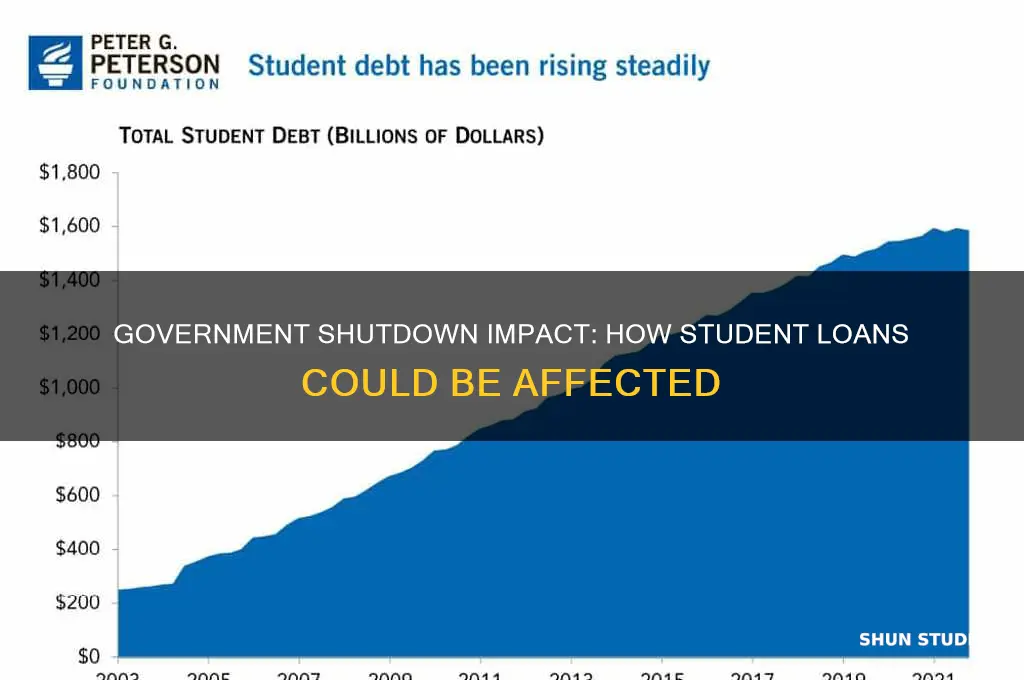

A government shutdown occurs when Congress fails to pass funding legislation, leading to the suspension of non-essential federal services. During such an event, many federal agencies and programs face disruptions, raising concerns about the impact on various sectors, including education. One pressing question for students and borrowers is whether a government shutdown will affect student loans. Typically, essential functions related to student loans, such as loan disbursements and customer service, may continue through agencies like the Department of Education, as they are often funded through mandatory spending. However, processing delays, reduced staffing, and limited access to resources could still occur, potentially causing inconvenience for borrowers. Additionally, long-term shutdowns might disrupt legislative or regulatory actions related to student loan policies, leaving borrowers in limbo regarding potential changes or relief measures. Understanding the specific implications requires monitoring official updates from relevant agencies during the shutdown period.

| Characteristics | Values |

|---|---|

| Direct Impact on Loan Disbursement | During a government shutdown, the Department of Education may continue to process and disburse federal student loans, as these are considered mandatory spending. However, delays or disruptions are possible if specific offices or personnel are furloughed. |

| Loan Servicing and Repayment | Federal student loan servicing (e.g., payments, forbearance requests) may experience delays or reduced support, as loan servicers could face limited access to government systems or guidance. |

| Income-Driven Repayment (IDR) Plans | Processing of IDR applications or recertifications might slow down, potentially affecting borrowers' ability to adjust their payments promptly. |

| Public Service Loan Forgiveness (PSLF) | Certification and processing for PSLF could face delays, impacting borrowers working toward loan forgiveness. |

