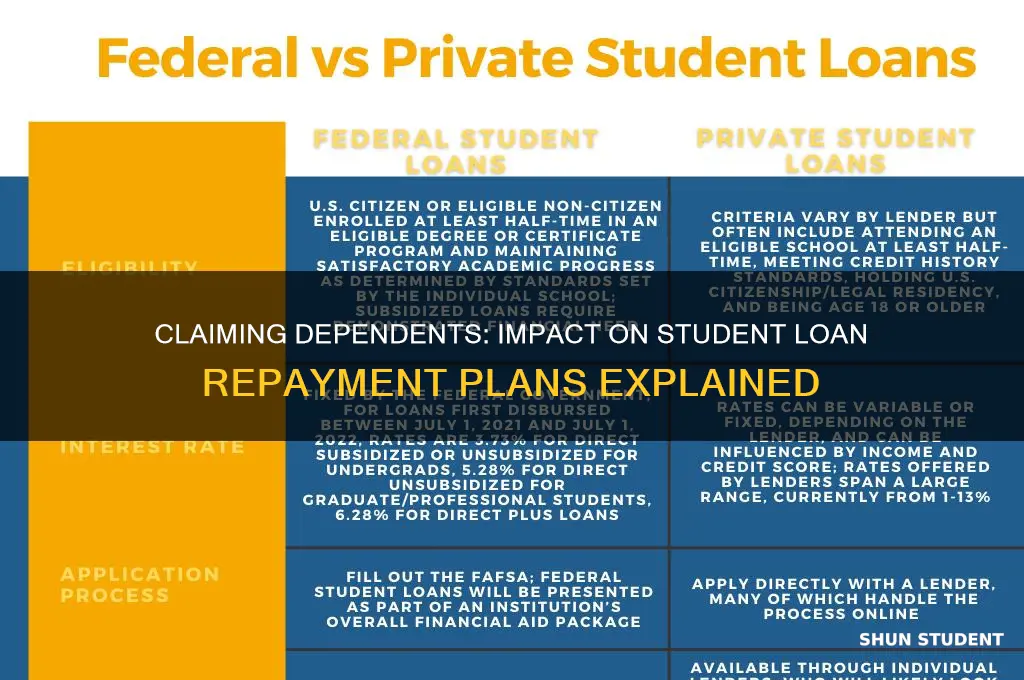

Claiming someone as a dependent can significantly impact student loan payments, particularly for income-driven repayment plans. These plans calculate monthly payments based on the borrower's income and family size, so adding a dependent may reduce the borrower's adjusted gross income, potentially lowering their required payment. However, this effect varies depending on the specific loan type and repayment plan. For instance, federal student loans under income-driven plans often benefit from an increased family size, while private loans typically do not consider dependency status. Additionally, claiming a dependent might affect eligibility for loan forgiveness programs or subsidies. Borrowers should carefully review their loan terms and consult with a financial advisor to understand how dependency claims could influence their repayment obligations.

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

What You'll Learn

![]()

Impact on Income-Driven Repayment Plans

Claiming a dependent can significantly alter the financial landscape for those enrolled in income-driven repayment (IDR) plans for student loans. These plans, which include options like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), calculate monthly payments based on discretionary income—a figure derived from your adjusted gross income (AGI) and family size. Adding a dependent increases your family size, which in turn raises the poverty guideline threshold used to determine discretionary income. This adjustment often results in lower monthly payments, as a larger portion of your income is considered necessary for living expenses.

For example, consider a single borrower earning $50,000 annually in a state with a poverty guideline of $13,590 for one person and $18,310 for two people. Without claiming a dependent, their discretionary income would be $36,410 ($50,000 - $13,590). On an IBR plan, they’d pay 15% of this amount, or $5,461 annually, or roughly $455 per month. However, if they claim a dependent, their discretionary income drops to $31,690 ($50,000 - $18,310), reducing their annual payment to $4,754, or about $396 per month. This $59 monthly difference can add up over time, especially for borrowers with multiple dependents or lower incomes.

