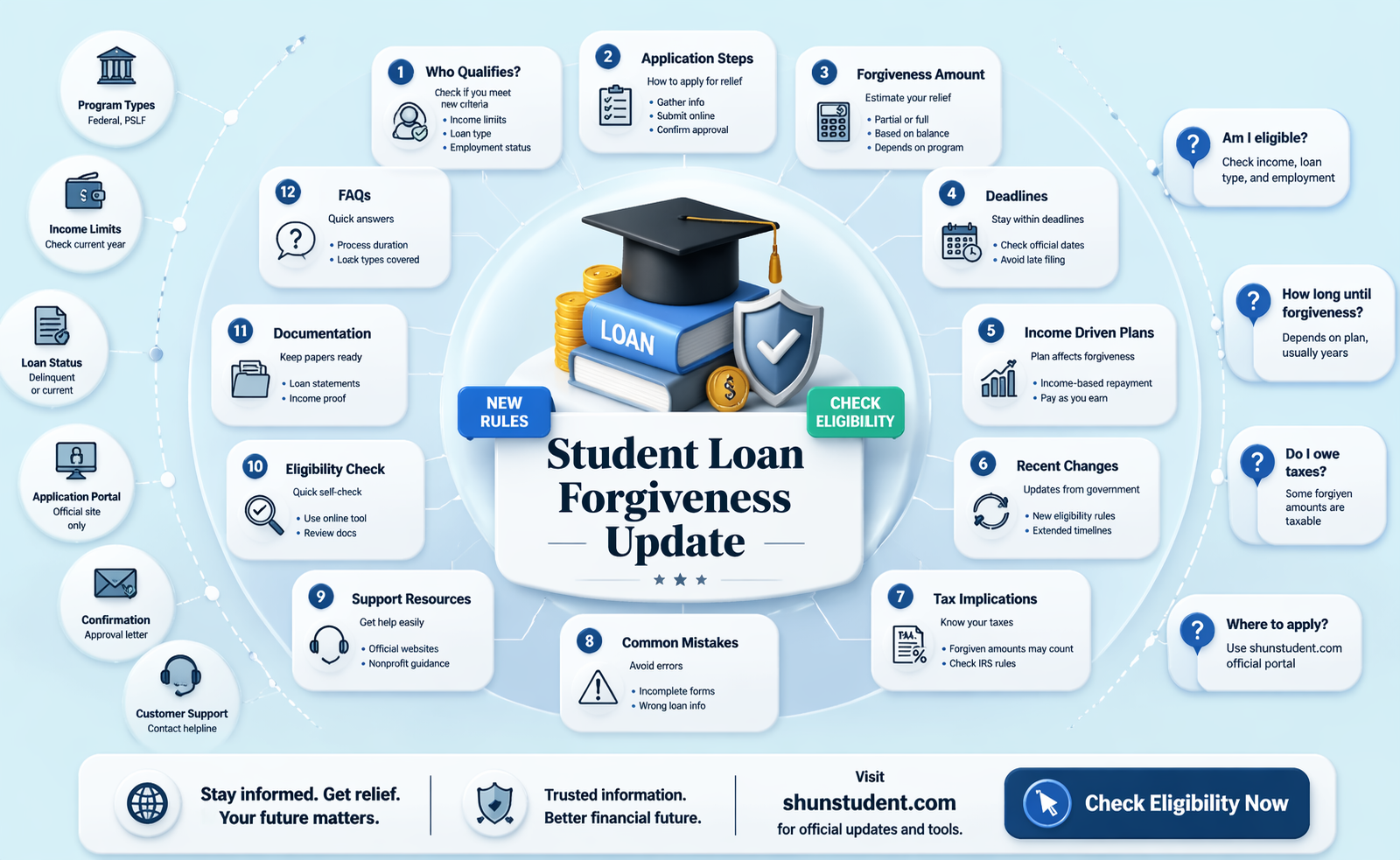

Navigating the complexities of student loan forgiveness can be overwhelming, especially with the ever-changing policies and programs. Many borrowers are left wondering, Am I still eligible for student loan forgiveness? Whether you’re enrolled in Public Service Loan Forgiveness (PSLF), income-driven repayment plans, or other forgiveness programs, understanding the current requirements, deadlines, and updates is crucial. Recent legislative changes, such as temporary waivers or new eligibility criteria, may impact your path to forgiveness. Staying informed about your loan status, repayment plan, and any available waivers can help ensure you’re on track to have your student debt forgiven. If you’re unsure about your eligibility or need guidance, consulting with a loan servicer or financial advisor can provide clarity and peace of mind.

