The real interest rate on student loans is a critical factor for borrowers to understand, as it reflects the actual cost of borrowing after accounting for inflation. Unlike the nominal interest rate, which is the advertised rate on a loan, the real interest rate adjusts for changes in the purchasing power of money over time. For student loan borrowers, this distinction is particularly important because it determines how much their debt will grow relative to their future earnings and the overall economy. High real interest rates can significantly increase the long-term burden of student debt, making it harder for graduates to achieve financial stability, while lower real rates may provide more manageable repayment terms. Understanding this concept is essential for making informed decisions about borrowing and repayment strategies.

Explore related products

What You'll Learn

- Federal vs. Private Rates: Compare government-backed loan rates with those from private lenders

- Fixed vs. Variable Rates: Analyze the stability of fixed rates versus fluctuating variable rates

- Interest Capitalization: Understand how unpaid interest adds to the loan principal

- Repayment Plans Impact: Explore how income-driven plans affect long-term interest costs

- Tax Deductibility: Learn about potential tax benefits for student loan interest payments

![]()

Federal vs. Private Rates: Compare government-backed loan rates with those from private lenders

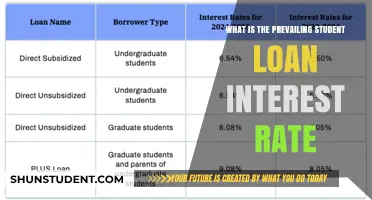

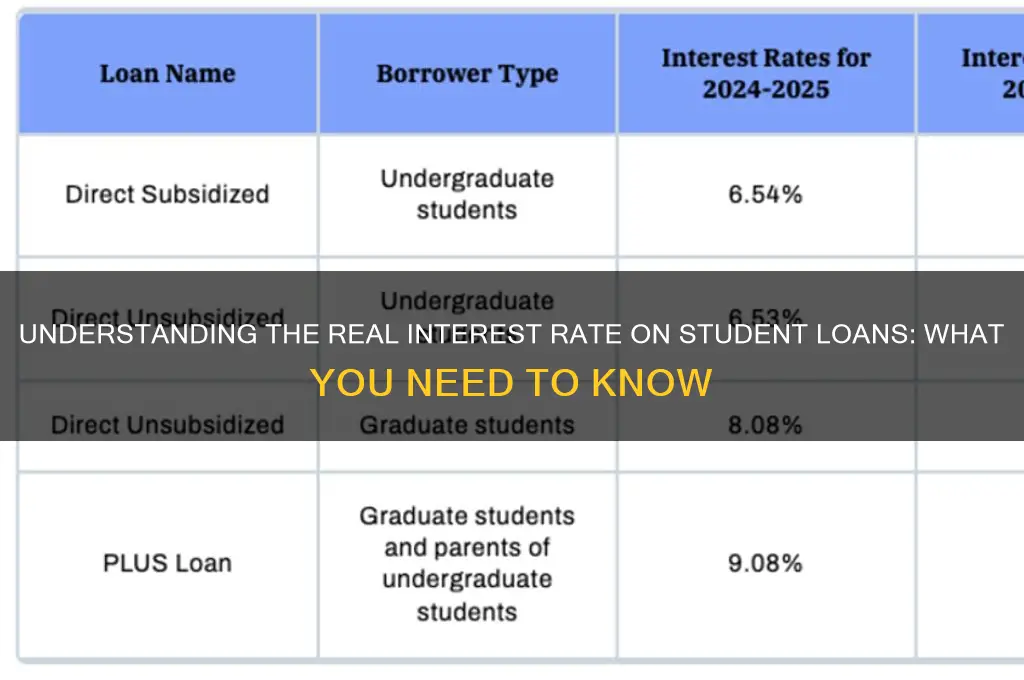

When considering student loans, one of the most critical factors to evaluate is the interest rate, as it significantly impacts the total cost of borrowing. Federal student loans and private student loans offer different interest rate structures, and understanding these differences is essential for making an informed decision. Federal student loans, which are government-backed, typically offer fixed interest rates that are set by Congress and remain consistent for the life of the loan. For the 2023-2024 academic year, undergraduate federal loans carry an interest rate of 5.5%, while graduate loans are at 7.05%, and PLUS loans (for parents and graduate students) are at 8.05%. These rates are generally lower than those offered by private lenders and come with additional benefits such as income-driven repayment plans, loan forgiveness options, and deferment or forbearance in times of financial hardship.

