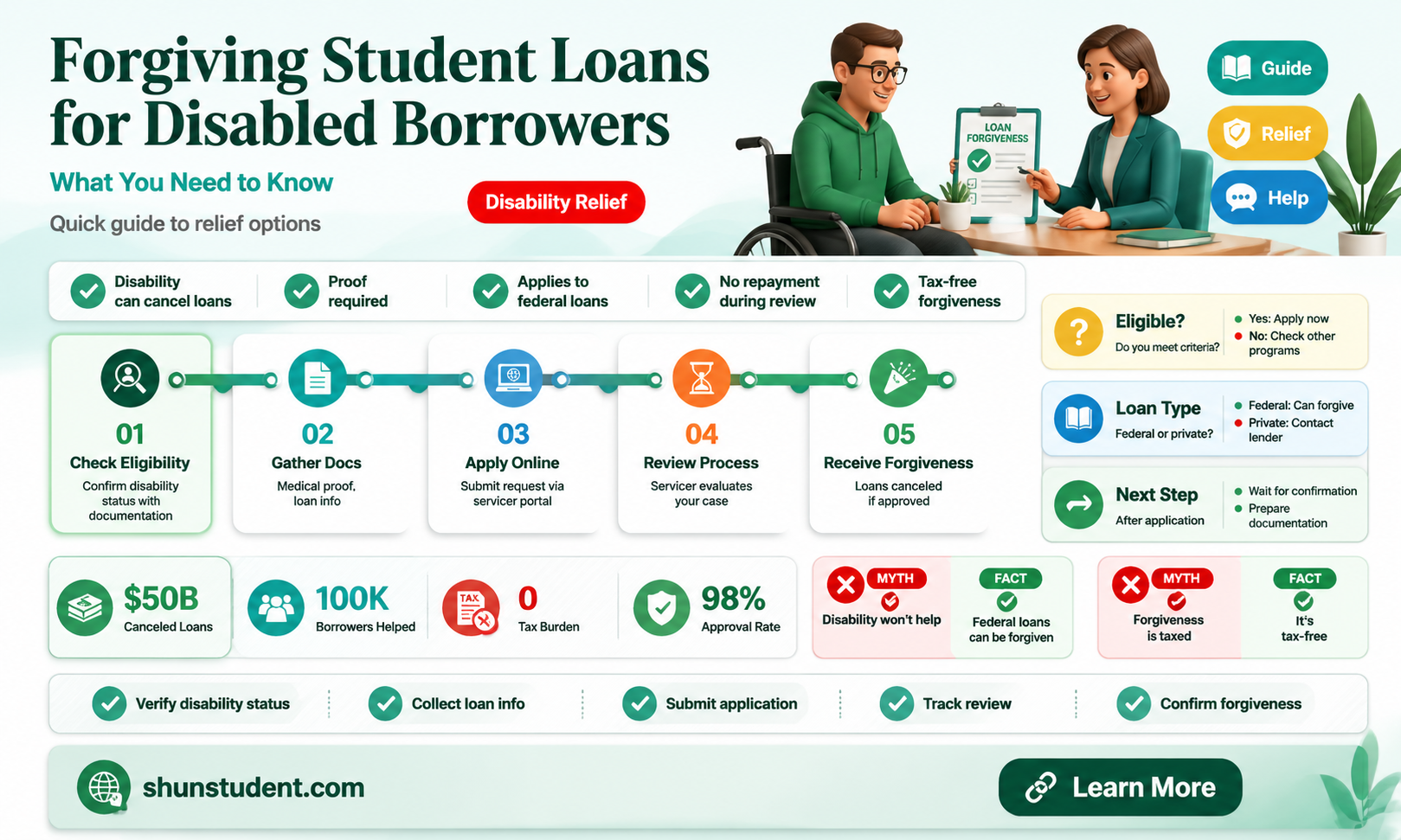

The question of whether disabled students are forgiven student loans is a critical issue that intersects education policy, disability rights, and financial equity. Many countries, including the United States, have implemented programs such as Total and Permanent Disability (TPD) discharge, which allow eligible individuals with significant disabilities to have their federal student loans forgiven. These initiatives aim to alleviate the financial burden on disabled borrowers who face substantial barriers to employment and economic stability. However, the process often requires rigorous documentation and can be challenging to navigate, leaving some disabled individuals unaware of their eligibility or unable to access relief. Additionally, disparities exist in the availability of such programs across different regions and loan types, raising concerns about inclusivity and fairness. As the conversation around student debt forgiveness continues to evolve, addressing the unique needs of disabled students remains a vital component of ensuring equitable access to financial relief.

