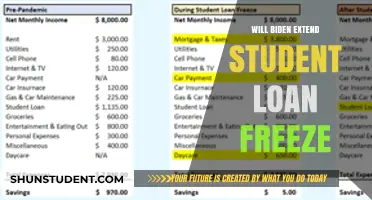

The question of whether President Joe Biden will cancel student debt has been a highly debated and closely watched issue since his presidential campaign. Biden has expressed support for some form of student debt relief, including proposals to forgive up to $10,000 in federal student loans per borrower, particularly for those with lower incomes. However, the specifics of such a plan, including eligibility criteria and the overall cost, remain uncertain. Advocates argue that canceling student debt would provide significant financial relief to millions of Americans burdened by educational loans, while critics raise concerns about the fairness and economic implications of such a move. As of now, the Biden administration continues to review its options, with no definitive decision announced, leaving borrowers and policymakers alike awaiting further developments.

| Characteristics | Values |

|---|---|

| Current Status | As of October 2023, President Biden has not implemented a blanket cancellation of all student debt. |

| Actions Taken | Biden has approved targeted student debt cancellation for specific groups:

|

| Total Debt Cancelled | Over $127 billion in student debt has been cancelled for over 3.6 million borrowers (as of October 2023). |

| Legal Challenges | Biden's broad student debt cancellation plan (up to $20,000 per borrower) was blocked by the Supreme Court in June 2023. |

| Future Plans | Biden administration continues to explore other avenues for student debt relief, including income-driven repayment plan reforms and fixing the PSLF program. |

| Political Debate | Student debt cancellation remains a highly debated issue, with supporters arguing it provides economic relief and critics expressing concerns about fairness and cost. |

Explore related products

$14.99 $14.99

What You'll Learn

- Biden's Campaign Promises: Reviewing Biden's stance on student debt cancellation during his presidential campaign

- Current Policy Actions: Analyzing recent executive orders or legislation related to student loan forgiveness

- Economic Impact: Assessing how canceling student debt could affect the U.S. economy

- Public Opinion: Exploring voter and demographic support for or against debt cancellation

- Legal Challenges: Examining potential legal obstacles to implementing widespread student loan forgiveness

![]()

Biden's Campaign Promises: Reviewing Biden's stance on student debt cancellation during his presidential campaign

During his 2020 presidential campaign, Joe Biden made several promises regarding student debt cancellation, positioning himself as an advocate for borrowers burdened by educational loans. One of his most notable commitments was to forgive a minimum of $10,000 in federal student debt per borrower, a proposal that resonated with millions of Americans struggling under the weight of escalating tuition costs and accruing interest. This pledge was part of a broader strategy to address the $1.7 trillion student debt crisis, which has stifled economic mobility for many young adults and families. Biden’s campaign also emphasized the need for targeted relief, particularly for low-income borrowers and those who attended predatory for-profit institutions, signaling a shift from blanket forgiveness to a more nuanced approach.

To understand Biden’s stance, it’s crucial to examine the context in which these promises were made. During the campaign, Biden faced pressure from progressive lawmakers like Senators Elizabeth Warren and Bernie Sanders, who advocated for more expansive forgiveness of $50,000 or more per borrower. Biden’s $10,000 proposal was seen as a compromise, balancing fiscal responsibility with the urgent need for relief. Additionally, his campaign highlighted the importance of using executive action to implement debt cancellation, a strategy that would bypass potential congressional gridlock. This approach was particularly appealing to voters who had grown frustrated with legislative inaction on student debt reform.

Since taking office, Biden’s actions on student debt cancellation have been incremental but significant. In August 2022, his administration announced the cancellation of up to $20,000 in federal student debt for Pell Grant recipients and up to $10,000 for other eligible borrowers, surpassing his initial campaign promise. This move, which was framed as a response to the economic hardships exacerbated by the COVID-19 pandemic, was met with both praise and criticism. Supporters hailed it as a transformative step toward financial relief, while opponents raised concerns about its legality and long-term economic implications. The Supreme Court’s subsequent decision to strike down the plan in June 2023 further complicated Biden’s ability to deliver on his campaign promises, forcing his administration to explore alternative pathways to debt relief.

