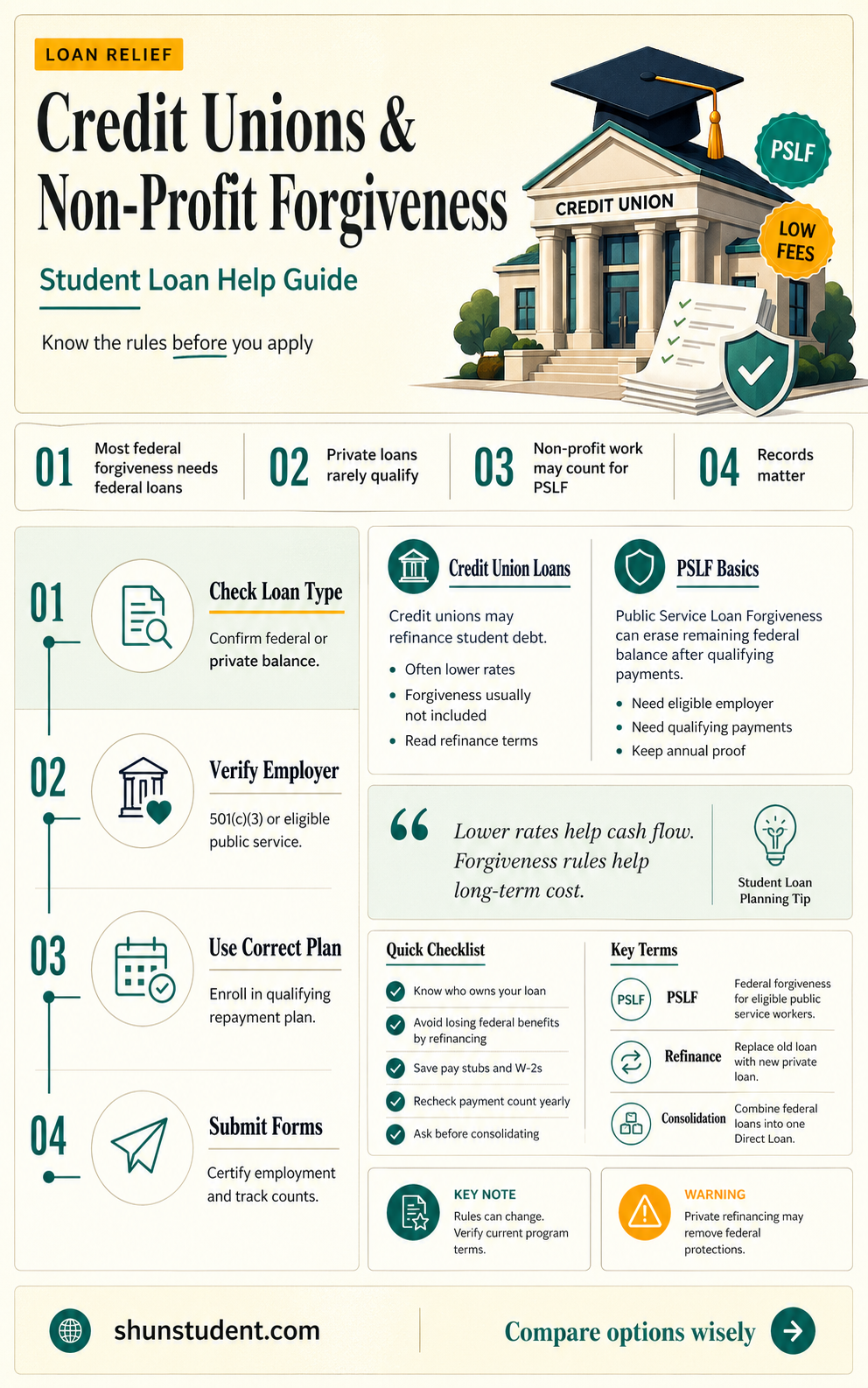

Credit unions, as nonprofit financial cooperatives, often offer unique benefits to their members, including competitive loan products and services. One area of interest is their role in student loan forgiveness programs, which aim to alleviate the burden of educational debt. Unlike traditional banks, credit unions operate with a member-focused mission, potentially making them more inclined to provide favorable terms or participate in forgiveness initiatives. However, the availability of such programs varies widely, as credit unions are not universally involved in student loan forgiveness. Understanding whether and how credit unions contribute to these efforts requires examining their individual policies, partnerships with government or nonprofit organizations, and commitment to supporting members' financial well-being.

