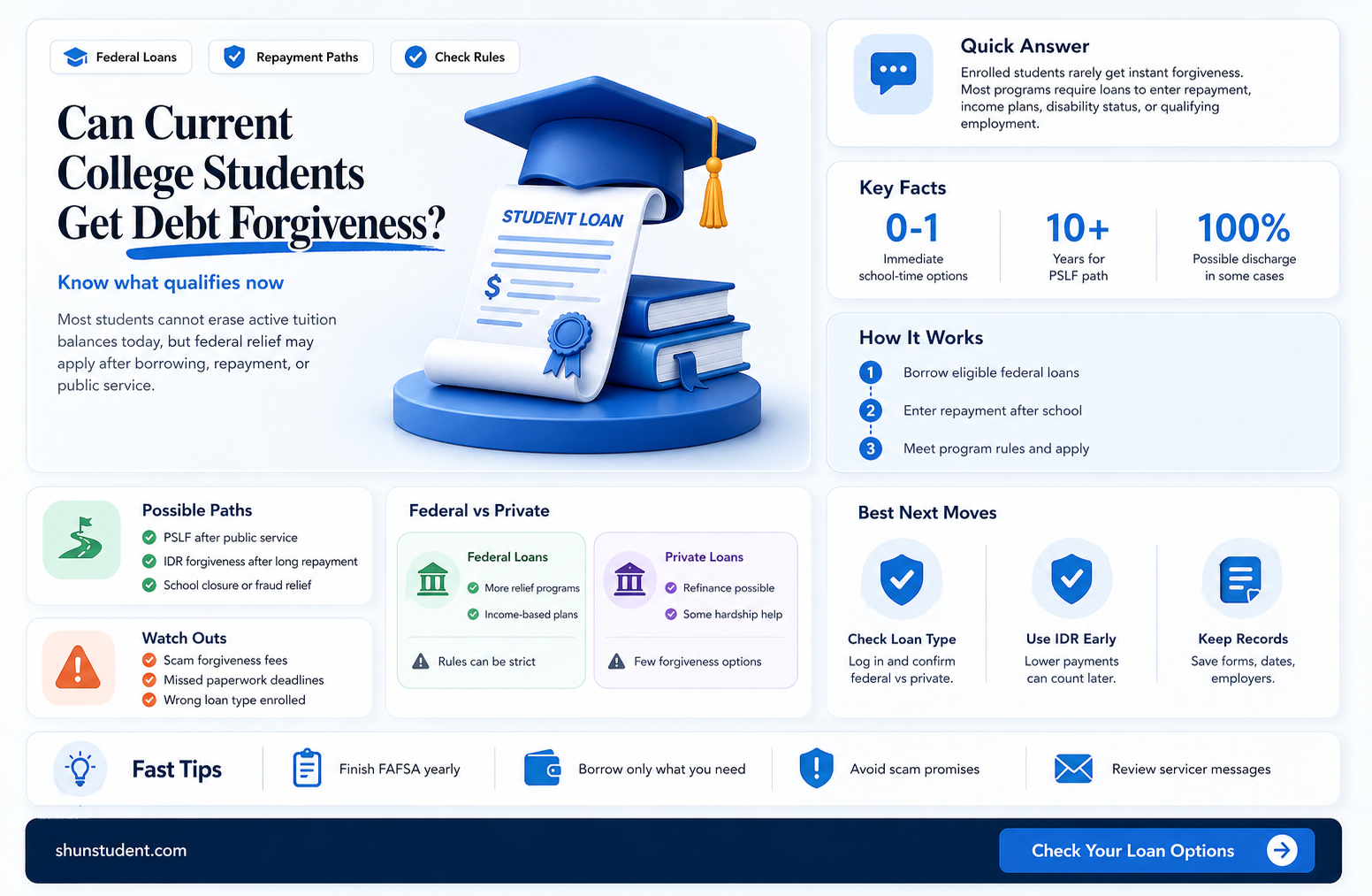

The topic of debt forgiveness for current college students has become increasingly relevant as student loan debt continues to soar, burdening millions of individuals and families. With the rising cost of higher education and the economic challenges faced by many, there is growing interest in understanding whether current college students are eligible for debt forgiveness programs. These initiatives, often proposed or implemented by governments and institutions, aim to alleviate financial strain and provide a fresh start for borrowers. Eligibility criteria can vary widely, depending on factors such as the type of loans, enrollment status, income levels, and specific policy frameworks. As discussions around debt forgiveness gain momentum, it is crucial for current students to stay informed about available options and potential changes that could impact their financial futures.