| Federal Student Aid (FAFSA) | The FAFSA website and processing may remain operational, but customer service support (e.g., call centers, help desks) could be limited or unavailable. |

| Default Resolution and Collections | Activities related to defaulted loans, such as rehabilitation or wage garnishments, may be paused or delayed during a shutdown. |

| Impact on Private Student Loans | Private student loans are generally unaffected by a government shutdown, as they are not tied to federal operations. |

| Long-Term Effects | Prolonged shutdowns could lead to backlogs in loan processing, repayment adjustments, and customer service inquiries, causing frustration for borrowers. |

| Historical Precedent | Past government shutdowns (e.g., 2013, 2018-2019) have shown minimal direct impact on student loan operations, but disruptions in customer service and administrative functions were noted. |

| Current Status (as of latest data) | As of the latest updates, federal student loan operations are expected to continue, but borrowers should monitor official announcements for any changes. |

Explore related products

What You'll Learn

- Loan Processing Delays: Shutdown may halt federal loan applications, causing delays for new borrowers

- Repayment Assistance: Services like income-driven plans could face disruptions during a shutdown

- Default Prevention: Limited support for borrowers at risk of defaulting on loans

- Customer Service Impact: Reduced staff may lead to longer wait times for inquiries

- Federal Aid Disbursement: Shutdown could delay financial aid payouts to students

![]()

Loan Processing Delays: Shutdown may halt federal loan applications, causing delays for new borrowers

A government shutdown can throw a wrench into the gears of federal student loan processing, leaving new borrowers in limbo. During a shutdown, the Department of Education, which oversees federal student aid programs, may furlough employees or operate with a skeleton crew. This reduction in staffing can bring loan application processing to a near standstill. For students relying on federal loans to cover tuition, housing, and other expenses, this delay can be more than an inconvenience—it can disrupt their entire academic and financial plan.

Consider the timeline: typically, federal student loan applications are processed within 2-4 weeks during normal operations. However, during a shutdown, this timeline can stretch indefinitely. For instance, during the 2018-2019 shutdown, the longest in U.S. history, many applicants reported delays of 6-8 weeks or more. For students starting a new semester, this delay can mean missing payment deadlines, risking enrollment holds, or even having to defer their education altogether. It’s not just about waiting longer—it’s about the cascading consequences of that wait.

To mitigate these delays, proactive steps are crucial. First, submit your Free Application for Federal Student Aid (FAFSA) as early as possible—ideally, as soon as it opens on October 1st. This ensures your application is in the queue before any potential shutdown. Second, monitor your application status closely. If a shutdown occurs, contact your school’s financial aid office for updates and alternative options, such as emergency loans or payment plans. Third, consider having a backup plan, like private loans or savings, though these should be last resorts due to higher interest rates and less flexible terms.

The impact of these delays isn’t just financial—it’s emotional and logistical. Imagine being a first-generation college student, navigating the complexities of higher education, only to have your funding held up by political gridlock. Or a parent returning to school, juggling work and family, now facing the added stress of uncertain finances. These delays can erode trust in federal aid programs and deter students from pursuing education altogether. For policymakers, this underscores the need for contingency plans to protect students during shutdowns, such as automated processing systems or emergency funding mechanisms.

In conclusion, while a government shutdown affects many areas of life, its impact on federal student loan processing is particularly acute for new borrowers. By understanding the potential delays and taking proactive steps, students can better navigate this challenge. However, the ultimate solution lies in systemic changes that prioritize the continuity of essential services like education funding, ensuring that students’ futures aren’t held hostage to political stalemates.

Supreme Court's Role in Student Loan Forgiveness: A Likely Outcome?

You may want to see also

Explore related products

![]()

Repayment Assistance: Services like income-driven plans could face disruptions during a shutdown

During a government shutdown, borrowers relying on income-driven repayment (IDR) plans could face unexpected hurdles. These plans, which tie monthly payments to income and family size, require annual recertification of financial details. Without operational staff, processing delays or rejections might occur, potentially pushing borrowers into higher payment tiers or even default. For instance, a borrower earning $40,000 annually with $50,000 in debt might see payments jump from $150 to $500 monthly if recertification fails.

