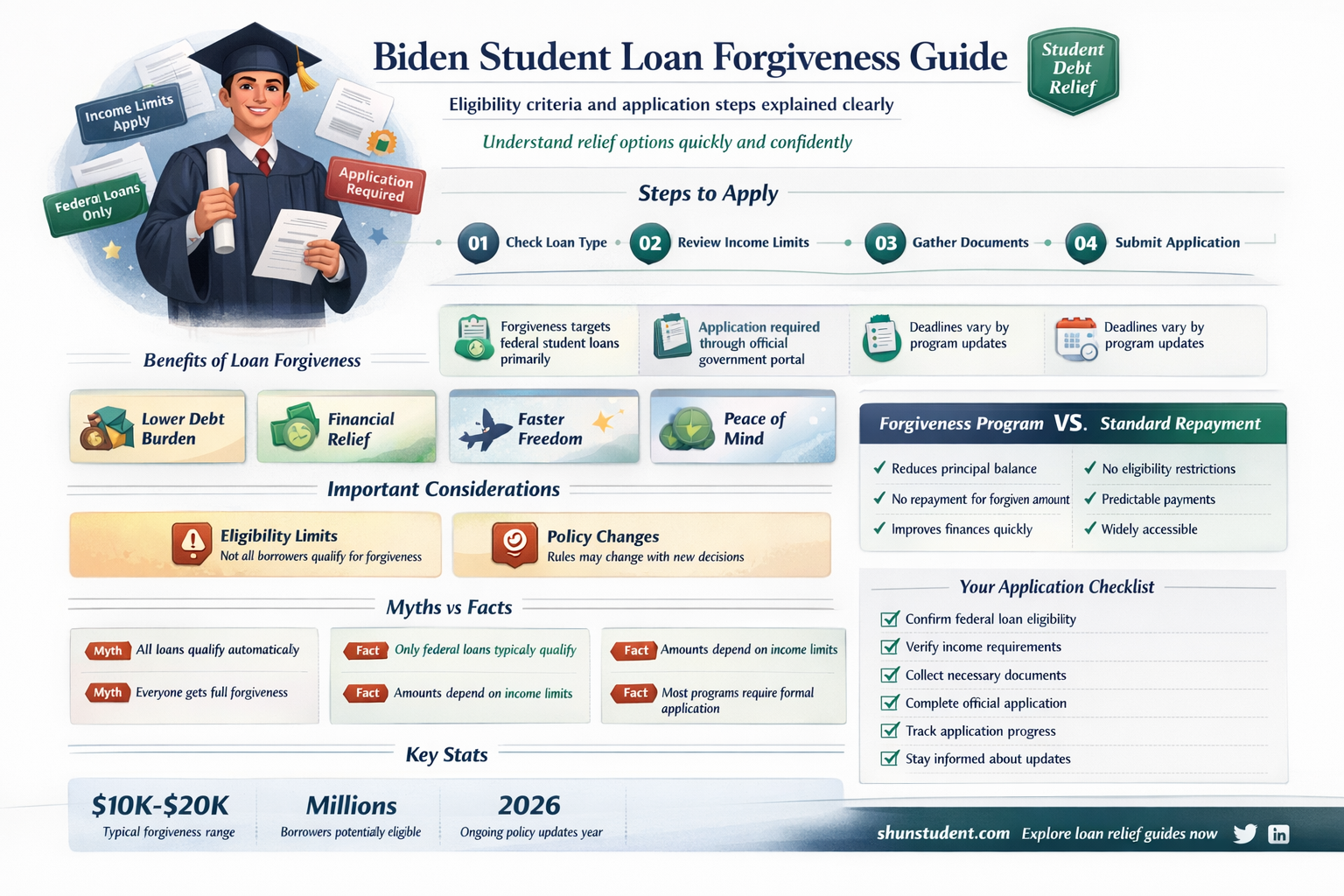

If you're wondering whether you're eligible for Biden's student loan forgiveness program, it's important to understand the key criteria. The program, officially known as the Public Service Loan Forgiveness (PSLF) waiver and the one-time student debt relief plan, targets specific groups of borrowers. For the PSLF waiver, you must have federal Direct Loans and work full-time for a qualifying employer, such as a government or nonprofit organization, with at least 10 years of eligible payments. The one-time debt relief plan, which offers up to $20,000 in forgiveness, is available to borrowers earning under $125,000 (or $250,000 for married couples) in 2020 or 2021, with Pell Grant recipients eligible for the full amount. Checking your loan type, employment status, and income level against these guidelines will help determine your eligibility.

