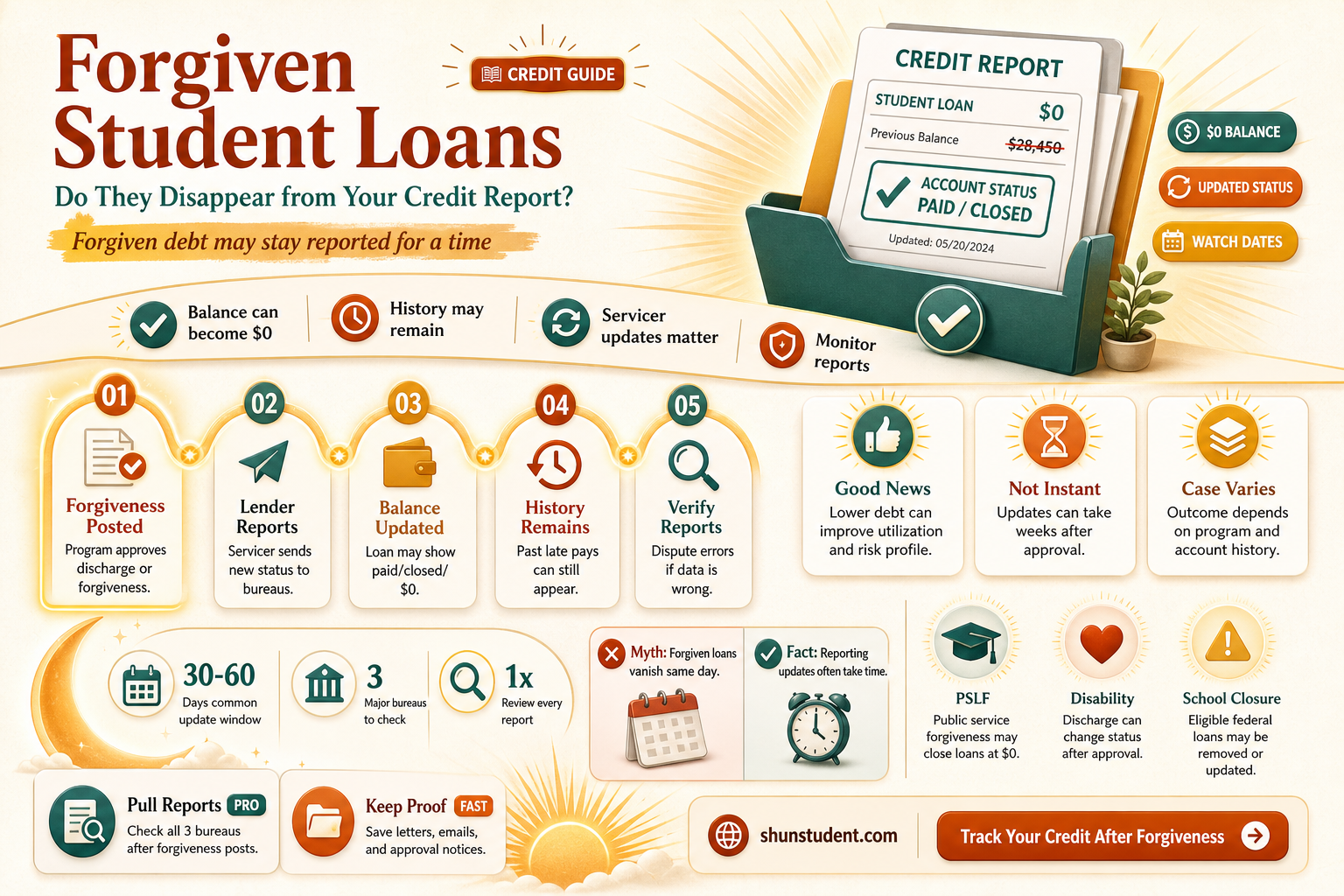

The question of whether forgiven student loans are removed from credit reports is a critical concern for many borrowers navigating the complexities of student loan forgiveness programs. When a student loan is forgiven, it means the borrower is no longer obligated to repay the debt, often due to meeting specific criteria such as public service, income-driven repayment plans, or other qualifying circumstances. However, the impact of this forgiveness on one’s credit report is not always straightforward. While the loan balance is eliminated, the way it is reported to credit bureaus can vary depending on the type of forgiveness and the lender’s policies. Some forgiven loans may remain on the credit report but are updated to reflect a $0 balance and a status of paid in full or settled, which may still influence credit scores. Understanding these nuances is essential for borrowers seeking to manage their financial health and ensure their credit reports accurately reflect their debt status after loan forgiveness.