| Characteristics | Values |

|---|---|

| Non-Profit Status | Credit unions are typically non-profit financial cooperatives. |

| Student Loan Forgiveness Programs | Credit unions do not directly offer federal student loan forgiveness. |

| Loan Refinancing Options | Some credit unions offer student loan refinancing with competitive rates. |

| Eligibility for Federal Forgiveness | Loans refinanced by credit unions may not qualify for federal forgiveness programs. |

| Community-Based Support | Credit unions may provide financial counseling and resources for borrowers. |

| Interest Rates | Often lower than traditional banks for refinancing. |

| Membership Requirement | Borrowers must be members of the credit union to access services. |

| Loan Servicing | Credit unions may service their own loans or partner with third parties. |

| Impact on Credit Score | Refinancing may temporarily impact credit score due to credit inquiries. |

| Availability of Programs | Limited compared to federal or specialized non-profit organizations. |

| Tax Benefits | Refinanced loans may not qualify for tax deductions available for federal loans. |

Explore related products

$6.99 $12.99

What You'll Learn

![]()

Credit union non-profit status

Credit unions, unlike traditional banks, operate as not-for-profit financial cooperatives, a status that fundamentally shapes their mission and operations. This non-profit structure means they are owned by their members, who are typically individuals sharing a common bond such as employment, community, or association. Profits generated by credit unions are returned to members in the form of lower loan rates, higher savings rates, and reduced fees, rather than distributed to external shareholders. This model aligns their interests with those of their members, fostering a more member-centric approach to financial services.

The non-profit status of credit unions has implications for student loan forgiveness programs, though it does not directly equate to automatic loan forgiveness. Credit unions are not inherently involved in administering federal student loan forgiveness programs, which are typically managed by government entities or designated loan servicers. However, their non-profit nature allows them to offer more favorable terms on private student loans, such as lower interest rates and flexible repayment options. For instance, some credit unions partner with organizations to provide refinancing options that reduce monthly payments or shorten loan terms, indirectly easing the burden of student debt.

One practical example of how credit unions leverage their non-profit status is through community-focused initiatives. For instance, a credit union might offer financial literacy workshops or one-on-one counseling to help members manage student debt effectively. These programs, often free or low-cost, empower borrowers to make informed decisions about repayment strategies, including exploring income-driven repayment plans or public service loan forgiveness. While not direct forgiveness, such support can significantly improve a borrower’s ability to navigate their debt.

It’s important to note that credit unions’ non-profit status does not exempt them from regulatory oversight or financial sustainability requirements. They must maintain sufficient capital and manage risk effectively to serve their members. This balance between mission and financial health sometimes limits their ability to offer large-scale forgiveness programs. Borrowers seeking relief should therefore approach credit unions with realistic expectations, focusing on refinancing opportunities or debt management assistance rather than expecting outright forgiveness.

In conclusion, while credit unions’ non-profit status does not directly translate to student loan forgiveness, it positions them as valuable allies for borrowers. Their member-focused model enables them to provide more affordable loan products and supportive services that can alleviate the strain of student debt. Borrowers should explore partnerships between credit unions and educational institutions or non-profits, as these collaborations often yield innovative solutions tailored to local needs. By understanding and leveraging these offerings, individuals can take proactive steps toward managing their student loans more effectively.

Unlock Debt-Free Future: Strategies for Student Loan Forgiveness Explained

You may want to see also

Explore related products

$36 $45

$18.98 $35

![]()

Student loan forgiveness programs

Credit unions, as nonprofit financial cooperatives, often offer unique benefits to their members, including potential advantages in student loan management. While they don’t directly administer federal student loan forgiveness programs, some credit unions partner with organizations or offer refinancing options that can reduce interest rates and monthly payments, indirectly easing the burden of student debt. For instance, programs like the Public Service Loan Forgiveness (PSLF) require specific federal loans, but credit unions can help members refinance private loans into more manageable terms, making it easier to qualify for forgiveness programs.