Despite these challenges, Biden has continued to emphasize his commitment to addressing student debt through other means. His administration has expanded income-driven repayment plans, making it easier for borrowers to manage their monthly payments, and has discharged billions of dollars in debt for defrauded students and those with permanent disabilities. These actions, while not direct cancellations, align with his campaign’s focus on targeted relief and systemic reform. However, the gap between Biden’s initial promises and the realities of implementation underscores the complexities of governing in a polarized political landscape.

For borrowers seeking clarity on whether Biden will cancel student debt, the takeaway is twofold: first, while broad-scale forgiveness remains uncertain, targeted relief efforts are ongoing and expanding. Second, staying informed about policy updates and exploring available repayment options is essential. Biden’s campaign promises were ambitious, but their fulfillment depends on navigating legal, political, and economic hurdles. As the debate over student debt continues, borrowers must remain proactive in advocating for their interests and leveraging existing programs to alleviate their financial burdens.

Navigating Student Loan Forgiveness: Who Can Guide You to Relief?

You may want to see also

Explore related products

![]()

Current Policy Actions: Analyzing recent executive orders or legislation related to student loan forgiveness

The Biden administration has taken significant steps to address the student loan crisis through a series of targeted executive actions and legislative efforts. One of the most notable measures is the extension of the student loan payment pause, which has provided millions of borrowers with financial relief during the COVID-19 pandemic. Initially set to expire in September 2020, the pause has been extended multiple times, most recently until December 31, 2022, offering borrowers a reprieve from payments and accruing interest. This action alone has saved borrowers an estimated $15 billion per month, highlighting the administration’s commitment to easing financial burdens.

Another critical policy action is the expansion of the Public Service Loan Forgiveness (PSLF) program. In October 2021, the Department of Education announced a temporary waiver that allows past payments on all types of federal loans to qualify for PSLF, regardless of the repayment plan. This change has the potential to erase debts for hundreds of thousands of public servants, including teachers, nurses, and nonprofit workers, who have dedicated their careers to serving their communities. Borrowers must take action by October 31, 2023, to benefit from this waiver, underscoring the urgency for eligible individuals to review their loan histories and apply.

Beyond these measures, the Biden administration has also pursued targeted loan cancellation for specific groups. For instance, in April 2022, the Department of Education announced $6.8 billion in loan forgiveness for over 200,000 borrowers who were defrauded by for-profit colleges, particularly those who attended institutions like Corinthian Colleges and ITT Tech. This action builds on previous efforts under the Borrower Defense to Repayment program, which had been largely stalled during the previous administration. Such moves signal a broader strategy to address systemic issues in the student loan system while providing immediate relief to vulnerable borrowers.

However, the most anticipated and contentious policy action remains the potential for broad-based student loan cancellation. While President Biden has expressed support for canceling up to $10,000 in federal student debt per borrower, with an additional $10,000 for Pell Grant recipients, no executive order has been issued to date. Legal challenges and political opposition have complicated this effort, raising questions about its feasibility. Advocates argue that such cancellation would stimulate the economy and reduce racial wealth gaps, while critics warn of its cost and fairness implications. As the administration navigates these complexities, borrowers are left in a state of uncertainty, underscoring the need for clear communication and decisive action.

In summary, the Biden administration’s policy actions on student loan forgiveness reflect a multi-pronged approach, combining immediate relief with long-term systemic reforms. While significant strides have been made, the ultimate fate of broad-based cancellation remains uncertain. Borrowers should stay informed about available programs, such as the PSLF waiver and Borrower Defense to Repayment, and take proactive steps to maximize their eligibility. As the debate continues, these policies serve as a critical lifeline for millions, offering hope for a more equitable and sustainable future in higher education financing.

Bankruptcy and Student Loans: Will Deferment End After Filing?

You may want to see also

Explore related products

![]()

Economic Impact: Assessing how canceling student debt could affect the U.S. economy

The cancellation of student debt has been a hotly debated topic, with proponents arguing it could stimulate economic growth and opponents warning of potential inflationary pressures. At the heart of this debate is the question of how such a policy would redistribute wealth and influence consumer behavior. If President Biden were to cancel a significant portion of student debt, approximately $1.7 trillion, it would directly impact the 45 million Americans currently burdened by this debt. This move could free up disposable income, allowing individuals to spend more on goods and services, potentially boosting sectors like housing, retail, and automotive industries. However, the economic ripple effects are complex and multifaceted, requiring a nuanced analysis of both short-term gains and long-term consequences.

