The topic of student loan forgiveness, particularly for direct loans, has been a subject of intense debate and speculation in recent years. With the rising cost of education and the burden of debt on millions of borrowers, many are eagerly awaiting updates on potential relief measures. Direct student loans, issued by the federal government, have become a focal point as policymakers and advocates push for comprehensive solutions to alleviate the financial strain on borrowers. Amidst various proposals and executive actions, understanding the current status and future prospects of direct student loan forgiveness is crucial for those seeking financial relief and a path toward economic stability.

| Characteristics | Values |

|---|---|

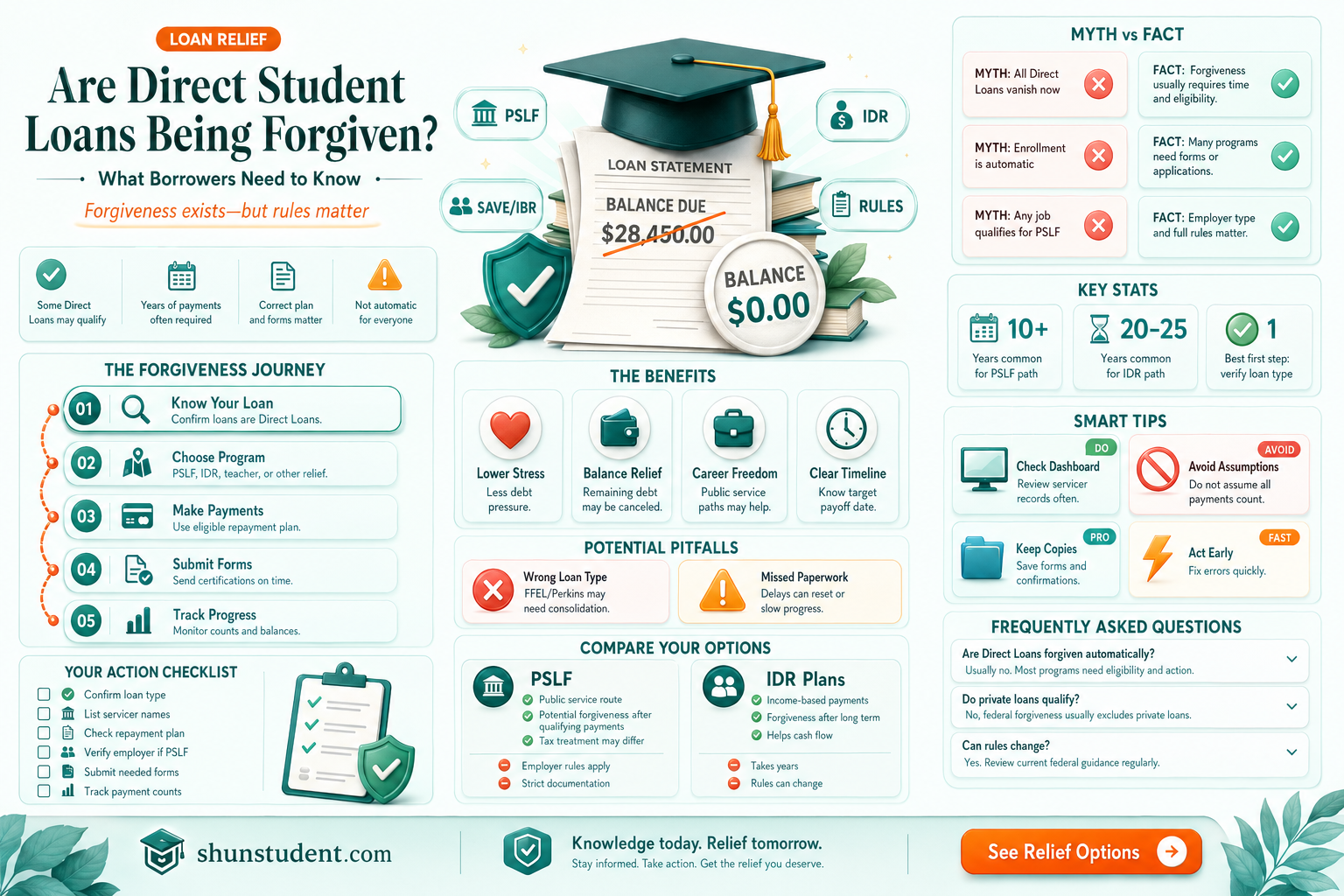

| Current Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, Temporary Expanded PSLF (TEPSLF) |

