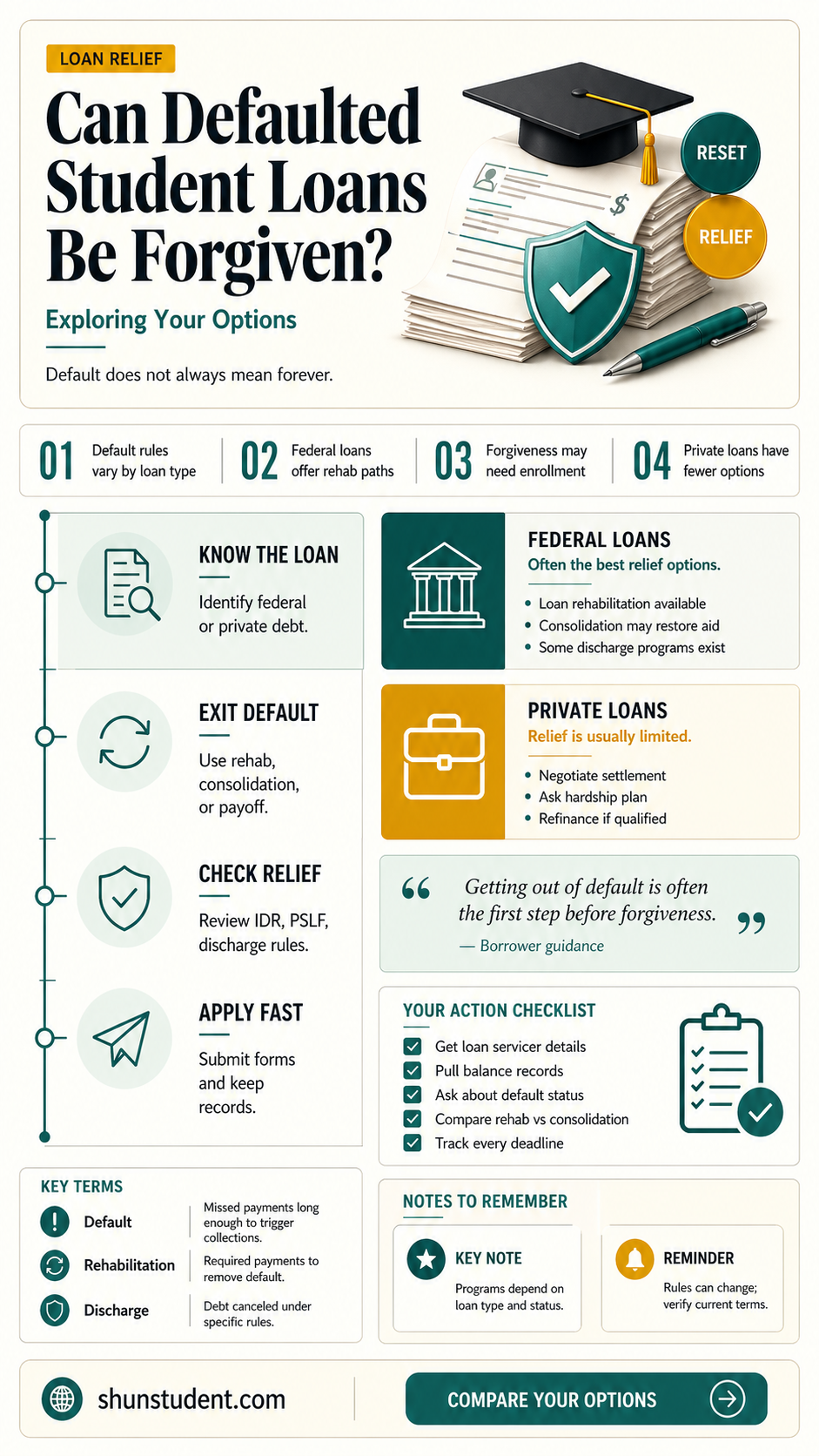

Defaulted student loans can be a significant financial burden, but there are pathways to forgiveness under certain conditions. While defaulting on student loans typically complicates the forgiveness process, options such as loan rehabilitation, consolidation, or qualifying for income-driven repayment plans can restore eligibility for loan forgiveness programs. Additionally, specific circumstances like total and permanent disability, public service, or school closure may offer opportunities for discharge. Understanding these options and taking proactive steps to address defaulted loans can provide a way forward for borrowers seeking relief from their student debt.

