Student debt forgiveness is a critical policy measure that addresses the growing financial burden faced by millions of individuals, particularly in countries like the United States, where educational costs have skyrocketed. By alleviating or eliminating student loan debt, forgiveness programs can significantly improve economic mobility, reduce financial stress, and empower borrowers to invest in their futures, such as buying homes, starting businesses, or saving for retirement. Additionally, it stimulates the broader economy by increasing consumer spending and reducing default rates, while also promoting equity by disproportionately benefiting low-income and minority communities who are often saddled with disproportionate debt. Ultimately, student debt forgiveness is not just a financial relief but a transformative tool for fostering social and economic justice.

Explore related products

What You'll Learn

- Economic Stimulus: Forgiveness boosts spending, stimulates economy, and creates jobs

- Reduced Inequality: Eases wealth gaps, especially for low-income and minority graduates

- Mental Health: Relieves stress, anxiety, and depression linked to debt burdens

- Career Flexibility: Encourages public service, entrepreneurship, and nonprofit work without debt constraints

- Homeownership & Savings: Enables savings, investments, and major life milestones like buying homes

![]()

Economic Stimulus: Forgiveness boosts spending, stimulates economy, and creates jobs

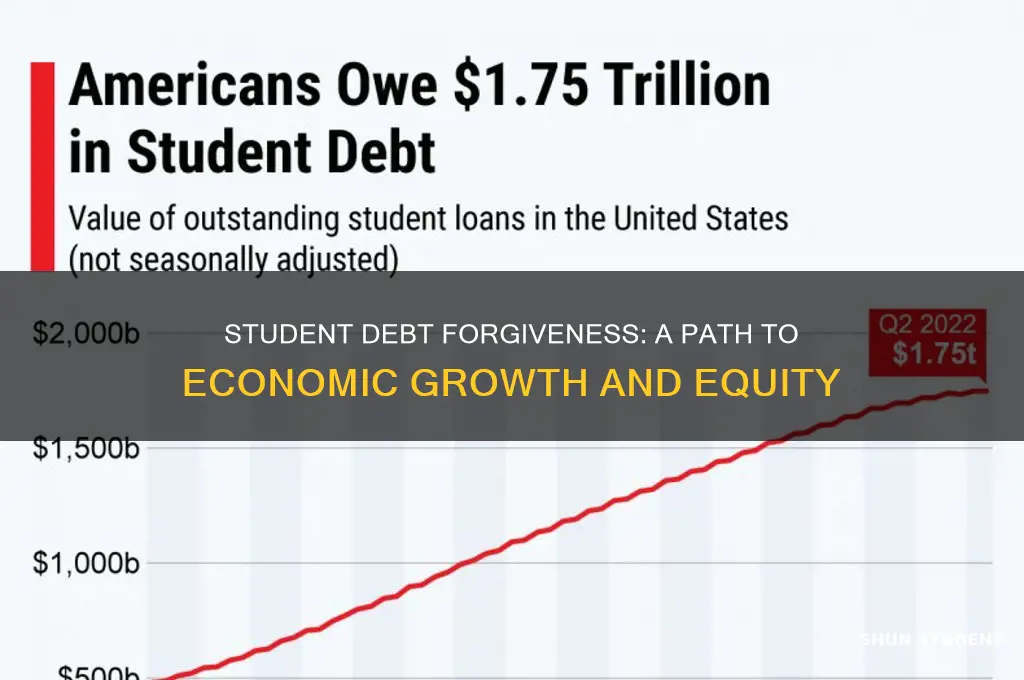

Student debt forgiveness isn’t just a financial reprieve for borrowers—it’s a powerful tool for economic revitalization. When individuals are freed from the burden of monthly loan payments, they gain disposable income that can be redirected into the economy. This isn’t theoretical; it’s backed by data. A 2021 study by the Roosevelt Institute found that canceling $1.3 trillion in student debt could boost GDP by $86 billion to $108 billion annually over the next decade. This influx of spending doesn’t just benefit borrowers—it creates a ripple effect, stimulating industries from retail to housing and beyond.

Consider the mechanics: a borrower with an extra $200 to $300 per month (the average student loan payment) might spend it on essentials like groceries, rent, or healthcare. But they’re also more likely to invest in discretionary purchases, such as dining out, travel, or home improvements. These actions inject cash into local businesses, which in turn hire more employees to meet demand. For example, a restaurant experiencing a 10% increase in customers due to increased consumer spending might need to hire additional staff, directly linking debt forgiveness to job creation.

Critics often argue that debt forgiveness is a one-time fix, but its economic benefits are sustained. When borrowers spend more, tax revenues rise, providing governments with additional funds to invest in infrastructure, education, and social programs. This creates a virtuous cycle: more jobs, higher wages, and increased economic activity. For instance, a 2020 Levy Economics Institute report estimated that canceling student debt could generate 1.5 million new jobs annually over the next decade. This isn’t just about alleviating individual hardship—it’s about building a more resilient economy.