Consider the immediate economic benefits: canceling student debt could inject billions of dollars into the economy annually. For instance, the average monthly student loan payment is around $400. If $10,000 in debt were canceled per borrower, it would save individuals roughly $100 per month, assuming a standard 10-year repayment plan. Multiply this by millions of borrowers, and the cumulative effect could be substantial. Increased consumer spending could drive GDP growth, create jobs, and reduce financial stress, particularly among younger demographics. A study by the Roosevelt Institute estimated that canceling $1.4 trillion in student debt could add between $86 billion and $108 billion to the economy annually over the next decade. This suggests a powerful short-term stimulus effect, but it’s only part of the equation.

However, the economic impact isn’t without potential drawbacks. Critics argue that widespread debt cancellation could exacerbate inflation, especially if it leads to increased demand without a corresponding increase in supply. Additionally, the policy could strain federal finances, as the government would absorb the cost of forgiven loans. This could necessitate higher taxes or reduced spending in other areas, potentially offsetting some of the economic benefits. Another concern is the moral hazard argument: canceling debt might discourage future borrowers from taking personal responsibility for their loans, though evidence on this remains inconclusive. Balancing these risks requires careful policy design, such as targeting relief to low- and middle-income borrowers or implementing gradual forgiveness to minimize economic shocks.

A comparative analysis with other stimulus measures provides further insight. For example, the 2021 stimulus checks directly increased consumer spending but had a limited long-term impact on economic growth. In contrast, student debt cancellation could have a more sustained effect by addressing a structural barrier to financial stability. However, unlike stimulus checks, debt cancellation is a one-time intervention, meaning its economic benefits might plateau after a few years. To maximize its impact, policymakers could pair debt cancellation with reforms to make higher education more affordable, such as increasing funding for public colleges or expanding income-driven repayment plans. This dual approach could address both the symptom (existing debt) and the root cause (rising tuition costs).

In conclusion, canceling student debt has the potential to reshape the U.S. economy by freeing up disposable income and reducing financial inequality. However, its success hinges on thoughtful implementation and complementary policies. For individuals, the immediate relief could be transformative, enabling investments in homes, businesses, or retirement savings. For the economy, the benefits could include increased consumer spending, reduced defaults, and a more equitable distribution of wealth. Yet, policymakers must navigate challenges like inflation and fiscal sustainability to ensure the policy achieves its intended goals. As the debate continues, one thing is clear: the economic impact of student debt cancellation would be profound, but its ultimate success depends on striking the right balance between relief and responsibility.

Unlock Debt-Free Education: Your Guide to Applying for Forgivable Student Loans

You may want to see also

Explore related products

![]()

Public Opinion: Exploring voter and demographic support for or against debt cancellation

Public opinion on student debt cancellation is a mosaic of perspectives, shaped by age, income, education level, and political affiliation. Polls consistently show that younger voters, particularly those aged 18–34, overwhelmingly support debt cancellation, with approval rates often exceeding 70%. This demographic bears the brunt of student loan burdens, with many delaying major life milestones like homeownership or starting families due to debt. For them, cancellation isn’t just policy—it’s a lifeline. Conversely, older generations, especially those over 65, are more divided, with only about 40% supporting broad cancellation. Many in this group either paid off their loans decades ago or never took on debt, leading to skepticism about the fairness of forgiving others’ obligations.

Income and education levels further stratify opinions. Lower-income households, earning under $50,000 annually, tend to favor cancellation, viewing it as a tool for economic mobility. However, support wanes among higher-income earners, particularly those above $100,000, who often argue that cancellation benefits the relatively privileged at the expense of taxpayers. Among college graduates, opinions split: those with advanced degrees are more likely to support cancellation, while those with only a bachelor’s degree are more ambivalent, perhaps reflecting varying debt levels and career outcomes.

Political affiliation is a dominant fault line in this debate. Democrats, especially progressives, champion cancellation as a matter of economic justice, with over 80% supporting some form of debt relief. Independents are more moderate, with about 55% in favor, often contingent on targeted relief rather than blanket forgiveness. Republicans, however, are staunchly opposed, with fewer than 30% supporting cancellation, citing concerns about fiscal responsibility and moral hazard. This partisan divide complicates Biden’s ability to implement broad cancellation without alienating key voter blocs.

