When it comes to deducting dependent student loan interest, the responsibility typically falls on the taxpayer who is legally obligated to pay the loan, which is usually the student borrower. However, in cases where a parent or guardian claims the student as a dependent on their tax return, they may be eligible to claim the student loan interest deduction if they have made payments toward the loan during the tax year. It's important to note that the student cannot claim the deduction if they are claimed as a dependent on someone else's tax return. The Internal Revenue Service (IRS) has specific rules and requirements for claiming this deduction, including income limits and restrictions on the type of loans that qualify. Understanding these guidelines is crucial for taxpayers to accurately report their deductions and avoid potential penalties or audits.

Explore related products

What You'll Learn

- IRS Rules on Deductions: Who qualifies to claim student loan interest deductions on tax returns

- Dependent Eligibility: Criteria for dependents to deduct student loan interest paid by parents

- Parent vs. Student: Who can claim the deduction if both parties contribute to payments

- Income Limits: How income thresholds affect eligibility for student loan interest deductions

- Documentation Required: Proof needed to claim deductions for dependent student loan interest payments

![]()

IRS Rules on Deductions: Who qualifies to claim student loan interest deductions on tax returns

The IRS allows taxpayers to deduct a certain amount of student loan interest paid during the tax year, but the rules are specific about who qualifies for this deduction. According to IRS Publication 970, the individual who is legally obligated to pay the student loan interest is generally the one eligible to claim the deduction. This means that if a parent takes out a loan for their dependent child's education, the parent is typically the one who can deduct the interest, provided they meet the other eligibility criteria. However, if the parent chooses to allow the dependent child to claim the deduction, the child must itemize their deductions and meet the income limits set by the IRS.

For dependent students, the ability to claim the student loan interest deduction is limited. If a parent claims the student as a dependent on their tax return, the student cannot take the deduction, even if they are the ones making the loan payments. The IRS considers the parent as the primary taxpayer responsible for the dependent's expenses, including education-related costs. This rule applies regardless of whether the loan is in the student's name or the parent's name. Therefore, it is crucial for families to plan and communicate regarding who will claim the deduction to avoid complications during tax filing.

To qualify for the student loan interest deduction, the taxpayer must meet certain income thresholds. For tax year 2023, the deduction begins to phase out for taxpayers with modified adjusted gross income (MAGI) above $70,000 ($140,000 for married filing jointly) and is completely phased out at $85,000 ($170,000 for married filing jointly). If a dependent student's income falls within these limits and the parent allows them to claim the deduction, the student must ensure their MAGI does not exceed these thresholds. Additionally, the loan must have been taken out for qualified education expenses, such as tuition, fees, and other necessary costs, at an eligible institution.

Another important rule is that the student must have been enrolled at least half-time in a degree, certificate, or other recognized credential program when the loan was issued. This requirement ensures that the loan is directly tied to the student's education. If the loan was taken out for a dependent's education but the dependent was not enrolled at least half-time, the interest on that loan does not qualify for the deduction. This rule underscores the importance of understanding the specific conditions under which student loan interest can be deducted.

Lastly, the IRS requires that the taxpayer claiming the deduction must be legally obligated to pay the interest. This means that if a parent pays the interest on a loan that is legally in the student's name, the parent cannot claim the deduction unless the student is no longer a dependent. Conversely, if the student is legally responsible for the loan and meets all other criteria, they can claim the deduction if the parent does not claim them as a dependent. Understanding these nuances is essential for maximizing tax benefits while remaining compliant with IRS regulations.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Explore related products

![]()

Dependent Eligibility: Criteria for dependents to deduct student loan interest paid by parents

When determining who can deduct dependent student loan interest, it's essential to understand the criteria for dependent eligibility, especially when parents are the ones making the payments. The Internal Revenue Service (IRS) has specific guidelines outlining who qualifies as a dependent and under what circumstances student loan interest paid by parents can be deducted. For a dependent to be eligible for this deduction, they must meet the IRS definition of a "qualifying child" or a "qualifying relative." A qualifying child must be under the age of 19, or under 24 if a full-time student, and must live with the parent for more than half the year. Additionally, the child must not provide more than half of their own financial support.

