If you've noticed an increase in your private student loan interest rate, there could be several reasons behind it. One possibility is that the lender has adjusted the rate due to changes in market conditions or economic indicators, such as the prime rate. Another reason might be related to your personal creditworthiness; if your credit score has decreased, the lender may have increased your interest rate to reflect the higher risk. Additionally, some private student loans have variable interest rates that can fluctuate over time, so your rate increase could simply be a result of the loan's terms. It's also worth checking if there have been any changes to your loan agreement or if you've missed any payments, as these factors can sometimes lead to an increase in interest rates. To fully understand the reason behind your rate increase, it's best to contact your lender directly and ask for an explanation.

Explore related products

What You'll Learn

- Market Interest Rates: Changes in the federal funds rate or LIBOR can influence private student loan interest rates

- Credit Score Changes: A drop in your credit score may lead to an increase in your loan's interest rate

- Loan Terms and Conditions: Your loan agreement might include clauses that allow for interest rate adjustments under certain conditions

- Economic Factors: Inflation, economic downturns, or other financial market conditions can impact interest rates

- Lender Policies: Changes in the lender's policies or risk assessment strategies can result in higher interest rates

![]()

Market Interest Rates: Changes in the federal funds rate or LIBOR can influence private student loan interest rates

Changes in market interest rates, such as the federal funds rate or the London Interbank Offered Rate (LIBOR), can have a significant impact on private student loan interest rates. When the Federal Reserve adjusts the federal funds rate, it affects the cost of borrowing for banks and other financial institutions. These institutions, in turn, may adjust the interest rates they charge on private student loans to reflect their own increased or decreased borrowing costs. Similarly, LIBOR serves as a benchmark for many adjustable-rate loans, including some private student loans. When LIBOR increases, the interest rates on these loans typically rise as well.

To understand how these changes might affect your private student loan, it's important to know whether your loan has a fixed or variable interest rate. If you have a fixed-rate loan, your interest rate will remain the same for the life of the loan, regardless of changes in market rates. However, if you have a variable-rate loan, your interest rate may fluctuate periodically based on changes in the underlying index, such as LIBOR. This means that if market interest rates rise, your loan's interest rate could increase, leading to higher monthly payments.

One way to mitigate the impact of rising interest rates on your private student loan is to consider refinancing. If you have a variable-rate loan and anticipate that interest rates will continue to rise, you may be able to refinance into a fixed-rate loan, locking in a lower interest rate for the remainder of your repayment term. However, refinancing may not be the best option for everyone, as it can involve closing costs and may extend your repayment term. It's important to carefully consider the terms and conditions of any refinancing offer to ensure that it aligns with your financial goals.

Another strategy to manage the impact of rising interest rates is to focus on paying down your loan balance as quickly as possible. By making extra payments or increasing your monthly payment amount, you can reduce the principal balance of your loan, which will decrease the amount of interest you owe over time. This can help offset the effects of rising interest rates and save you money in the long run.

In conclusion, changes in market interest rates can have a direct impact on private student loan interest rates, particularly for variable-rate loans. By understanding how these changes work and exploring options such as refinancing or making extra payments, you can take steps to manage the impact of rising interest rates on your student loan debt.

Maximize Your Savings: Where to Find Student Loan Interest Tax Deductions

You may want to see also

Explore related products

![]()

Credit Score Changes: A drop in your credit score may lead to an increase in your loan's interest rate