To maximize the stimulus effect, policymakers should pair debt forgiveness with targeted measures. For example, capping forgiveness at a certain income level ensures that the benefits go to those most likely to spend the extra funds immediately. Additionally, coupling forgiveness with investments in affordable education can prevent future debt crises while sustaining long-term economic growth. The key is to view forgiveness not as an expense but as an investment in a healthier, more dynamic economy.

In practical terms, here’s how it works: if 10 million borrowers receive $10,000 in debt relief, that’s $100 billion injected into the economy. Even if only half is spent within the first year, that’s still $50 billion in new economic activity. Businesses respond by expanding operations, hiring more workers, and increasing production. The result? A stronger job market, higher consumer confidence, and a more stable financial system. Student debt forgiveness isn’t just good for borrowers—it’s a strategic move to supercharge the economy.

Dependent Students and Loan Forgiveness: Eligibility and Key Considerations

You may want to see also

Explore related products

$29.99

![]()

Reduced Inequality: Eases wealth gaps, especially for low-income and minority graduates

Student debt disproportionately burdens low-income and minority graduates, exacerbating existing wealth gaps. For these groups, education is often the sole pathway to upward mobility, yet the weight of debt stifles their ability to build financial stability. Forgiveness programs directly address this disparity by removing a significant barrier to wealth accumulation, allowing these graduates to invest in homes, start businesses, or save for the future—opportunities typically reserved for their higher-income peers.

Consider the numbers: Black college graduates, for instance, owe an average of $25,000 more in student debt than their white counterparts just four years after graduation. This disparity widens over time, as Black borrowers are more likely to default or struggle with repayment due to systemic inequalities in income and employment. Debt forgiveness isn’t just a financial reprieve; it’s a corrective measure against systemic racism and classism embedded in the education financing system. By targeting relief for these groups, forgiveness programs can begin to level the playing field.

To maximize the impact of debt forgiveness on inequality, policymakers should adopt a tiered approach. For example, forgiving $10,000 for all borrowers but increasing that amount to $20,000 or more for those from households earning below the median income could disproportionately benefit low-income and minority graduates. Additionally, pairing forgiveness with income-driven repayment plans or public service loan forgiveness programs can ensure long-term financial stability for these populations. Practical steps like these transform forgiveness from a one-time benefit into a foundation for sustained economic growth.

Critics argue that broad forgiveness programs may disproportionately benefit higher-earning graduates, but this overlooks the compounding effects of debt on marginalized communities. For a low-income graduate earning $40,000 annually, even a $10,000 reduction in debt can free up hundreds of dollars monthly—funds that could be redirected toward rent, groceries, or emergency savings. This isn’t just about fairness; it’s about creating a society where education truly serves as a great equalizer, not a debt trap.

Student Loan Forgiveness: A Step-by-Step Guide to Applying via Nelnet

You may want to see also

Explore related products

![]()

Mental Health: Relieves stress, anxiety, and depression linked to debt burdens

The weight of student debt can crush more than just a graduate's bank account; it can suffocate their mental well-being. Studies consistently show a strong correlation between student loan debt and increased levels of stress, anxiety, and depression. A 2018 survey by the American Psychological Association found that 45% of millennials with student loans reported feeling overwhelmed by their debt, compared to 28% of millennials without student loans. This financial burden often translates into sleepless nights, constant worry, and a sense of hopelessness about the future.

Debt forgiveness offers a lifeline, not just financially, but mentally.

Imagine carrying a heavy backpack filled with bricks, representing your student loans. Every step feels labored, every decision weighed down by the burden. Now, imagine that backpack suddenly lightened. The relief would be immediate and profound. Debt forgiveness provides this kind of psychological release, allowing individuals to breathe easier, think clearer, and focus on building a life beyond mere survival.

Research suggests that debt forgiveness can lead to significant improvements in mental health outcomes. A study published in the Journal of Consumer Affairs found that individuals who received debt relief experienced reductions in symptoms of depression and anxiety, along with increased feelings of financial security and overall well-being.

This isn't just about abstract feelings; it's about tangible improvements in daily life. Reduced stress levels can lead to better sleep, improved concentration, and a stronger immune system. Lower anxiety can foster healthier relationships, increased productivity at work, and a greater capacity for joy. Debt forgiveness, in essence, becomes a form of preventative mental health care, addressing a root cause of widespread distress.

Step-by-Step Guide to Submitting Your Student Loan Forgiveness Application

You may want to see also

Explore related products

![]()

Career Flexibility: Encourages public service, entrepreneurship, and nonprofit work without debt constraints

Student debt forgiveness liberates individuals from the financial shackles that often dictate career choices. Burdened by hefty loan repayments, many graduates feel compelled to pursue high-paying corporate jobs, even if their passions lie elsewhere. This phenomenon, known as "job-locking," stifles career flexibility and limits the talent pool in sectors like public service, entrepreneurship, and nonprofit work. By eliminating or reducing student debt, individuals gain the freedom to choose careers aligned with their values and interests, rather than being forced into roles solely for financial stability.