| Characteristics | Values |

|---|---|

| Forgiveness Possibility | Yes, defaulted student loans can be forgiven under specific conditions. |

| Primary Forgiveness Program | Public Service Loan Forgiveness (PSLF) after consolidation and rehabilitation. |

| Rehabilitation Process | Requires 9 out of 10 consecutive monthly payments to rehabilitate loans. |

| Consolidation Requirement | Defaulted loans must be consolidated into a Direct Consolidation Loan. |

| Tax Implications | Forgiven amounts may be taxable as income (except for PSLF). |

| Credit Impact | Default status removed after rehabilitation, improving credit score. |

| Timeframe for Forgiveness | Varies; PSLF requires 120 qualifying payments post-rehabilitation. |

| Eligibility for Federal Aid | Regains eligibility for federal student aid after rehabilitation. |

| Collection Activities | Cease after rehabilitation or consolidation. |

| Private Loan Forgiveness | Rarely forgiven; depends on lender policies or bankruptcy (difficult). |

| Income-Driven Repayment (IDR) | Can enroll in IDR plans after rehabilitation for manageable payments. |

| Statute of Limitations | No federal statute; varies by state for private loans. |

| Bankruptcy Discharge | Extremely rare for federal loans; possible for private loans under hardship. |

| Latest Updates (as of 2023) | Fresh Start initiative helps remove defaults and restore aid eligibility. |

Explore related products

What You'll Learn

![]()

Bankruptcy Discharge Possibility

Defaulted student loans can feel like an inescapable burden, but bankruptcy discharge offers a glimmer of hope—albeit a faint one. Unlike credit card debt or medical bills, student loans are notoriously difficult to discharge in bankruptcy due to the "undue hardship" standard, a legal hurdle higher than Mount Everest. This standard, established by the *Brunner test*, requires borrowers to prove they cannot maintain a minimal standard of living, that their financial situation is unlikely to improve, and that they’ve made good-faith efforts to repay the loans. Meeting these criteria is rare, with only about 0.1% of bankruptcy filers even attempting it, and fewer succeeding.

To navigate this process, start by filing for Chapter 7 or Chapter 13 bankruptcy, as these are the only types that allow for student loan discharge. Next, file an *adversary proceeding*, a separate lawsuit within the bankruptcy case, to challenge the student loans. Here’s where specificity matters: gather evidence of your financial distress, such as medical bills, unemployment records, or disability documentation. A 50-year-old borrower with a permanent disability and no savings, for instance, might have a stronger case than a 30-year-old with temporary job loss. Consult a bankruptcy attorney specializing in student loans—their expertise can make or break your case.

Critics argue the system is rigged against borrowers, and they’re not wrong. The *Brunner test* is subjective, leaving outcomes to the discretion of judges who may interpret "undue hardship" differently. Some courts have begun applying the *Totality of Circumstances* test, which considers factors like age, health, and future earning potential more holistically. However, this alternative is not universally adopted, creating a geographic lottery for borrowers. For example, a borrower in Massachusetts might face a stricter judge than one in California, despite identical circumstances.

Despite the odds, success stories exist. In 2022, a 60-year-old woman with $100,000 in student loans and no assets secured a discharge after proving her chronic illness prevented employment. Her case highlights the importance of persistence and detailed documentation. Practical tip: keep a financial diary tracking expenses, job applications, and loan repayment attempts. This record can serve as powerful evidence in court.

In conclusion, while bankruptcy discharge for student loans is rare, it’s not impossible. The process demands meticulous preparation, legal expertise, and a bit of luck. If you’re drowning in defaulted loans, don’t dismiss bankruptcy outright—but approach it as a last resort, armed with evidence and a skilled attorney. The system may be flawed, but for some, it remains the only lifeline.

Track Student Loan Forgiveness: A Step-by-Step Guide for Borrowers

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) Eligibility

Defaulted student loans cast a long shadow, but Public Service Loan Forgiveness (PSLF) offers a glimmer of hope for those committed to serving the greater good. This program, established in 2007, provides a pathway to debt relief for borrowers who dedicate their careers to public service. However, navigating the eligibility requirements can be complex.

Understanding these requirements is crucial, as even a minor misstep can derail your path to forgiveness.

