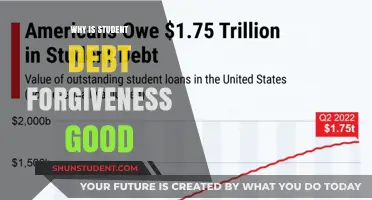

Student loan forgiveness has been a highly anticipated relief measure for millions of borrowers, yet the process has been plagued by delays, leaving many frustrated and uncertain about their financial futures. Despite legislative efforts like the Public Service Loan Forgiveness (PSLF) program and the recent one-time adjustment by the Biden administration, bureaucratic hurdles, complex eligibility requirements, and administrative inefficiencies have slowed progress. Additionally, legal challenges and political opposition have further complicated implementation, while the sheer volume of applications has overwhelmed servicing agencies. As a result, borrowers continue to face prolonged wait times, accruing interest, and mounting debt, raising questions about the government’s ability to deliver on its promises and provide meaningful relief to those in need.

| Characteristics | Values |

|---|---|

| Legislative and Legal Challenges | Ongoing lawsuits and appeals blocking implementation, particularly from Republican states and organizations. |

| Complexity of Programs | Intricate eligibility criteria and verification processes for programs like PSLF and IDR Account Adjustment. |

| Volume of Applications | Millions of borrowers applying simultaneously, overwhelming processing systems. |

| Administrative Delays | Slow rollout of updated guidelines and technical issues within the Education Department. |

| Political Opposition | Republican opposition and legal challenges arguing the program is unconstitutional or exceeds executive authority. |

| Court Injunctions | Supreme Court’s June 2023 ruling against Biden’s broad forgiveness plan, halting progress. |

| Program Redesign | Need to rework forgiveness programs post-court rulings, causing further delays. |

| Budgetary Constraints | Limited funding and resources allocated for processing applications efficiently. |

| Public Pressure | Growing borrower frustration and advocacy for faster resolution. |

| Economic Impact | Concerns about the cost of forgiveness and its long-term economic effects. |

Explore related products

![NMLS Study Cards: NMLS MLO Test Prep 2025-2026 for the SAFE Mortgage Loan Originator Exam with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61f1NUOp4iL._AC_UY218_.jpg)

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UY218_.jpg)

![NMLS Study Guide: SAFE Mortgage Loan Originator Test Prep Secrets Book, Full-Length MLO Practice Exam, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71wuD4SQlSL._AC_UY218_.jpg)

What You'll Learn

- Legislative Delays: Congressional debates and partisan gridlock slow policy implementation and final approval

- Legal Challenges: Lawsuits from opposing states and groups halt progress in courts

- Administrative Complexity: Processing millions of applications requires time and resources

- Verification Issues: Confirming eligibility and debt details slows individual case reviews

- Funding Disputes: Budget allocation debates delay program execution and disbursement

![]()

Legislative Delays: Congressional debates and partisan gridlock slow policy implementation and final approval

Congressional debates over student loan forgiveness have become a battleground for competing visions of economic fairness and fiscal responsibility. At the heart of the delay is the clash between progressive lawmakers, who argue that broad-scale debt cancellation is essential for alleviating the financial burden on millions of Americans, and conservative counterparts, who contend that such measures are an overreach of federal power and a misuse of taxpayer funds. These ideological divides are not merely abstract—they translate into tangible delays as bills stall in committee, amendments pile up, and procedural tactics like filibusters are employed to block progress. For instance, the debate over whether to cap forgiveness at $10,000 or $50,000 per borrower has repeatedly derailed negotiations, leaving millions in limbo.

Consider the legislative process itself, which is designed to be deliberate but often becomes a quagmire of partisan interests. A bill proposing student loan forgiveness must navigate multiple stages: drafting, committee review, floor debate, and reconciliation between House and Senate versions. Each step is an opportunity for gridlock. For example, the 2022 proposal to cancel up to $20,000 in student debt faced immediate challenges in the Senate, where a single dissenting voice can halt progress. The lack of a clear bipartisan consensus means that even minor disagreements can balloon into months-long stalemates, delaying relief for borrowers who are accruing interest in the meantime.

To understand the practical impact of these delays, imagine a 30-year-old borrower with $30,000 in debt at a 6% interest rate. Each month of legislative inaction adds approximately $150 in interest to their balance. Multiply that by the 12 months it takes for a bill to move through Congress, and the borrower has accrued an additional $1,800 in debt—money that could have been forgiven had the policy been implemented promptly. This example underscores how legislative delays are not just bureaucratic hurdles but real-world financial burdens for millions of Americans.

Breaking the gridlock requires strategic compromise and innovative solutions. One approach is to tie student loan forgiveness to broader economic reforms, such as workforce development programs or income-driven repayment plans, which could appeal to both sides of the aisle. Another tactic is to leverage executive action, as seen in the Biden administration’s attempts to bypass congressional stalemate through the Department of Education. However, such moves often face legal challenges, further prolonging the process. Borrowers, meanwhile, are left to navigate a patchwork of temporary fixes, like payment pauses, while awaiting permanent relief.