One practical strategy involves consolidating high-interest private loans through a credit union. By refinancing at a lower rate, borrowers can free up funds to make consistent payments toward federal loans eligible for forgiveness. For example, a borrower with a 7% private loan might refinance to 4% through a credit union, saving hundreds annually. These savings can then be directed toward income-driven repayment plans, which are prerequisites for programs like PSLF or income-driven forgiveness.

It’s crucial to note that not all credit unions offer student loan refinancing, and terms vary widely. Borrowers should compare offers carefully, considering factors like fixed vs. variable rates, repayment terms, and eligibility requirements. For instance, some credit unions require membership, which may involve a small fee or affiliation with a specific employer or community group. Additionally, refinancing federal loans into private ones eliminates access to federal forgiveness programs, so this step should be taken only if the borrower is ineligible for such programs or has a clear strategy to manage private debt.

A lesser-known benefit is that some credit unions provide financial literacy resources or counseling to help members navigate student loan forgiveness options. These services can clarify eligibility criteria, repayment plan options, and application processes, reducing the risk of errors that could delay forgiveness. For example, a credit union might host workshops on PSLF certification or income-driven repayment plan enrollment, ensuring members take full advantage of available programs.

In conclusion, while credit unions don’t directly offer nonprofit student loan forgiveness, their refinancing options and member-focused services can significantly support borrowers pursuing forgiveness. By strategically refinancing private loans and leveraging credit union resources, borrowers can align their finances to meet the requirements of federal forgiveness programs. Always consult with a financial advisor or loan specialist to ensure your strategy aligns with your long-term financial goals.

Understanding the 10k Student Loan Forgiveness Plan: What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Eligibility for credit union members

Credit union members often wonder if their membership opens doors to unique student loan forgiveness opportunities. While credit unions are not-for-profit financial cooperatives, their involvement in student loan forgiveness programs varies widely. Eligibility for such programs hinges on specific criteria, often tied to the credit union’s partnerships, member status, and the type of loan held. Understanding these nuances is crucial for members seeking relief from student debt.

To determine eligibility, start by verifying your membership status and tenure with the credit union. Many programs require a minimum membership period, typically six months to a year, to qualify for benefits. Next, assess the type of student loan you hold. Credit unions primarily offer private student loans, which are less likely to qualify for forgiveness compared to federal loans. However, some credit unions partner with organizations or government programs to provide forgiveness options for members in specific professions, such as teachers, nurses, or public servants.

Another critical factor is your employment sector. Credit unions often prioritize members working in public service or nonprofit roles for forgiveness programs. For instance, a credit union might offer partial loan forgiveness to members employed in education or healthcare after a set number of years. Additionally, income-based eligibility criteria may apply, with lower-income members receiving more substantial benefits. Always review the credit union’s specific program guidelines to understand these thresholds.

Practical steps to maximize eligibility include maintaining a strong financial relationship with your credit union. Regularly using their services, such as checking accounts, credit cards, or auto loans, can enhance your standing. Additionally, stay informed about new programs by subscribing to newsletters or attending member meetings. If your credit union doesn’t offer forgiveness programs, inquire about refinancing options to lower interest rates or consolidate debt, which can indirectly ease repayment burdens.

In conclusion, eligibility for credit union-based student loan forgiveness is not universal but depends on membership tenure, loan type, employment sector, and financial behavior. Proactive engagement with your credit union and thorough research into available programs are key to unlocking potential benefits. While not all members will qualify, those who meet specific criteria can find meaningful relief through these not-for-profit institutions.

Nonprofit Student Loan Forgiveness: Who Qualifies and How to Apply

You may want to see also

Explore related products

![]()

Differences from federal forgiveness

Credit unions, as nonprofit financial cooperatives, offer student loan forgiveness programs that differ significantly from federal options. Unlike federal programs, which are standardized and widely accessible, credit union forgiveness initiatives are often tailored to specific communities or membership criteria. For instance, a credit union might require borrowers to maintain an active account or reside in a particular geographic area to qualify. This localized approach contrasts with federal programs like Public Service Loan Forgiveness (PSLF), which are available nationwide to eligible public servants after 10 years of qualifying payments.

