a proposal to forgive $20,000 in debt for Pell Grant recipients—a group disproportionately from low-income backgrounds—has gained traction as a targeted solution. This approach acknowledges the systemic inequities in higher education financing without alienating skeptical lawmakers.

Practical implementation of partial forgiveness requires careful design. Candidates must address questions like whether private student loans qualify, how to handle accrued interest, and whether forgiven amounts will be taxed as income. For example, capping forgiveness at $10,000 but excluding it from taxable income could maximize benefits for borrowers. Additionally, pairing forgiveness with reforms to prevent future debt crises—such as lowering interest rates or expanding grant programs—is essential for long-term sustainability. Borrowers should stay informed about eligibility criteria and application processes as these plans evolve.

Kentucky's Tax Rules: Student Loan Forgiveness Implications Explained

You may want to see also

Explore related products

$14.95 $14.95

![]()

Republican Stance on Debt Cancellation

The Republican Party's stance on student debt cancellation is rooted in fiscal conservatism and a belief in personal responsibility. Unlike their Democratic counterparts, who often advocate for broad-scale debt forgiveness, Republicans typically oppose such measures, arguing that they unfairly burden taxpayers and distort market incentives. This position is exemplified by key figures like Senator Mitch McConnell, who has criticized debt cancellation as a "giveaway" that benefits higher-income individuals at the expense of those who did not attend college. Understanding this perspective requires examining the party’s core principles and their application to the student debt crisis.

Analyzing the Republican argument reveals a focus on long-term economic consequences. Republicans contend that canceling student debt without addressing the root causes of rising tuition costs would exacerbate inflation and increase the national deficit. For instance, the Congressional Budget Service estimated that a one-time cancellation of $10,000 per borrower would cost taxpayers approximately $377 billion. Republicans propose alternative solutions, such as income-driven repayment plans and expanding Pell Grants, which target financial aid to low-income students without erasing existing debt. These approaches align with their emphasis on accountability and market-based solutions.

A comparative analysis highlights the stark contrast between Republican and Democratic approaches. While Democrats frame debt cancellation as a matter of social justice and economic stimulus, Republicans view it as a moral hazard that undermines the value of hard work and financial prudence. This ideological divide is evident in legislative actions, such as Republican opposition to President Biden’s executive order canceling up to $20,000 in student debt for eligible borrowers. Critics within the GOP argue that such policies reward irresponsible borrowing and penalize those who have already paid off their loans or chosen not to pursue higher education.

Persuasively, Republicans advocate for a shift in focus from debt cancellation to systemic reforms in higher education. They argue that addressing skyrocketing tuition costs, increasing transparency in college pricing, and promoting vocational training are more sustainable solutions. For example, Senator Rand Paul has proposed allowing students to declare bankruptcy on federal loans, a measure aimed at holding both borrowers and lenders accountable. By prioritizing these reforms, Republicans aim to create a more equitable and efficient education system without resorting to what they see as financially reckless policies.

In practical terms, individuals seeking relief from student debt under a Republican administration should explore existing programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans. These options, while not as immediate as broad cancellation, provide pathways to manageable payments or eventual forgiveness based on income and career choices. Additionally, borrowers can take proactive steps such as refinancing private loans at lower interest rates or pursuing employer-sponsored repayment assistance programs. While Republicans may not support widespread debt cancellation, their focus on accountability and reform offers alternative avenues for addressing the student debt burden.

Cancer and Student Loan Forgiveness: Exploring Options for Financial Relief

You may want to see also

Explore related products

![]()

Impact of Forgiveness on Voter Turnout

Student debt forgiveness has emerged as a pivotal campaign promise for presidential candidates, but its impact on voter turnout is nuanced. Historically, young voters, who carry the bulk of student debt, have lower turnout rates compared to older demographics. A candidate pledging to forgive student debt could galvanize this group, potentially shifting electoral dynamics. For instance, in 2020, Biden’s proposal to cancel $10,000 in student debt was linked to increased enthusiasm among voters aged 18–29, though actual turnout gains were modest. This suggests that while forgiveness can energize voters, its effectiveness depends on how concretely and credibly the promise is communicated.

To maximize turnout, candidates must pair forgiveness pledges with targeted outreach strategies. Research shows that young voters respond more to personalized messaging than broad policy statements. Campaigns should leverage social media platforms like TikTok and Instagram to explain how forgiveness would directly benefit individual voters. For example, highlighting that 43 million Americans hold student debt, with an average balance of $37,000, can make the issue feel urgent and personal. Additionally, partnering with grassroots organizations focused on youth engagement can amplify the message and build trust.

However, the impact of forgiveness on turnout isn’t guaranteed. Skepticism about a candidate’s ability to deliver on such a promise can dampen enthusiasm. For instance, Biden’s delayed and partial implementation of debt relief has led to frustration among some voters. Candidates must address this by outlining clear, actionable plans for forgiveness, such as specifying whether it will be achieved through executive action or legislation. Transparency builds credibility, which is essential for translating policy promises into votes.

Comparatively, candidates who frame forgiveness as part of a broader economic justice agenda may see greater turnout benefits. Linking debt relief to issues like affordable housing, healthcare, and job creation can appeal to a wider coalition of voters. For example, Bernie Sanders’ 2020 campaign proposed free college tuition alongside debt cancellation, resonating with both young voters and working-class families. This holistic approach not only addresses immediate financial burdens but also aligns with long-term economic aspirations, making it a more compelling reason to vote.

In conclusion, student debt forgiveness can influence voter turnout, particularly among young and indebted populations, but its effectiveness hinges on execution. Candidates must combine bold promises with targeted outreach, transparency, and a broader policy vision. Without these elements, forgiveness risks becoming an empty slogan rather than a mobilizing force. For voters, the takeaway is clear: scrutinize candidates’ plans, engage with campaigns, and recognize that your vote is a tool to hold leaders accountable for their promises.

Can Police Officers Qualify for Federal Student Loan Forgiveness?

You may want to see also

Frequently asked questions

Several candidates have proposed student debt forgiveness plans, including full or partial cancellation. Notable examples include candidates advocating for forgiving up to $10,000 to $50,000 in federal student loans, often with income caps or eligibility criteria.

No, not all candidates support student debt forgiveness. Some advocate for alternative solutions like income-driven repayment plans, lowering interest rates, or expanding Pell Grants instead of direct forgiveness.

Proposals vary widely. Some candidates suggest forgiving up to $10,000 per borrower, while others propose $50,000 or more, often targeting federal loans and specific income groups.

Most forgiveness proposals focus on federal student loans. Private loans are rarely included, though some candidates suggest refinancing options or protections for private loan borrowers.

![The Manchurian Candidate (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/71tovXO167L._AC_UY218_.jpg)