Explore related products

What You'll Learn

- Income Limits: Check if your income falls below the eligibility threshold for loan forgiveness

- Loan Types: Determine if your federal student loans qualify for forgiveness under Biden’s plan

- Repayment Plans: Understand if your current repayment plan affects forgiveness eligibility

- Public Service: Explore forgiveness options for public service or nonprofit workers

- Application Process: Learn how to apply and what documents are required for forgiveness

![]()

Income Limits: Check if your income falls below the eligibility threshold for loan forgiveness

One of the critical factors in determining eligibility for Biden’s student loan forgiveness program is your income level. The program sets specific thresholds based on your annual earnings, which vary depending on your filing status (single or married). For example, as of the latest guidelines, individuals earning less than $125,000 per year and married couples filing jointly with incomes under $250,000 may qualify for up to $10,000 in loan forgiveness. Pell Grant recipients can receive up to $20,000, provided they meet the same income criteria. These limits are not arbitrary; they aim to target relief toward borrowers with the greatest financial need.

To assess your eligibility, start by gathering your most recent tax return or pay stubs to calculate your annual income. If you’re self-employed, use your adjusted gross income (AGI) from your tax filings. Keep in mind that the program uses your income from the year prior to the application period, so 2021 or 2022 tax data is typically relevant. If your income fluctuates, consider whether your current earnings align with the eligibility threshold or if you anticipate falling below it in the near future. Tools like the IRS’s tax transcript service can help you verify your income if needed.

It’s important to note that income limits are not the only eligibility criterion, but they are a deal-breaker if exceeded. For instance, even if you hold eligible federal loans, surpassing the income threshold disqualifies you from forgiveness. However, if your income falls just above the limit, explore strategies like adjusting your tax deductions or contributing to retirement accounts to potentially lower your AGI. Consulting a financial advisor or tax professional can provide tailored advice for your situation.

Finally, stay informed about updates to the program, as income thresholds and eligibility rules may evolve. The Department of Education’s Federal Student Aid website is a reliable resource for the latest information. Remember, meeting the income requirement is a significant step toward securing relief, but it’s just one piece of the puzzle. Verify all eligibility criteria to ensure you’re on track to benefit from this opportunity.

Will Arizona Tax Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Loan Types: Determine if your federal student loans qualify for forgiveness under Biden’s plan

Not all federal student loans are created equal when it comes to Biden's forgiveness plan. The program specifically targets loans held by the Department of Education, meaning privately refinanced federal loans are ineligible. This distinction is crucial, as many borrowers may assume their federal loan status automatically qualifies them, regardless of the servicer.

Can Nelnet Student Loans Be Forgiven? Exploring Options for Relief

You may want to see also

Explore related products

![]()

Repayment Plans: Understand if your current repayment plan affects forgiveness eligibility

Your current repayment plan can significantly impact your eligibility for Biden’s student loan forgiveness programs. Income-driven repayment (IDR) plans, such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), are specifically designed to align with forgiveness pathways. Borrowers on these plans may qualify for forgiveness after 20 or 25 years of qualifying payments, depending on the plan and loan type. Conversely, standard repayment plans, which typically last 10 years, do not offer forgiveness unless payments are made under an IDR plan concurrently. Understanding your plan’s structure is the first step in determining your eligibility for forgiveness.

Switching to an IDR plan could be a strategic move if you’re aiming for forgiveness. These plans cap monthly payments at a percentage of your discretionary income, often making them more affordable than standard plans. For example, REPAYE sets payments at 10% of discretionary income, while IBR limits payments to 10% or 15%, depending on when the loan was taken out. However, switching plans isn’t without considerations. Lower monthly payments may result in more interest accruing over time, potentially increasing the total amount forgiven. Weigh the long-term benefits of forgiveness against the immediate financial relief of lower payments.

A critical factor in forgiveness eligibility is ensuring your payments qualify under your repayment plan. Only payments made while enrolled in an IDR plan count toward the 20 or 25-year forgiveness threshold. For instance, if you’ve been on a standard plan for 5 years and switch to REPAYE, only payments made under REPAYE will count toward forgiveness. Additionally, payments must be made on time and in full to qualify. Partial or late payments may not count, so maintaining consistent compliance with your plan’s terms is essential.

Borrowers on non-IDR plans, such as graduated or extended repayment, are not automatically disqualified from forgiveness but face a steeper path. These plans do not offer forgiveness unless you consolidate into a Direct Loan and enroll in an IDR plan. Consolidation can reset the clock on qualifying payments, so timing is crucial. For example, if you’ve made 10 years of payments on a graduated plan, consolidating and switching to an IDR plan would restart your forgiveness timeline. Evaluate whether the long-term benefits of forgiveness outweigh the reset before making changes.

Finally, stay informed about policy updates, as forgiveness eligibility rules can evolve. For instance, the Biden administration’s one-time account adjustment in 2023 allowed certain borrowers to receive credit for past payment periods, regardless of their repayment plan. Such adjustments could shorten your path to forgiveness. Regularly review your loan servicer’s communications and federal student aid announcements to ensure you’re maximizing your eligibility. Understanding how your repayment plan interacts with forgiveness programs empowers you to make informed decisions about managing your student debt.

Student Loan Forgiveness Bill Blocked: What Does This Mean?

