The question of whether Democrats will forgive student loans has become a central issue in American politics, reflecting broader debates about economic inequality, higher education, and government intervention. With millions of Americans burdened by student debt, many are looking to the Democratic Party for solutions, as progressive lawmakers and advocates push for widespread loan forgiveness. President Biden’s campaign promises and recent actions, such as targeted debt relief programs, have fueled both hope and skepticism. While some Democrats argue that canceling student debt would stimulate the economy and address systemic inequities, others worry about the cost, fairness, and potential political backlash. The issue remains divisive, not only within the party but also among voters, as policymakers grapple with balancing relief for borrowers with fiscal responsibility and long-term education reform.

| Characteristics | Values |

|---|---|

| Current Policy Stance | Democrats have advocated for student loan forgiveness but face legal and political challenges. Biden’s $400 billion forgiveness plan was blocked by the Supreme Court in 2023. |

| Proposed Forgiveness Amount | Up to $20,000 in forgiveness for eligible borrowers (with additional $10,000 for Pell Grant recipients). |

| Eligibility Criteria | Borrowers earning < $125,000/year (individuals) or < $250,000/year (married couples). |

| Total Cost Estimate | Approximately $400 billion (one-time forgiveness). |

| Legal Status | Biden’s 2022 plan was struck down by the Supreme Court in June 2023, citing lack of congressional authorization. |

| Alternative Efforts | Focus shifted to improving income-driven repayment plans and fixing Public Service Loan Forgiveness (PSLF). |

| Public Opinion | Mixed support; ~50% of Americans support broad forgiveness, but opposition exists over fairness and cost. |

| Republican Opposition | Strong opposition, arguing it is unfair to non-borrowers and fiscally irresponsible. |

| Ongoing Actions | Paused student loan payments until October 2023; exploring executive actions within legal limits. |

| Legislative Hurdles | Requires congressional approval for large-scale forgiveness, unlikely with divided government. |

| Impact on Borrowers | ~40 million borrowers could benefit, with an average savings of $12,000 per borrower. |

| Economic Arguments | Proponents argue it boosts spending; critics warn of inflationary pressure and moral hazard. |

| Future Prospects | Uncertain; depends on 2024 election outcomes and legal/legislative developments. |

Explore related products

What You'll Learn

![]()

Biden's campaign promise and its impact on voter trust

During his 2020 presidential campaign, Joe Biden pledged to forgive at least $10,000 in federal student loan debt per borrower, a promise that resonated deeply with millions of Americans burdened by educational debt. This commitment was not merely a policy proposal but a symbolic gesture of empathy toward a generation stifled by financial strain. However, the slow and piecemeal execution of this promise—complicated by legal challenges and political maneuvering—has left many voters questioning the administration’s resolve. For young and first-time voters who turned out in record numbers for Biden, the delay feels like a broken contract, raising doubts about the Democratic Party’s ability to deliver on progressive campaign promises.

The impact of this unfulfilled pledge extends beyond policy; it strikes at the core of voter trust. When a candidate’s words fail to align with their actions, it erodes the credibility not just of the individual but of the party they represent. For instance, Biden’s initial $10,000 forgiveness plan, which aimed to benefit 43 million borrowers, was blocked by the Supreme Court in June 2023. While the administration has since canceled $138 billion in student debt through targeted initiatives (e.g., Public Service Loan Forgiveness and income-driven repayment plans), these efforts are perceived as insufficient by many who expected broad, immediate relief. This discrepancy between expectation and reality has created a trust deficit, particularly among younger voters who view student debt forgiveness as a litmus test for the party’s commitment to economic justice.

To rebuild trust, the Biden administration must adopt a two-pronged strategy: transparency and tangible action. First, clear communication about the legal and political hurdles faced in implementing broad forgiveness is essential. Voters are more likely to forgive delays if they understand the complexities involved. Second, the administration should accelerate targeted relief programs and explore executive actions that bypass congressional gridlock. For example, expanding eligibility for income-driven repayment plans or automatically enrolling eligible borrowers in forgiveness programs could demonstrate progress. Practical steps like these, combined with a renewed commitment to legislative solutions, could signal to voters that the promise, though delayed, is not forgotten.