One key distinction lies in the funding and eligibility requirements. Federal forgiveness programs are backed by government resources and have clear, uniform guidelines. In contrast, credit union programs are typically funded through the institution’s own reserves or partnerships, leading to more varied eligibility criteria. For example, a credit union might forgive a portion of a loan after a borrower completes financial literacy courses or demonstrates consistent on-time payments. This flexibility can benefit borrowers who don’t meet federal program criteria but align with the credit union’s mission-driven goals.

Another difference is the scale and scope of forgiveness. Federal programs often offer full loan forgiveness after a set period, such as 20–25 years for income-driven repayment plans. Credit unions, however, may provide smaller, incremental forgiveness amounts, such as $1,000 annually for up to five years. While this may not eliminate the entire debt, it can significantly reduce the financial burden for borrowers. For instance, a borrower with $30,000 in debt could save thousands in interest by combining credit union forgiveness with regular payments.

Borrowers should also consider the application process and documentation. Federal programs require detailed paperwork, such as employment certification for PSLF, and may involve lengthy approval times. Credit unions often streamline this process, offering simpler applications and quicker decisions. However, borrowers must carefully review the terms, as some credit union programs may require ongoing membership or specific account activities to maintain eligibility.

In summary, while federal forgiveness programs provide broad, standardized relief, credit union options offer localized, mission-driven alternatives. Borrowers should assess their eligibility, the forgiveness amount, and program requirements to determine the best fit. Combining both approaches—leveraging federal programs for long-term relief and credit union initiatives for immediate savings—can maximize debt reduction strategies. Always consult with a financial advisor to tailor a plan to your unique circumstances.

Student Loan Forgiveness Application Timeline: When Can You Apply?

You may want to see also

Explore related products

![]()

Impact on credit scores

Credit unions, as nonprofit financial institutions, often offer student loan forgiveness programs that can significantly impact borrowers’ credit scores. Unlike traditional banks, credit unions prioritize member welfare over profit, which can lead to more flexible repayment terms and forgiveness options. When a borrower enrolls in a credit union’s forgiveness program, the way their student loan is reported to credit bureaus can change. For instance, if the program reduces the principal balance or marks the loan as “paid in full” ahead of schedule, this positive update can boost the borrower’s credit score by lowering their credit utilization ratio and demonstrating responsible financial management.

However, the impact isn’t always straightforward. Some forgiveness programs may temporarily lower a credit score if the loan is reclassified or removed from the credit report entirely. This occurs because the credit mix—one of the factors influencing credit scores—may shift if the student loan was the borrower’s only installment account. Additionally, if the forgiveness process involves a settlement for less than the full amount owed, it could be reported as a negative mark, similar to a partial payment, which can harm the credit score. Borrowers should carefully review the terms of any forgiveness program to understand how it will be reported to credit bureaus.

To maximize the positive impact on credit scores, borrowers should ensure their credit union reports forgiven loans as “paid as agreed” rather than “settled” or “forgiven.” This distinction is crucial because “paid as agreed” reflects fulfillment of the original loan terms, even if the balance was reduced through a nonprofit program. Borrowers can also request a detailed payoff letter from the credit union to provide to credit bureaus if discrepancies arise. Proactive communication with both the credit union and credit bureaus can prevent reporting errors that might unfairly penalize the borrower’s score.

Another practical tip is to maintain other credit accounts in good standing during the forgiveness process. For example, keeping credit card balances below 30% of their limits and making timely payments on other loans can offset any temporary dip caused by changes to the student loan account. Borrowers should also monitor their credit reports regularly using free services like AnnualCreditReport.com to catch and dispute inaccuracies promptly. By combining forgiveness programs with disciplined credit management, borrowers can not only eliminate student debt but also strengthen their overall credit profile.

Capella Student Loan Forgiveness: Steps to Erase Your Debt

You may want to see also

Frequently asked questions

Yes, credit unions are typically non-profit financial cooperatives owned and operated by their members, not shareholders.

Credit unions do not directly offer student loan forgiveness programs, as these are typically government or employer-based initiatives.

Yes, many credit unions offer student loan refinancing or consolidation options, which may lower interest rates or monthly payments but do not equate to loan forgiveness.

Credit unions may offer lower interest rates, personalized service, and financial education resources, but they do not provide non-profit-specific student loan forgiveness programs.