You may want to see also

Explore related products

![]()

Public Service: Explore forgiveness options for public service or nonprofit workers

Public service and nonprofit workers often carry significant student loan debt, but they may qualify for specialized forgiveness programs designed to reward their commitment to serving the greater good. The Public Service Loan Forgiveness (PSLF) program is a cornerstone of these options, offering tax-free forgiveness after 120 qualifying payments while working full-time for a government or nonprofit employer. To maximize eligibility, ensure your loans are federal Direct Loans, enroll in an income-driven repayment plan, and submit the Employment Certification Form annually to track progress.

Beyond PSLF, the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) initiative provides a second chance for borrowers who made payments under a non-qualifying repayment plan. This program evaluates payments under graduated or extended plans, potentially counting them toward the 120-payment requirement. Additionally, the Limited PSLF (LPSLFW) waiver, though expired in October 2023, retroactively credited payments for borrowers in any repayment plan, including those with Federal Family Education Loans (FFEL) or Perkins Loans. If you missed this opportunity, review your payment history with your loan servicer to ensure all eligible payments were counted.

For nonprofit workers, the Income-Driven Repayment (IDR) forgiveness programs offer an alternative pathway. After 20–25 years of qualifying payments under plans like PAYE, REPAYE, IBR, or ICR, the remaining balance is forgiven, though the forgiven amount may be taxed as income. Pairing IDR with PSLF can be particularly strategic, as it allows borrowers to make lower monthly payments while working toward forgiveness. For example, a social worker earning $45,000 annually with $100,000 in debt could reduce monthly payments to as little as $100 under REPAYE while qualifying for PSLF.

A critical caution: avoid falling for scams promising expedited forgiveness or debt cancellation. Legitimate forgiveness programs require consistent documentation and adherence to specific criteria. Always work directly with your loan servicer or the Department of Education to verify eligibility and track progress. For instance, use the PSLF Help Tool to confirm employer eligibility and ensure your payments are correctly applied. By staying informed and proactive, public service and nonprofit workers can navigate these programs effectively, turning years of service into a pathway to financial freedom.

Unlock Student Loan Forgiveness: A Step-by-Step Sign-Up Guide

You may want to see also

Explore related products

![]()

Application Process: Learn how to apply and what documents are required for forgiveness

The Biden administration’s student loan forgiveness program has sparked widespread interest, but navigating the application process can feel like deciphering a complex tax form. Fortunately, the process is designed to be accessible, though it requires attention to detail and preparation. To begin, borrowers must determine their eligibility, which hinges on factors like income, loan type, and repayment plan. Once eligibility is confirmed, the application itself is straightforward, primarily involving an online form and submission of specific documents. Understanding these steps is crucial to avoid delays or rejections.

The application process starts with accessing the official government portal, where borrowers can find the forgiveness application form. This form requires basic personal information, such as your name, Social Security number, and contact details. Additionally, you’ll need to provide details about your loans, including the loan servicer and the type of loans you hold. Federal Direct Loans and federally managed FFELP loans are eligible, but privately held FFELP loans are not. Double-check your loan types through your servicer or the National Student Loan Data System (NSLDS) to ensure accuracy.

Documentation is a critical component of the application. While the process is largely automated, having certain documents on hand can expedite verification. These include recent tax returns (Form 1040) to confirm income eligibility, especially if you’re applying for forgiveness under the Public Service Loan Forgiveness (PSLF) program or income-driven repayment plans. If you’ve made qualifying payments, gather payment records or statements from your loan servicer. For public service workers, an Employer Certification Form (ECF) is required to verify employment. Keep digital copies of these documents, as the application allows for uploads.

One common pitfall is assuming the process is entirely automated. While the system pre-fills some information for existing borrowers, manual verification may be necessary. For instance, if your income fluctuates or you’ve switched jobs, you may need to submit additional proof. Similarly, borrowers who consolidated their loans recently should ensure their payment history is accurately reflected. Proactive communication with your loan servicer can prevent discrepancies and ensure a smoother application experience.

Finally, patience is key. The forgiveness program has seen high demand, which can lead to processing delays. After submitting your application, monitor your email for updates and respond promptly to any requests for additional information. While the process may seem daunting, staying organized and informed can significantly increase your chances of success. Remember, this isn’t a race—accuracy and completeness are far more important than speed.

Retroactive Student Loan Forgiveness: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Eligibility depends on your income and the type of loans you have. Borrowers earning less than $125,000 (individuals) or $250,000 (married couples) annually are eligible for up to $10,000 in forgiveness on federal student loans. Pell Grant recipients may qualify for up to $20,000 in forgiveness.

No, only federal student loans held by the U.S. Department of Education are eligible for forgiveness under this program. Private loans are not included.

The application process is now closed. If you haven’t applied, check with your loan servicer or visit the Federal Student Aid website for updates or alternative relief options.

Yes, Parent PLUS loans are eligible for forgiveness if the borrower meets the income requirements. However, the forgiveness amount is based on the parent’s income, not the student’s.