Explore related products

What You'll Learn

- Federal vs. Private Loans: Eligibility differences for government and private lender debt forgiveness programs

- Income-Driven Repayment Plans: Qualifying for forgiveness through long-term, income-based payment options

- Public Service Loan Forgiveness: Requirements for students working in public service sectors

- Student Loan Cancellation Policies: Current laws and proposals for debt cancellation eligibility

- State-Specific Forgiveness Programs: Regional opportunities for college students to reduce or eliminate debt

![]()

Federal vs. Private Loans: Eligibility differences for government and private lender debt forgiveness programs

Current college students navigating the complexities of debt forgiveness must first understand the stark differences between federal and private loans. Federal loans, backed by the government, offer a variety of forgiveness programs tied to factors like income, profession, and repayment plan. For instance, the Public Service Loan Forgiveness (PSLF) program forgives remaining balances after 120 qualifying payments for those in eligible public service jobs. In contrast, private loans, issued by banks or credit unions, rarely offer forgiveness options. While some private lenders may provide relief in extreme cases, such as permanent disability, these instances are exceptions rather than the rule. This fundamental disparity underscores the importance of distinguishing between loan types when exploring forgiveness opportunities.

For federal loan borrowers, eligibility for forgiveness programs often hinges on specific criteria. Income-Driven Repayment (IDR) plans, for example, cap monthly payments at a percentage of discretionary income and forgive remaining balances after 20–25 years of consistent payments. Teachers working in low-income schools may qualify for up to $17,500 in forgiveness through the Teacher Loan Forgiveness program. To maximize eligibility, students should consolidate loans into a Direct Consolidation Loan, as only this type qualifies for programs like PSLF. Practical tip: Track payments meticulously, as errors in documentation can disqualify borrowers from forgiveness.

Private loan borrowers face a far more limited landscape. While some lenders offer partial relief for borrowers facing economic hardship, full forgiveness is virtually nonexistent. However, students can explore alternative strategies, such as refinancing to lower interest rates or negotiating settlements in cases of severe financial distress. Caution: Refinancing federal loans into private ones eliminates access to government forgiveness programs, a decision that should not be taken lightly. For those with private loans, focusing on aggressive repayment strategies or seeking employer-assisted repayment benefits may be more fruitful than pursuing forgiveness.

A comparative analysis reveals that federal loans provide a structured pathway to forgiveness, whereas private loans leave borrowers with few options. For instance, a nursing student with federal loans could qualify for PSLF by working in a nonprofit hospital, while a peer with private loans would have no such recourse. This highlights the critical role of loan type in shaping long-term financial outcomes. Takeaway: Students should prioritize federal loans when borrowing and carefully weigh the trade-offs if considering private options, as the absence of forgiveness programs can significantly impact repayment burdens.

Instructively, current college students should take proactive steps to align their borrowing strategy with their post-graduation goals. For federal loan borrowers, enrolling in an IDR plan immediately after graduation can set the stage for future forgiveness. Private loan borrowers should focus on building a robust financial plan, including emergency funds and high-yield career paths, to mitigate the lack of forgiveness options. Ultimately, understanding the eligibility differences between federal and private loans empowers students to make informed decisions that minimize debt-related stress and maximize financial stability.

Hope Walz's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: Qualifying for forgiveness through long-term, income-based payment options

Current college students burdened by federal loans may not yet qualify for debt forgiveness, but they can strategically position themselves for future relief through Income-Driven Repayment (IDR) plans. These plans tie monthly payments to income and family size, offering a lifeline for those with limited earnings post-graduation. By enrolling in an IDR plan immediately after entering repayment, students can begin the clock on the 20- to 25-year forgiveness timeline, even if their payments are as low as $0. This long-term strategy requires patience but can significantly reduce financial strain over time.

To qualify for an IDR plan, students must first enter repayment status, which typically begins six months after graduation, leaving school, or dropping below half-time enrollment. At this point, they can choose from four main IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), or Income-Contingent Repayment (ICR). Each plan has specific eligibility criteria, such as income thresholds and loan types, but all aim to cap monthly payments at a manageable percentage of discretionary income, ranging from 10% to 20%. For instance, a recent graduate earning $30,000 annually with a family size of one might pay as little as $175 per month under the REPAYE plan.