| Eligibility Criteria | Varies by program; e.g., PSLF requires 120 qualifying payments and government/nonprofit employment |

| Loan Types Eligible | Direct Loans (Federal Family Education Loan Program [FFELP] loans may require consolidation) |

| Recent Updates (as of 2023) | One-time IDR account adjustment (2023) to address payment counting errors; no broad student loan forgiveness due to Supreme Court ruling |

| Supreme Court Ruling (June 2023) | Struck down Biden’s $400 billion mass student loan forgiveness plan, limiting broad forgiveness |

| Remaining Forgiveness Options | Targeted programs like PSLF, IDR, disability discharge, closed school discharge, and borrower defense to repayment |

| Pending Proposals | No active proposals for mass forgiveness; focus on improving existing programs and addressing administrative errors |

| Loan Payment Status (as of Oct 2023) | Payments resumed after COVID-19 pause; interest accrual restarted |

| Debt Cancellation Statistics | Over $132 billion forgiven for 3.6 million borrowers (via targeted programs, not mass forgiveness) |

| Future Outlook | No widespread forgiveness expected; emphasis on program reforms and addressing servicing issues |

Explore related products

What You'll Learn

- Eligibility Criteria: Who qualifies for student loan forgiveness under current programs

- Public Service Loan Forgiveness (PSLF): Requirements and benefits for public service workers

- Income-Driven Repayment Plans: How these plans lead to loan forgiveness over time

- Biden Administration’s Forgiveness Plan: Updates on the $10,000-$20,000 forgiveness proposal

- Loan Forgiveness Scams: How to avoid fraudulent forgiveness schemes targeting borrowers

![]()

Eligibility Criteria: Who qualifies for student loan forgiveness under current programs?

Student loan forgiveness isn’t automatic—it hinges on meeting specific eligibility criteria tied to federal programs. The most prominent is Public Service Loan Forgiveness (PSLF), which requires 120 qualifying payments while working full-time for a government or nonprofit organization. These payments must be made under an income-driven repayment plan, and the loans must be federal Direct Loans. For example, a teacher at a public school or a nurse at a nonprofit hospital could qualify after 10 years of consistent payments.

Another pathway is Income-Driven Repayment (IDR) Forgiveness, which applies to borrowers whose payments are calculated based on income and family size. Depending on the plan—such as Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE)—forgiveness kicks in after 20 or 25 years of payments. This option is particularly beneficial for borrowers with high debt relative to their income. For instance, a social worker earning $40,000 annually with $100,000 in loans could see forgiveness after 20–25 years, depending on their plan.

Teacher Loan Forgiveness targets educators in low-income schools, offering up to $17,500 in forgiveness for those who teach full-time for five consecutive years in eligible subjects or schools. Math and science teachers in secondary schools, for example, qualify for the maximum amount, while elementary teachers can receive up to $5,000. This program requires federal Direct Loans or FFEL Loans, and the five years of service must be continuous.

Lastly, Borrower Defense to Repayment provides relief for students misled by their college or university. If a school violated state laws or engaged in fraudulent practices, borrowers may apply for full discharge of their Direct Loans. For instance, students of now-defunct for-profit institutions like Corinthian Colleges or ITT Tech have successfully used this program. Documentation of the school’s misconduct is critical for approval.

Understanding these criteria is essential for navigating forgiveness programs effectively. Each has unique requirements, from employment type to repayment plan specifics, so borrowers must carefully assess their eligibility and document their progress to ensure they meet all conditions.

ROTC and Student Loan Forgiveness: Exploring Repayment Options for Cadets

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Requirements and benefits for public service workers

Public service workers burdened by student debt have a lifeline in the form of the Public Service Loan Forgiveness (PSLF) program. This federal initiative offers a path to debt relief for those who dedicate their careers to serving the public good. However, navigating the program's requirements can be complex.

Understanding the eligibility criteria is crucial. To qualify for PSLF, borrowers must make 120 qualifying payments while working full-time for a qualifying employer. "Full-time" generally means working at least 30 hours per week, and qualifying employers include government organizations at any level (federal, state, local), 501(c)(3) non-profit organizations, and some other types of non-profits that provide specific public services.

The type of loan matters. Only Direct Loans are eligible for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you'll need to consolidate them into a Direct Consolidation Loan to qualify. Crucially, payments made under certain repayment plans, such as income-driven repayment plans, count towards the 120 required payments.

The benefits of PSLF are substantial. After making 120 qualifying payments, the remaining balance on your Direct Loans is forgiven tax-free. This can represent a significant financial windfall, allowing public service workers to shed the burden of student debt and achieve greater financial freedom.