| Characteristics | Values |

|---|---|

| Eligibility Criteria | Total and Permanent Disability (TPD) as certified by a physician, Veteran Affairs, or Social Security Administration. |

| Loan Types Covered | Federal student loans (Direct Loans, FFEL, Perkins Loans) and TEACH Grants (in certain cases). |

| Application Process | Submit a TPD discharge application with supporting documentation to the U.S. Department of Education. |

| Documentation Required | Proof of disability from a physician, VA, or SSA; no tax return required if using SSA data. |

| Automatic Discharge | Automatic for recipients of SSA disability benefits or VA disability rating of 100% P&T. |

| Monitoring Period | 3-year post-approval monitoring period for earned income and new federal loans/TEACH Grants. |

| Tax Implications | Loan discharge may be considered taxable income (check IRS guidelines). |

| Impact on Credit Score | Discharged loans are removed from credit reports and do not negatively impact credit. |

| Private Loan Eligibility | Private student loans are not eligible for federal TPD discharge. |

| Reinstatement of Loans | Loans may be reinstated if monitoring period conditions are violated. |

| Current Policy (as of 2023) | Streamlined process for SSA recipients; expanded eligibility for VA beneficiaries. |

| Pending Changes | Proposed reforms to simplify the process and reduce monitoring period burdens. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Loan Forgiveness

In the United States, disabled students may qualify for Total and Permanent Disability (TPD) discharge, a federal program that forgives federal student loans for borrowers who can no longer work due to a permanent disability. To be eligible, borrowers must meet specific criteria, including providing documentation from a physician, the Social Security Administration (SSA), or the U.S. Department of Veterans Affairs (VA). This process requires careful attention to detail, as incomplete applications are often rejected.

Documentation Requirements: The Key to Unlocking Forgiveness

Borrowers pursuing TPD discharge must submit comprehensive documentation to prove their disability. For SSA recipients, this involves granting permission to share disability information with the loan servicer. Alternatively, borrowers can submit a certification from a physician, detailing the nature and duration of the disability. VA recipients must provide documentation confirming their disability rating. Ensuring all required forms are complete and accurate is crucial, as errors can delay or derail the application process.

Navigating the Application Process: A Step-by-Step Guide

To initiate the TPD discharge process, borrowers should first contact their loan servicer or visit the official government website for disability discharge. The application typically involves three monitoring periods, during which borrowers must confirm their income and employment status. Failure to comply with these requirements may result in loan reinstatement. It’s essential to keep detailed records and respond promptly to any requests for additional information.

Common Pitfalls to Avoid: Lessons from Real-World Cases

Many applicants face challenges due to misunderstandings about eligibility or incomplete documentation. For instance, borrowers who return to work during the monitoring period may jeopardize their discharge. Similarly, failing to update contact information can lead to missed notifications. A notable example is the case of a borrower whose discharge was revoked after they exceeded income limits during the third monitoring period. Such scenarios underscore the importance of strict adherence to program guidelines.

Maximizing Your Chances: Practical Tips for Success

To enhance the likelihood of approval, borrowers should gather all necessary documents before applying and double-check their accuracy. Seeking assistance from disability advocates or legal aid organizations can provide valuable support. Additionally, maintaining open communication with loan servicers and staying informed about program updates are critical steps. By approaching the process systematically and proactively, disabled borrowers can navigate the complexities of TPD discharge more effectively.

Student Loan Forgiveness in Sallie Mae: What You Need to Know

You may want to see also

Explore related products

![]()

Types of Disabilities Qualifying for Forgiveness

Student loan forgiveness for disabled borrowers is a critical yet often misunderstood benefit. To qualify, the U.S. Department of Education requires documentation of a total and permanent disability (TPD), defined as the inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. This definition is stringent, but it opens the door for individuals with a range of disabilities to seek relief from federal student loan debt. Understanding which disabilities qualify is the first step toward accessing this life-changing program.

Physical disabilities that meet the TPD criteria often include severe conditions such as advanced-stage cancers, end-stage renal disease requiring dialysis, or paralysis resulting from spinal cord injuries. For example, a borrower with amyotrophic lateral sclerosis (ALS) would likely qualify, as the disease’s progressive nature aligns with the 60-month requirement. Similarly, individuals with severe multiple sclerosis or cerebral palsy may be eligible if their conditions prevent them from working. Documentation typically requires a physician’s certification confirming the disability’s severity and expected duration.