While IDR plans offer immediate relief, their true value lies in the forgiveness component. After 20 to 25 years of consistent payments, any remaining balance is forgiven, though borrowers may owe taxes on the forgiven amount. For example, a borrower on the PAYE plan could see forgiveness after 20 years, while someone on ICR would wait 25 years. This makes IDR plans particularly appealing for students pursuing careers in public service or nonprofit sectors, where incomes may remain modest for extended periods. However, it’s crucial to recertify income and family size annually to avoid payment increases or plan disqualification.

One common misconception is that IDR plans are only for those in dire financial situations. In reality, they are a strategic tool for anyone anticipating long-term financial uncertainty or planning to pursue lower-paying careers. For instance, a student studying social work or education can enroll in an IDR plan immediately after graduation, ensuring payments remain affordable while they build their career. Over time, as their income grows, payments may increase, but the forgiveness timeline remains intact, providing a safety net for the future.

To maximize the benefits of IDR plans, students should proactively research their options before entering repayment. Tools like the Federal Student Aid Loan Simulator can help estimate monthly payments and forgiveness timelines under different plans. Additionally, staying informed about policy changes, such as the recent IDR Account Adjustment, which retroactively counts certain periods toward forgiveness, can further accelerate progress. While current students cannot yet enroll, understanding these plans now allows them to make informed decisions once repayment begins, turning a daunting debt into a manageable long-term commitment.

Student Loan Forgiveness and Inflation: Economic Impact Explored

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness: Requirements for students working in public service sectors

Current college students often wonder if they can qualify for debt forgiveness, especially if they plan to work in public service. One of the most promising pathways is the Public Service Loan Forgiveness (PSLF) program, which offers tax-free forgiveness of federal student loans after 120 qualifying payments. However, eligibility hinges on specific criteria that students must navigate carefully.

To qualify for PSLF, students must first secure employment in a public service organization, defined as government entities at any level, 501(c)(3) nonprofit organizations, or other qualifying nonprofits. This includes roles in education, healthcare, law enforcement, and military service. Crucially, the type of employer, not the role itself, determines eligibility. For instance, a teacher at a public school qualifies, but a teacher at a for-profit charter school does not. Students should verify their employer’s eligibility using the PSLF Help Tool provided by the U.S. Department of Education.

The second requirement is having the right type of federal student loans. Only Direct Loans qualify for PSLF; Federal Family Education Loans (FFEL) and Perkins Loans do not, unless consolidated into a Direct Consolidation Loan. Students with non-qualifying loans can consolidate them, but beware: consolidation restarts the payment counter for PSLF. Payments made before consolidation do not count toward the 120 required.

The third critical factor is making 120 qualifying payments under an income-driven repayment (IDR) plan. These plans, such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE), cap monthly payments at a percentage of discretionary income. Payments must be made on time and in full to qualify. Periods of deferment, forbearance, or default do not count. Students should submit the Employer Certification Form annually to ensure payments are tracking correctly.

Finally, students must apply for forgiveness after completing 120 qualifying payments. This involves submitting the PSLF application and providing proof of employment and payments. Approval rates have historically been low due to administrative errors, so meticulous record-keeping is essential. Recent updates, such as the Limited PSLF Waiver (which expired in October 2022), have expanded eligibility retroactively, but future waivers are uncertain.

In summary, while PSLF offers a clear path to debt forgiveness for public service workers, current college students must strategically plan their employment, loan type, repayment plan, and documentation to qualify. Early research and proactive steps can turn this program into a powerful tool for financial freedom.

Hope Waltz's Student Loan Forgiveness: Fact or Fiction?

You may want to see also

Explore related products

$9.99 $12.99

![]()

Student Loan Cancellation Policies: Current laws and proposals for debt cancellation eligibility

Current federal student loan cancellation policies primarily target borrowers who have already completed their education, leaving current college students with limited direct eligibility. The Public Service Loan Forgiveness (PSLF) program, for example, requires borrowers to make 120 qualifying payments while working full-time in public service—a pathway unavailable to students still in school. Similarly, income-driven repayment (IDR) plans offer forgiveness after 20–25 years of payments, a timeline that begins only after graduation. While these programs benefit former students, they do not address the debt current students are accruing. However, one exception is the Closed School Discharge, which allows students to have loans canceled if their school closes while they are enrolled or shortly after withdrawal. This narrow policy highlights the gap in broader eligibility for current students.