Ultimately, the lesson is clear: legislative delays are not just a function of disagreement but of a system ill-equipped to handle urgent, large-scale issues. Until Congress finds a way to prioritize collaboration over partisanship, student loan forgiveness will remain trapped in a cycle of debate and delay. For borrowers, this means continued uncertainty and financial strain—a stark reminder that the cost of inaction is measured not in dollars alone, but in lives and livelihoods.

Steps to Obtain Your Student Loan Forgiveness Copy Easily

You may want to see also

Explore related products

$13.95 $22

![]()

Legal Challenges: Lawsuits from opposing states and groups halt progress in courts

Legal challenges have emerged as a formidable roadblock to the swift implementation of student loan forgiveness programs, with lawsuits from opposing states and groups effectively halting progress in the courts. These legal battles center on constitutional and procedural grounds, often arguing that the executive branch overstepped its authority or that the forgiveness plans violate federal law. For instance, six Republican-led states sued the Biden administration in 2022, claiming the student loan forgiveness plan bypassed congressional approval and infringed on states’ rights by potentially harming their tax revenues and student loan servicing industries. This lawsuit, among others, led to injunctions that froze the program, preventing millions of borrowers from receiving relief.

The complexity of these cases lies in the interplay between federal authority and state sovereignty. Opponents argue that the Higher Education Relief Opportunities for Students (HEROES) Act of 2003, which the administration cited to justify forgiveness, does not grant broad debt cancellation powers. Instead, they contend it is limited to modifying loan terms during national emergencies. This legal interpretation has been a focal point in courtrooms, where judges must decide whether the executive branch acted within its statutory limits. The resulting judicial scrutiny has created a protracted timeline, as cases wind through district courts, appeals courts, and potentially the Supreme Court.

Another layer of legal challenges comes from groups representing student loan servicers and for-profit colleges, which claim financial harm from forgiveness programs. For example, the Job Creators Network Foundation argued that the forgiveness plan would reduce revenue for loan servicers and disrupt the student loan market. These lawsuits highlight the economic ripple effects of debt cancellation, framing it as an issue of fairness and unintended consequences. While these arguments may seem peripheral, they have successfully delayed implementation by raising questions about standing and the scope of administrative power.

To navigate this legal maze, borrowers must stay informed about case developments and understand their rights. Practical tips include monitoring updates from the Department of Education, retaining documentation of loan payments, and exploring alternative relief programs like income-driven repayment plans. Advocates for forgiveness can also support legislative solutions, such as passing a congressional bill to codify debt cancellation, which would bypass many legal challenges. While the courts deliberate, the takeaway is clear: legal opposition has transformed student loan forgiveness into a high-stakes battle of constitutional interpretation, with borrowers caught in the crossfire.

NJ Student Loan Forgiveness: Eligibility Criteria and Application Guide

You may want to see also

Explore related products

![]()

Administrative Complexity: Processing millions of applications requires time and resources

The sheer volume of student loan forgiveness applications is staggering, with millions of borrowers seeking relief. Each application represents a unique financial history, loan type, and eligibility criteria, making the review process akin to solving a million complex puzzles. This administrative burden is not merely about numbers; it’s about the intricate details that require meticulous verification to ensure fairness and compliance with federal regulations. For instance, income-driven repayment plans, public service loan forgiveness, and total and permanent disability discharges each have distinct requirements, adding layers of complexity to the review process.

Consider the steps involved in processing a single application: verifying employment records, calculating qualifying payments, cross-referencing loan types, and ensuring compliance with ever-evolving federal guidelines. Multiply this by millions, and the scale of the challenge becomes clear. The Department of Education’s loan servicers must navigate outdated systems, incomplete applicant data, and the need for manual reviews in many cases. For example, public service loan forgiveness applications often require manual verification of employer certifications, a process that can take weeks or even months per application. This labor-intensive work is further compounded by the need to prioritize applications based on submission date, loan type, and other factors.

To illustrate, imagine a factory tasked with assembling intricate machinery. Each piece must fit perfectly, and every step must be verified for quality. Now, imagine that factory is processing not hundreds but millions of these machines simultaneously, with no room for error. This analogy captures the essence of the administrative complexity at play. The system is not designed to handle such volume efficiently, leading to bottlenecks and delays. Borrowers, meanwhile, are left in limbo, unsure of their status or when relief might come.

Practical solutions exist, but they require significant investment in technology and personnel. Automating parts of the verification process, for instance, could reduce manual labor and speed up reviews. However, such upgrades are costly and time-consuming to implement. Another approach is to streamline eligibility criteria, reducing the need for case-by-case reviews. For example, blanket forgiveness for certain loan types or income brackets could bypass the need for individual assessments. Yet, these measures face political and logistical hurdles, leaving the system mired in inefficiency.

The takeaway is clear: administrative complexity is not just a bureaucratic excuse but a tangible barrier to timely student loan forgiveness. Borrowers must understand that the delay is not due to indifference but to the overwhelming scale and intricacy of the task. While frustration is justified, recognizing the systemic challenges can temper expectations and highlight the need for systemic reform. Until then, patience—though difficult—remains a necessary virtue.