While the financial relief is appealing, borrowers must navigate potential pitfalls. For instance, REPAYE plans require borrowers to report spousal income and include it in the payment calculation if married filing jointly. Claiming a dependent doesn’t offset this inclusion, so married borrowers might see less benefit than single parents. Additionally, IDR plans require annual recertification of income and family size. Failing to update this information accurately can lead to payment adjustments, capitalized interest, or even removal from the plan. Borrowers should use the Federal Student Aid website to recertify promptly and ensure all details are current.

A practical tip for maximizing this strategy is to time dependent claims strategically. If you anticipate a significant income increase in the coming year, claim the dependent during the recertification period to lock in lower payments for the next 12 months. Conversely, if your income is expected to drop, delay claiming the dependent until the following recertification cycle to minimize payments during the lower-earning period. Tools like the Department of Education’s Loan Simulator can help model these scenarios to determine the optimal approach.

In conclusion, claiming a dependent can be a powerful tool for reducing student loan payments on IDR plans, but it requires careful planning and awareness of the rules. By understanding how family size impacts discretionary income calculations and staying vigilant during recertification, borrowers can leverage this strategy to manage their debt more effectively. Always consult official resources or a financial advisor to ensure your decisions align with your long-term financial goals.

Is Student Loan Forgiveness Legal? Understanding the Legal Framework

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![]()

Dependent Status and Tax Benefits

Claiming someone as a dependent on your taxes can significantly impact your financial landscape, particularly when it comes to student loan payments. The Internal Revenue Service (IRS) allows taxpayers to claim certain individuals as dependents, which can result in valuable tax benefits. For instance, the Child Tax Credit and the Credit for Other Dependents can reduce your tax liability by up to $2,000 per dependent, with a portion of it being refundable. Additionally, claiming a dependent can qualify you for the Earned Income Tax Credit (EITC), which can provide substantial financial relief depending on your income level. These tax benefits can free up funds that could be allocated toward student loan payments, effectively reducing the burden of educational debt.

However, the interplay between dependent status and student loan repayment plans requires careful consideration. Income-driven repayment (IDR) plans, such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE), calculate monthly payments based on your adjusted gross income (AGI) and family size. If you claim a dependent, your family size increases, which can lower your monthly student loan payments. For example, a single borrower earning $50,000 annually with $30,000 in student loans might see their monthly payment drop from $300 to $200 under an IDR plan by adding a dependent. This reduction occurs because the formula accounts for the additional financial responsibility of supporting another person.

It’s crucial to weigh the pros and cons of claiming a dependent in this context. While the tax benefits and potential reduction in student loan payments are attractive, claiming a dependent also affects the student’s eligibility for financial aid. If the dependent is a college student, being claimed on someone else’s taxes can limit their access to need-based aid, such as Pell Grants or subsidized loans. For instance, a student who is claimed as a dependent must report their parents’ income on the FAFSA, which could result in a higher Expected Family Contribution (EFC) and reduced aid eligibility. Families should assess whether the tax savings and lower loan payments outweigh the potential loss of financial aid for the student.

To navigate this complexity, consider a step-by-step approach. First, evaluate the dependent’s financial situation and whether they meet IRS criteria, such as the residency test and income threshold (generally, their gross income must be less than $4,700 in 2023). Second, calculate the potential tax savings and student loan payment reductions using online calculators or consulting a tax professional. Third, assess the impact on financial aid by using tools like the FAFSA forecaster. Finally, make an informed decision based on long-term financial goals. For example, if the dependent is a young adult with minimal income, claiming them might be advantageous, especially if the tax savings can be directed toward aggressive student loan repayment.