Proposals for debt cancellation have begun to address this gap, though their implementation remains uncertain. The Free College Movement, championed by lawmakers like Senator Bernie Sanders, advocates for tuition-free public college and student debt cancellation, including for current students. Another proposal, the Student Borrower Bill of Rights, seeks to expand eligibility for loan forgiveness by simplifying IDR plans and reducing repayment burdens. Notably, President Biden’s targeted debt relief initiatives, such as the $10,000 to $20,000 cancellation plan (currently stalled in court), excluded current students unless they had federal loans prior to enrollment. These proposals underscore a growing recognition of the need to include current students in debt relief efforts, but they remain contingent on legislative and legal outcomes.

A comparative analysis reveals that while current students are largely ineligible for existing forgiveness programs, they are not entirely excluded from all forms of relief. For instance, borrower defense to repayment allows students to seek loan cancellation if their school misled them, regardless of enrollment status. Additionally, state-level initiatives, such as New York’s Excelsior Scholarship, offer tuition-free college but do not directly address existing debt. In contrast, countries like Germany and Norway provide tuition-free education, eliminating the need for student loans altogether. This global perspective suggests that while U.S. policies are evolving, they still fall short of comprehensive solutions for current students.

To navigate this landscape, current students should take proactive steps to minimize future debt and explore available relief options. First, exhaust federal grants and scholarships before taking out loans. Second, monitor legislative updates on proposals like the Free College Act or Debt-Free College Act, which could expand eligibility for cancellation. Third, consider attending a tuition-free or low-cost institution, such as community colleges or schools with generous aid packages. Finally, stay informed about state-specific programs, as some offer loan repayment assistance for students in high-demand fields like healthcare or education. While current policies offer limited relief, strategic planning and advocacy can help mitigate the burden.

Does Kaiser Permanente Employment Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

State-Specific Forgiveness Programs: Regional opportunities for college students to reduce or eliminate debt

While federal student loan forgiveness programs often dominate the conversation, a hidden gem for current college students lies in state-specific forgiveness programs. These initiatives, tailored to regional needs and priorities, offer targeted debt relief opportunities that federal programs might overlook.

Imagine a future teacher committing to serve in a high-need school district in exchange for a significant portion of their student loans forgiven, or a recent nursing graduate having their debt reduced for working in an underserved rural community. These are just a few examples of the possibilities unlocked by state-specific programs.

Each state crafts its own unique approach, reflecting its economic landscape and workforce demands. Some programs target specific professions like healthcare, education, or public service, while others focus on geographic areas facing critical shortages. Eligibility criteria vary widely, often considering factors like residency, degree type, employment commitments, and income levels.

Navigating the Landscape: A Practical Guide

To unlock these opportunities, students must become adept navigators of their state's higher education landscape. Start by visiting your state's higher education website or department of education. These resources often house dedicated sections outlining available forgiveness programs, eligibility requirements, and application procedures.

Don't be afraid to reach out directly to program administrators for clarification or guidance. Many states also have dedicated hotlines or email addresses for inquiries. Remember, these programs are designed to benefit students and communities alike, so don't hesitate to seek assistance.

Beyond the Basics: Maximizing Your Chances

While meeting basic eligibility criteria is essential, going the extra mile can significantly enhance your chances of securing state-based forgiveness. Consider these strategies:

- Strategic Career Planning: Align your academic and career goals with the professions targeted by your state's programs. Research in-demand fields and geographic areas to identify opportunities for both personal fulfillment and debt relief.

- Early Engagement: Some programs require commitments made during your studies, such as enrolling in specific programs or completing internships in designated areas. Start exploring options early to maximize your eligibility.

- Document Everything: Keep meticulous records of your academic achievements, work experience, and any commitments made related to forgiveness programs. This documentation will be crucial during the application process.

A Win-Win Scenario:

State-specific forgiveness programs represent a win-win scenario for both students and communities. Students gain access to much-needed financial relief, while states address critical workforce shortages and strengthen their local economies. By proactively seeking out these opportunities, current college students can not only alleviate the burden of debt but also contribute meaningfully to their communities.

Income-Based Repayment and Student Loan Forgiveness: What You Need to Know

You may want to see also

Frequently asked questions

Current college students are generally not eligible for federal student loan forgiveness programs until they graduate, leave school, or drop below half-time enrollment. Forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans require borrowers to make qualifying payments after completing their education.

Some states or colleges offer loan forgiveness or repayment assistance programs for students in specific fields (e.g., healthcare, education) or those who meet certain criteria. Eligibility varies, so students should research programs offered by their state, school, or employer.

Future debt forgiveness initiatives, such as those proposed by policymakers, may include current students if they meet specific criteria (e.g., income limits, loan type). However, eligibility depends on the details of the program and is not guaranteed. Students should stay informed about legislative updates.