Comparatively, the student debt issue highlights a broader challenge for Democrats: balancing idealism with pragmatism without alienating their base. While Biden’s campaign promise was aspirational, its execution has been constrained by a divided government and judicial opposition. This tension underscores the need for Democrats to reframe their messaging, emphasizing incremental victories while maintaining a long-term vision for systemic reform. For voters, the lesson is clear: campaign promises are only as strong as the mechanisms in place to fulfill them. Trust is built not just on words but on the consistent, visible effort to turn those words into action.

Unlocking Student Loan Forgiveness: A Guide for College Students

You may want to see also

Explore related products

![]()

Economic effects of widespread student debt cancellation

Student debt cancellation, a policy championed by some Democrats, could inject up to $1.7 trillion into the economy, but its effects are far from uniform. Proponents argue that freeing millions from debt would stimulate consumer spending, particularly in sectors like housing and retail. Imagine a 30-year-old teacher with $50,000 in debt suddenly having an extra $500 monthly. That money could go toward a down payment on a home, a new car, or even starting a family—all activities that ripple through the economy. However, critics warn of inflationary pressures if spending outpaces supply, especially in industries already strained by labor shortages.

Analyzing the distributional impact reveals a nuanced picture. While cancellation would benefit 43 million borrowers, the majority of whom are low- to middle-income, it also raises questions of fairness. A recent graduate with $100,000 in debt from a private university might see greater relief than a peer who chose a less expensive public institution. Additionally, those who already paid off their loans or never attended college could feel disenfranchised. Policymakers must balance equity with economic efficiency, perhaps by capping relief at certain income levels or loan amounts.

From a macroeconomic perspective, widespread cancellation could reduce the risk of a debt-driven recession. High student loan burdens have been linked to lower entrepreneurship rates, as individuals prioritize debt repayment over business ventures. For instance, a study by the Federal Reserve found that student debt reduces the likelihood of small business formation by 14%. By alleviating this burden, cancellation could unleash a wave of innovation, creating jobs and driving economic growth. However, this outcome depends on how borrowers allocate their newfound funds—savings or investment would have a different impact than increased consumption.

A cautionary tale emerges when comparing student debt cancellation to other stimulus measures. Direct cash payments during the pandemic, for example, provided immediate relief but also contributed to inflationary spikes. To avoid similar pitfalls, cancellation could be phased in over several years, allowing the economy to adjust gradually. Pairing it with reforms like income-driven repayment plans or increased funding for public colleges could address root causes of debt while mitigating short-term economic shocks.

Ultimately, the economic effects of widespread student debt cancellation hinge on implementation details and broader policy context. While it holds the potential to stimulate growth, reduce inequality, and foster innovation, it is not a silver bullet. Policymakers must weigh its benefits against risks like inflation, moral hazard, and opportunity cost. For borrowers, the impact could be life-changing, but for the economy, it’s a delicate balance—one that requires careful design and strategic execution.

Does AOC Qualify for Student Loan Forgiveness? Exploring Eligibility and Impact

You may want to see also

Explore related products

![]()

Republican opposition and potential legislative roadblocks

Republican opposition to Democratic student loan forgiveness proposals is rooted in fiscal conservatism and concerns about economic fairness. GOP lawmakers argue that broad-scale debt cancellation would disproportionately benefit higher-income earners, as those with advanced degrees often hold larger loan balances. This, they claim, would amount to a regressive wealth transfer funded by taxpayers who did not attend college or have already paid off their debts. For instance, a 2022 Congressional Budget Office report estimated that the top 25% of earners would receive nearly 40% of the benefits from a $10,000 forgiveness plan, amplifying critiques that such policies are poorly targeted.