The student loan interest deduction is generally claimed by the person who is legally obligated to pay the debt. However, if parents pay their dependent child’s student loan interest, the IRS allows the parents to claim the deduction if the dependent meets the eligibility criteria and does not file a joint return. The dependent themselves cannot claim the deduction if the parents are claiming them as a dependent on their tax return. This rule ensures that the deduction is not claimed twice and adheres to IRS regulations regarding dependent exemptions and deductions.

Another critical criterion is that the student loan must have been taken out for qualified education expenses, such as tuition, fees, books, and other necessary supplies. The loan must also be in the dependent’s name, even if the parents are making the payments. If the loan is in the parent’s name, the interest paid is not eligible for the student loan interest deduction under the dependent’s eligibility rules. This distinction is crucial, as it directly impacts who can claim the deduction and under what circumstances.

Furthermore, the dependent must be enrolled in an eligible institution, which includes most accredited colleges, universities, and vocational schools. The IRS requires that the student be enrolled at least half-time in a program leading to a degree, certificate, or other recognized credential. This enrollment status is verified by the educational institution and must be maintained throughout the period for which the interest payments are being deducted. Failure to meet these enrollment requirements can disqualify the interest payments from being eligible for the deduction.

Lastly, the deduction for student loan interest is subject to income limits, which apply to the parents claiming the dependent. For tax year 2023, the deduction begins to phase out for taxpayers with modified adjusted gross incomes (MAGI) above $70,000 ($140,000 for joint filers) and is completely phased out at $85,000 ($170,000 for joint filers). Parents must ensure their income falls within these thresholds to qualify for the deduction. Understanding these criteria is vital for parents who wish to claim the student loan interest deduction for their dependent children, as it ensures compliance with IRS rules and maximizes potential tax benefits.

Top Private Student Loans: Lowest Interest Rates Compared

You may want to see also

Explore related products

![]()

Parent vs. Student: Who can claim the deduction if both parties contribute to payments

When it comes to claiming the student loan interest deduction, the rules can be complex, especially when both parents and students contribute to the payments. The IRS has specific guidelines to determine who is eligible to claim this deduction, primarily focusing on who is legally responsible for the loan and who actually pays the interest. Generally, the student loan interest deduction can only be claimed by the taxpayer who is legally obligated to repay the loan. This means if the loan is solely in the student's name, the student is the one eligible to claim the deduction, regardless of who makes the payments.

However, if the parent has taken out a loan in their own name, such as a Parent PLUS Loan, the parent is the one legally obligated to repay the debt and, therefore, the one who can claim the deduction. This holds true even if the student makes payments on the parent's loan. The key factor is the legal responsibility for the loan, not who contributes to the payments. It’s important for families to understand this distinction to avoid errors on their tax returns, as claiming a deduction improperly can lead to audits or penalties.

In cases where both the parent and the student have loans in their respective names, each party can claim the deduction for the interest paid on their own loans. For example, if a parent pays interest on a Parent PLUS Loan and the student pays interest on a loan in their name, both can claim their respective deductions. However, if the parent and student are making payments on a loan that is solely in the student's name, only the student can claim the deduction, even if the parent is contributing financially.

One common misconception is that parents can claim the deduction if they provide financial support for their child’s education or loan payments. This is not the case unless the loan is in the parent’s name. The IRS does not allow parents to claim the deduction for loans they are not legally responsible for, even if they are helping with payments. This rule ensures that the deduction is claimed by the taxpayer who is legally liable for the debt.

To maximize tax benefits, families should carefully review their loan agreements and consult a tax professional if needed. Proper documentation of payments and loan responsibilities is crucial. For instance, if a parent and student agree to split payments on a loan in the student’s name, the student should still claim the full deduction, as they are the legal obligor. Clear communication and planning between parents and students can help avoid confusion and ensure compliance with IRS rules.

In summary, the student loan interest deduction is typically claimed by the individual legally responsible for the loan. Parents can only claim the deduction if the loan is in their name, such as with a Parent PLUS Loan. When both parties contribute to payments, the deduction must be claimed by the legal obligor of the loan. Understanding these rules is essential for parents and students to navigate their tax obligations accurately and efficiently.

