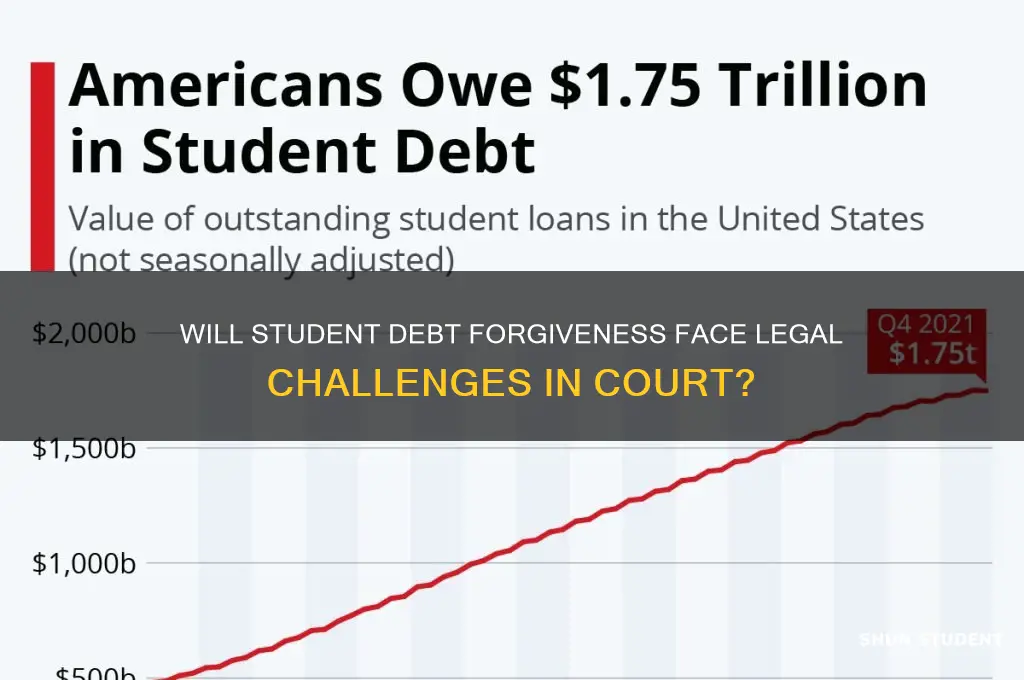

The prospect of widespread student debt forgiveness has sparked intense debate and legal scrutiny, raising questions about whether such policies will face challenges in court. Critics argue that forgiving student debt through executive action could exceed presidential authority and violate constitutional principles, potentially leading to lawsuits from states, lenders, or taxpayers who claim financial harm. Additionally, legal challenges may focus on issues of fairness, equal protection, and the separation of powers, as opponents contend that Congress, not the executive branch, holds the authority to enact such sweeping financial measures. With the Biden administration’s previous attempts at debt relief already facing judicial setbacks, the likelihood of future legal battles remains high, leaving the fate of student debt forgiveness uncertain and deeply intertwined with constitutional and procedural interpretations.

| Characteristics | Values |

|---|---|

| Legal Challenges Filed | Multiple lawsuits have been filed challenging the Biden administration's student debt forgiveness plan. Notable cases include Nebraska v. Biden and Missouri v. Biden. |

| Plaintiffs | Republican-led states, conservative groups, and individuals who argue they are harmed by the policy, such as taxpayers or loan servicers. |

| Key Arguments Against Forgiveness | - Violation of the Administrative Procedure Act (APA) due to lack of public comment. - Exceeds executive authority under the HEROES Act. - Infringes on states' rights and causes financial harm. |

| Current Status | As of October 2023, the Supreme Court has ruled against the Biden administration's broad student debt forgiveness plan, deeming it unconstitutional. |

| Impact on Borrowers | Millions of borrowers who were eligible for relief (up to $20,000) have had their debt forgiveness blocked. |

| Alternative Relief Efforts | The administration has shifted focus to income-driven repayment plans, Public Service Loan Forgiveness (PSLF), and targeted debt cancellation for specific groups (e.g., defrauded students). |

| Political Implications | The issue remains highly partisan, with Democrats advocating for relief and Republicans opposing it as fiscally irresponsible and legally dubious. |

| Public Opinion | Polls show divided opinions, with a majority of Democrats supporting forgiveness and a majority of Republicans opposing it. |

| Future Legal Challenges | Any future debt forgiveness initiatives are likely to face similar legal challenges, requiring congressional action to ensure legitimacy. |

Explore related products

What You'll Learn

![]()

Legal Standing of Challengers

The concept of legal standing is pivotal in determining whether challenges to student debt forgiveness will hold up in court. Legal standing requires that plaintiffs demonstrate a concrete and particularized injury, a causal connection between the injury and the challenged action, and a likelihood that a favorable decision will redress the injury. In the context of student debt forgiveness, potential challengers—such as states, lenders, or individual taxpayers—must meet these criteria to bring a case. For example, a state might argue that debt forgiveness reduces tax revenue or harms state-based loan programs, but it must prove direct harm rather than speculative or generalized grievances. Without standing, even the most politically charged challenges will be dismissed before reaching the merits of the case.