Legislatively, Republicans have multiple tools to obstruct Democratic initiatives. In the Senate, the filibuster remains a significant hurdle, requiring 60 votes to advance most legislation. With the current partisan divide, Democrats would need bipartisan support or a workaround like budget reconciliation, which has strict rules limiting its use to policies directly impacting federal spending. However, even reconciliation is not foolproof; the Senate parliamentarian’s interpretation of the Byrd Rule could exclude student debt cancellation if deemed extraneous to the budget. This procedural roadblock was evident in 2021 when efforts to include forgiveness in the Build Back Better Act faced skepticism.

Another strategic obstacle is Republican framing of the issue as a moral hazard. Critics argue that forgiving debt without addressing the root causes of rising tuition costs would incentivize future borrowing and shift financial responsibility from individuals to the collective taxpayer. This narrative resonates with their base and complicates Democratic messaging, particularly in swing districts where voters may view such policies as fiscally irresponsible. Polling from Pew Research Center shows that while a majority of Democrats support loan forgiveness, Republican voters overwhelmingly oppose it, underscoring the partisan divide.

Practical tips for navigating this opposition include targeting relief to lower-income borrowers through income-driven repayment plans or means-tested forgiveness, which could mitigate GOP critiques of regressivity. Democrats could also pair forgiveness with reforms to curb college costs, such as increasing Pell Grants or regulating predatory lending practices, to address systemic issues. However, such compromises may alienate progressive factions within the party, highlighting the delicate balance required to advance legislation in a polarized Congress.

In conclusion, Republican opposition to student loan forgiveness is both ideological and procedural, leveraging fiscal arguments, legislative mechanisms, and public opinion to impede Democratic goals. While workarounds exist, they demand strategic concessions and creative policy design. Without bipartisan cooperation or significant procedural reform, large-scale debt cancellation will remain an uphill battle, illustrating the constraints of divided government on ambitious social programs.

Terminal Illness and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

$14.95 $14.95

![]()

Moral hazard debate: fairness vs. financial responsibility

The moral hazard debate surrounding student loan forgiveness hinges on a delicate balance between fairness and financial responsibility. Proponents argue that forgiving loans would rectify systemic inequalities, as many borrowers, particularly from low-income backgrounds, were misled by predatory lending practices or faced limited economic opportunities post-graduation. For instance, data shows that Black students owe an average of $7,400 more in student loans than their white peers upon graduation, a disparity that widens to $25,000 after four years due to compounding interest and lower wealth accumulation. Forgiveness, in this view, is a corrective measure to address these structural injustices.

Critics, however, warn that widespread loan forgiveness could create a moral hazard by incentivizing future borrowers to take on excessive debt under the assumption that it will eventually be absolved. This argument often cites the principle of personal accountability, emphasizing that individuals who voluntarily entered into loan agreements should honor their commitments. A counterpoint to this is the distinction between forgiving loans for all versus targeted relief for those most burdened, such as capping forgiveness at $50,000 for borrowers earning below $125,000 annually. Such a nuanced approach could mitigate moral hazard concerns while still addressing inequities.

From a financial responsibility perspective, the cost of forgiveness—estimated at $1.6 trillion for full cancellation—raises questions about its sustainability and opportunity cost. Critics argue that redirecting these funds toward improving public education, lowering tuition, or expanding income-driven repayment plans could prevent future debt crises. For example, investing in community colleges or vocational training programs could reduce reliance on expensive four-year degrees. Yet, advocates counter that the economic benefits of forgiveness, such as increased consumer spending and homeownership rates, could offset its costs over time.

A practical middle ground might involve pairing limited forgiveness with reforms to prevent future debt accumulation. For instance, implementing stricter regulations on for-profit colleges, which account for 10% of higher education enrollment but 35% of student loan defaults, could curb predatory practices. Additionally, expanding Pell Grants or introducing a federal tuition-free college program could reduce the need for loans altogether. Such a dual approach would address both the fairness of relieving current burdens and the responsibility of preventing future crises.