Zero Payments on Student Loans: Does Interest Still Accrue?

You may want to see also

Explore related products

![]()

Income Limits: How income thresholds affect eligibility for student loan interest deductions

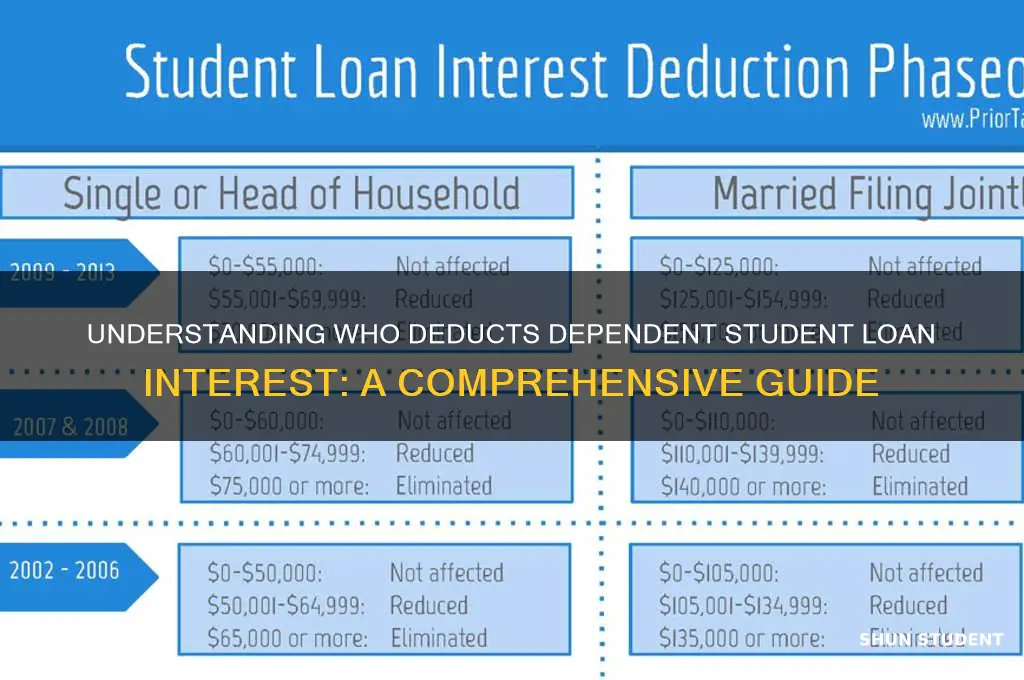

When considering who can deduct dependent student loan interest, understanding the role of income limits is crucial. The Internal Revenue Service (IRS) sets specific income thresholds that determine eligibility for the student loan interest deduction. This deduction allows taxpayers to reduce their taxable income by up to $2,500 of the interest paid on qualified student loans during the tax year. However, not everyone qualifies, and income limits play a significant role in this determination. For single filers, the deduction begins to phase out once their modified adjusted gross income (MAGI) exceeds $70,000 and is completely eliminated at $85,000. For married couples filing jointly, the phaseout starts at $140,000 and ends at $170,000. These thresholds are important because they directly impact whether a taxpayer, including those with dependent students, can claim the deduction.

For parents claiming dependents who are students, the income limits apply to the parents' tax return if the student is claimed as a dependent. This means that even if the student is the one making loan payments, the parents' income level determines eligibility for the deduction. If the parents' income exceeds the thresholds, they cannot claim the student loan interest deduction, regardless of the amount paid. This rule underscores the importance of understanding the interplay between dependency status and income limits. It also highlights why some taxpayers may not qualify for the deduction, even if they have significant student loan interest payments.

It’s important to note that the student loan interest deduction is an "above-the-line" deduction, meaning it can be claimed even if the taxpayer does not itemize deductions. However, the income limits remain a critical factor in eligibility. For taxpayers whose income falls within the phaseout range, the deduction is reduced proportionally. For example, a single filer with a MAGI of $80,000 would have a partial deduction, as their income falls within the phaseout range of $70,000 to $85,000. This proportional reduction is calculated based on the IRS formula, which considers the taxpayer's income relative to the phaseout thresholds.