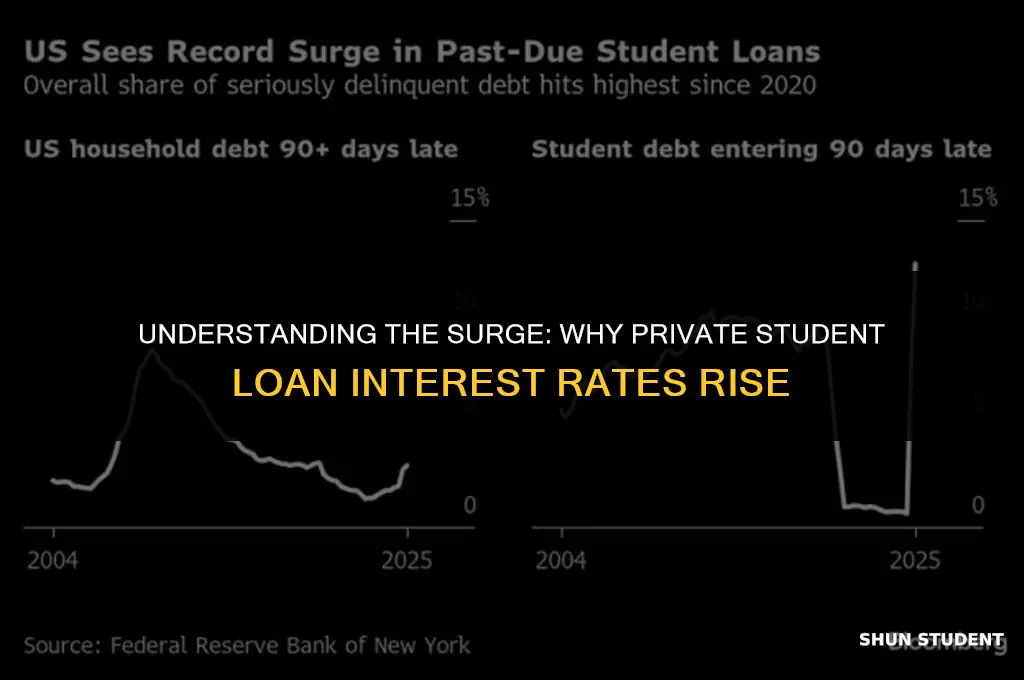

A drop in your credit score can have significant implications for your financial health, particularly when it comes to your private student loan interest rate. Lenders often use credit scores as a measure of a borrower's creditworthiness, and a lower score may indicate a higher risk of default. As a result, lenders may increase the interest rate on your loan to compensate for this perceived risk.

One of the most common reasons for a credit score drop is missed or late payments. If you've failed to make payments on time, it can negatively impact your credit utilization ratio, which is a key factor in determining your credit score. A high credit utilization ratio can signal to lenders that you're overextended and may struggle to repay your debts, leading to an increase in your loan interest rate.

Another factor that can contribute to a credit score drop is a high balance on your credit cards. Even if you're making payments on time, carrying a large balance can negatively impact your credit utilization ratio and, consequently, your credit score. Lenders may view this as a sign that you're relying too heavily on credit and may be at risk of defaulting on your loans.

To avoid a credit score drop and the subsequent increase in your private student loan interest rate, it's essential to maintain good credit habits. This includes making payments on time, keeping your credit card balances low, and monitoring your credit report regularly for any errors or discrepancies. By taking these steps, you can help ensure that your credit score remains strong and your loan interest rate stays competitive.

Missed the Cut: Understanding Student Loan Interest Deduction Eligibility

You may want to see also

Explore related products

![]()

Loan Terms and Conditions: Your loan agreement might include clauses that allow for interest rate adjustments under certain conditions

Your loan agreement is a legally binding document that outlines the terms and conditions of your loan, including the interest rate. It's crucial to understand that this rate isn't always fixed and can change under certain circumstances. One of the key clauses in your agreement might allow for interest rate adjustments based on specific conditions. These could include changes in the prime rate, your credit score, or even the loan's default status.

For instance, if your loan agreement includes a variable interest rate clause, your rate could fluctuate with the market. This means that if the prime rate increases, your loan's interest rate might also go up, leading to higher monthly payments. Similarly, if your credit score drops significantly, your lender might view you as a higher risk and increase your interest rate accordingly.

Another common clause is the default rate. If you miss a certain number of payments or fail to meet other loan obligations, your lender could increase your interest rate to a higher default rate. This is often done to compensate for the increased risk of non-repayment.

It's also important to note that some loan agreements might include a clause for periodic rate reviews. This allows the lender to adjust the interest rate at set intervals, such as annually or semi-annually, based on current market conditions or other factors outlined in the agreement.

To avoid unexpected rate hikes, it's essential to carefully review your loan agreement and understand the specific clauses related to interest rate adjustments. If you're unsure about any terms or conditions, don't hesitate to reach out to your lender for clarification. By staying informed and proactive, you can better manage your loan and avoid potential financial surprises.

Exploring the Benefits and Impact of Undergraduate Student Government Association

You may want to see also

Explore related products

![]()

Economic Factors: Inflation, economic downturns, or other financial market conditions can impact interest rates

Inflation is a key economic factor that can lead to an increase in interest rates. When the general price level of goods and services rises, the purchasing power of money decreases. To combat inflation, central banks may raise interest rates to make borrowing more expensive, thereby reducing consumer spending and slowing down economic growth. This can have a direct impact on private student loans, as lenders may adjust their interest rates in response to changes in the federal funds rate set by the central bank.