Explore related products

What You'll Learn

- Eligibility Requirements: Understand income limits, repayment plans, and employment criteria for loan forgiveness programs

- Public Service Loan Forgiveness (PSLF): Learn about PSLF rules, qualifying payments, and employer certification process

- Income-Driven Repayment (IDR): Explore IDR plans, forgiveness timelines, and recalculating payment amounts

- Biden Administration Updates: Stay informed on recent policy changes and potential forgiveness expansions

- Tax Implications: Discover if forgiven loan amounts are taxable and exceptions to tax rules

![]()

Eligibility Requirements: Understand income limits, repayment plans, and employment criteria for loan forgiveness programs

Navigating the eligibility maze for student loan forgiveness requires a keen eye on three critical factors: income limits, repayment plans, and employment criteria. Each program, whether it’s Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness, sets distinct thresholds. For instance, PSLF demands 120 qualifying payments while working full-time for a government or nonprofit organization, whereas IDR plans like REPAYE cap monthly payments at 10% of discretionary income and forgive remaining balances after 20–25 years. Understanding these specifics is the first step to determining if you’re on track for forgiveness.

Income limits are a cornerstone of many forgiveness programs, particularly IDR plans. For example, if your adjusted gross income (AGI) falls below 150% of the federal poverty guideline for your family size, your monthly payment could be as low as $0, still counting toward forgiveness. However, exceeding these limits can increase your payments and delay forgiveness. Use the Federal Student Aid website to calculate your discretionary income and ensure you’re enrolled in the right plan. Pro tip: Recertify your income annually to avoid payment spikes and maintain eligibility.

Repayment plans are not one-size-fits-all. PSLF requires borrowers to be on a Direct Loan and enrolled in an IDR plan or the 10-year Standard Repayment Plan (though the latter rarely leads to forgiveness). IDR plans like PAYE or IBR are more forgiving, capping payments at 10–15% of discretionary income. Caution: Switching plans mid-repayment can reset your forgiveness clock. For example, moving from IBR to REPAYE restarts the 20–25-year countdown. Always consult a loan servicer before making changes.

Employment criteria are stringent, especially for PSLF. Qualifying employers include federal, state, local, or tribal government agencies, 501(c)(3) nonprofits, and some other nonprofit organizations. Part-time workers must meet the employer’s definition of full-time or work at least 30 hours per week. Keep detailed records of employment and payments—PSLF requires an Employment Certification Form (ECF) to track progress. For IDR forgiveness, employment is less critical, but consistent payments are paramount.

In conclusion, eligibility for student loan forgiveness hinges on meticulous adherence to income limits, repayment plans, and employment criteria. Missteps like missing recertification deadlines or switching plans without guidance can derail progress. By staying informed and proactive, you can maximize your chances of securing forgiveness. Regularly review program guidelines, consult resources like the Department of Education’s Loan Simulator, and seek advice from financial aid experts to ensure you’re on the right path.

Simone Biles and Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Learn about PSLF rules, qualifying payments, and employer certification process

Public Service Loan Forgiveness (PSLF) offers a lifeline to borrowers committed to careers in public service, but navigating its requirements can be daunting. To qualify, you must make 120 qualifying payments while working full-time for a qualifying employer. These payments must be made under an income-driven repayment plan, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), and be on time, in full, and after October 1, 2007. Understanding these rules is the first step to securing forgiveness.

Qualifying payments are not just about meeting deadlines; they hinge on your employment status and repayment plan. For instance, payments made during periods of deferment or forbearance do not count toward the 120 required. Additionally, your employer must be a government organization at any level, a 501(c)(3) not-for-profit, or another type of not-for-profit that provides qualifying public services. Private employers, even those in public service sectors, do not qualify unless they meet specific criteria. This distinction is critical, as working in a public service role for a non-qualifying employer will not advance your PSLF eligibility.

The employer certification process is a proactive step borrowers should take annually or when changing jobs. By submitting the Employment Certification Form (ECF), you ensure your payments are tracked correctly and confirm your employer’s eligibility. This process also helps identify potential issues early, such as incorrect repayment plans or employment gaps. For example, if you switch from a qualifying employer to a non-qualifying one, your future payments will not count toward PSLF unless you return to eligible employment. Regular certification acts as a safeguard, keeping your forgiveness path on track.