It's important to note that PSLF requires meticulous record-keeping. Borrowers should submit an Employment Certification Form annually or when changing employers to ensure their payments are counted correctly. The Department of Education's Federal Student Aid website provides detailed guidance and resources to help borrowers navigate the PSLF process. While the requirements may seem stringent, the potential for debt forgiveness makes PSLF a valuable program for public service workers committed to a career of service.

Discovering Forgivable Student Loans: A Comprehensive Guide for Borrowers

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans: How these plans lead to loan forgiveness over time

For borrowers grappling with federal student loan debt, Income-Driven Repayment (IDR) plans offer a lifeline by tying monthly payments to income and family size. These plans aren’t just about affordability—they’re a pathway to loan forgiveness after a set period, typically 20 or 25 years, depending on the plan. For example, under the Revised Pay As You Earn (REPAYE) plan, borrowers can qualify for forgiveness after 20 years of payments if all loans were for undergraduate study, or 25 years if any loans were for graduate or professional study. This structured forgiveness mechanism transforms long-term debt management into a predictable journey toward financial freedom.

To maximize the benefits of IDR plans, borrowers must choose the right plan for their financial situation. For instance, the Pay As You Earn (PAYE) plan caps monthly payments at 10% of discretionary income and forgives remaining balances after 20 years. However, eligibility requires demonstrating partial financial hardship, such as having a higher loan balance relative to income. In contrast, the Income-Based Repayment (IBR) plan offers a slightly higher payment cap (10% or 15% of discretionary income, depending on when the loan was taken out) but extends the forgiveness timeline to 20 or 25 years. Borrowers should use the Federal Student Aid Loan Simulator to compare plans and project long-term outcomes.

One critical aspect often overlooked is the tax implications of loan forgiveness. When loans are forgiven under IDR plans, the forgiven amount may be treated as taxable income, potentially resulting in a significant tax bill. However, the American Rescue Act of 2021 temporarily exempts forgiven student loan balances from federal income tax through 2025. Borrowers should consult a tax professional to plan for potential tax liabilities beyond this period and explore strategies like saving a portion of their income annually to cover future tax obligations.

Persistence and vigilance are key to success with IDR plans. Borrowers must recertify their income and family size annually to maintain their payment amount and progress toward forgiveness. Missing recertification deadlines can lead to a switch to a standard repayment plan, derailing the forgiveness timeline. Additionally, keeping detailed records of payments is essential, as administrative errors in tracking qualifying payments have historically plagued IDR programs. Tools like the Department of Education’s IDR Payment Counter, launched in 2023, help borrowers track their progress and ensure accuracy.

In summary, Income-Driven Repayment plans are a strategic tool for achieving student loan forgiveness, but they require careful selection, proactive tax planning, and consistent administrative follow-through. By understanding the nuances of each plan and staying engaged in the process, borrowers can turn a daunting debt burden into a manageable—and ultimately forgivable—financial commitment.

Unlocking 20-Year Student Loan Forgiveness: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Biden Administration’s Forgiveness Plan: Updates on the $10,000-$20,000 forgiveness proposal

The Biden Administration's student loan forgiveness plan has been a beacon of hope for millions of borrowers, but its journey has been fraught with legal challenges and procedural hurdles. Initially, the proposal promised to cancel $10,000 in federal student loan debt for eligible borrowers, with an additional $10,000 for those who received Pell Grants. This initiative aimed to alleviate the financial burden on low- and middle-income individuals, many of whom have been saddled with debt for decades. However, the plan was swiftly blocked by the Supreme Court in June 2023, citing the administration’s overreach of authority under the HEROES Act. Despite this setback, the administration has not abandoned its efforts, pivoting to alternative strategies to provide relief.

One of the key updates post-Supreme Court ruling is the Biden Administration’s focus on income-driven repayment (IDR) plans and targeted loan forgiveness programs. For instance, the Saving on a Valuable Education (SAVE) Plan, launched in 2023, significantly reduces monthly payments for borrowers by capping them at a smaller percentage of discretionary income. Additionally, the plan offers faster forgiveness for smaller loan balances, with borrowers eligible for cancellation after 10 years of payments if their original loan amount was $12,000 or less. This approach, while not as sweeping as the original $10,000-$20,000 proposal, provides tangible relief to a substantial portion of borrowers, particularly those with lower incomes.

