The end of the 0% interest period on student loans is a pressing concern for many borrowers, as it marks a significant shift in repayment obligations. This interest-free period, implemented as a temporary relief measure during the COVID-19 pandemic, has allowed millions to pause payments and avoid accruing interest on their federal student loans. However, with the resumption of payments on the horizon, borrowers are eager to know when this benefit will expire. Understanding the exact date when 0% interest ends is crucial for financial planning, as it will impact monthly payments and overall loan balances, prompting borrowers to explore repayment strategies and potential forgiveness programs to manage their debt effectively.

| Characteristics | Values |

|---|---|

| End Date of 0% Interest Period | September 30, 2024 (as per recent extensions) |

| Applicable Loans | Federal student loans held by the U.S. Department of Education |

| Interest Rate After End Date | Returns to original rates (e.g., 4.99% for undergraduate Direct Loans) |

| Payment Resumption | October 2024 (exact date varies by servicer) |

| COVID-19 Relief Measure | Part of the CARES Act and subsequent extensions |

| Impact on Borrowers | Resumed payments and interest accrual after the end date |

| Loan Forgiveness Programs | Unaffected by the end of 0% interest period |

| Private Student Loans | Not eligible for 0% interest; terms vary by lender |

| Announcements | Updates provided by the U.S. Department of Education |

| Preparation for Borrowers | Recommended to contact loan servicers for updated payment details |

Explore related products

What You'll Learn

- Grace Period Length: Understand the duration before interest accrues after graduation or leaving school

- Loan Type Differences: Federal vs. private loans have varying 0% interest end dates

- Deferment Impact: How postponing payments affects when interest-free periods conclude

- COVID-19 Extensions: Temporary relief measures and their expiration timelines for student loans

- Repayment Plan Effects: Income-driven plans may alter when 0% interest ends

![]()

Grace Period Length: Understand the duration before interest accrues after graduation or leaving school

The grace period on student loans is a critical aspect for borrowers to understand, as it directly impacts when interest begins to accrue after graduation or leaving school. For federal student loans, the grace period typically lasts six months for most loan types, including Direct Subsidized and Unsubsidized Loans. This means borrowers have a six-month window after their education ends before they are required to start making payments. During this time, interest does not accrue on subsidized loans, but it does on unsubsidized loans, though payment is not required until the grace period ends. This period allows graduates to transition into the workforce and prepare financially for repayment.

For Perkins Loans, the grace period is also six months, similar to other federal loans. However, it’s important to note that Perkins Loans are no longer being issued as of 2017, so this applies only to existing borrowers. On the other hand, PLUS Loans for parents and graduate students do not have a traditional grace period. Instead, repayment begins immediately after the loan is fully disbursed, unless the borrower requests a deferment while the student is enrolled at least half-time. Understanding these differences is essential for managing repayment effectively.

Private student loans often have varying grace periods, which can range from zero to twelve months, depending on the lender. Some private lenders may offer no grace period at all, meaning interest begins accruing immediately after graduation or leaving school. Others may provide a longer grace period as an incentive. Borrowers should carefully review their loan agreements to determine the exact duration and plan accordingly. Unlike federal loans, private loans are less standardized, making it crucial to understand the terms specific to your lender.

It’s also important to consider how the grace period interacts with deferment and forbearance options. For federal loans, borrowers may be eligible for additional deferment if they return to school or experience economic hardship. Private loans may offer forbearance options but typically do not provide the same flexibility as federal loans. Knowing these options can help borrowers avoid unnecessary interest accrual and financial strain.

Lastly, borrowers should be aware that the grace period is a one-time benefit and does not reset if they return to school after using it. For example, if a borrower uses their six-month grace period after graduating with a bachelor’s degree and then enrolls in a graduate program, the grace period will not apply again upon completion of the graduate degree. Planning ahead and understanding these nuances can help borrowers make informed decisions about their student loan repayment strategy.

Reddit's Guide to Understanding Your Student Loan Interest Rate

You may want to see also

Explore related products

![]()

Loan Type Differences: Federal vs. private loans have varying 0% interest end dates

The end date for 0% interest on student loans varies significantly between federal and private loans, primarily due to differences in their governing policies and structures. For federal student loans, the U.S. Department of Education has implemented temporary measures in response to economic conditions, such as the COVID-19 pandemic. As of recent updates, the 0% interest period on federal student loans has been extended multiple times, with the current end date tied to specific legislative or executive actions. For instance, during the pandemic, federal loan interest was paused, and no interest accrued, with the end date subject to further extensions based on federal policy decisions. Borrowers should monitor announcements from the Department of Education or their loan servicers to stay informed about any changes.