Ultimately, the moral hazard debate is not a binary choice but a spectrum of policy options. By focusing on targeted relief, systemic reforms, and long-term sustainability, policymakers can navigate the tension between fairness and financial responsibility. The challenge lies in crafting solutions that acknowledge past injustices without perpetuating risky borrowing behaviors, ensuring that the next generation does not face the same dilemmas as today’s borrowers.

Spotting Student Loan Forgiveness Scams: Key Signs to Watch For

You may want to see also

Explore related products

![]()

Long-term consequences for higher education costs and borrowing

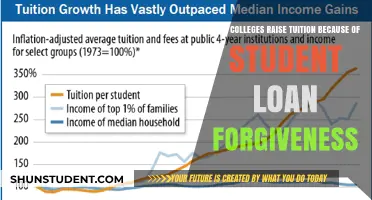

The prospect of student loan forgiveness by Democrats has sparked debates about its long-term impact on higher education costs and borrowing behaviors. While immediate relief for borrowers is a central focus, the ripple effects on tuition inflation, institutional accountability, and future student decisions cannot be ignored. For instance, if colleges anticipate that students’ debts might be forgiven, they may have less incentive to control rising tuition fees, perpetuating a cycle of escalating costs. This dynamic underscores the need for a nuanced approach to forgiveness policies that address both borrower relief and systemic reform.

Consider the comparative example of income-driven repayment plans versus broad-scale loan forgiveness. Income-driven plans cap monthly payments at a percentage of discretionary income, often forgiving remaining balances after 20–25 years. While this provides long-term relief, it does little to curb the upfront borrowing behavior of prospective students. In contrast, widespread forgiveness could inadvertently signal to future students that borrowing excessively is a low-risk strategy, potentially driving up loan amounts. To mitigate this, policymakers could pair forgiveness with stricter regulations on tuition increases, such as tying federal funding to colleges’ ability to keep costs in check.

From an analytical perspective, the long-term consequences of student loan forgiveness hinge on its design and accompanying measures. For example, if forgiveness is limited to borrowers earning below a certain threshold, it could reduce moral hazard while still providing relief to those most in need. However, without addressing the root causes of high tuition—such as administrative bloat or over-reliance on federal aid—costs will continue to rise. A persuasive argument emerges for coupling forgiveness with reforms like increased funding for public institutions or incentivizing low-cost degree programs, ensuring that higher education remains accessible without relying solely on debt.

A descriptive lens reveals the human impact of these policies. Imagine a 25-year-old graduate with $50,000 in debt, currently paying 10% of their $40,000 salary under an income-driven plan. Forgiveness could free them from decades of financial strain, but without systemic changes, the next generation might face even higher debt burdens. Practical tips for borrowers include staying informed about policy updates, exploring refinancing options, and advocating for institutional transparency in tuition pricing. For policymakers, the takeaway is clear: forgiveness alone is insufficient; it must be part of a broader strategy to make higher education affordable and sustainable.

Finally, a cautionary note: the long-term consequences of student loan forgiveness could inadvertently widen educational disparities. If private institutions continue to raise tuition unchecked, while public institutions remain underfunded, forgiveness might disproportionately benefit students from wealthier backgrounds who attend private colleges. To avoid this, Democrats could prioritize targeted forgiveness for low-income borrowers and invest in public higher education, ensuring that all students, regardless of their institution, have access to affordable pathways. Such a balanced approach would address both immediate relief and the systemic drivers of educational debt.

Cancer and Student Loan Forgiveness: Exploring Options for Financial Relief

You may want to see also

Frequently asked questions

Democrats have proposed various student loan forgiveness plans, but complete forgiveness for all borrowers is not guaranteed. Proposals often target specific groups, such as low-income borrowers or those with federal loans, and may include income-based caps or loan amount limits.

Democrats’ proposals vary, with some advocating for $10,000 to $50,000 in forgiveness per borrower. The exact amount depends on the plan, eligibility criteria, and legislative negotiations.

The timeline for implementation depends on legislative approval and administrative processes. If passed, forgiveness could begin within months, but specifics would be outlined in the final legislation or executive action.