Analyzing past cases provides insight into the hurdles challengers face. In *Department of Commerce v. New York* (2019), the Supreme Court emphasized that plaintiffs must show a "concrete and redressable" injury. Applying this standard to student debt forgiveness, a private lender might claim financial harm if borrowers’ loans are canceled, but courts may question whether such harm is direct enough to confer standing. Similarly, individual taxpayers generally lack standing to challenge government spending decisions unless they can demonstrate a specific, individualized injury. This precedent suggests that challengers must carefully construct their arguments to avoid being dismissed on procedural grounds.

A persuasive argument for standing could come from states claiming that debt forgiveness interferes with their sovereign interests. For instance, if a state operates its own loan programs or relies on tax revenue from student loan servicers, it might argue that federal forgiveness disrupts its financial stability. However, even here, the injury must be tangible and not merely ideological. States would need to provide evidence of direct economic harm, such as reduced funding for education programs or increased administrative costs. This approach requires a detailed, data-driven case rather than broad political rhetoric.

Comparatively, challenges from individual borrowers who oppose debt forgiveness present a unique standing dilemma. These plaintiffs might argue that forgiveness programs create inequity or violate their rights, but courts are unlikely to recognize such claims as concrete injuries. For standing, these challengers would need to show how forgiveness directly harms them, which is difficult without a clear financial or legal injury. This contrasts with cases where plaintiffs challenge policies that directly affect their rights, such as voting restrictions or property seizures.

Instructively, potential challengers should focus on three key steps to establish standing: first, identify a specific, measurable injury; second, link that injury directly to the debt forgiveness policy; and third, demonstrate how a court ruling could remedy the harm. For example, a state could quantify lost tax revenue from forgiven loans and argue that invalidating the policy would restore those funds. Caution must be taken to avoid over-relying on speculative or ideological claims, as courts will scrutinize the concreteness of the injury. Ultimately, the success of any challenge hinges on meeting these procedural requirements before substantive arguments are even considered.

Understanding the Distribution Process of Student Loan Forgiveness Programs

You may want to see also

Explore related products

![]()

Constitutional Authority Concerns

One of the central legal challenges to student debt forgiveness hinges on whether the executive branch possesses the constitutional authority to unilaterally cancel such debts. Critics argue that the Constitution grants Congress, not the President, the power to allocate federal funds and modify financial obligations. The Higher Education Act of 1965, often cited as the basis for forgiveness actions, does grant the Secretary of Education authority to "compromise, waive, or release" student loans, but opponents contend this does not extend to mass cancellation without explicit congressional approval. This tension raises questions about the separation of powers and the limits of executive action.

To illustrate, consider the 2022 Biden administration’s attempt to forgive up to $20,000 in student debt per borrower. Legal scholars and opponents quickly pointed to Article I, Section 9 of the Constitution, which states that only Congress can appropriate funds. By forgiving trillions in debt without congressional authorization, critics argue, the administration overstepped its constitutional bounds. This argument was central to lawsuits filed by states and advocacy groups, which claimed the action violated the Appropriations Clause and the Administrative Procedure Act.

A persuasive counterargument, however, is that the executive branch has historically exercised broad discretion in managing federal programs, including student loans. Proponents of debt forgiveness cite the HEROES Act of 2003, which allows the Secretary of Education to modify loan terms during national emergencies. The COVID-19 pandemic, they argue, provided a valid emergency context for such action. Yet, this interpretation remains contentious, as it stretches the original intent of the HEROES Act, which was designed to assist military personnel, not enact sweeping economic policy.

Practical implications of these constitutional concerns are significant. If courts rule that the executive branch lacks authority to forgive student debt, future attempts at large-scale cancellation would require congressional legislation. This shifts the battleground to Capitol Hill, where partisan divides could stall or block such efforts. For borrowers, this means uncertainty and the need to stay informed about legal developments and potential legislative actions.

In conclusion, constitutional authority concerns are not merely academic—they are the linchpin of legal challenges to student debt forgiveness. Understanding this debate requires examining the interplay between executive power, congressional authority, and statutory interpretation. For policymakers, advocates, and borrowers alike, navigating these complexities is essential to shaping the future of student debt relief.