In conclusion, dependent status offers tangible tax benefits that can indirectly ease student loan payments, particularly through income-driven repayment plans. However, the decision should be made with a full understanding of its implications for financial aid and overall financial health. By carefully analyzing the specifics of your situation and seeking professional advice when needed, you can maximize the benefits while minimizing potential drawbacks.

Discovering Forgivable Student Loans: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![]()

Effect on Loan Eligibility Criteria

Claiming someone as a dependent can significantly alter the financial landscape when applying for student loans, particularly in the context of federal aid eligibility. The Free Application for Federal Student Aid (FAFSA) uses the number of dependents in a household to calculate the Expected Family Contribution (EFC), a key factor in determining loan eligibility and grant amounts. For instance, a higher number of dependents may reduce the EFC, potentially increasing the student's eligibility for subsidized loans or grants. Conversely, if a student is claimed as a dependent on someone else’s tax return, their eligibility for certain loans may be based on their parents’ income, which could limit their access to higher loan amounts or favorable interest rates.

Consider a scenario where a parent claims their college-aged child as a dependent. This decision directly impacts the child’s FAFSA application, as parental income and assets are factored into the EFC calculation. For example, if the parent earns $80,000 annually, the EFC might be significantly higher than if the student filed independently. This could reduce the student’s eligibility for need-based loans like Perkins Loans or subsidized Direct Loans, which are reserved for those demonstrating financial need. On the other hand, if the student is not claimed as a dependent, they may qualify for higher loan limits under unsubsidized Direct Loans, though interest accrues immediately.

Private student loans operate under a different set of rules but are equally affected by dependency status. Lenders often require a creditworthy cosigner if the borrower is a dependent, as they typically lack sufficient credit history. For instance, a dependent student with a cosigner might secure a private loan with a 5% interest rate, whereas an independent student with a similar profile could face rates as high as 12% without one. This underscores the importance of understanding how dependency status influences not only federal aid but also private loan terms.

To navigate these complexities, students and families should weigh the pros and cons of claiming dependency. For example, if a parent’s income is modest, claiming the student as a dependent might yield tax benefits that outweigh the reduction in loan eligibility. Conversely, if the parent’s income is high, the student might benefit from filing independently, though this could disqualify them from certain tax credits. Practical tips include using FAFSA’s dependency questionnaire to assess status accurately and consulting a financial aid advisor to model different scenarios. Ultimately, the decision should align with long-term financial goals, balancing immediate loan needs with future tax implications.

Student Loan Forgiveness Approval: How to Check Your Status Now

You may want to see also

Explore related products

$23.99

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![TurboTax Deluxe Online Edition 2025, Federal Tax Return [Activation Code]](https://m.media-amazon.com/images/I/61bFazlntVL._AC_UL320_.jpg)

![]()

Changes in Financial Aid Calculations

Claiming someone as a dependent can significantly alter the financial landscape for student loan payments, primarily through its impact on financial aid calculations. The Free Application for Federal Student Aid (FAFSA) uses a formula called the Expected Family Contribution (EFC) to determine eligibility for grants, work-study, and loans. When a student is claimed as a dependent, their parents’ income and assets are factored into the EFC, often reducing the amount of need-based aid they qualify for. For instance, a family with an annual income of $80,000 and $50,000 in assets might see their EFC increase by 22% if the student is claimed as a dependent, compared to being considered independent. This higher EFC translates to fewer grants and more reliance on loans, potentially increasing the overall debt burden.

The dependency status also affects the types of loans a student can access. Dependent students are eligible for lower-limit federal loans, such as the Direct Subsidized Loan, which caps borrowing at $5,500 for the first year of undergraduate study. In contrast, independent students can borrow up to $9,500 in the same period. While this might seem like a disadvantage, dependent students often benefit from parental support, which can offset the need for higher loan amounts. However, if parents are unwilling or unable to contribute, the lower loan limits can force students to seek private loans with less favorable terms, such as higher interest rates and fewer repayment options.