Consider the aspiring social worker who dreams of supporting underserved communities but feels trapped in a lucrative finance job to pay off $100,000 in student loans. Debt forgiveness could empower this individual to transition into a lower-paying but deeply fulfilling role, knowing their financial burden is alleviated. Similarly, an entrepreneur with a vision for a sustainable startup might hesitate to take the leap due to the risk of failure and the weight of debt. Without this constraint, they could pursue innovation, potentially creating jobs and contributing to economic growth.

The ripple effects of career flexibility extend beyond individual fulfillment. Public service sectors, such as education and healthcare, often struggle to attract and retain talent due to lower salaries. Debt forgiveness could incentivize more graduates to enter these fields, addressing critical workforce shortages. Nonprofit organizations, which rely on passionate individuals to drive social change, could also benefit from an influx of debt-free talent. This shift would strengthen the social fabric by ensuring these vital sectors are staffed with dedicated professionals.

However, implementing debt forgiveness requires careful consideration. Policymakers must balance the benefits of career flexibility with the need for fiscal responsibility. Targeted forgiveness programs, such as those tied to public service commitments or income-driven repayment plans, could maximize impact while minimizing costs. Additionally, pairing forgiveness with financial literacy initiatives could help recipients make informed career choices and avoid future debt traps.

In conclusion, student debt forgiveness is a powerful tool for unlocking career flexibility and fostering a more dynamic workforce. By removing financial barriers, it empowers individuals to pursue public service, entrepreneurship, and nonprofit work, ultimately driving societal progress. While challenges exist, thoughtful implementation can ensure that debt forgiveness not only benefits individuals but also strengthens the communities they serve.

Sallie Mae Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Homeownership & Savings: Enables savings, investments, and major life milestones like buying homes

Student debt forgiveness can significantly reshape the financial trajectories of millions, particularly when it comes to homeownership and savings. For many, the burden of student loans delays or outright eliminates the possibility of saving for a down payment on a home. According to the National Association of Realtors, 45% of first-time homebuyers report that student debt has hindered their ability to purchase a home. By forgiving this debt, individuals can redirect funds previously allocated to loan payments toward savings accounts or investment portfolios, accelerating their path to homeownership. This shift not only stabilizes personal finances but also stimulates the housing market, creating a ripple effect of economic benefits.

Consider the practical implications: a 30-year-old earning $60,000 annually with $30,000 in student debt at a 6% interest rate pays approximately $333 monthly. With forgiveness, this individual could instead save that $333 monthly. Over five years, assuming a modest 4% annual return on savings, they would accumulate over $21,000—a substantial portion of a typical 20% down payment on a $200,000 home. This example underscores how debt forgiveness transforms monthly obligations into opportunities for wealth-building, enabling individuals to achieve milestones that were previously out of reach.

Beyond homeownership, the ability to save and invest opens doors to other major life goals. For instance, freed from student debt, individuals can allocate funds to retirement accounts, emergency savings, or even starting a business. A study by the Levy Economics Institute found that student debt forgiveness could increase annual GDP by tens of billions of dollars, as borrowers spend more on goods, services, and investments. This economic boost is not just theoretical—it’s a tangible outcome of empowering individuals to save and invest rather than service debt.

However, achieving these benefits requires strategic planning. For those newly relieved of student debt, financial advisors recommend prioritizing high-interest savings accounts, contributing to employer-matched retirement plans, and exploring low-risk investment options like index funds. Additionally, leveraging first-time homebuyer programs or down payment assistance can further expedite homeownership. The key is to view debt forgiveness not as a windfall but as a tool for long-term financial security.

In conclusion, student debt forgiveness is a catalyst for homeownership and savings, enabling individuals to redirect funds toward meaningful investments in their future. By eliminating this financial burden, borrowers can save systematically, invest wisely, and achieve milestones that lay the foundation for generational wealth. The impact extends beyond personal finances, contributing to a more robust economy and equitable society. For those freed from student debt, the path to homeownership and financial stability is no longer a distant dream but an attainable reality.

Unlocking Student Loan Forgiveness: Weekly Work Hours Explained

You may want to see also

Frequently asked questions

Student debt forgiveness can stimulate the economy by freeing up disposable income for borrowers, allowing them to spend more on goods, services, and investments, which in turn boosts economic growth.

It alleviates financial stress, improves credit scores, and enables individuals to pursue major life milestones like buying a home, starting a family, or saving for retirement without the burden of debt.

Student debt disproportionately affects low-income and minority communities, perpetuating economic inequality. Forgiveness helps address systemic disparities and provides opportunities for marginalized groups to achieve financial stability.

By reducing the debt burden on current borrowers, it sets a precedent for reforming higher education financing, making college more accessible and affordable for future students and reducing reliance on loans.