When considering student loan interest rates, it is generally observed that federal student loans tend to offer more favorable terms compared to private loans. Federal loans often come with fixed interest rates that are set by the government and are typically lower than those offered by private lenders. Additionally, federal loans provide various repayment plans and forgiveness options, making them a more accessible and flexible choice for many borrowers. On the other hand, private student loans usually have variable interest rates, which can fluctuate over time, potentially leading to higher overall costs. Factors such as credit history, income, and cosigner involvement can influence the interest rates offered by private lenders, making federal loans a more consistent and often more affordable option for students.

Explore related products

What You'll Learn

![]()

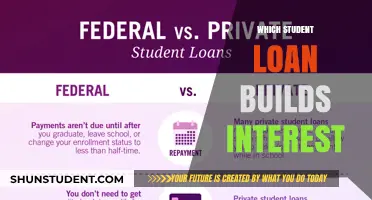

Federal vs. Private Loans

When comparing Federal vs. Private Loans in terms of student loan interest rates, federal loans generally offer more favorable terms. Federal student loans are funded by the U.S. Department of Education and come with fixed interest rates set by Congress. These rates are typically lower than those offered by private lenders, making federal loans a more cost-effective option for most borrowers. For the 2023-2024 academic year, for example, undergraduate federal loan rates were set at 5.5% for Direct Subsidized and Unsubsidized Loans, while private loan rates can range from 4% to 13% or higher, depending on the borrower’s creditworthiness and market conditions.

One key advantage of federal loans is their borrower-friendly repayment options, which are not typically available with private loans. Federal loans offer income-driven repayment plans that cap monthly payments at a percentage of the borrower’s income, as well as options for loan forgiveness after a certain number of qualifying payments. Private loans, on the other hand, rarely provide such flexibility. Their repayment terms are often stricter, and interest rates can be variable, meaning they may increase over time, adding to the overall cost of the loan.

Another factor to consider is credit requirements. Federal student loans do not require a credit check (except for PLUS Loans), making them accessible to students with limited or poor credit history. Private lenders, however, typically require a strong credit profile or a cosigner to qualify for the lowest interest rates. This can be a significant barrier for students who are just starting to build their credit or lack a cosigner with good credit.

Loan forgiveness programs are another area where federal loans outshine private loans. Programs like Public Service Loan Forgiveness (PSLF) offer the opportunity to have remaining loan balances forgiven after 10 years of qualifying payments and employment in public service. Private loans do not offer such forgiveness programs, meaning borrowers are responsible for repaying the full amount, regardless of their career path or financial situation.

In summary, while private loans may occasionally offer competitive rates to borrowers with excellent credit, federal loans generally provide better interest rates and terms for the majority of students. Their fixed rates, flexible repayment options, and access to loan forgiveness programs make them a more secure and predictable choice. Borrowers should exhaust federal loan options before considering private loans, as federal loans are designed to prioritize affordability and accessibility for students.

Which Student Loan Type Carries the Highest Interest Rates?

You may want to see also

Explore related products

![]()

Credit Score Impact

When considering who generally has better student loan interest rates, it’s essential to understand the role of credit scores in this process. Lenders, whether they are private institutions or government programs, often use credit scores as a key factor in determining interest rates. A higher credit score typically indicates lower financial risk to the lender, which can result in more favorable interest rates for the borrower. Conversely, a lower credit score may lead to higher interest rates, as lenders may perceive the borrower as a greater risk. This dynamic is particularly relevant in private student loans, where creditworthiness plays a significant role in the terms offered.

The credit score impact on student loan interest rates is most pronounced in private loans. Private lenders often require a credit check to assess the borrower’s financial history and reliability. Borrowers with excellent credit scores (typically 750 or above) are more likely to secure lower interest rates, as they demonstrate a history of responsible financial behavior. On the other hand, borrowers with fair or poor credit scores may face higher interest rates or may need a cosigner to qualify for a loan. A cosigner with a strong credit score can help mitigate the lender’s risk, potentially leading to better interest rates for the primary borrower.

For federal student loans, the credit score impact is less direct but still relevant in certain scenarios. Most federal loans, such as Direct Subsidized and Unsubsidized Loans, do not require a credit check, and interest rates are standardized based on the type of loan and the disbursement date. However, federal PLUS Loans, which are available to graduate students and parents, do consider credit history. Borrowers with adverse credit (such as recent bankruptcies or delinquent accounts) may be denied a PLUS Loan or may need an endorser to qualify. While federal loan interest rates are generally fixed and not personalized based on credit scores, the ability to qualify for certain federal loans can still be influenced by creditworthiness.