One often-overlooked aspect is how dependency status influences eligibility for state-based aid and institutional scholarships. Many states and colleges use FAFSA data to award their own financial aid packages. For example, a dependent student in California might miss out on Cal Grants if their family’s EFC exceeds the state’s threshold, even if the student’s individual financial need is high. Similarly, merit-based scholarships that consider family income may become less accessible. To mitigate this, families should explore alternative strategies, such as maximizing tax deductions or adjusting income timing, to lower their EFC without compromising long-term financial goals.

Finally, it’s crucial to understand the long-term implications of dependency status on loan repayment plans. Dependent students often have less control over their financial aid package, which can limit their ability to choose income-driven repayment plans later. For example, if a dependent student consolidates their loans after graduation, their parents’ income may still be considered in determining repayment terms, potentially leading to higher monthly payments. Independent students, on the other hand, can qualify for plans like Pay As You Earn (PAYE) based solely on their own income and family size. This underscores the importance of carefully weighing the immediate benefits of dependency against its future consequences on loan management.

Are Student Loans Forgiven for CCMAs? Exploring Debt Relief Options

You may want to see also

Explore related products

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Dependent Claims and Loan Forgiveness Programs

Claiming a dependent on your taxes can significantly impact your eligibility for certain student loan repayment plans, particularly income-driven repayment (IDR) plans. These plans calculate your monthly payment based on your adjusted gross income (AGI) and family size. Adding a dependent increases your family size, which can lower your monthly payment. For example, if you’re single with no dependents and earn $40,000 annually, your payment under an IDR plan might be $200 per month. Adding a dependent could reduce this to $150, as the formula adjusts for the additional financial responsibility. However, this benefit hinges on accurately reporting your family size and income to your loan servicer.

While claiming a dependent can lower IDR payments, it may complicate eligibility for loan forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven forgiveness. These programs require consistent, qualifying payments over a set period (10–25 years), and any changes to your payment amount or plan could reset your progress. For instance, if you switch IDR plans due to a change in family size, your payment history might not carry over, delaying forgiveness. To avoid this, ensure your loan servicer updates your information promptly and confirm that your payments still qualify under the program’s rules.

A lesser-known strategy involves leveraging dependent claims to maximize forgiveness under IDR plans. If you anticipate qualifying for forgiveness after 20–25 years, strategically increasing your family size (e.g., claiming a parent or child) can lower your payments, minimizing the total amount forgiven. This reduces your tax liability on forgiven debt, as the IRS treats forgiven amounts as taxable income. For example, if $50,000 is forgiven, claiming a dependent could reduce your taxable income by lowering your payments, potentially saving thousands in taxes. Consult a tax professional to ensure compliance with IRS rules.

Finally, beware of pitfalls when claiming dependents for student loan purposes. The IRS and Department of Education have strict definitions of who qualifies as a dependent, and discrepancies can lead to audits or repayment plan adjustments. For instance, claiming a roommate or friend as a dependent to lower payments is fraudulent and carries severe penalties. Additionally, if your dependent’s status changes (e.g., they graduate or move out), update your loan servicer immediately to avoid overpayment or plan disqualification. Always document your eligibility and keep records of tax filings and loan correspondence.

Do You Qualify for Federal Student Loan Forgiveness? Find Out Now

You may want to see also

Frequently asked questions

Yes, claiming someone as a dependent can affect your income-driven repayment (IDR) plan. The adjusted gross income (AGI) used to calculate your payment includes the income of your dependent, which may increase your discretionary income and result in higher monthly payments.

Claiming a dependent does not directly impact your eligibility for student loan forgiveness programs like Public Service Loan Forgiveness (PSLF). However, it may affect your income-driven payment amount, which could influence the total amount forgiven after the required repayment period.

If the dependent’s income is low or nonexistent, it may still be included in your AGI for income-driven repayment calculations. However, if their income is minimal, the impact on your payments may be small. It’s best to use the IRS guidelines and consult a financial advisor to assess the specific effect.

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)