To mitigate risks, borrowers should proactively gather and submit recertification documents 60–90 days before their deadline, even if a shutdown looms. Use the Federal Student Aid website to access forms and track submission status. Keep copies of all correspondence and consider setting aside funds to cover potential payment gaps. For example, if your current payment is $200, saving $600 (three months’ worth) provides a buffer during processing delays.

A shutdown could also disrupt access to loan servicers, who handle IDR applications and adjustments. During the 2018–2019 shutdown, servicer call centers operated at reduced capacity, leaving borrowers in limbo. To avoid this, familiarize yourself with online account management tools and automated services. For instance, Navient and MOHELA offer online recertification portals that may remain functional even if phone lines are down.

Finally, borrowers nearing forgiveness under IDR plans—such as those 20–25 years into repayment—should verify their qualifying payment counts before a shutdown. Errors in tracking could delay forgiveness, especially if staff are unavailable to correct records. Request a payment history statement now and cross-reference it with your own records. If discrepancies exist, submit a dispute form immediately to ensure progress isn’t lost during operational disruptions.

In summary, while income-driven plans offer flexibility, their reliance on government processing makes them vulnerable during shutdowns. Borrowers can safeguard their financial stability by acting early, leveraging digital tools, and maintaining thorough documentation. Preparation today prevents payment shocks tomorrow.

Is Student Loan Debt Forgiveness a Worthwhile Financial Solution?

You may want to see also

Explore related products

![]()

Default Prevention: Limited support for borrowers at risk of defaulting on loans

A government shutdown can exacerbate the challenges faced by student loan borrowers, particularly those already at risk of default. During such periods, federal agencies like the Department of Education may operate with reduced staff or halt non-essential services, limiting the support available to borrowers. This includes delays in processing loan applications, repayment plan adjustments, and responses to inquiries, which can push vulnerable borrowers closer to default. For instance, borrowers seeking to enroll in income-driven repayment plans or apply for forbearance may face extended wait times, leaving them without immediate relief.

Consider the case of a borrower earning below the poverty line who relies on an income-driven repayment plan to keep monthly payments manageable. During a shutdown, delays in processing their application could result in payments defaulting to a higher standard amount, causing financial strain. Similarly, borrowers in deferment or forbearance may encounter difficulties renewing their status, risking accidental default. These scenarios highlight the urgent need for proactive measures to protect at-risk borrowers during government disruptions.

To mitigate default risks during a shutdown, borrowers should take preemptive steps. First, ensure all repayment plans and deferment requests are submitted well in advance, as processing times may double or triple. Second, maintain detailed records of all communications with loan servicers, including dates and representative names, to resolve potential disputes later. Third, explore alternative resources, such as nonprofit credit counseling agencies, which often continue operating during shutdowns and can provide guidance on budgeting and repayment strategies.

Despite these individual actions, systemic gaps remain. The federal government could implement contingency plans, such as automatic extensions for expiring deferments or forbearances during shutdowns, to reduce default risks. Additionally, loan servicers could be required to prioritize communications with borrowers flagged as high-risk for default. Without such measures, the burden falls disproportionately on borrowers, who may lack the financial cushion to absorb unexpected payment increases or administrative delays.

In conclusion, while borrowers can take steps to minimize default risks during a government shutdown, the onus should not rest solely on them. Policymakers and loan servicers must address the structural vulnerabilities that leave at-risk borrowers exposed during federal disruptions. Until then, proactive planning and resourcefulness remain the best defense for those navigating the precarious intersection of student debt and political instability.

