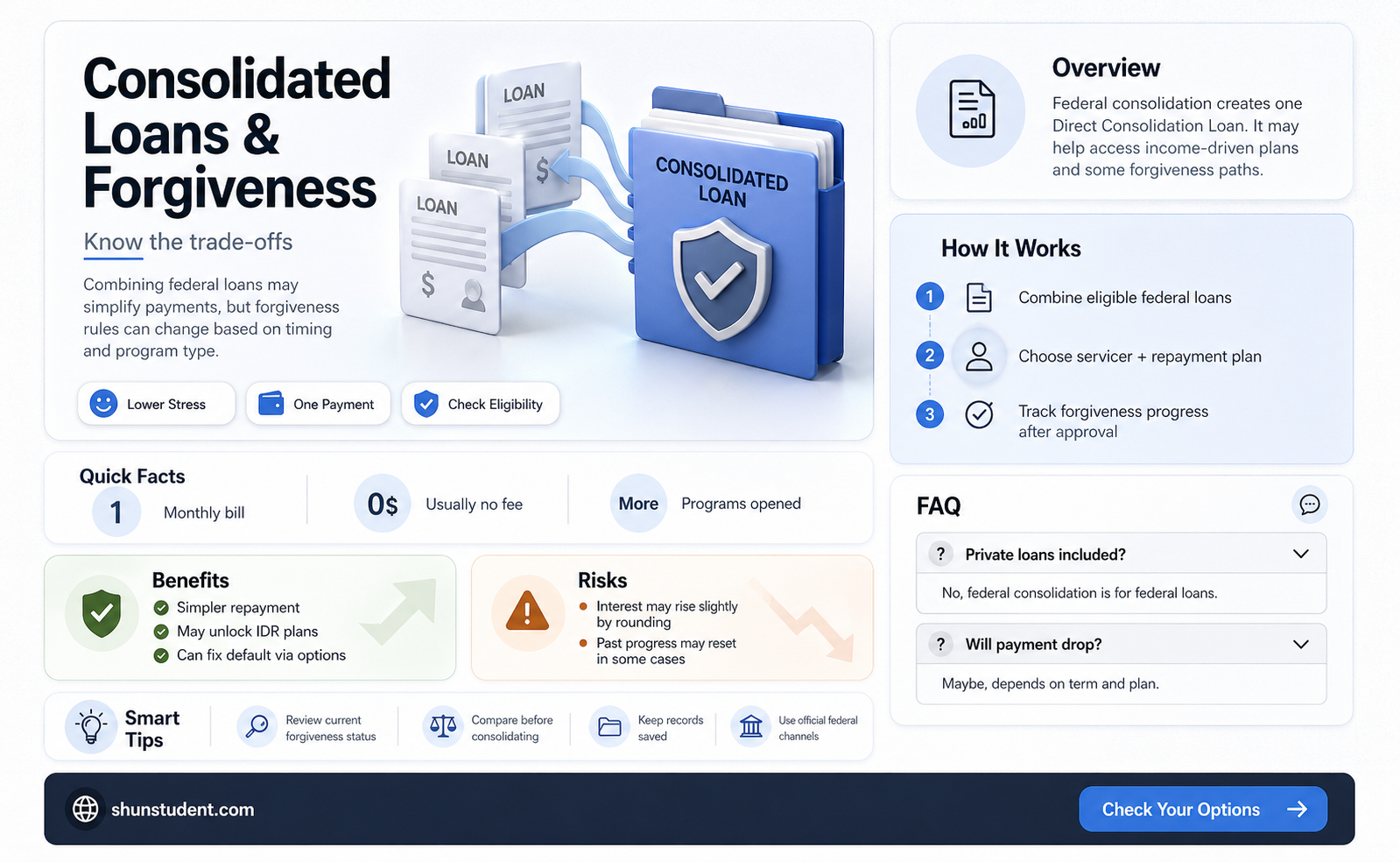

Consolidated loans, which combine multiple student loans into a single payment, are a popular option for borrowers seeking to simplify their repayment process. However, a common concern among borrowers is whether these consolidated loans remain eligible for student loan forgiveness programs. The answer largely depends on the type of consolidation and the specific forgiveness program in question. Federal Direct Consolidation Loans, for instance, are generally eligible for income-driven repayment (IDR) plans and Public Service Loan Forgiveness (PSLF), provided the underlying loans were eligible. Conversely, private consolidation loans typically do not qualify for federal forgiveness programs. Borrowers must carefully review the terms of both their consolidation and the forgiveness program to ensure continued eligibility, as consolidating can sometimes reset the clock on forgiveness timelines or disqualify certain loans from consideration.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Consolidated loans are generally eligible for student loan forgiveness programs, but eligibility depends on the type of consolidation and forgiveness program. |