Forgiving Student Loan Debt: Economic Boost or Unfair Burden?

You may want to see also

Explore related products

![]()

Potential Executive Overreach Claims

The Biden administration's student debt forgiveness plan has sparked intense debate, with critics arguing it constitutes executive overreach. At the heart of this claim is the question of whether the executive branch has the unilateral authority to cancel hundreds of billions in student debt without explicit congressional approval. This action, proponents of the overreach argument contend, bypasses the legislative process and sets a dangerous precedent for future presidential actions.

Here’s a breakdown of the key concerns:

The Power of the Purse: The Constitution grants Congress the power to appropriate funds and manage the nation’s finances. Critics argue that canceling student debt effectively involves spending taxpayer money, a power reserved for Congress. By unilaterally forgiving debt, the administration is arguably usurping this power, potentially weakening the legislative branch's role in fiscal policy.

Imagine if every president could unilaterally cancel debts or allocate funds based on their own priorities, bypassing the deliberative process of Congress. This would fundamentally alter the balance of power outlined in the Constitution.

Statutory Authority: The administration cites the Higher Education Relief Opportunities for Students (HEROES) Act as justification for its actions. This Act grants the Secretary of Education broad authority to modify student loan programs during national emergencies. However, critics argue that the COVID-19 pandemic, while severe, does not justify such a sweeping and permanent debt cancellation. They contend that the HEROES Act was intended for targeted relief, not a blanket forgiveness program.

Separation of Powers: The principle of separation of powers is a cornerstone of American democracy. It ensures that no single branch of government holds excessive power. By unilaterally canceling student debt, critics argue, the executive branch is encroaching on the legislative domain, blurring the lines between these distinct branches and potentially undermining the system of checks and balances.

This overreach, they warn, could set a precedent for future presidents to bypass Congress on other contentious issues, leading to a dangerous concentration of power in the executive.

Legal Challenges and Uncertainty: The potential for legal challenges to the debt forgiveness plan is high. Lawsuits arguing executive overreach are already underway, and the Supreme Court may ultimately decide the fate of the program. This legal uncertainty creates anxiety for borrowers who are unsure if their debt will truly be forgiven.

The debate over executive overreach in the student debt forgiveness plan highlights the complex interplay between presidential power, congressional authority, and the rule of law. While the desire to alleviate the burden of student debt is understandable, the means by which this is achieved must be carefully considered to ensure the long-term health of our democratic institutions.

COVID-19 Student Loan Forgiveness: What Borrowers Need to Know Now

You may want to see also

Explore related products

$14.95 $14.95

![]()

Impact on Existing Lawsuits

The introduction of student debt forgiveness programs has the potential to significantly alter the landscape of existing lawsuits related to student loans. For instance, borrowers who have filed lawsuits against loan servicers for alleged misconduct or mismanagement may find their cases impacted by the new policy. If a borrower’s debt is forgiven, claims for damages related to overpayment or improper handling of their account could become moot, as the financial harm they sought to remedy no longer exists. This shift could lead to a wave of case dismissals or settlements, as plaintiffs and defendants reassess the viability of ongoing litigation.

Consider the procedural implications for class-action lawsuits, where groups of borrowers collectively challenge lending practices. If a substantial portion of the class qualifies for debt forgiveness, the court may need to redefine the class or even decertify it, as the commonality of injury—a cornerstone of class-action litigation—diminishes. For example, in *Sweet v. Cardona*, a case challenging the Public Service Loan Forgiveness program, the court might need to reevaluate standing if many plaintiffs no longer hold qualifying debt. Defense attorneys could argue that the case is no longer justiciable, while plaintiffs might counter that residual harms, such as credit damage, persist.

From a strategic standpoint, borrowers with pending lawsuits should consult legal counsel to weigh the pros and cons of accepting debt forgiveness. While forgiveness offers immediate financial relief, it may foreclose the possibility of recovering additional damages or obtaining injunctive relief against lenders. For instance, a borrower suing for $50,000 in damages might receive $20,000 in debt forgiveness but lose the chance to hold the servicer accountable for systemic issues. Attorneys should advise clients to carefully review the terms of forgiveness programs, as some may require waiving the right to pursue future claims.

Finally, the interplay between debt forgiveness and existing lawsuits underscores the need for legislative clarity. Policymakers must address whether forgiven debt extinguishes related claims or if borrowers retain the right to seek redress for past harms. For example, the Higher Education Act could be amended to specify that forgiveness does not preclude litigation for violations such as predatory lending or fraud. Without such guidance, courts will face a patchwork of interpretations, potentially leading to inconsistent outcomes across jurisdictions. Borrowers and advocates should push for explicit protections to ensure that debt relief does not inadvertently shield wrongdoers from accountability.