One common pitfall is assuming all federal loan types qualify for PSLF. Only Direct Loans are eligible; Federal Family Education Loans (FFEL) and Perkins Loans do not qualify unless consolidated into a Direct Consolidation Loan. Consolidation resets your payment count, so timing is crucial. For instance, consolidating after making 60 qualifying payments means you’ll start anew, needing another 120 payments post-consolidation. Strategic planning, such as consolidating early and certifying employment promptly, can prevent setbacks.

Finally, PSLF is not automatic; you must apply for forgiveness after completing 120 qualifying payments. The PSLF application requires documentation of your employment and payments, making consistent record-keeping essential. Borrowers should also be aware of the Temporary Expanded Public Service Loan Forgiveness (TEPSLF) program, which can forgive loans under non-qualifying repayment plans if other criteria are met. By staying informed and proactive, public service workers can maximize their chances of achieving loan forgiveness.

Do Student Loan Forgiveness Companies Deliver on Their Promises?

You may want to see also

Explore related products

![]()

Income-Driven Repayment (IDR): Explore IDR plans, forgiveness timelines, and recalculating payment amounts

Income-Driven Repayment (IDR) plans are a lifeline for borrowers juggling federal student loans, offering payments capped at a percentage of discretionary income. Four main plans exist: Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each plan calculates payments differently—for instance, REPAYE sets payments at 10% of discretionary income, while IBR uses 10% or 15% depending on loan type. Understanding these nuances is critical, as the wrong plan could mean higher payments or delayed forgiveness.

Forgiveness timelines under IDR plans vary, but they typically range from 20 to 25 years, depending on the plan and loan type. For example, REPAYE and PAYE promise forgiveness after 20 years for undergraduate loans and 25 years for graduate loans. IBR and ICR extend forgiveness to 20 or 25 years, depending on when the loans were taken out. However, these timelines reset if you switch plans or miss recertification deadlines. Tracking your qualifying payments is essential, as forgiveness isn’t automatic—you must apply for it.

Recalculating payment amounts annually is a cornerstone of IDR plans, but it’s also a common pitfall. Payments are based on your adjusted gross income (AGI) and family size, which must be recertified every 12 months. Miss this deadline, and your payments could spike to the standard 10-year plan rate. Pro tip: Set a calendar reminder 30 days before your recertification date and gather tax documents early. If your income drops unexpectedly—say, due to job loss—request an immediate recalculation to lower your payments.

Comparing IDR plans reveals trade-offs. REPAYE, for instance, offers the lowest payment cap but includes spousal income in calculations, even if filing taxes separately. PAYE excludes spousal income but requires "new borrower" status after 2007. IBR splits into two versions: one for older loans (15% of income) and one for newer loans (10%). ICR ties payments to the lesser of 20% of discretionary income or the standard 12-year plan, making it less favorable for most. Analyzing these differences ensures you align with your financial goals.

Finally, IDR plans aren’t a one-size-fits-all solution. They’re ideal for borrowers with high debt-to-income ratios or those pursuing Public Service Loan Forgiveness (PSLF). However, if your income is expected to rise significantly, standard repayment might save you money in the long run. Use the Federal Student Aid Loan Simulator to model scenarios and determine the best path. Remember, IDR is a tool—wield it wisely to balance affordability today with forgiveness tomorrow.

Seeking Public Forgiveness for Student Plus Loans: Is It Possible?

You may want to see also

Explore related products

![]()

Biden Administration Updates: Stay informed on recent policy changes and potential forgiveness expansions

The Biden administration has been actively addressing the student loan crisis, with recent updates signaling potential expansions in forgiveness programs. As of the latest announcements, borrowers should closely monitor policy changes that could directly impact their eligibility and repayment plans. Key initiatives include targeted relief for specific groups, such as public service workers and those defrauded by for-profit institutions, alongside broader reforms aimed at simplifying the forgiveness process. Staying informed is crucial, as these updates often come with strict deadlines and specific application requirements.

Analyzing the trends, the administration’s approach has shifted from blanket forgiveness to more nuanced, income-driven solutions. For instance, the Saving on a Valuable Education (SAVE) plan, launched in 2023, caps monthly payments at a lower percentage of discretionary income and forgives remaining balances after 10 years for borrowers with original loan amounts of $12,000 or less. This reflects a strategic focus on low-balance borrowers while addressing long-term affordability. Comparatively, previous plans required 20–25 years of payments, making this a significant improvement for eligible individuals.