| Federal Direct Consolidation Loans | Eligible for programs like Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) Forgiveness, and Temporary Expanded PSLF (TEPSLF). |

| Private Loan Consolidation | Not eligible for federal student loan forgiveness programs. Private consolidation refinances loans into a single private loan. |

| FFEL or Perkins Loans Consolidated | Must be consolidated into a Federal Direct Consolidation Loan to qualify for PSLF or IDR Forgiveness. |

| Impact on Payment Count | Consolidation resets the qualifying payment count for PSLF and IDR Forgiveness, unless consolidated under TEPSLF rules. |

| Interest Rates | Consolidated loans have a fixed rate based on the weighted average of the original loans, rounded up to the nearest one-eighth of 1%. |

| Repayment Plans | Access to income-driven repayment plans, which are required for IDR Forgiveness. |

| Temporary Expanded PSLF (TEPSLF) | Allows previously ineligible payments (e.g., FFEL or non-IDR payments) to count toward forgiveness if consolidated by Oct. 31, 2023. |

| One-Time Account Adjustment | Consolidated loans may benefit from the one-time account adjustment to count past payments toward IDR or PSLF forgiveness. |

| Loan Servicer | Consolidated loans are typically serviced by federal loan servicers, ensuring compliance with forgiveness program requirements. |

| Tax Implications | Forgiveness of consolidated loans may be tax-free under certain programs (e.g., PSLF, IDR Forgiveness). |

| Current Policy (as of 2023) | Consolidated loans remain eligible for forgiveness, but borrowers must meet specific program requirements. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Consolidated Loans

Consolidated loans, when managed correctly, can still qualify for student loan forgiveness programs, but the eligibility criteria are stringent and often misunderstood. The first critical factor is the type of loans being consolidated. Federal student loans, such as Direct Loans, Stafford Loans, and PLUS Loans, are eligible for consolidation under the Direct Consolidation Loan program, which retains access to forgiveness options like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness. However, private loans consolidated through private lenders are typically ineligible for federal forgiveness programs. Borrowers must ensure their consolidation strategy aligns with their long-term forgiveness goals.

Another key criterion is the timing of consolidation. For PSLF, for instance, payments made on consolidated loans only count toward the required 120 qualifying payments if the consolidation is done before applying for forgiveness. Consolidating after making payments on unconsolidated loans may reset the payment counter, delaying eligibility. Similarly, borrowers pursuing IDR forgiveness must understand that consolidating can affect their payment history, potentially extending the forgiveness timeline. Strategic timing is essential to maximize eligibility without inadvertently resetting progress.

The repayment plan chosen after consolidation also plays a pivotal role. Consolidated loans must be repaid under an eligible plan, such as an IDR plan, to qualify for forgiveness. Standard repayment plans, which often have higher monthly payments, do not qualify for forgiveness unless the borrower switches to an IDR plan. Borrowers should carefully evaluate their financial situation and choose a plan that balances affordability with forgiveness eligibility. For example, switching to an IDR plan like REPAYE or PAYE can lower monthly payments and align with forgiveness requirements.

Lastly, employment and certification requirements remain unchanged for consolidated loans. Borrowers pursuing PSLF must still work full-time for a qualifying employer, such as a government or nonprofit organization, and submit Employment Certification Forms regularly. Consolidated loans do not exempt borrowers from these obligations; they simply streamline multiple loans into one payment. Maintaining accurate records and staying compliant with program rules is crucial to ensuring eligibility for forgiveness after consolidation.

In summary, consolidated loans remain eligible for student loan forgiveness, but borrowers must navigate specific criteria to preserve their eligibility. By consolidating federal loans, timing the consolidation strategically, enrolling in an eligible repayment plan, and meeting ongoing employment requirements, borrowers can position themselves to benefit from forgiveness programs. Careful planning and adherence to program rules are essential to avoid pitfalls and achieve debt relief.

Can DeVry Student Loans Be Forgiven? Exploring Your Options

You may want to see also

Explore related products

![]()

Types of Forgiveness Programs Available

Consolidated student loans remain eligible for forgiveness under specific programs, but the type of forgiveness available depends on the program’s criteria and the borrower’s circumstances. Understanding the landscape of forgiveness programs is crucial for maximizing relief. Here’s a breakdown of the key options.

Public Service Loan Forgiveness (PSLF) stands out as one of the most accessible programs for consolidated loans. To qualify, borrowers must make 120 eligible payments while working full-time for a government or nonprofit organization. Consolidation is not only allowed but often necessary, as only Direct Loans are eligible for PSLF. Borrowers with Federal Family Education Loans (FFEL) or Perkins Loans must consolidate into a Direct Consolidation Loan to qualify. A critical tip: ensure your employer certifies your employment annually to avoid disqualification.