To navigate this complex landscape, policymakers must consider targeted approaches. For instance, capping cancellation at $50,000 per borrower could address the most severe debt burdens while mitigating criticism of overreach. Income-based eligibility thresholds, such as limiting relief to those earning under $75,000 annually, could also build broader support. Pairing cancellation with reforms to prevent future debt crises, like lowering college costs or expanding Pell Grants, could appeal to both proponents and skeptics.

Ultimately, public opinion on student debt cancellation reflects deeper tensions about fairness, responsibility, and opportunity. While broad cancellation enjoys significant support, particularly among younger and lower-income voters, it faces resistance from older, wealthier, and conservative demographics. Crafting a policy that balances these perspectives will require nuance, creativity, and a willingness to compromise. For Biden, the challenge isn’t just about debt—it’s about bridging divides in a polarized electorate.

Why Student Loan Forgiveness Delays Persist: Unraveling the Slow Process

You may want to see also

Explore related products

![]()

Legal Challenges: Examining potential legal obstacles to implementing widespread student loan forgiveness

The authority to cancel student debt on a mass scale hinges largely on statutory interpretation, specifically the Higher Education Act of 1965. Section 432(a) grants the Secretary of Education the power to "enforce, pay, compromise, waive, or release any right, title, claim, lien, or demand" related to federal student loans. Proponents argue this language provides broad discretion for forgiveness. However, legal challenges will likely center on whether this authority extends to blanket cancellation versus case-by-case modifications, setting the stage for protracted litigation over congressional intent and administrative reach.

A second critical obstacle lies in Article I of the Constitution, which vests all legislative powers in Congress. Opponents of widespread forgiveness will argue that canceling trillions in debt constitutes a policy decision rightfully reserved for lawmakers, not executive fiat. Courts will need to weigh whether the executive branch is overstepping by effectively rewriting loan terms without explicit statutory authorization, potentially violating the separation of powers doctrine. This structural challenge could prove insurmountable if judges view forgiveness as legislating by proxy.

Standing to sue presents a procedural hurdle that could derail challenges before reaching the merits. Plaintiffs must demonstrate concrete, particularized injury traceable to the forgiveness policy. Taxpayer standing is generally insufficient, leaving potential challengers to identify specific harmed parties, such as private loan servicers or states claiming fiscal injury. However, even if standing is established, courts may still dismiss cases under the political question doctrine, ruling that debt cancellation is inherently a policy matter unsuited for judicial resolution.

Even if legal authority is established, implementing forgiveness would require navigating due process and equal protection claims. Borrowers excluded from relief (e.g., those with private loans or who already repaid debt) could argue arbitrary discrimination. Additionally, servicers and guaranty agencies might claim deprivation of property rights without adequate process. While these arguments face uphill battles, they could delay implementation through injunctive relief, creating administrative chaos and political backlash.

Ultimately, the Supreme Court’s recent skepticism of expansive administrative powers (e.g., *West Virginia v. EPA*) suggests a cautious approach to executive action. Lower courts will likely scrutinize forgiveness claims under the major questions doctrine, requiring clear congressional authorization for transformative policies. While not insurmountable, these legal barriers underscore the need for legislative solutions, as executive action alone risks years of litigation and uncertain outcomes, leaving borrowers in limbo.

Unlock 10K Student Loan Forgiveness: Top Application Destinations

You may want to see also

Frequently asked questions

As of now, President Biden has not announced plans to cancel all student loan debt entirely. His administration has focused on targeted relief measures, such as income-driven repayment plans, Public Service Loan Forgiveness reforms, and limited debt cancellation for specific groups (e.g., borrowers defrauded by for-profit schools).

President Biden campaigned on canceling $10,000 in student loan debt per borrower, but this has not been implemented broadly. His administration has provided targeted relief, including $10,000 to $20,000 in cancellation for Pell Grant recipients under a 2022 proposal, which is currently stalled due to legal challenges.

The student loan payment pause ended in October 2023, and payments resumed in the same month. There are no current plans to extend the pause further, though the administration has emphasized efforts to make repayment more manageable through reforms and relief programs.

![EidolonGreen [China Medicinal Herb] Bidens Tripartita(Bidens Tripartita L./Trifid Bur-marigold/Gui Zhen Cao/鬼针草/귀신침 초) Dried Bulk Herb 3 Oz (88 g)](https://m.media-amazon.com/images/I/61B8U7-NK2S._AC_UL320_.jpg)