In contrast, private student loans operate under different terms, as they are issued by banks, credit unions, or other financial institutions. Private lenders are not bound by federal policies and typically do not offer extended 0% interest periods unless explicitly stated in the loan agreement. The end date for 0% interest on private loans, if applicable, is usually defined in the loan contract and is often tied to specific conditions, such as in-school deferment or grace periods. Once these conditions expire, interest begins to accrue, and borrowers are responsible for repayment. Private loan borrowers must carefully review their loan terms to understand when interest will resume.

Another key difference lies in the flexibility and borrower protections offered by federal loans compared to private loans. Federal loans often include options like income-driven repayment plans, loan forgiveness programs, and extended deferment or forbearance periods, which can indirectly affect interest accrual. During periods of 0% interest, federal loan borrowers can take advantage of these programs to manage their debt more effectively. Private loans, however, rarely offer such protections, and borrowers may face higher financial risk once the 0% interest period ends. This underscores the importance of understanding the specific terms of each loan type.

For federal loan borrowers, the end of the 0% interest period typically means a return to the standard interest rate as outlined in their loan agreement. However, federal loans may also offer additional benefits, such as temporary interest waivers or reduced rates, depending on legislative actions. Private loan borrowers, on the other hand, should prepare for interest to accrue immediately after the agreed-upon 0% interest period ends, often without additional protections or extensions. This makes it crucial for borrowers to plan their finances accordingly and explore refinancing options if necessary.

In summary, the end date for 0% interest on student loans depends heavily on whether the loans are federal or private. Federal loan borrowers benefit from policy-driven extensions and protections, while private loan borrowers must adhere to the terms set by their lenders. Understanding these differences is essential for effective loan management and financial planning. Borrowers should stay informed about updates from their loan servicers and consider their repayment strategies as the 0% interest period approaches its end.

When Do UK Student Loans Begin Accruing Interest?

You may want to see also

Explore related products

![]()

Deferment Impact: How postponing payments affects when interest-free periods conclude

Student loan borrowers often wonder when the interest-free period on their loans will end, especially when considering options like deferment. Deferment allows borrowers to temporarily postpone their loan payments, but it’s crucial to understand how this decision impacts the conclusion of the 0% interest period. For federal student loans, the interest-free period typically applies to subsidized loans while the borrower is in school, during the grace period after graduation, and in certain deferment situations. However, for unsubsidized loans, interest accrues during deferment, which can significantly affect the overall loan balance when payments resume.

When a borrower enters deferment, the treatment of interest depends on the type of loan. For subsidized federal loans, the government pays the interest during deferment, meaning the interest-free period effectively continues. This ensures that the loan balance remains unchanged when payments restart. In contrast, unsubsidized federal loans and most private student loans accrue interest during deferment. This means the borrower will face a higher balance once the deferment period ends, as the unpaid interest is capitalized (added to the principal balance). Understanding this distinction is essential for borrowers to make informed decisions about deferment.

Deferment can extend the timeline for when the 0% interest period concludes, but it does so at a cost for unsubsidized loans. For example, if a borrower defers payments for 12 months on an unsubsidized loan with a 5% interest rate, the accrued interest will be added to the principal. When payments resume, the borrower will be paying interest on a larger balance, increasing the total cost of the loan. This can delay the point at which the borrower begins to reduce the principal, effectively prolonging the life of the loan and the time it takes to become interest-free through repayment.

Borrowers should also consider how deferment affects their overall financial strategy. While deferment provides temporary relief from payments, it may not be the best option for those aiming to minimize long-term costs. For instance, if a borrower can afford to pay the accruing interest on an unsubsidized loan during deferment, doing so can prevent capitalization and keep the loan balance from growing. This proactive approach can help borrowers end the interest-free period sooner by maintaining control over their loan balance and avoiding unnecessary costs.

In summary, deferment impacts when the 0% interest period concludes by either preserving the interest-free status for subsidized loans or allowing interest to accrue for unsubsidized loans. Borrowers must weigh the immediate benefits of postponing payments against the potential long-term costs, especially for loans where interest continues to grow during deferment. By carefully evaluating their loan types and financial situation, borrowers can make strategic decisions that align with their goals and minimize the overall impact of deferment on their student loan obligations.

Key Factors That Disqualify You from Student Loan Interest Deduction

You may want to see also

Explore related products

![]()

COVID-19 Extensions: Temporary relief measures and their expiration timelines for student loans

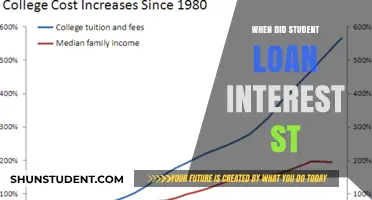

In response to the economic challenges posed by the COVID-19 pandemic, the U.S. Department of Education implemented temporary relief measures for federal student loan borrowers, including a pause on loan payments, a 0% interest rate, and a halt on collections for defaulted loans. These measures, initially introduced in March 2020 under the CARES Act, were designed to provide financial flexibility during the crisis. The 0% interest rate on federal student loans has been a critical component of this relief, effectively stopping the accrual of interest on eligible loans, which has saved borrowers billions of dollars collectively.