To navigate these changes, borrowers should take proactive steps. First, verify your loan type and servicer through the Federal Student Aid website, as only federal loans qualify for forgiveness programs. Second, enroll in income-driven repayment plans like SAVE to maximize eligibility for future forgiveness. Third, monitor official government channels and reputable financial news sources for updates, as misinformation can spread quickly. Caution is advised against third-party services promising expedited forgiveness, as these often come with fees and may not deliver results.

A persuasive argument for staying informed lies in the potential financial savings. For example, borrowers who qualify for Public Service Loan Forgiveness (PSLF) can have their remaining balance forgiven after 10 years of qualifying payments, tax-free. However, missing deadlines or failing to meet criteria could result in years of additional payments. The administration’s recent waiver programs, which temporarily relaxed certain PSLF requirements, highlight the importance of timely action. Such opportunities are often limited and may not recur.

Descriptively, the landscape of student loan forgiveness is evolving rapidly, with the Biden administration’s updates offering both hope and complexity. From targeted relief for defrauded borrowers under the Borrower Defense to Repayment program to broader reforms like the SAVE plan, the focus is on addressing systemic issues while providing immediate relief. Practical tips include setting calendar reminders for application deadlines, keeping detailed records of payments, and consulting with certified loan counselors for personalized advice. By staying engaged and informed, borrowers can position themselves to benefit from these transformative changes.

Unlock Retroactive Student Loan Forgiveness: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Tax Implications: Discover if forgiven loan amounts are taxable and exceptions to tax rules

Forgiven student loan amounts can trigger unexpected tax bills, but not always. The IRS generally considers forgiven debt as taxable income, yet exceptions exist, particularly for student loans. Understanding these nuances is crucial for borrowers navigating loan forgiveness programs.

For instance, the Public Service Loan Forgiveness (PSLF) program and income-driven repayment (IDR) plans offer tax-free forgiveness after meeting specific criteria. However, private loan settlements or cancellations outside these programs may still be taxable. This distinction highlights the importance of aligning your forgiveness strategy with tax-exempt provisions.

To avoid tax surprises, borrowers should scrutinize the terms of their forgiveness program. PSLF, for example, requires 120 qualifying payments while working full-time for a government or nonprofit employer. Similarly, IDR plans like PAYE or REPAYE offer tax-free forgiveness after 20–25 years of payments, depending on the plan. Conversely, employer-provided student loan assistance, unless excluded by the CARES Act (extended through 2025), may be taxable as income. Tracking these details ensures compliance and minimizes tax liabilities.

Exceptions to taxable forgiveness are not universal. For example, the American Rescue Act of 2021 temporarily exempts forgiven student loans from taxation through 2025, benefiting borrowers in IDR plans or those receiving forgiveness due to school closures. However, this exemption is time-bound, and future legislation could alter the landscape. Borrowers should stay informed about policy changes and consult tax professionals to strategize effectively.

Practical steps can mitigate tax implications. Maintain detailed records of payments, employment, and program enrollment to substantiate eligibility for tax-free forgiveness. If facing taxable forgiveness, consider setting aside funds to cover potential tax obligations. Additionally, explore state tax laws, as some states may still tax forgiven amounts even if federally exempt. Proactive planning transforms a complex issue into a manageable aspect of financial health.

Disability Student Loan Forgiveness: Tax Implications Explained

You may want to see also

Frequently asked questions

Yes, eligibility for student loan forgiveness depends on the specific program, such as Public Service Loan Forgiveness (PSLF), income-driven repayment (IDR) plans, or limited-time initiatives like the Biden administration’s one-time adjustment. Check the requirements for your program to confirm eligibility.

Recent changes, such as updates to PSLF or IDR plans, may expand eligibility or simplify the process. Review the latest updates from the Department of Education to ensure your application aligns with current rules.

If you’re enrolled in a qualifying repayment plan (e.g., PSLF or IDR) and meet all requirements, you should remain on track for forgiveness. Verify your progress with your loan servicer to ensure no disruptions.

If your loans re-enter repayment, continue making qualifying payments under your forgiveness program. The payment pause did not reset forgiveness timelines, so your progress should continue as long as you meet program requirements.