Tech Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

![]()

Customer Service Impact: Reduced staff may lead to longer wait times for inquiries

During a government shutdown, the reduction in staff at federal agencies can significantly disrupt the customer service experience for student loan borrowers. With fewer representatives available to handle inquiries, wait times for phone calls, emails, and online chats are likely to increase. For instance, during the 2018-2019 shutdown, borrowers reported hold times exceeding 30 minutes for simple account questions, a stark contrast to the average 5-10 minutes pre-shutdown. This delay can be particularly frustrating for those seeking urgent assistance with payment processing, loan consolidation, or forbearance requests.

The impact of longer wait times extends beyond mere inconvenience. Borrowers facing financial hardship or confusion about their repayment options may find themselves in a precarious position if they cannot reach a representative promptly. For example, a borrower nearing the end of their grace period might struggle to enroll in an income-driven repayment plan, potentially leading to missed payments and accruing interest. Similarly, students awaiting disbursement of their loans could face delays in receiving funds, jeopardizing their ability to cover tuition or living expenses.

To mitigate these challenges, borrowers should proactively explore self-service options available on federal student loan websites. Many common tasks, such as updating contact information, checking loan balances, and applying for deferment, can be completed online without direct assistance. Additionally, borrowers can leverage third-party resources, such as nonprofit credit counseling agencies, which often provide free guidance on student loan management during periods of reduced government support.

While these alternatives can help alleviate some of the burden, they are not a complete solution. Complex issues, such as resolving discrepancies in loan accounts or navigating public service loan forgiveness, often require direct interaction with a knowledgeable representative. In these cases, borrowers may need to exercise patience and persistence, scheduling callbacks or follow-up appointments to ensure their concerns are addressed. Ultimately, the reduced staff during a government shutdown underscores the importance of staying informed and prepared, as even temporary disruptions can have lasting consequences for student loan borrowers.

Unlock Debt-Free Future: Strategies for Student Loan Forgiveness Explained

You may want to see also

![]()

Federal Aid Disbursement: Shutdown could delay financial aid payouts to students

A government shutdown can throw a wrench into the gears of federal aid disbursement, potentially delaying financial aid payouts to students. This disruption occurs because the Department of Education, responsible for processing and distributing federal student aid, operates on funds allocated by Congress. During a shutdown, non-essential government functions, including many within the Department of Education, may be suspended or significantly slowed.

As a result, students relying on federal grants, loans, or work-study programs might face unexpected financial strain.

Consider a hypothetical scenario: Sarah, a sophomore at a public university, depends on a Pell Grant and federal student loans to cover tuition and living expenses. Her aid is typically disbursed at the start of each semester. However, if a shutdown occurs during this critical period, the processing of her aid could be delayed. This delay could force Sarah to scramble for alternative funding, potentially jeopardizing her ability to remain enrolled.

While some essential Department of Education staff may remain on duty during a shutdown, their capacity to process aid applications and disburse funds is significantly reduced. This bottleneck can lead to a backlog of applications, further prolonging the wait time for students in need.

It's crucial for students to proactively prepare for the possibility of a shutdown. This includes closely monitoring news updates regarding government funding and contacting their university's financial aid office for guidance. Some institutions may offer emergency loans or temporary assistance to bridge the gap until federal aid is disbursed. Additionally, students should explore alternative funding sources, such as private scholarships or part-time employment, to mitigate the impact of potential delays.

Sanford Brown Closure: Steps to Qualify for Student Loan Forgiveness

You may want to see also

Frequently asked questions

Yes, a government shutdown may delay the processing of new student loan applications, as federal employees responsible for handling these applications could be furloughed or have limited capacity to work.

In most cases, scheduled student loan disbursements should continue as usual during a government shutdown, as these payments are typically automated and not immediately impacted by the shutdown.

Yes, you can still submit the FAFSA during a government shutdown, as the application process is primarily online and automated. However, processing delays may occur if federal staff are unavailable.

Existing student loan forgiveness programs and repayment plans should continue to function during a government shutdown, but customer service and support may be limited due to reduced staffing.