Economic downturns can also influence interest rates. During a recession, demand for goods and services decreases, leading to lower prices and reduced inflationary pressures. In response, central banks may lower interest rates to stimulate borrowing and investment, helping to revive the economy. However, this can create a challenging environment for lenders, who may need to increase their interest rates to maintain profitability and manage risk.

Other financial market conditions, such as changes in the yield curve or fluctuations in global commodity prices, can also impact interest rates. For example, if the yield curve inverts, indicating that short-term interest rates are higher than long-term rates, it may signal an impending recession. Lenders may respond by increasing their interest rates to protect against potential losses. Similarly, if global commodity prices rise, it can lead to higher inflation expectations, prompting lenders to adjust their interest rates accordingly.

In the context of private student loans, these economic factors can have a significant impact on borrowers. If interest rates increase, it can lead to higher monthly payments and increased overall borrowing costs. Borrowers may need to adjust their budgets or consider refinancing options to manage their debt more effectively. Understanding the relationship between economic factors and interest rates can help borrowers make informed decisions about their student loans and financial planning.

Meritrust Student Visa Interest Rates: What You Need to Know

You may want to see also

Explore related products

$2.99 $17.99

![]()

Lender Policies: Changes in the lender's policies or risk assessment strategies can result in higher interest rates

Lenders periodically review and adjust their policies and risk assessment strategies to adapt to changing market conditions, regulatory requirements, and internal business objectives. These changes can have a direct impact on the interest rates offered to borrowers, including those with private student loans. For instance, if a lender perceives an increase in the risk of default among student loan borrowers, they may raise interest rates to compensate for the heightened risk.

One specific scenario where this might occur is when there is a shift in the economic outlook. During times of economic uncertainty or recession, lenders may become more cautious and increase interest rates to protect themselves from potential losses. This can be particularly true for private student loans, which are not backed by the federal government and therefore carry more risk for the lender.

Another factor that can influence lender policies is changes in regulatory requirements. For example, if new laws or regulations are introduced that affect the cost of lending, such as increased capital requirements or stricter underwriting standards, lenders may pass these costs on to borrowers in the form of higher interest rates.

Additionally, lenders may adjust their policies in response to changes in their business strategy or market position. For instance, a lender that is looking to expand its market share may offer more competitive interest rates, while a lender that is seeking to reduce its risk exposure may increase rates for certain types of loans.

To mitigate the impact of these policy changes, borrowers should stay informed about market trends and regulatory developments that could affect their loan terms. They should also consider refinancing their loans if they find that their interest rates have increased significantly. By shopping around for the best rates and terms, borrowers can potentially save money and better manage their student loan debt.

When Does Student Loan Interest End: A Complete Guide

You may want to see also

Frequently asked questions

There could be several reasons for an increase in your private student loan interest rate. Some common factors include changes in market conditions, fluctuations in the prime interest rate, or adjustments based on your creditworthiness. It's essential to review your loan agreement and contact your lender to understand the specific reasons behind the rate increase.

Yes, changes in your credit score can impact your private student loan interest rate. Lenders often use credit scores to assess the risk of lending to you. If your credit score decreases, the lender may view you as a higher risk and increase your interest rate accordingly. Maintaining a good credit score is crucial to securing favorable loan terms.

Market conditions, such as inflation and economic trends, can significantly influence private student loan interest rates. Lenders may adjust rates in response to changes in the cost of borrowing or to remain competitive in the market. Economic downturns or periods of high inflation may lead to increased interest rates to mitigate the lender's risk.

The specific cap on interest rate increases for private student loans varies depending on the lender and the terms of your loan agreement. Some loans may have a fixed cap, while others may allow for variable rate changes. It's crucial to carefully review your loan contract to understand any limitations on interest rate increases.

If your private student loan interest rate has increased significantly, you may want to explore options such as refinancing your loan, consolidating your debt, or negotiating with your lender. Refinancing or consolidating may help you secure a lower interest rate, potentially saving you money over the life of the loan. Additionally, reaching out to your lender to discuss your concerns may lead to a resolution or alternative repayment plan.