Improving one’s credit score can have a long-term credit score impact on student loan interest rates, especially when refinancing or taking out private loans. Borrowers with higher credit scores may be eligible for refinancing options that offer lower interest rates, reducing the overall cost of their student debt. Actions such as paying bills on time, reducing credit card balances, and avoiding new debt can help improve a credit score over time. Additionally, regularly monitoring credit reports for errors and addressing them promptly can ensure that a borrower’s credit score accurately reflects their financial responsibility.

Lastly, the credit score impact extends beyond just the interest rate to other loan terms and opportunities. A strong credit score can open doors to additional financial products, such as credit cards with rewards or personal loans with favorable terms, which can indirectly support a borrower’s ability to manage student loan debt. Conversely, a poor credit score can limit financial flexibility and increase the cost of borrowing in the future. Therefore, maintaining a good credit score is not only beneficial for securing better student loan interest rates but also for overall financial health and stability.

Understanding the Student Loan Interest Deduction on Your 1040 Form

You may want to see also

Explore related products

![]()

Loan Type Differences

When comparing student loan interest rates, one of the most critical factors to consider is the type of loan being offered. Student loans generally fall into two broad categories: federal student loans and private student loans. Each type has distinct characteristics that directly impact the interest rates borrowers receive. Federal student loans are issued by the U.S. Department of Education and typically offer lower, fixed interest rates set by Congress. These rates are standardized and do not vary based on the borrower's credit history. For example, as of the 2023-2024 academic year, undergraduate federal loans have a fixed rate of 5.5%, while graduate loans are at 7.05%. Federal loans also come with borrower protections, such as income-driven repayment plans and loan forgiveness options, which can provide long-term financial flexibility.

In contrast, private student loans are offered by banks, credit unions, and other financial institutions. Their interest rates are highly variable and depend on the borrower's credit score, income, and other financial factors. Private loans often have higher interest rates than federal loans, especially for borrowers with limited or poor credit history. Additionally, private loans may offer variable interest rates, which can fluctuate over time based on market conditions, potentially increasing the overall cost of the loan. While some private lenders advertise competitive rates that may be lower than federal rates for well-qualified borrowers, they lack the protections and repayment options available with federal loans.

Another key difference lies in subsidized vs. unsubsidized federal loans. Subsidized federal loans are available to undergraduate students with demonstrated financial need, and the government pays the interest on these loans while the borrower is in school, during the grace period, and in deferment. This feature effectively reduces the overall cost of the loan. Unsubsidized federal loans, on the other hand, accrue interest from the time they are disbursed, regardless of the borrower's enrollment status. Graduate students and students without financial need may only qualify for unsubsidized loans, which can result in higher total repayment amounts.

Parent PLUS loans, another federal loan type, are available to parents of dependent undergraduate students. These loans generally have higher interest rates than undergraduate federal loans, with rates set at 8.05% for the 2023-2024 academic year. While they offer the same fixed-rate structure as other federal loans, the higher rate reflects the increased risk associated with lending to parents rather than students. Parent PLUS loans also have fewer repayment options compared to other federal loans, making them a less favorable choice for some families.

Lastly, refinancing options can impact interest rates for both federal and private loans. Private lenders offer refinancing opportunities that allow borrowers to replace their existing loans with a new loan at a potentially lower interest rate. However, refinancing federal loans into private loans eliminates access to federal protections and repayment plans. For borrowers with high-interest private loans or those with improved credit since taking out their loans, refinancing can be a viable strategy to secure better rates. However, it’s essential to weigh the benefits against the loss of federal loan advantages.

In summary, the type of student loan significantly influences the interest rates borrowers receive. Federal loans generally offer lower, fixed rates with borrower protections, while private loans provide variable rates based on creditworthiness. Understanding these differences is crucial for making informed decisions about financing education and managing long-term debt.

Maximize Your Savings: Where to Find Student Loan Interest Tax Deductions

You may want to see also

Explore related products

![]()

Cosigner Benefits

When it comes to securing better student loan interest rates, having a cosigner can be a game-changer. A cosigner is typically a person with a strong credit history who agrees to share responsibility for the loan, and their involvement can significantly impact the terms of the loan. Generally, private student loans offer more competitive interest rates when a cosigner is involved, as lenders view these loans as less risky. This is because the cosigner’s creditworthiness provides an additional layer of security, assuring the lender that the loan is more likely to be repaid. As a result, borrowers with cosigners often qualify for lower interest rates compared to those applying independently, especially if the borrower has limited or poor credit history.

One of the primary benefits of having a cosigner is the potential for substantial interest rate reductions. Lenders often use the cosigner’s credit score and financial stability to determine the loan terms, which can lead to rates that are significantly lower than what the borrower would receive on their own. For example, a borrower with a fair credit score might face double-digit interest rates without a cosigner, but with a cosigner who has excellent credit, the rate could drop by several percentage points. Over the life of the loan, this reduction can save thousands of dollars in interest payments, making repayment more manageable and less financially burdensome.