| Characteristics | Values |

|---|---|

| Removal from Credit Report | Forgiven student loans are typically removed from credit reports. |

| Timeframe for Removal | Removal usually occurs within 30-45 days after forgiveness is processed. |

| Impact on Credit Score | Removal can improve credit score by eliminating negative marks or balances. |

| Type of Forgiveness Programs | Applies to programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment plans. |

| Reporting by Credit Bureaus | Credit bureaus (Equifax, Experian, TransUnion) update reports accordingly. |

| Documentation Required | No additional documentation is typically needed; removal is automatic. |

| Effect on Loan Status | Loans are marked as "paid in full" or "forgiven" before removal. |

| Exceptions | Private student loans may not follow the same rules as federal loans. |

| Tax Implications | Forgiven loans may be taxable, but this does not affect credit reporting. |

| Verification Process | Borrowers can verify removal by checking their credit reports post-forgiveness. |

Explore related products

What You'll Learn

- Impact on Credit Score: Forgiven loans may initially drop score, but recovery is possible over time

- Reporting Timeframe: Negative marks from forgiven loans typically remain for 7 years

- Credit Report Updates: Lenders must update reports to reflect forgiven status accurately

- Debt Settlement vs. Forgiveness: Settled debts may appear differently than forgiven loans on reports

- Disputing Errors: Incorrect forgiven loan entries can be disputed for removal

![]()

Impact on Credit Score: Forgiven loans may initially drop score, but recovery is possible over time

Forgiven student loans can trigger a temporary dip in your credit score, often due to the updated status reflecting as a "settled" or "forgiven" account rather than "paid in full." This change may signal to credit scoring models that the debt was resolved under less favorable terms, potentially lowering your score by 20 to 50 points initially. However, this impact isn’t permanent. Understanding the mechanics behind this fluctuation is key to navigating its effects and planning for recovery.

To mitigate the initial drop, monitor your credit report closely after loan forgiveness is processed. Ensure the forgiven account is accurately reported—errors like incorrect balances or statuses can exacerbate the damage. Dispute any inaccuracies with the credit bureaus promptly. Additionally, maintain a low credit utilization ratio (below 30%) on other accounts and avoid opening new credit lines during this period. These steps help stabilize your score while the forgiven loan’s impact fades.

Comparatively, forgiven student loans differ from discharged medical debt or paid-off credit cards. While medical debt removal often boosts scores immediately, forgiven loans may linger as a negative mark for up to seven years, depending on the reporting practices of the lender. However, their weight diminishes over time, especially if you demonstrate consistent positive credit behavior. For instance, paying bills on time, reducing debt, and keeping old accounts open can offset the forgiven loan’s impact within 12 to 24 months.

Recovery isn’t just possible—it’s probable with strategic action. Start by building a robust credit history through secured credit cards or small installment loans. If you’re over 21, ensure your oldest accounts remain active to preserve credit age. For younger borrowers (18–25), focus on establishing a solid payment history, as this factor carries significant weight in scoring models. Over time, the forgiven loan’s influence will wane, and your score will reflect your current financial habits more than past setbacks.

Finally, treat forgiven student loans as a learning opportunity rather than a permanent stain. While the initial drop can feel discouraging, it’s a temporary hurdle, not a roadblock. By understanding the mechanics, taking proactive steps, and staying disciplined, you can not only recover but also strengthen your credit profile. Remember: credit scores are dynamic, and forgiveness doesn’t define your financial future—your actions do.

Medical Coders and Student Loan Forgiveness: Eligibility Explained

You may want to see also

Explore related products

![]()

Reporting Timeframe: Negative marks from forgiven loans typically remain for 7 years

Negative marks from forgiven student loans don't vanish from your credit report the moment the debt is erased. The Fair Credit Reporting Act (FCRA) dictates a standard reporting timeframe for most negative information, including forgiven loans: seven years. This means that even though the loan is forgiven, the record of delinquency or default leading up to that forgiveness will linger, potentially impacting your creditworthiness during that period.