Mental health disabilities also qualify if they meet the TPD standard. Conditions like schizophrenia, severe bipolar disorder, or major depressive disorder with psychotic features can render individuals unable to maintain employment. For instance, a borrower with treatment-resistant schizophrenia, supported by a psychiatrist’s diagnosis and treatment history, could apply for forgiveness. However, milder forms of mental health conditions, even if chronic, may not meet the threshold unless they demonstrably prevent substantial gainful activity.

Intellectual disabilities and neurodevelopmental disorders are another category eligible for forgiveness. Borrowers with Down syndrome, severe autism spectrum disorder, or intellectual disabilities documented by IQ testing and adaptive functioning assessments may qualify. For example, an individual with an IQ below 70 and significant deficits in daily living skills could submit evidence from a licensed psychologist or physician. The key is proving the disability’s permanence and its impact on employability.

Finally, degenerative conditions that worsen over time, such as Parkinson’s disease or Huntington’s disease, often meet the TPD criteria. These disabilities are inherently progressive, making it easier to demonstrate their long-term impact. Borrowers with such conditions should provide medical records showing diagnosis, progression, and functional limitations. Practical tips include keeping detailed medical documentation and applying for Social Security Disability Insurance (SSDI) first, as approval automatically qualifies for TPD discharge.

In summary, qualifying disabilities span physical, mental, intellectual, and degenerative conditions, but the burden of proof lies with the borrower. Accurate, comprehensive documentation is essential, and leveraging existing SSDI or Veterans Affairs disability determinations can streamline the process. For disabled borrowers, this forgiveness program offers not just financial relief but a chance to rebuild without the weight of student debt.

Can Consolidated Loans Be Forgiven Under Student Loan Forgiveness Programs?

You may want to see also

Explore related products

![]()

Application Process for Disabled Students

Disabled students seeking loan forgiveness face a labyrinthine application process that demands precision and patience. The first step involves verifying eligibility under the Total and Permanent Disability (TPD) discharge program, which requires proof of a physical or mental impairment expected to result in death, last for a continuous period of at least 60 months, or prevent substantial gainful activity. Documentation must come from a physician, the Social Security Administration (SSA), or the U.S. Department of Veterans Affairs (VA). For instance, SSA recipients must provide a Benefits Planning Query (BPQY) or a Notice of Award letter, while VA beneficiaries need a certification of 100% disability.

Once eligibility is confirmed, the application itself is deceptively straightforward but fraught with potential pitfalls. Applicants must complete the TPD discharge application form, available on the Federal Student Aid website, and submit it via mail or online. Crucially, the form requires detailed personal information, including loan account numbers and contact details. A common mistake is incomplete documentation, which can delay or derail the process. For example, failing to include the physician’s certification form with the correct medical language can result in rejection.

After submission, the waiting game begins. The U.S. Department of Education reviews applications within 4–6 weeks, but processing times can extend due to backlogs or errors. During this period, applicants are placed in a three-year monitoring period if approved preliminarily. This phase prohibits earning above the poverty guideline threshold, taking new federal student loans, or receiving educational benefits like Pell Grants. Violating these conditions can reinstate the debt, making vigilance essential.

A lesser-known but critical aspect is the role of loan servicers. While the Department of Education handles the application, servicers like Nelnet or MOHELA manage communication and monitoring. Applicants should maintain records of all correspondence and follow up regularly to ensure their case isn’t overlooked. For instance, if a physician’s form is lost, immediate resubmission with proof of delivery can prevent unnecessary delays.

Finally, approved applicants must navigate post-discharge complexities. Taxes on forgiven amounts were waived under the American Rescue Act through 2025, but future tax implications remain uncertain. Additionally, discharged loans may reappear if monitoring period conditions are violated. Practical tips include setting calendar reminders for annual income verification and consulting a tax professional to plan for potential liabilities. This process, while daunting, offers a lifeline to disabled borrowers—but only with meticulous attention to detail.

Canada Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Impact of Loan Forgiveness on Credit Scores

Loan forgiveness for disabled students, while a financial relief, often leaves individuals wondering about its ripple effects on their credit scores. The assumption that debt erasure equates to credit score improvement is a common misconception. In reality, the impact is nuanced, influenced by how the forgiveness is reported to credit bureaus and the individual’s overall credit profile. For instance, if a loan is marked as "paid as agreed" after forgiveness, it may have a neutral or slightly positive effect. However, if it’s reported as "settled" or "forgiven," it could signal financial hardship to lenders, potentially lowering the score temporarily.