Another key aspect is how the income limits affect dependent students who file their own taxes. If a student is not claimed as a dependent on their parents' tax return, they may be eligible to claim the deduction themselves, provided their own income falls below the thresholds. However, if the student remains a dependent, the parents' income limits still apply, even if the student is financially independent. This distinction is often a point of confusion, emphasizing the need for careful consideration of dependency status and income levels when determining eligibility for the student loan interest deduction.

Lastly, taxpayers should be aware of how income limits interact with other tax benefits related to education. For instance, the student loan interest deduction cannot be claimed in conjunction with the tuition and fees deduction or the American Opportunity Credit for the same student in the same year. Additionally, if a taxpayer's income exceeds the thresholds, they may need to explore alternative strategies, such as maximizing contributions to retirement accounts, to lower their MAGI and potentially regain eligibility for the deduction. Understanding these income limits and their implications is essential for taxpayers seeking to optimize their tax situation while managing student loan interest payments.

Who Can Claim Student Loan Interest for Dependents: Tax Rules Explained

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Documentation Required: Proof needed to claim deductions for dependent student loan interest payments

When claiming deductions for dependent student loan interest payments, it is essential to provide accurate and complete documentation to support your claim. The Internal Revenue Service (IRS) requires taxpayers to maintain records that substantiate their eligibility for the deduction. This includes proof that the student loan meets the criteria for a qualified education loan and that the taxpayer is legally responsible for the interest payments. The primary document needed is Form 1098-E, Student Loan Interest Statement, which is issued by the lender and reports the amount of interest paid during the tax year. If you do not receive this form but have paid qualifying interest, you must still report the amount on your tax return and retain detailed records of your payments.

In addition to Form 1098-E, taxpayers must provide documentation that establishes the relationship between the taxpayer and the dependent student. This is crucial because the deduction is only available if the taxpayer claims the student as a dependent on their tax return. IRS Form 1040, Schedule 1 is used to claim the student loan interest deduction, and it must be accompanied by proof of dependency, such as a birth certificate, adoption papers, or other legal documents that confirm the relationship. For married taxpayers filing jointly, both spouses must meet the eligibility criteria, and documentation should clearly show that the dependent is related to at least one of the spouses.

Another critical piece of documentation is evidence that the student loan was used for qualified education expenses. The IRS requires that the loan be taken out solely to pay for higher education costs, such as tuition, fees, books, supplies, and room and board, for the taxpayer, their spouse, or their dependent. Loan agreements and disbursement statements from the educational institution or lender can serve as proof that the funds were used for eligible expenses. If the loan was taken out for a dependent, additional documentation linking the dependent to the educational institution, such as enrollment records or transcripts, may be necessary.

Taxpayers should also maintain records of their payments, including bank statements, canceled checks, or electronic payment confirmations, that show the interest portion of the student loan payments. This is particularly important if the lender does not provide Form 1098-E or if the form is incomplete. Keeping a detailed log of payments, including dates, amounts, and the breakdown of principal versus interest, can help ensure accuracy and provide backup documentation in case of an audit. It is advisable to retain these records for at least three years after filing the tax return, as the IRS may request them to verify the deduction.

Lastly, if the dependent student loan was taken out by someone other than the taxpayer (e.g., the student themselves), but the taxpayer is legally obligated to repay the loan, additional documentation is required. This includes legal agreements or court documents that establish the taxpayer’s responsibility for the loan. For example, if a parent co-signed the loan or entered into a written agreement to repay it, these documents must be retained and provided if requested by the IRS. Ensuring all documentation is organized and readily available will streamline the process of claiming the deduction and reduce the risk of errors or disputes.

When Did Student Loans Switch to Compounding Interest?

You may want to see also

Frequently asked questions

The parent who claims the dependent on their tax return is generally eligible to deduct the student loan interest, provided they meet the IRS requirements for income limits and other criteria.

No, if the student is claimed as a dependent on someone else’s tax return, they cannot deduct the student loan interest, even if they file their own taxes.

If the student is not claimed as a dependent, they may be eligible to deduct their own student loan interest, provided they meet the IRS requirements for income and other qualifications.

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)