Imagine a scar that fades over time but doesn't disappear overnight. That's how forgiven loan marks behave on your credit report.

This seven-year clock typically starts ticking from the date of the first delinquency that led to the loan's forgiveness. For example, if you missed payments starting in January 2020 and the loan was forgiven in December 2022, the negative mark would likely remain on your report until January 2027. It's crucial to understand this timeline, as it directly affects your ability to secure loans, credit cards, or even rentals with favorable terms during this period.

While the forgiven loan itself is no longer a burden, its shadow can cast a long one on your financial profile.

It's important to note that this seven-year rule isn't absolute. Certain circumstances can shorten or extend the reporting period. For instance, bankruptcies involving student loans might result in a longer reporting timeframe. Conversely, successfully disputing inaccurate information on your credit report can lead to its removal before the seven years are up.

Don't let the seven-year timeframe discourage you. Proactive steps can mitigate the impact of forgiven loan marks. Regularly reviewing your credit report for inaccuracies and disputing them is essential. Additionally, focusing on building positive credit history through timely payments on other accounts and responsible credit usage can help outweigh the negative impact of the forgiven loan mark over time. Think of it as nurturing healthy skin around the scar – it may not erase the mark entirely, but it can significantly improve the overall appearance.

Filing for Student Loan Forgiveness on TurboTax: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Credit Report Updates: Lenders must update reports to reflect forgiven status accurately

Lenders and credit bureaus are legally obligated to ensure that forgiven student loans are accurately reflected on credit reports. Under the Fair Credit Reporting Act (FCRA), any outdated, inaccurate, or incomplete information must be corrected or removed. When a student loan is forgiven, it transitions from an outstanding debt to a resolved obligation, and this change must be documented promptly. Failure to update the forgiven status can mislead future lenders, potentially harming the borrower’s creditworthiness. For instance, a forgiven loan still listed as “past due” or “in collections” could unfairly lower a credit score, affecting access to loans, housing, or employment.

The process of updating credit reports begins with the lender or loan servicer reporting the forgiven status to the credit bureaus—Equifax, Experian, and TransUnion. This should occur within 30 to 45 days of forgiveness, though delays are not uncommon. Borrowers must proactively verify these updates by obtaining a free credit report from AnnualCreditReport.com. If the forgiven loan remains inaccurately listed, they should dispute the error directly with the credit bureau and provide proof of forgiveness, such as a letter from the loan servicer or the Department of Education. Persistence is key, as disputes can take up to 30 days to resolve.

One critical oversight often occurs with income-driven repayment (IDR) or Public Service Loan Forgiveness (PSLF) programs. For example, a borrower who completes 10 years of qualifying payments under PSLF may find their credit report still reflects the original loan balance or payment history. Lenders must report the forgiven amount as “paid as agreed” or “settled,” not as a charge-off or default. Borrowers should scrutinize their reports for such discrepancies, especially if applying for a mortgage or auto loan, where even minor inaccuracies can lead to higher interest rates or denials.

To safeguard against reporting errors, borrowers should maintain detailed records of all communications with loan servicers and forgiveness approvals. Automated tools like credit monitoring services can alert them to changes in their credit report, ensuring timely action. Additionally, advocating for legislative reforms that mandate stricter penalties for non-compliance could incentivize lenders to prioritize accuracy. Until then, staying informed and proactive remains the borrower’s best defense against the lingering effects of forgiven student loans on their credit profile.

Can Federal Student Loans Be Forgiven? Exploring Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Debt Settlement vs. Forgiveness: Settled debts may appear differently than forgiven loans on reports

Forgiven student loans and settled debts both offer relief from financial burdens, but their impact on your credit report can differ significantly. Understanding these differences is crucial for managing your credit health effectively. When a student loan is forgiven, it typically appears as "paid in full" or "settled for less than the full balance" on your credit report, depending on the forgiveness program. For instance, Public Service Loan Forgiveness (PSLF) shows the loan as paid in full, while income-driven repayment plans may reflect a settled status. This distinction matters because creditors view "paid in full" more favorably than "settled," which implies a negotiated reduction.

