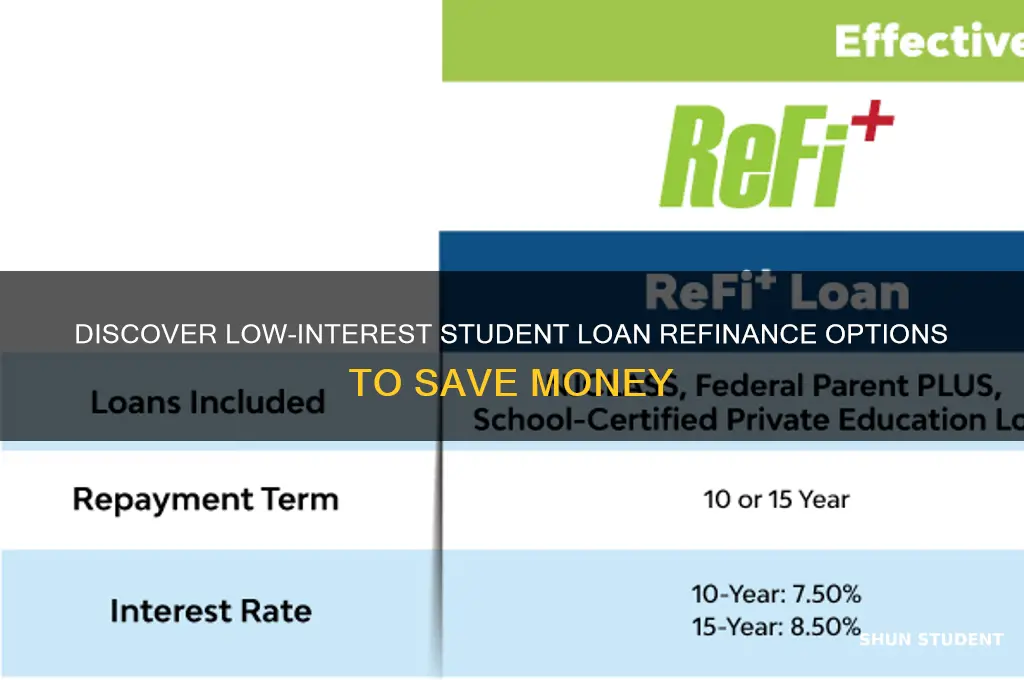

Refinancing student loans can be a smart financial move for borrowers looking to lower their monthly payments or reduce the total interest paid over the life of the loan. When considering refinancing, one of the most critical factors is finding lenders that offer low interest rates. Currently, several financial institutions, including online lenders like SoFi, Earnest, and CommonBond, as well as traditional banks such as Citizens Bank and Laurel Road, are known for competitive refinancing rates. Eligibility for these low rates often depends on factors like credit score, income stability, and debt-to-income ratio. Borrowers with excellent credit and a strong financial profile are more likely to secure the lowest available rates, making it essential to shop around and compare offers to find the best deal. Additionally, federal loan borrowers should weigh the benefits of refinancing against the loss of federal protections, such as income-driven repayment plans and loan forgiveness programs.

Explore related products

$14.01 $29.99

What You'll Learn

![]()

Federal Student Loan Refinancing Options

When considering Federal Student Loan Refinancing Options, it’s important to understand that federal loans cannot be refinanced through the federal government itself. However, borrowers can refinance federal loans into private loans, which may offer lower interest rates. This process, known as private student loan refinancing, replaces existing federal loans with a new private loan, often at a lower interest rate. While this can reduce monthly payments or shorten the loan term, it’s crucial to weigh the benefits against the loss of federal protections, such as income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options.

One of the primary reasons borrowers explore refinancing is to secure a lower interest rate. Private lenders like SoFi, Earnest, Laurel Road, and CommonBond are known for offering competitive rates, especially for borrowers with strong credit histories and stable incomes. These lenders often advertise variable rates starting as low as 2-4% and fixed rates around 3-6%, depending on market conditions and the borrower’s financial profile. To qualify for the lowest rates, borrowers typically need a credit score of 700 or higher and a debt-to-income ratio that demonstrates financial stability.