Another critical update is the administration’s efforts to address administrative errors in loan servicing that have prevented borrowers from receiving credit toward forgiveness. Through the IDR Account Adjustment, the Department of Education has retroactively credited borrowers for months spent in forbearance or certain repayment plans, bringing millions closer to loan cancellation. This initiative, while less publicized, has had a profound impact on borrowers who have been paying for years without seeing progress toward forgiveness. It underscores the administration’s commitment to fixing systemic issues within the student loan system.

For borrowers navigating these changes, practical steps include enrolling in the SAVE Plan to take advantage of its lower payment caps and faster forgiveness timelines. Additionally, borrowers should review their payment histories to ensure they receive credit for all qualifying months under the IDR Account Adjustment. Those with private loans or ineligible federal loans should explore refinancing options, though this may not be suitable for everyone, especially if it disqualifies them from future forgiveness programs. Staying informed through official Department of Education channels is crucial, as the landscape continues to evolve.

In comparison to previous administrations, the Biden Administration’s approach to student loan forgiveness is both ambitious and pragmatic. While the original $10,000-$20,000 proposal faced legal defeat, the shift toward targeted reforms and administrative fixes demonstrates a willingness to adapt. This strategy, though slower and less comprehensive, has the potential to deliver meaningful relief to millions of borrowers. The takeaway is clear: while broad-based forgiveness remains elusive, incremental changes are making a difference, offering hope to those burdened by student debt.

Disability and Student Loans: Can Debt Be Forgiven?

You may want to see also

Explore related products

![]()

Loan Forgiveness Scams: How to avoid fraudulent forgiveness schemes targeting borrowers

As the debate over direct student loan forgiveness continues, scammers are capitalizing on borrowers' hopes and uncertainties. Fraudulent schemes promising loan forgiveness or reduction have surged, preying on those desperate for financial relief. These scams often mimic official communications, using convincing language and branding to appear legitimate. Recognizing the red flags is crucial to protecting yourself from financial loss and identity theft.

Step 1: Verify the Source

Legitimate loan forgiveness programs are administered through the U.S. Department of Education or authorized loan servicers. Scammers, however, often contact borrowers via unsolicited emails, texts, or phone calls, claiming to be affiliated with these entities. Always verify the sender’s identity by checking official websites or contacting your loan servicer directly using verified contact information. Ignore any communication that pressures you to act immediately or requests personal information upfront.

Caution: Common Scam Tactics

Fraudsters employ several tactics to deceive borrowers. One common scheme involves charging upfront fees for services that are either unnecessary or nonexistent. Another tactic is promising expedited forgiveness in exchange for sensitive information, such as your FSA ID or Social Security number. Some scammers even create fake websites that mimic official platforms, tricking borrowers into sharing login credentials. Be wary of guarantees of loan forgiveness, as no legitimate program can assure eligibility without a formal application process.

Example: A Real-Life Scenario

Consider the case of a borrower who received a call from a company claiming to be a "student loan debt advisor." The caller promised to eliminate $10,000 in debt for a $500 fee. The borrower, eager for relief, paid the fee but later discovered no action had been taken on their loans. Worse, their personal information was compromised, leading to unauthorized charges on their credit card. This example underscores the importance of skepticism and due diligence when approached with such offers.

Takeaway: Protect Yourself Proactively

To avoid falling victim to loan forgiveness scams, stay informed about official programs and their requirements. Regularly monitor your loan accounts for unauthorized changes and report suspicious activity immediately. Remember, legitimate forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment plans, do not require upfront payments or personal information via unsolicited requests. By staying vigilant and verifying every offer, you can safeguard your finances and avoid fraudulent schemes targeting vulnerable borrowers.

Forgiving Student Loans: Economic Boost or Unfair Burden?

You may want to see also

Frequently asked questions

No, not all direct student loans are eligible for forgiveness. Eligibility depends on the specific forgiveness program, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans, and meeting their requirements.

As of now, there is no blanket forgiveness for all direct student loans. Forgiveness programs are targeted and require borrowers to meet specific criteria, such as working in public service or making qualifying payments under an IDR plan.

To qualify, you typically need to enroll in an income-driven repayment plan, make 120 qualifying payments (for PSLF), or meet the terms of other forgiveness programs like Teacher Loan Forgiveness or IDR forgiveness after 20–25 years of payments.

The Biden administration has implemented limited student loan forgiveness initiatives, such as targeted relief for specific groups (e.g., borrowers defrauded by schools) and the one-time debt relief program (currently paused due to legal challenges). No universal forgiveness has been announced.

Contact your loan servicer or visit the Federal Student Aid website to review your loan type and eligibility for forgiveness programs. You can also explore options like income-driven repayment plans to work toward potential forgiveness.