In contrast, private student loans are offered by banks, credit unions, and other financial institutions, and their interest rates can vary widely based on the borrower's creditworthiness, the loan term, and market conditions. Private loan rates can be either fixed or variable, with variable rates often starting lower but fluctuating over time based on economic indices like the LIBOR or Prime Rate. As of recent data, private student loan interest rates typically range from 4% to 12% or higher, depending on the lender and the borrower's financial profile. While some private loans may offer lower rates than federal loans for well-qualified borrowers, they lack the flexible repayment options and protections provided by federal loans.

One key advantage of federal student loans is their predictability and stability. Since the interest rates are fixed and determined by legislation, borrowers know exactly what their rate will be for the entire duration of the loan. This makes budgeting and long-term financial planning easier. Private loans, on the other hand, may offer lower initial rates, but variable rates can increase over time, potentially leading to higher overall costs. Additionally, federal loans do not require a credit check for most borrowers, making them accessible to students with limited or no credit history.

Another important consideration is the repayment flexibility offered by federal loans. Programs like income-driven repayment (IDR) plans tie monthly payments to the borrower's income and family size, making them more manageable for those with lower earnings. Federal loans also offer loan forgiveness options, such as Public Service Loan Forgiveness (PSLF), which private loans do not. Private lenders may offer some forbearance or deferment options, but they are typically less comprehensive and more restrictive than federal programs.

In summary, while private student loans might offer lower interest rates for borrowers with excellent credit, federal student loans generally provide more favorable terms overall due to their fixed rates, repayment flexibility, and borrower protections. When comparing federal vs. private rates, it’s crucial to weigh not only the interest rate but also the long-term benefits and risks associated with each type of loan. For most borrowers, federal loans are the safer and more cost-effective choice, especially for those who may need access to income-driven repayment plans or loan forgiveness programs in the future.

Understanding New Zealand's Student Loan Interest Rates: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Fixed vs. Variable Rates: Analyze the stability of fixed rates versus fluctuating variable rates

When considering student loans, one of the most critical decisions borrowers face is choosing between fixed and variable interest rates. Fixed rates remain constant throughout the life of the loan, providing predictability and stability. This means your monthly payments will stay the same, making it easier to budget and plan for the future. For example, if you secure a fixed rate of 5%, it will remain 5% regardless of economic conditions or market fluctuations. This stability is particularly appealing in uncertain economic times, as it shields borrowers from potential increases in interest rates. However, fixed rates are often higher initially compared to variable rates, as lenders factor in the risk of potential rate hikes over time.

On the other hand, variable rates fluctuate based on market conditions, typically tied to an underlying index such as the London Interbank Offered Rate (LIBOR) or the Prime Rate. While variable rates often start lower than fixed rates, they can increase or decrease over time, depending on economic trends. For instance, during periods of low interest rates, variable rates can be advantageous, reducing the overall cost of the loan. However, if interest rates rise, so will your monthly payments, potentially leading to financial strain. This unpredictability makes variable rates riskier, especially for long-term loans like student debt, where repayment can span decades.

The choice between fixed and variable rates depends heavily on your risk tolerance and financial outlook. If you prefer certainty and are concerned about potential rate increases, a fixed rate offers peace of mind. It’s particularly beneficial if you expect interest rates to rise in the future. Conversely, if you’re comfortable with risk and believe interest rates will remain low or even decrease, a variable rate could save you money in the short to medium term. However, it’s crucial to assess your ability to handle higher payments if rates do rise.

Another factor to consider is the current economic environment. During periods of low interest rates, variable rates may seem more attractive, but it’s essential to remember that rates can—and often do—change. Fixed rates, while higher initially, provide a hedge against future economic uncertainty. Additionally, some lenders offer the option to refinance loans later, which can allow borrowers to switch from a variable to a fixed rate if circumstances change. However, refinancing is not guaranteed and depends on factors like credit score and market conditions.

In conclusion, the decision between fixed and variable rates hinges on your financial stability, risk tolerance, and economic forecasts. Fixed rates offer unwavering stability and predictability, making them ideal for borrowers seeking long-term security. Variable rates, while initially lower, come with the risk of fluctuating payments, which can be a double-edged sword depending on market trends. When evaluating student loan options, carefully weigh the pros and cons of each to determine which aligns best with your financial goals and circumstances. Understanding the real interest rate implications of both options is key to making an informed decision.