Before refinancing federal loans, borrowers should carefully evaluate their financial goals. If the primary aim is to reduce monthly payments, refinancing to a lower interest rate with a longer repayment term can achieve this. However, extending the loan term may result in paying more interest over time. Conversely, refinancing to a shorter term can save money on interest but will increase monthly payments. Borrowers should use online calculators provided by lenders to compare scenarios and determine the best option for their situation.

It’s also essential to consider alternatives to refinancing federal loans. For example, federal programs like income-driven repayment plans can lower monthly payments based on income and family size, and they may offer loan forgiveness after 20-25 years of qualifying payments. Additionally, the Public Service Loan Forgiveness (PSLF) program forgives remaining federal loan balances after 10 years of payments for eligible borrowers working in public service. These options retain federal benefits and may be more advantageous than refinancing, depending on the borrower’s career path and financial circumstances.

For those still determined to refinance federal loans, shopping around for the best offer is critical. Borrowers should compare interest rates, fees, repayment terms, and customer service from multiple lenders. Some lenders offer perks like rate discounts for autopay, career coaching, or unemployment protection, which can add value to the refinancing deal. Additionally, checking prequalified rates with several lenders allows borrowers to assess their options without impacting their credit score, as this typically involves a soft credit inquiry.

In summary, while Federal Student Loan Refinancing Options technically do not exist through the federal government, refinancing federal loans into private loans can provide access to lower interest rates. However, borrowers must carefully consider the trade-offs, including the loss of federal protections. Private lenders like SoFi, Earnest, and Laurel Road offer competitive rates, but eligibility depends on creditworthiness. Exploring federal repayment plans and forgiveness programs is also advisable before committing to refinancing. By thoroughly researching and comparing options, borrowers can make an informed decision that aligns with their long-term financial goals.

When Does Accrued Interest Increase Your Student Loan Balance?

You may want to see also

Explore related products

![]()

Private Lenders with Competitive Rates

When considering refinancing student loans, private lenders often emerge as strong contenders due to their competitive interest rates and flexible terms. These lenders cater to borrowers seeking to lower their monthly payments or reduce the overall cost of their loans. Among the top private lenders offering low interest rates are SoFi, Earnest, and Laurel Road. Each of these lenders has carved a niche in the student loan refinancing market by providing rates that often undercut federal loan options, especially for borrowers with strong credit histories and stable incomes.

SoFi stands out for its comprehensive approach to refinancing, offering fixed and variable rates that are among the lowest in the industry. Borrowers can also take advantage of additional perks such as career coaching and unemployment protection. To qualify for SoFi’s most competitive rates, applicants typically need a credit score of at least 650 and a steady income source. The lender’s streamlined online application process makes it easy for borrowers to check their rates without impacting their credit score.

Earnest is another private lender known for its competitive rates, particularly for borrowers with high earning potential and low debt-to-income ratios. Unlike many lenders, Earnest considers factors beyond credit scores, such as savings habits and career trajectory, to determine eligibility and rates. This personalized approach often results in lower interest rates for qualified applicants. Additionally, Earnest allows borrowers to customize their loan terms, providing greater flexibility in managing monthly payments.

Laurel Road is highly regarded for its refinancing options tailored to medical and dental professionals, though it serves borrowers from all fields. The lender offers some of the lowest fixed and variable rates available, with no application or origination fees. Laurel Road also provides a quick online application process and the option to defer payments for up to 18 months for qualifying medical residents. Its competitive rates and borrower-friendly policies make it a top choice for many refinancing their student loans.

When exploring private lenders with competitive rates, it’s essential to compare offers carefully. Factors such as loan terms, repayment options, and additional benefits should be considered alongside interest rates. Borrowers should also be mindful of the trade-offs, such as losing federal loan protections like income-driven repayment plans or loan forgiveness programs when refinancing with a private lender. By researching and applying to multiple lenders, borrowers can secure the lowest possible interest rates and optimize their student loan repayment strategy.

When Does 0% Interest End on Student Loans?