Income-Driven Repayment (IDR) Forgiveness is another pathway, particularly for borrowers with high debt relative to their income. Programs like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) offer forgiveness after 20–25 years of qualifying payments. Consolidated loans are eligible, but the clock resets on the forgiveness timeline. For example, if you’ve already made 5 years of payments under IBR and then consolidate, you’ll start anew. Pro tip: Recertify your income annually to maintain eligibility and avoid payment increases.

Teacher Loan Forgiveness provides up to $17,500 in relief for educators working in low-income schools. Consolidated loans are eligible, but only if they include Direct Subsidized or Unsubsidized Loans. FFEL or Perkins Loans must be consolidated into a Direct Loan first. Eligibility requires five consecutive years of teaching, and the amount forgiven varies by subject taught. For instance, secondary math and science teachers qualify for the full $17,500, while elementary teachers receive up to $5,000.

Perkins Loan Cancellation is a lesser-known but valuable option for borrowers with consolidated Perkins Loans. Forgiveness is available for teachers, nurses, law enforcement officers, and other public service roles. Cancellation occurs incrementally, with 100% forgiveness after five years of service. However, Perkins Loans must be consolidated into a Direct Consolidation Loan to qualify for other forgiveness programs like PSLF. Caution: Consolidating resets the cancellation timeline, so weigh the trade-offs carefully.

In summary, consolidated loans retain eligibility for forgiveness, but the process varies by program. Borrowers must navigate specific requirements, such as loan type, repayment plan, and employment certification, to maximize their chances of relief. Strategic planning, such as consolidating FFEL or Perkins Loans into Direct Loans, can open doors to programs like PSLF or IDR forgiveness. Always consult official resources or a loan servicer to ensure compliance with program rules.

Unlock $10K Student Loan Forgiveness: Your Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Impact of Consolidation on Forgiveness

Consolidating student loans can significantly impact eligibility for forgiveness programs, but the effects vary depending on the type of consolidation and forgiveness plan. Federal Direct Consolidation Loans, for instance, can simplify repayment by combining multiple federal loans into one, but they reset the clock on forgiveness timelines for income-driven repayment (IDR) plans. This means any qualifying payments made before consolidation no longer count toward the 20- or 25-year forgiveness threshold. Borrowers pursuing Public Service Loan Forgiveness (PSLF) must also note that consolidation is required if they have Federal Family Education Loans (FFEL) or Perkins Loans, as only Direct Loans qualify for PSLF. However, consolidating resets payment counts for PSLF as well, unless borrowers have already made significant progress toward the 120 required payments.

For borrowers on IDR plans, consolidating can be a double-edged sword. While it streamlines multiple loans into a single payment, it may increase the total interest paid over time, especially if higher-interest loans are combined. Additionally, consolidating Parent PLUS Loans with other federal loans can make them eligible for IDR plans, but this move disqualifies them from PSLF unless the borrower is also pursuing public service. Borrowers must weigh these trade-offs carefully, as consolidation can both open doors to forgiveness and inadvertently delay it.

A lesser-known but critical detail is how consolidation affects loan forgiveness under the one-time adjustment initiative. This temporary program, introduced in 2022, allows the Department of Education to retroactively count certain periods (like time spent in forbearance) toward IDR and PSLF forgiveness. Consolidated loans are eligible for this adjustment, but borrowers must ensure their consolidation is processed before the program’s deadline. Failure to consolidate in time could exclude them from this opportunity, potentially costing years of progress toward forgiveness.

Practical steps for borrowers include reviewing their loan types and repayment histories before consolidating. Those close to the forgiveness threshold on an IDR plan may benefit from avoiding consolidation altogether, while those with FFEL or Perkins Loans seeking PSLF should consolidate immediately to qualify. Borrowers should also consult the Federal Student Aid website or a loan servicer to model how consolidation will affect their forgiveness timeline. For example, a borrower with 10 years of qualifying PSLF payments on FFEL Loans should consolidate into a Direct Loan to ensure those payments count toward the 120 required.

In conclusion, consolidation’s impact on student loan forgiveness hinges on strategic timing and program specifics. While it can simplify repayment and unlock eligibility for certain plans, it often resets progress toward forgiveness, requiring careful consideration. Borrowers must align consolidation with their long-term goals, leveraging tools like the one-time adjustment to maximize benefits. By understanding these nuances, they can navigate the complex intersection of consolidation and forgiveness effectively.