Consider the mechanics of credit scoring models like FICO or VantageScore. These systems weigh factors such as payment history, credit utilization, and types of credit. Loan forgiveness typically removes the debt obligation but doesn’t erase the account’s history. If the borrower had a record of on-time payments before the disability discharge, that positive history remains intact, bolstering the score. Conversely, if the account was delinquent prior to forgiveness, the negative marks stay on the report for up to seven years, overshadowing the relief provided by the discharge.

Practical steps can mitigate potential downsides. First, verify how the forgiven loan is reported on your credit report. Disputing inaccurate reporting—such as a loan marked as "defaulted" instead of "paid as agreed"—can prevent unnecessary score damage. Second, maintain other credit accounts responsibly. Regular, on-time payments on credit cards or other loans can offset any minor negative impact from the forgiven student loan. Third, monitor your credit score regularly using free tools like AnnualCreditReport.com to track changes and address issues promptly.

A comparative analysis reveals that loan forgiveness for disabled students differs from other forms of debt relief, such as bankruptcy or debt settlement. Bankruptcy, for example, can drop a credit score by 150–250 points and remains on the report for up to 10 years. In contrast, disability-based loan forgiveness is less severe, often resulting in a minor dip or no change if managed correctly. However, unlike bankruptcy, it doesn’t provide a fresh financial start; it merely removes one obligation while preserving the credit history associated with the account.

In conclusion, the impact of loan forgiveness on credit scores for disabled students is not uniform but depends on reporting accuracy, pre-existing credit behavior, and post-forgiveness financial management. While the relief itself doesn’t guarantee a higher score, proactive steps can minimize adverse effects. Understanding these dynamics empowers borrowers to navigate their financial futures with clarity and confidence, ensuring that loan forgiveness serves as a stepping stone rather than a stumbling block.

When Do Forgiven Student Loans Disappear from Your Credit Report?

You may want to see also

Explore related products

$12.95 $22.99

![]()

Federal vs. Private Loan Forgiveness Programs

Disabled students seeking loan forgiveness face a stark divide between federal and private programs. Federal initiatives, such as the Total and Permanent Disability (TPD) Discharge, offer a clear pathway to relief. To qualify, borrowers must provide documentation of their disability from the Social Security Administration, the Department of Veterans Affairs, or a physician. Once approved, federal loans are fully discharged, and borrowers are no longer obligated to repay the debt. This program is a lifeline for many, as it eliminates the financial burden without tax penalties, thanks to recent legislative changes.

Private lenders, however, operate under no such mandate. While some private loan servicers may offer disability discharge options, they are far less standardized and often more restrictive. Borrowers typically need to prove a severe, permanent disability that prevents them from working, and even then, approval is not guaranteed. Unlike federal programs, private loan forgiveness may come with tax implications, as the discharged amount could be considered taxable income. This disparity underscores the importance of scrutinizing loan terms before borrowing and prioritizing federal aid when possible.

For those navigating this landscape, a strategic approach is essential. First, exhaust federal loan options before considering private loans, as federal programs provide more robust protections. Second, maintain thorough documentation of your disability status, as this will streamline the application process for TPD Discharge. Third, if private loans are unavoidable, negotiate terms upfront or seek lenders that explicitly offer disability discharge provisions. Finally, consult with a financial advisor or disability advocate to explore all available options and avoid pitfalls.

The contrast between federal and private loan forgiveness programs highlights a broader issue: the uneven safety net for disabled borrowers. While federal initiatives have made significant strides in recent years, private lenders lag behind, leaving many vulnerable. Advocacy for standardized private loan discharge policies is crucial to ensure equitable treatment for all disabled students. Until then, borrowers must remain vigilant, informed, and proactive in managing their debt.

Minnesota's Tax Rules on Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

No, not all disabled students are automatically forgiven their student loans. However, individuals with a total and permanent disability (TPD) may qualify for a Total and Permanent Disability (TPD) discharge, which forgives federal student loans.

To apply for a TPD discharge, you must submit an application to the U.S. Department of Education, providing documentation of your disability from a physician, the Social Security Administration (SSA), or the Department of Veterans Affairs (VA).

Private student loans are not eligible for federal TPD discharge. However, some private lenders may offer disability-related loan forgiveness or assistance programs, so it’s worth contacting your lender directly.

A TPD discharge does not negatively impact your credit score. However, the forgiven amount may be considered taxable income unless you qualify for an exception under the American Rescue Plan Act of 2021.

If you receive a TPD discharge and later recover, you must notify the Department of Education. There is a three-year monitoring period during which you must meet certain conditions; failure to do so may result in the reinstatement of your loans.