You may want to see also

Explore related products

$16.29 $19.95

$109 $149.99

![]()

Credit Score Impact on Rates

When considering refinancing student loans, your credit score plays a pivotal role in determining the interest rates you qualify for. Lenders use credit scores as a primary indicator of your financial reliability and risk level. Generally, a higher credit score signals to lenders that you are a responsible borrower, which can lead to lower interest rates. Conversely, a lower credit score may result in higher rates or even disqualification from certain refinancing options. Understanding this relationship is crucial for anyone looking to secure the best possible terms when refinancing student loans.

A credit score typically ranges from 300 to 850, with scores above 700 considered good and scores above 750 deemed excellent. Borrowers with excellent credit scores are more likely to qualify for the lowest interest rates available. For instance, lenders like SoFi, Earnest, and Laurel Road often offer competitive rates to borrowers with strong credit histories. These lenders may advertise rates as low as 2-4% for fixed APRs, but such offers are usually reserved for individuals with top-tier credit scores. If your credit score falls below 650, you may find it challenging to secure favorable rates, and some lenders might not approve your application at all.

Improving your credit score before refinancing can significantly impact the rates you’re offered. Steps such as paying down existing debt, ensuring on-time payments, and correcting any errors on your credit report can boost your score over time. Additionally, having a co-signer with a strong credit profile can help you qualify for lower rates if your own score is insufficient. However, relying on a co-signer comes with its own risks, as they become equally responsible for the loan.

It’s also important to note that not all lenders weigh credit scores equally. Some lenders, like CommonBond or Citizens Bank, may consider other factors such as your income, employment history, and educational background in addition to your credit score. However, your credit score remains a dominant factor in the underwriting process. Comparing offers from multiple lenders can help you find the best rates based on your unique financial situation, even if your credit score isn’t perfect.

Lastly, refinancing with a low credit score isn’t impossible, but it requires careful strategy. Some lenders specialize in working with borrowers who have fair or poor credit, though their rates may be higher. Federal student loan refinancing isn’t an option, as federal loans cannot be refinanced through private lenders, but private student loans can be refinanced to potentially lower your interest rate. Monitoring your credit score regularly and taking steps to improve it will position you to secure the lowest possible rates when refinancing student loans.

Where Does Student Loan Interest Go on Your Tax Return?

You may want to see also

Explore related products

$9.91 $26.99

![]()

Variable vs. Fixed Interest Rates

When considering refinancing student loans, one of the most critical decisions borrowers face is choosing between variable and fixed interest rates. Both options have distinct advantages and drawbacks, and understanding them is essential to securing the lowest possible interest rate. A fixed interest rate remains constant throughout the life of the loan, providing predictability and stability in monthly payments. This is particularly appealing in a rising interest rate environment, as borrowers are shielded from potential increases. On the other hand, variable interest rates fluctuate based on market conditions, typically tied to an index like the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR). Initially, variable rates are often lower than fixed rates, making them an attractive option for those who plan to pay off their loans quickly or expect interest rates to remain stable or decline.

For borrowers seeking the lowest interest rates to refinance student loans, variable rates often appear more enticing upfront. Lenders like SoFi, Earnest, and Laurel Road frequently offer competitive variable rates that are significantly lower than their fixed-rate options. However, this comes with inherent risk. If market interest rates rise, so will the borrower's monthly payments, potentially increasing the overall cost of the loan. Borrowers with variable rates must be financially prepared for this uncertainty, especially if they are on a tight budget. Conversely, fixed rates from lenders such as CommonBond, Citizens Bank, and Discover Student Loans provide long-term security, ensuring that payments remain unchanged regardless of economic conditions.

The choice between variable and fixed rates largely depends on the borrower's financial situation, risk tolerance, and outlook on interest rates. For instance, if a borrower expects to pay off their loan within a few years and believes interest rates will remain low or decrease, a variable rate could save them money. However, if the borrower values consistency and wants to avoid the risk of rising payments, a fixed rate is the safer option. It’s also worth noting that some lenders offer hybrid options or allow borrowers to switch from variable to fixed rates for a fee, providing additional flexibility.

Another factor to consider is the current economic climate. In a low-interest-rate environment, variable rates may seem particularly appealing, but borrowers should be cautious about potential future increases. Conversely, in a high-interest-rate environment, fixed rates may be more competitive, offering protection against further hikes. Prospective refinancers should research historical interest rate trends and consult financial advisors to make an informed decision.