Discovering New Horizons: The Most Fascinating Aspect of Student Life

You may want to see also

Explore related products

![]()

Interest Capitalization: Understand how unpaid interest adds to the loan principal

Interest capitalization is a critical concept for student loan borrowers to understand, as it directly impacts the total cost of their loans. When you have an unsubsidized federal student loan or certain private loans, any unpaid interest that accrues while you’re in school, during grace periods, or in deferment may be added to the principal balance of your loan. This process is known as interest capitalization, and it effectively increases the amount you owe, as future interest is then calculated on a larger principal. For example, if you borrow $10,000 and $1,000 in interest accrues while you’re in school, that $1,000 is added to the principal, making your new loan balance $11,000. This means you’ll pay interest on $11,000 moving forward, rather than the original $10,000.

The real interest rate on student loans becomes even more significant when interest capitalization occurs, as it compounds the cost of borrowing. To illustrate, if your loan has a 5% interest rate and $500 in unpaid interest capitalizes, that $500 becomes part of the principal. Over time, you’ll pay 5% interest on the new, higher balance, which includes the capitalized interest. This can lead to a substantial increase in the total amount you repay over the life of the loan. For borrowers with multiple periods of capitalization (such as during grace periods or deferment), the effect is cumulative, making it essential to minimize unpaid interest whenever possible.

One of the most effective ways to avoid interest capitalization is to make interest payments while you’re in school or during grace periods, even if they’re not required. For example, if your monthly accruing interest is $25, paying this amount regularly prevents it from capitalizing and keeps your loan balance from growing. While this may be challenging for students with limited income, even small payments can make a difference. Some borrowers also consider refinancing their loans after graduation to secure a lower interest rate, which can reduce the impact of capitalization if it occurs later.

It’s important to note that not all student loans capitalize interest in the same way. Subsidized federal loans, for instance, do not capitalize interest while the borrower is in school, during the grace period, or in deferment, as the government covers the interest during these times. Private loans, however, often capitalize interest more frequently, and their terms can vary widely. Borrowers should carefully review their loan agreements to understand when and how interest capitalization applies to their specific loans. Knowing these details can help you make informed decisions to manage your debt effectively.

Finally, understanding the real interest rate on your student loans in the context of interest capitalization is crucial for long-term financial planning. The real interest rate accounts for inflation and reflects the true cost of borrowing. When combined with the effects of capitalization, a seemingly low nominal interest rate can result in significantly higher repayment amounts. For instance, a 6% nominal interest rate may translate to a higher real interest rate when inflation is low, and if capitalization occurs, the effective rate you pay over time increases further. By staying informed and proactive, borrowers can minimize the impact of interest capitalization and better manage their student loan debt.

Understanding the Maximum Interest Rates on Student Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Plans Impact: Explore how income-driven plans affect long-term interest costs

Income-driven repayment (IDR) plans are designed to make federal student loan payments more manageable by capping monthly payments at a percentage of the borrower’s discretionary income. While these plans offer immediate relief by lowering monthly payments, they significantly impact long-term interest costs. Unlike standard repayment plans, where the loan balance decreases steadily over time, IDR plans often result in borrowers paying less than the accruing interest each month, especially if their income is low relative to their debt. This can lead to *interest capitalization*, where unpaid interest is added to the principal balance, causing the total debt to grow over time. For example, if a borrower’s monthly payment does not cover the accruing interest, the difference is capitalized, increasing the loan balance and the total interest paid over the life of the loan.

The real interest rate on student loans, which accounts for inflation and the actual cost of borrowing, becomes even more critical under IDR plans. Federal student loans typically have fixed interest rates, but the effective cost of borrowing increases when interest capitalization occurs. Borrowers on IDR plans may find themselves in a situation where their loan balances grow despite making consistent payments. This is particularly true for those with high debt-to-income ratios, as their monthly payments may not keep pace with the accruing interest. Over time, this can result in significantly higher total repayment amounts compared to standard plans, even though IDR plans offer loan forgiveness after 20–25 years of qualifying payments.

Another factor to consider is how IDR plans interact with the real interest rate environment. During periods of high inflation, the real interest rate on student loans may decrease, as inflation erodes the value of the debt. However, if a borrower’s income grows slowly or remains stagnant, their IDR payments may not increase enough to cover the accruing interest, leading to continued capitalization. Conversely, in low-inflation environments, the real interest rate remains closer to the nominal rate, and the impact of capitalization becomes more pronounced. Borrowers must carefully weigh these dynamics when choosing an IDR plan, as the long-term cost of their loans can vary widely based on economic conditions and income growth.