Another advantage of having a cosigner is the increased likelihood of loan approval. Many students, especially those just starting their academic journey, have little to no credit history, which can make it difficult to qualify for private student loans. A cosigner with a strong credit profile can bridge this gap, improving the chances of approval. This is particularly beneficial for borrowers pursuing higher education at expensive institutions or in fields requiring significant financial investment, as it ensures access to the necessary funds without relying solely on federal aid or high-interest loans.

Cosigners also provide flexibility in loan terms, allowing borrowers to choose repayment plans that align with their financial situation. With a cosigner, borrowers may qualify for longer repayment terms or deferred payment options, which can lower monthly payments and ease the financial strain during the early years of a career. Additionally, some lenders offer cosigner release options after a certain number of on-time payments, allowing the borrower to take full responsibility for the loan once they’ve established their own creditworthiness. This not only benefits the borrower but also protects the cosigner by removing their obligation after a set period.

Lastly, having a cosigner can educate borrowers about financial responsibility and credit management. By working with a cosigner, often a family member or trusted friend, borrowers gain insight into the importance of maintaining a good credit score and managing debt wisely. This mentorship aspect can be invaluable, as it encourages borrowers to develop healthy financial habits that will benefit them long after the student loan is repaid. In essence, a cosigner not only helps secure better interest rates but also contributes to the borrower’s long-term financial success.

Understanding Student Loan Interest: When Does Compounding Begin?

You may want to see also

Explore related products

$16.53 $22.99

![]()

Repayment Plan Effects

When considering who generally has better student loan interest rates, it’s important to recognize that repayment plans play a significant role in determining the overall cost of borrowing. Different repayment plans can affect interest accrual, monthly payments, and the total amount repaid over time. For instance, federal student loans often offer income-driven repayment (IDR) plans, which can lower monthly payments based on income and family size. However, these plans may result in more interest accruing over the life of the loan, especially if payments are insufficient to cover the monthly interest. Conversely, standard repayment plans typically have higher monthly payments but minimize interest costs by ensuring the loan is paid off in a shorter period, usually 10 years.

The choice of repayment plan directly impacts the effective interest rate a borrower experiences. For example, borrowers with high incomes may opt for standard or accelerated repayment plans to pay off their loans faster, thereby reducing the total interest paid. On the other hand, borrowers with lower incomes might choose IDR plans to manage cash flow, even though this could lead to higher overall interest costs due to extended repayment terms. Private student loans, which generally have fixed or variable interest rates, often lack the flexibility of federal repayment plans, making it crucial for borrowers to carefully consider their repayment strategy from the outset.

Repayment plans also influence eligibility for loan forgiveness programs, which can indirectly affect interest rates. For instance, borrowers on IDR plans may qualify for loan forgiveness after 20–25 years of consistent payments, effectively capping the total interest paid. This makes IDR plans particularly beneficial for borrowers with high debt relative to their income. In contrast, borrowers on standard plans do not typically qualify for forgiveness unless they work in public service, meaning they must pay off the full principal and interest without relief.

Another critical aspect of repayment plan effects is how they interact with interest capitalization. For federal loans, unpaid interest can capitalize (be added to the principal balance) when a borrower leaves a deferment or forbearance period or switches out of an IDR plan. This increases the total amount of interest that accrues over time. Borrowers on IDR plans may avoid capitalization if their payments cover at least the monthly interest, but those with partial financial hardship may still face capitalization, worsening their interest burden.

Lastly, repayment plans can impact credit scores and financial flexibility. Consistently making payments on time under any plan helps build credit, but missed payments due to unaffordable monthly amounts (common in standard plans for some borrowers) can harm credit scores. IDR plans, by reducing monthly payments, may help borrowers avoid delinquency or default, preserving their creditworthiness. However, the trade-off is often higher long-term interest costs. Borrowers must weigh these factors when selecting a repayment plan to optimize both short-term affordability and long-term interest savings.

Understanding the Federal Student Loan Interest Paid Tax Form

You may want to see also

Frequently asked questions

Federal student loans generally offer better interest rates than private lenders because they are subsidized by the government and have fixed rates set by law.

Undergraduate students often receive lower interest rates on federal loans compared to graduate students, as Direct Subsidized Loans are only available to undergraduates, and graduate loans tend to have higher rates.

For private student loans, borrowers with higher credit scores typically qualify for better interest rates, whereas federal student loan rates are not based on credit score.

Adding a cosigner with strong credit can help borrowers secure lower interest rates on private student loans, but it does not impact federal loan rates, which are standardized.