Can the President Legally Cancel Student Debt? Exploring Authority Limits

You may want to see also

Explore related products

![Special report from the Select committee on the public works loans acts amendment bill and public works loans acts consolidation bill, consolidated into the public works loans bill; to [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Public Service Loan Forgiveness (PSLF) Rules

Consolidated loans can indeed remain eligible for student loan forgiveness under the Public Service Loan Forgiveness (PSLF) program, but the process requires careful navigation. The PSLF program forgives the remaining balance on Direct Loans after 120 qualifying payments for borrowers employed full-time in eligible public service jobs. However, not all consolidated loans automatically qualify. Only Direct Consolidation Loans are eligible for PSLF; Federal Family Education Loans (FFEL) or Perkins Loans must be consolidated into the Direct Loan program to qualify. This critical step ensures that previously ineligible loans can now count toward forgiveness.

To maximize PSLF eligibility, borrowers must follow specific steps. First, confirm your employment qualifies as public service by submitting the Employment Certification Form (ECF) annually or whenever you change employers. This ensures your payments are tracked correctly. Second, consolidate any non-Direct Loans into a Direct Consolidation Loan through the federal student aid website. Note that consolidating resets the payment count, so time your consolidation strategically to avoid losing progress. Finally, enroll in an income-driven repayment (IDR) plan to lower monthly payments and align with PSLF requirements.

A common pitfall is assuming all payments made before consolidation count toward PSLF. In reality, only payments made *after* consolidating into a Direct Loan qualify. For example, if you made 60 payments on a FFEL loan before consolidating, those payments do not count. Start your 120 qualifying payments only after consolidation and while working in public service. This clarity prevents delays in forgiveness eligibility.

The PSLF program also requires borrowers to remain in public service throughout the repayment period. Switching to a non-qualifying employer mid-repayment can disqualify you. Use the ECF to verify eligibility annually and maintain records of all payments and employment certifications. Additionally, monitor your loan servicer’s accuracy; errors in payment counts are common. By staying proactive and informed, borrowers can ensure their consolidated loans remain on track for PSLF forgiveness.

Can Nonprofit Work Erase Student Debt? Exploring Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plan Compatibility

Consolidated loans can indeed remain eligible for student loan forgiveness, but the compatibility with Income-Driven Repayment (IDR) plans is a critical factor. IDR plans, such as Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), tie monthly payments to income and family size, offering a pathway to forgiveness after 20 or 25 years of qualifying payments. When consolidating loans, borrowers must understand how this process interacts with IDR eligibility to maximize their chances of forgiveness.

Step 1: Assess Your Loan Types Before Consolidation

Federal student loans, including Direct Loans and FFEL Loans, are eligible for IDR plans. However, consolidating loans through the federal Direct Consolidation Loan program is often necessary to combine multiple loans into a single payment. If you have older FFEL or Perkins Loans, consolidation can make them eligible for IDR plans and Public Service Loan Forgiveness (PSLF). Private loans, however, cannot be consolidated into the federal program and are ineligible for IDR plans or forgiveness. Always verify your loan types using the National Student Loan Data System (NSLDS) before proceeding.

Caution: Payment Count Reset

Consolidating loans resets the qualifying payment count for forgiveness under IDR plans. For example, if you’ve made 5 years of payments toward the 20 or 25-year forgiveness threshold, consolidating will restart the clock. This trade-off may be worthwhile if consolidation simplifies repayment or makes previously ineligible loans eligible for IDR. However, borrowers nearing forgiveness should weigh the benefits carefully to avoid delaying their forgiveness timeline.

Tip: Choose the Right IDR Plan Post-Consolidation

After consolidating, select an IDR plan that aligns with your financial goals. For instance, REPAYE caps monthly payments at 10% of discretionary income and offers interest subsidies, making it ideal for borrowers with high debt-to-income ratios. Conversely, PAYE limits payments to 10% of discretionary income but requires proof of financial hardship. Use the Federal Student Aid Loan Simulator to estimate payments and forgiveness timelines under each plan before committing.

Consolidation can enhance IDR compatibility, but it requires careful planning. By consolidating strategically, borrowers can streamline repayment, access IDR benefits, and maintain eligibility for forgiveness. Always consult a loan servicer or financial advisor to evaluate your unique situation and ensure consolidation aligns with your long-term financial goals. With the right approach, consolidated loans can remain a viable path to student loan forgiveness.

Should You Apply for Student Loan Forgiveness? A Quick Guide

You may want to see also

Frequently asked questions

Yes, consolidated loans are still eligible for student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness, as long as the underlying loans were eligible federal student loans.

Consolidating loans can reset your payment count toward forgiveness programs like PSLF or IDR. However, if you’re pursuing PSLF, you can submit an Employer Certification Form to count previous qualifying payments made before consolidation.

No, private loans cannot be consolidated into a federal Direct Consolidation Loan to become eligible for federal student loan forgiveness programs. Only federal loans can be consolidated for forgiveness purposes.

Yes, federal Direct Consolidation Loans are eligible for forgiveness programs like PSLF and IDR forgiveness. However, the terms and eligibility criteria of the underlying loans (e.g., Stafford, Perkins, or Direct Loans) still apply after consolidation.