Ultimately, the decision between variable and fixed interest rates hinges on personal circumstances and financial goals. Borrowers prioritizing low initial payments and willing to accept risk may lean toward variable rates, while those seeking stability and long-term predictability will likely prefer fixed rates. When comparing lenders for the lowest interest rates to refinance student loans, it’s crucial to evaluate both options carefully, considering not just the rate itself but also the potential long-term implications. Lenders like Splash Financial and LendKey often provide tools and resources to help borrowers model different scenarios, aiding in this critical decision-making process.

In summary, while variable rates often start lower and can be advantageous in certain situations, fixed rates offer peace of mind and protection against market volatility. Borrowers should assess their financial health, repayment timeline, and economic forecasts before choosing. By doing so, they can ensure that their decision aligns with their goals and maximizes the benefits of refinancing their student loans.

Unveiling the Destination: Where Federal Student Loan Interest Ends Up

You may want to see also

Explore related products

![]()

Refinancing Eligibility Requirements

When considering refinancing student loans to secure a lower interest rate, understanding the eligibility requirements is crucial. Lenders typically assess several factors to determine if you qualify for refinancing. One of the primary requirements is a strong credit score, usually in the range of 650 or higher, though some lenders may require scores of 700 or more for the best rates. A higher credit score demonstrates financial responsibility and reduces the lender's risk, making you a more attractive candidate for refinancing. If your credit score is below the threshold, you may still qualify by adding a creditworthy cosigner to your application.

Another key eligibility factor is your income and employment status. Lenders want to ensure you have a stable and sufficient income to repay the loan. Most require a minimum annual income, often ranging from $30,000 to $40,000, though this can vary. Additionally, you typically need to be employed or have a job offer in place. Some lenders may also consider your debt-to-income ratio (DTI), which compares your monthly debt payments to your monthly gross income. A lower DTI, generally below 50%, improves your chances of approval.

The type and status of your existing student loans also play a role in refinancing eligibility. Most lenders refinance both federal and private student loans, but some may have restrictions. For example, if you have federal loans, refinancing them with a private lender means losing access to federal benefits like income-driven repayment plans and loan forgiveness programs. Additionally, your loans must typically be in good standing, meaning they are not in default or delinquency. Some lenders may also require that you have completed your degree, while others may refinance loans for non-degree programs or certificates.

Your financial history and overall creditworthiness are further scrutinized during the refinancing process. Lenders may review your payment history, looking for consistent, on-time payments on existing debts. They may also assess your savings and assets to gauge your financial stability. A history of responsible financial management increases your likelihood of approval. Additionally, some lenders require a minimum loan amount, often $5,000 to $10,000, and a maximum loan limit, which can range from $100,000 to $500,000 or more, depending on the lender and your degree type.

Lastly, citizenship and residency status are important eligibility criteria. Most lenders require borrowers to be U.S. citizens or permanent residents, though some may work with international students who have a cosigner who is a U.S. citizen or resident. Proof of identity and residency, such as a Social Security number, driver’s license, or passport, is typically required during the application process. Understanding these eligibility requirements will help you identify which lenders offering low interest rates are the best fit for your financial situation.

Understanding Student Loan Interest Refunds: What Percentage Can You Recover?

You may want to see also

Frequently asked questions

Interest rates for student loan refinancing vary by lender, but as of recent data, lenders like Earnest, SoFi, and Laurel Road often offer competitive rates starting as low as 2-4% for qualified borrowers.

Federal student loans typically have fixed interest rates set by the government, which may be higher than private refinancing rates for borrowers with excellent credit. However, federal loans offer benefits like income-driven repayment plans and loan forgiveness programs that private loans do not.

Borrowers with a high credit score (typically 700+), stable income, and a low debt-to-income ratio are most likely to qualify for the lowest interest rates when refinancing student loans.

Yes, credit unions like PenFed and banks like Citizens Bank often offer competitive refinancing rates, especially for members or customers with strong financial profiles.

Yes, adding a cosigner with a strong credit history can help you qualify for lower interest rates, as it reduces the lender’s risk. However, not all lenders allow cosigners for refinancing.