Can Police Officers and Law Enforcement Get Student Loan Forgiveness?

You may want to see also

Explore related products

$9.99 $12.99

$14.95 $14.95

![]()

Verification Issues: Confirming eligibility and debt details slows individual case reviews

One of the primary bottlenecks in the student loan forgiveness process is the meticulous verification of eligibility and debt details. Each application requires cross-referencing multiple data points, including loan types, repayment plans, employment history, and income levels. This process, while necessary to prevent fraud and ensure compliance, is inherently time-consuming. For instance, the Public Service Loan Forgiveness (PSLF) program alone demands proof of 120 qualifying payments and employer certification, a task that can take months to validate. The sheer volume of applications exacerbates the delay, as each case must be reviewed individually, leaving borrowers in limbo.

Consider the steps involved in verifying eligibility: first, the borrower submits their application, which is then matched against federal databases to confirm loan types and repayment history. Next, employment records are scrutinized to ensure the borrower meets public service criteria. Finally, payment histories are audited to verify the number of qualifying payments. Any discrepancies—such as missing documentation or mismatched records—halt the process, requiring additional back-and-forth between the borrower and the servicer. This multi-step verification is not just bureaucratic red tape; it’s a critical safeguard against misuse of taxpayer funds. However, the complexity of these checks inevitably slows down approvals.

To illustrate, imagine a borrower who has made 110 qualifying payments but is missing records for the remaining 10. Without complete documentation, their application cannot proceed. Similarly, a borrower whose employer certification form contains errors must resubmit the form, adding weeks to the review timeline. These examples highlight the fragility of the verification process—a single missing detail can derail an application. While borrowers are often advised to keep meticulous records, the reality is that many lack access to historical payment data or struggle to navigate the certification process, further complicating matters.

The takeaway here is that while verification issues are a necessary part of the student loan forgiveness process, they are also a significant source of delay. Borrowers can expedite their cases by proactively gathering all required documents, including payment histories, employment certifications, and loan statements, before submitting their applications. Additionally, staying in regular contact with loan servicers to confirm receipt of documents and address any issues early can help mitigate delays. Policymakers, meanwhile, could explore streamlining verification processes, such as integrating automated checks or creating a centralized database for employment certification, to reduce the burden on both borrowers and reviewers. Until such improvements are made, verification will remain a critical—and time-consuming—step in the path to loan forgiveness.

Understanding the Timeline for Consolidating Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Funding Disputes: Budget allocation debates delay program execution and disbursement

The tug-of-war over federal budgets has become a central roadblock in the execution of student loan forgiveness programs. At the heart of the issue is the sheer scale of funding required—estimates suggest forgiving $10,000 per borrower could cost upwards of $377 billion, while broader proposals soar into the trillions. When Congress debates where to allocate such massive sums, student loan forgiveness often competes with other urgent priorities like healthcare, infrastructure, and defense. This zero-sum game forces lawmakers to weigh immediate relief for borrowers against long-term fiscal sustainability, creating a gridlock that stalls progress.

Consider the mechanics of budget allocation: the Congressional Budget Office (CBO) must score the cost of forgiveness programs, projecting their impact on the federal deficit. Critics argue these scores overestimate costs by assuming all loans would be forgiven, even though many borrowers may not qualify or apply. This inflated perception of expense fuels opposition, particularly from fiscal conservatives who view forgiveness as a misallocation of taxpayer funds. Meanwhile, proponents counter that the economic benefits—such as increased consumer spending and reduced defaults—justify the investment. The result? A stalemate where ideological divides overshadow practical solutions.

Practical tips for navigating this impasse include advocating for phased implementation. Instead of a one-time, trillion-dollar payout, policymakers could structure forgiveness in tranches tied to specific milestones, such as years in public service or income-driven repayment plans. This approach would spread costs over time, easing budgetary concerns while delivering incremental relief to borrowers. Additionally, exploring alternative funding mechanisms, like redirecting subsidies from loan servicers or imposing a financial transactions tax, could alleviate the burden on general funds.

A comparative analysis reveals that countries like Germany and Norway manage student debt through tuition-free education and low-interest loans, avoiding the need for mass forgiveness. While the U.S. system differs structurally, these examples underscore the importance of addressing root causes—skyrocketing tuition and predatory lending practices—rather than relying solely on forgiveness. Until such reforms materialize, budget allocation debates will remain a critical bottleneck, leaving borrowers in limbo as politicians wrangle over dollars and cents.

Student Loan Forgiveness Canceled: What Borrowers Need to Know Now

You may want to see also

Frequently asked questions

Student loan forgiveness is taking longer than expected due to high application volumes, complex eligibility requirements, and administrative challenges within the Department of Education and loan servicers.

Delays in the PSLF program are often due to issues with employer certification, incorrect payment counts, and the need for manual reviews to ensure compliance with program rules.

Legal challenges, such as lawsuits against forgiveness programs, have led to temporary halts or delays in implementation, as courts review the legality and scope of the programs.

Some borrowers are still waiting due to ongoing policy adjustments, technical issues with loan servicers, and the need to verify eligibility for specific forgiveness programs like the one-time adjustment or income-driven repayment plans.