IDR plans also have implications for borrowers pursuing Public Service Loan Forgiveness (PSLF) or other forgiveness programs. While these plans can reduce monthly payments and provide a pathway to forgiveness, the growing loan balance due to interest capitalization can complicate financial planning. Borrowers must ensure they remain in qualifying repayment plans and make on-time payments to maximize their chances of forgiveness. Additionally, the tax implications of forgiven debt should be considered, as forgiven amounts may be treated as taxable income, further affecting the overall cost of borrowing.

In summary, income-driven repayment plans can provide much-needed flexibility for borrowers with limited incomes, but they often come with higher long-term interest costs due to interest capitalization. The real interest rate on student loans plays a crucial role in this dynamic, as it determines the actual cost of borrowing after accounting for inflation. Borrowers must carefully evaluate their income growth prospects, economic conditions, and forgiveness eligibility when choosing an IDR plan to minimize the impact on their long-term financial health. While these plans offer relief in the short term, they require strategic planning to avoid excessive interest costs over time.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Tax Deductibility: Learn about potential tax benefits for student loan interest payments

When considering the real interest rate on student loans, it's essential to factor in potential tax benefits that can effectively reduce the overall cost of borrowing. One significant advantage for student loan borrowers is the tax deductibility of student loan interest payments. This benefit allows eligible taxpayers to deduct up to $2,500 of the interest paid on qualified student loans from their taxable income, thereby lowering their tax liability. This deduction is particularly valuable because it is an "above-the-line" deduction, meaning you can claim it even if you don’t itemize your deductions. Understanding this tax benefit is crucial, as it directly impacts the real interest rate you pay on your student loans by reducing the after-tax cost of borrowing.

To qualify for the student loan interest deduction, certain criteria must be met. First, the loan must have been taken out solely for qualified education expenses, such as tuition, fees, books, and room and board, for the borrower, their spouse, or dependents. Additionally, the borrower’s income must fall below specific thresholds: as of the latest guidelines, the deduction begins to phase out for single filers with modified adjusted gross income (MAGI) above $70,000 and is completely phased out at $85,000. For married couples filing jointly, the phaseout begins at $140,000 and ends at $170,000. If you meet these criteria, the deduction can significantly offset the real interest rate on your student loans by providing a direct financial benefit at tax time.

Another important aspect of the student loan interest deduction is that it applies to both federal and private student loans, as long as they meet the qualified education expense criteria. However, the loan must be in the borrower’s name, and the borrower must be legally obligated to repay it. Parents who take out loans for their children, for example, cannot claim the deduction unless the loan is in their name. This flexibility makes the deduction accessible to a wide range of borrowers, further reducing the real interest rate burden on student loans.

Maximizing the student loan interest deduction requires careful planning and documentation. Borrowers should keep detailed records of all interest payments made throughout the year, as lenders are required to provide a Form 1098-E, which reports the amount of interest paid. Additionally, if you’re close to the income phaseout thresholds, consider strategies to lower your MAGI, such as contributing to retirement accounts or timing income and deductions strategically. By leveraging this tax benefit effectively, borrowers can effectively lower the real interest rate on their student loans and save money over the life of the loan.

Finally, it’s worth noting that the student loan interest deduction is just one of several tax benefits available to student loan borrowers. For example, the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) provide additional tax credits for qualified education expenses. While these credits are not directly related to interest payments, they can further reduce the overall financial burden of student loans. By combining these benefits with the interest deduction, borrowers can gain a clearer understanding of the real interest rate they’re paying and take proactive steps to minimize their student loan costs.

Understanding Student Loan Interest Rates: A Comprehensive Guide for Borrowers

You may want to see also

Frequently asked questions

The real interest rate on student loans is the nominal interest rate adjusted for inflation. It reflects the actual cost of borrowing after accounting for changes in purchasing power over time.

The nominal interest rate is the stated rate on the loan, while the real interest rate subtracts the inflation rate to show the true cost of borrowing in terms of purchasing power.

The real interest rate helps borrowers understand the true cost of their loans by accounting for inflation. It provides a clearer picture of how much their debt will grow relative to their future earnings and economic conditions.

To calculate the real interest rate, subtract the inflation rate from the nominal interest rate. For example, if your loan has a 6% nominal rate and inflation is 2%, the real interest rate is 4% (6% - 2% = 4%).