Debt settlement, on the other hand, involves negotiating with creditors to pay less than what you owe. Settled debts often appear as "settled for less than the full balance" on your credit report, which can signal financial distress to future lenders. For example, if you settle a $10,000 credit card debt for $5,000, the account will reflect this partial payment. While settling a debt removes the obligation, it doesn’t erase the negative mark. Settled accounts typically remain on your credit report for seven years from the date of settlement, impacting your credit score during that period.

The key difference lies in how these resolutions are perceived by credit scoring models. Forgiven student loans, especially those under government programs, are generally viewed as less damaging than settled debts. For instance, a forgiven federal student loan under PSLF is unlikely to harm your credit score, as it’s seen as fulfillment of a contractual agreement. In contrast, settled debts often carry a stigma, as they indicate a failure to meet the original terms of the loan. This can lower your credit score by 50–100 points, depending on your overall credit history.

Practical tip: If you’re considering debt settlement, weigh the long-term impact on your credit report. For student loans, explore forgiveness programs first, as they often provide a cleaner resolution. For example, if you qualify for PSLF, pursue that route instead of settling the debt. Additionally, monitor your credit report after any settlement or forgiveness to ensure accuracy. Disputing errors, such as a forgiven loan incorrectly marked as settled, can help mitigate damage.

In conclusion, while both debt settlement and loan forgiveness alleviate financial strain, their credit report implications vary. Forgiven student loans, particularly those under structured programs, tend to appear more favorably than settled debts. By understanding these nuances, you can make informed decisions to protect and improve your credit health. Always prioritize forgiveness options for student loans and approach debt settlement with caution, considering its lasting impact on your financial profile.

Optum Student Loan Forgiveness: What Employees Need to Know

You may want to see also

Explore related products

![]()

Disputing Errors: Incorrect forgiven loan entries can be disputed for removal

Forgiven student loans should theoretically vanish from your credit report, but errors happen. If you spot an incorrect entry for a forgiven loan, you have the right to dispute it. The Fair Credit Reporting Act (FCRA) empowers consumers to challenge inaccuracies on their credit reports, and forgiven loans lingering on your record fall squarely into this category.

Identifying the Error: Start by obtaining a free copy of your credit report from AnnualCreditReport.com. Scrutinize the student loan section for any forgiven loans still listed as active, delinquent, or in collections. Note the creditor, account number, and specific inaccuracy (e.g., "shows as unpaid" when forgiven). Documentation is key—gather proof of forgiveness, such as settlement letters or official notifications from your loan servicer.

Initiating the Dispute: Submit a formal dispute to the credit bureau(s) reporting the error. You can do this online, by mail, or by phone, though written disputes (via certified mail) provide a paper trail. Include a clear explanation of the error, copies of your proof (not originals), and a request for removal. Under the FCRA, bureaus must investigate disputes within 30 days, though extensions may apply if they need more information.

Escalating to the Creditor: If the bureau fails to correct the error, contact the creditor or loan servicer directly. Provide the same documentation and request they update their reporting to reflect the loan’s forgiven status. Creditors are legally obligated to report accurate information, and failure to do so can result in penalties under the FCRA.

Final Recourse: Persistent errors may require legal intervention. Consult a consumer protection attorney specializing in credit reporting disputes. They can help file a lawsuit against the bureau or creditor for non-compliance with the FCRA, potentially securing damages for harm caused by the inaccurate reporting.

Proactive monitoring and swift action are critical. Incorrect forgiven loan entries can depress your credit score, hinder loan approvals, and inflate interest rates. By disputing errors, you reclaim control over your financial narrative and ensure your credit report accurately reflects your financial standing.

Does Student Loan Forgiveness Call You? Uncovering the Truth

You may want to see also

Frequently asked questions

No, forgiven student loans are not immediately removed from your credit report. They typically remain on your report for 7 years from the date of settlement or forgiveness, as per the Fair Credit Reporting Act.

Once forgiven student loans are removed from your credit report, they will no longer impact your credit score. However, their presence on your report before removal may affect your score depending on how they were reported (e.g., in good standing or delinquent).

You can dispute inaccurate information related to forgiven student loans with the credit bureaus, but they cannot be removed early if reported correctly. Ensure the loan is marked as "paid in full" or "settled" after forgiveness to reflect the accurate status.