Is Loan Forgiveness for Graduate Students a Viable Solution?

You may want to see also

Explore related products

![]()

Role of Judicial Precedent

The role of judicial precedent in determining the fate of student debt forgiveness hinges on the legal doctrine of *stare decisis*, which compels courts to follow past decisions when faced with similar cases. In the context of student debt forgiveness, prior rulings on executive authority, separation of powers, and standing to sue will shape how courts evaluate challenges to such policies. For instance, the Supreme Court’s 2023 decision in *Biden v. Nebraska*, which struck down the administration’s initial student loan forgiveness plan, established a precedent that executive actions under the Higher Education Relief Opportunities for Students (HEROES) Act must be narrowly tailored to address specific emergencies. This ruling will likely influence future litigation, as challengers will cite it to argue that broad debt forgiveness exceeds statutory authority.

Analyzing the *Biden v. Nebraska* case reveals how judicial precedent operates as both a constraint and a roadmap. The Court’s 6-3 majority opinion emphasized that the HEROES Act does not grant the Secretary of Education the power to cancel student debt en masse. This precedent sets a high bar for any future forgiveness initiatives, requiring them to demonstrate a direct connection to the COVID-19 emergency and avoid overreach. Advocates for debt relief, however, may seek to distinguish new proposals from the invalidated plan by highlighting narrower scope or alternative statutory bases, such as the Higher Education Act. This strategic maneuvering underscores the dynamic interplay between precedent and legal innovation.

Instructively, litigants challenging student debt forgiveness must carefully navigate the landscape of judicial precedent to build a compelling case. First, they should identify and cite relevant rulings that limit executive authority, such as *Biden v. Nebraska* or *Department of Homeland Security v. Regents of the University of California* (2020), which scrutinized the repeal of DACA. Second, they must establish standing by demonstrating concrete harm, a requirement reinforced by precedents like *Spokeo, Inc. v. Robins* (2016). Third, challengers should frame their arguments within the doctrine of major questions, a principle articulated in *West Virginia v. EPA* (2022), which holds that significant policy changes require clear congressional authorization. By grounding their case in established precedent, challengers can strengthen their legal footing.

Persuasively, the role of judicial precedent also highlights the tension between legal stability and policy adaptability. While precedent ensures consistency and predictability in the law, it can also stifle progressive reforms by anchoring courts to past decisions. For student debt forgiveness, this tension is particularly acute, as the issue intersects with broader debates about economic inequality and government intervention. Critics argue that rigid adherence to precedent may perpetuate systemic injustices, while proponents counter that it safeguards the rule of law. Striking a balance requires courts to interpret precedent flexibly, considering the evolving context of student debt and its societal impact.

Comparatively, the role of judicial precedent in student debt forgiveness cases differs from its application in other policy areas, such as healthcare or environmental regulation. In *NFIB v. Sebelius* (2012), the Supreme Court upheld the Affordable Care Act’s individual mandate by interpreting it as a tax, demonstrating how precedent can be creatively applied to achieve policy goals. Similarly, environmental cases like *Massachusetts v. EPA* (2007) have relied on precedent to expand regulatory authority. In contrast, student debt forgiveness challenges have thus far resulted in narrower interpretations of executive power, reflecting the judiciary’s skepticism toward unilateral action in this domain. This divergence underscores the context-specific nature of precedent and its influence on policy outcomes.

Practically, understanding the role of judicial precedent empowers stakeholders to anticipate legal challenges and craft strategies accordingly. For policymakers, this means designing forgiveness programs with an eye toward existing rulings, such as by limiting scope or securing explicit congressional approval. For advocates, it involves leveraging precedent to build public and legal support, while also pushing for judicial reinterpretation where necessary. For borrowers, awareness of precedent can temper expectations and inform decisions about loan repayment or litigation participation. By treating precedent as a living tool rather than a static barrier, all parties can navigate the complex terrain of student debt forgiveness more effectively.

Trump's Student Loan Forgiveness for Disabled Veterans: Fact or Fiction?

You may want to see also

Frequently asked questions

Yes, student debt forgiveness is likely to face legal challenges, particularly from states, organizations, or individuals who argue it exceeds executive authority or violates constitutional principles.

Republican-led states, conservative groups, and individuals who believe they are harmed by the policy (e.g., taxpayers or loan servicers) are most likely to file lawsuits against student debt forgiveness.

Challengers may argue that the policy violates the separation of powers, lacks statutory authority under the Higher Education Relief Opportunities for Students (HEROES) Act, or infringes on states' rights and taxpayer standing.