The expiration timeline for these relief measures has been extended multiple times since their inception. As of the latest update, the payment pause and 0% interest rate were extended through August 31, 2022, following President Biden’s announcement in April 2022. This extension was intended to provide borrowers additional time to prepare for the resumption of payments, especially as the economy continued to recover from the pandemic. It’s important for borrowers to note that this date is subject to change, as policymakers may adjust timelines based on ongoing economic conditions.

For borrowers with federally held loans, the 0% interest period will officially end on September 1, 2022, unless further extensions are announced. After this date, interest will resume accruing at the standard rates outlined in the loan agreements. Borrowers should plan accordingly by reviewing their loan balances, understanding their repayment options, and considering enrolling in income-driven repayment plans if necessary. Loan servicers are expected to communicate directly with borrowers ahead of the expiration to ensure a smooth transition.

It’s crucial to distinguish between federally held loans and private or commercially held FFEL Program loans, as the latter are not eligible for the 0% interest rate or payment pause under the COVID-19 relief measures. Borrowers with private loans should contact their lenders directly to explore available options, such as forbearance or refinancing, though these may come with different terms and conditions. Additionally, borrowers in default on federal loans have been protected from wage garnishments and tax refund seizures during the relief period, but these collections activities will resume after the expiration date.

To maximize the benefits of the remaining relief period, borrowers should take proactive steps. This includes updating contact information with loan servicers, exploring loan forgiveness programs like Public Service Loan Forgiveness (PSLF), and setting aside funds to prepare for the resumption of payments. The Department of Education has also encouraged borrowers to consider making voluntary payments during the 0% interest period to reduce their principal balance, which can lead to long-term savings. Staying informed through official channels, such as the Federal Student Aid website, is essential as the situation evolves.

Maximize Your Deduction: Understanding State Student Loan Interest Limits

You may want to see also

Explore related products

![]()

Repayment Plan Effects: Income-driven plans may alter when 0% interest ends

The temporary 0% interest rate on federal student loans, implemented during the COVID-19 pandemic, has been a significant relief for many borrowers. However, the end of this interest-free period is tied to specific conditions, and choosing an income-driven repayment (IDR) plan can complicate the timeline. Income-driven plans, which cap monthly payments based on income and family size, often extend the loan term, and this can directly impact when the 0% interest period ends. For borrowers on these plans, understanding how their repayment strategy interacts with the interest pause is crucial for financial planning.

Income-driven repayment plans recalculate monthly payments annually based on the borrower’s updated income and family size. During the 0% interest period, any payment made under these plans goes entirely toward the principal balance, reducing the overall debt. However, once the interest pause ends, the dynamics shift. For borrowers on IDR plans, the end of 0% interest may be delayed if they remain in a payment amount that is less than the accruing interest, a situation known as "negative amortization." This occurs when the monthly payment is insufficient to cover the interest, causing the loan balance to grow rather than shrink.

The specific terms of the IDR plan also play a role in determining when the 0% interest period ends. For instance, plans like Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE) have different rules regarding interest capitalization and payment calculations. Under REPAYE, for example, the government pays half of the unpaid interest on subsidized loans and all of the unpaid interest on unsubsidized loans for the first three years of repayment. This subsidy can effectively extend the benefits of the 0% interest period for some borrowers, but it depends on their payment amount and loan type.

Borrowers on income-driven plans should closely monitor their loan status and payment amounts as the end of the 0% interest period approaches. If their income increases significantly, their monthly payments may rise, potentially accelerating the timeline for when interest resumes. Conversely, if their income remains low, they may continue to benefit from the interest pause, especially if their payments do not cover the accruing interest. It’s essential to stay informed about policy updates, as changes to IDR plans or the interest pause could further alter repayment timelines.

Finally, borrowers should consider their long-term financial goals when choosing or staying on an income-driven plan. While these plans offer lower monthly payments and potential loan forgiveness after 20–25 years, they may also extend the period during which interest could accrue. For those nearing the end of the 0% interest period, evaluating whether to switch to a standard repayment plan or make extra payments to reduce the principal balance could be beneficial. Consulting with a financial advisor or loan servicer can provide personalized guidance tailored to individual circumstances.

Understanding the Real Interest Rate on Student Loans: What You Need to Know

You may want to see also

Frequently asked questions

The 0% interest period on federal student loans, implemented as part of COVID-19 relief measures, ended on August 31, 2023. Interest began accruing again on September 1, 2023.

No, the 0% interest period only applied to federal student loans. Private student loans were not included in this relief measure, and their interest rates are determined by the lender.

Yes, federal student loan payments resumed in October 2023, after the 0% interest period ended. Borrowers were notified by their loan servicers about their new payment amounts.

No, the 0% interest period has ended for federal student loans. However, some repayment plans or deferment options may offer lower interest rates or temporary relief, depending on your circumstances.