Qualifying Employment: The Cornerstone of PSLF

The foundation of PSLF eligibility rests on your employer. You must work full-time for a qualifying employer, which includes government organizations at any level (federal, state, local, or tribal), 501(c)(3) non-profit organizations, and some other types of non-profits that provide specific public services. This encompasses a wide range of professions, from teachers and nurses to social workers and public defenders. It's essential to verify your employer's eligibility using the PSLF Help Tool provided by the U.S. Department of Education.

Keep in mind that working for a qualifying employer doesn't automatically guarantee eligibility. You must also be employed in a role that directly contributes to the organization's public service mission.

Loan Type and Repayment Plan: Crucial Details

Not all student loans are created equal when it comes to PSLF. Only Direct Loans are eligible for forgiveness under this program. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you'll need to consolidate them into a Direct Consolidation Loan to qualify.

Furthermore, you must be enrolled in an income-driven repayment (IDR) plan. These plans cap your monthly payments based on your income and family size, making them more manageable for borrowers with lower incomes. Popular IDR plans include Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE).

Choosing the right IDR plan is crucial, as it directly impacts your monthly payments and the overall time it takes to reach forgiveness.

The 120 Payments Rule: Persistence Pays Off

PSLF requires borrowers to make 120 qualifying payments while working full-time for a qualifying employer and enrolled in an IDR plan. These payments must be made on time and in full. It's important to note that these payments don't need to be consecutive. If you take a break from public service or switch employers, you can pick up where you left off as long as you meet the eligibility criteria when you resume making payments.

Navigating the PSLF Process: Tips for Success

- Document Everything: Keep meticulous records of your employment, loan payments, and enrollment in an IDR plan. This documentation will be crucial when applying for forgiveness.

- Submit the Employment Certification Form (ECF): This form verifies your qualifying employment and helps track your progress towards forgiveness. Submit it annually or whenever you change employers.

- Stay Informed: PSLF regulations can change. Regularly check the Federal Student Aid website for updates and guidance.

- Seek Professional Help: If you're unsure about your eligibility or the application process, consider consulting with a student loan counselor or attorney specializing in student loan debt.

PSLF offers a valuable opportunity for public servants to escape the burden of student loan debt. By understanding the eligibility requirements and diligently following the process, you can turn your commitment to service into a path towards financial freedom.

Unlock Debt-Free Future: Strategies to Get Student Loans Forgiven or Dismissed

You may want to see also

Explore related products

![]()

Loan Rehabilitation Programs Overview

Defaulted student loans cast a long shadow, impacting credit scores, wage garnishments, and even tax refunds. Yet, there exists a path to redemption: loan rehabilitation programs. These structured plans offer a lifeline to borrowers, allowing them to restore their loans to good standing and regain access to federal benefits.

Unlike forgiveness, which eliminates debt entirely, rehabilitation focuses on repairing the damage caused by default. It’s a commitment, requiring borrowers to make nine voluntary, on-time payments within a 10-month period. These payments are tailored to income, ensuring affordability for even those with limited means.

The process begins with contacting the loan holder or collection agency. They’ll outline the terms, including the monthly payment amount, which is typically 15% of discretionary income. Discretionary income is calculated by subtracting essential living expenses from total income. For example, a borrower earning $30,000 annually with modest expenses might have a monthly rehabilitation payment of around $150.

Rehabilitation isn’t instantaneous. Completing the nine payments removes the default from the borrower’s credit report, but it doesn’t erase the late payment history. However, it does restore eligibility for federal student aid, loan consolidation, and income-driven repayment plans. Think of it as a financial reset button, allowing borrowers to re-engage with their loans on more favorable terms.

It’s crucial to approach rehabilitation with determination. Missing payments can derail the process, requiring a fresh start. Borrowers should prioritize these payments, potentially adjusting budgets or seeking financial counseling for support.

While rehabilitation demands effort, the rewards are substantial. It’s a chance to break free from the consequences of default and rebuild financial stability. For those burdened by defaulted student loans, rehabilitation programs offer a tangible path toward a brighter financial future.

Using Your W-2 to Qualify for Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Statute of Limitations Impact

The statute of limitations on debt collection can significantly influence the fate of defaulted student loans, often determining whether borrowers face indefinite repayment or potential relief. This legal time frame varies by state, typically ranging from 3 to 10 years, after which creditors lose the right to sue for repayment. For defaulted student loans, understanding this timeline is crucial because it can limit the lender’s ability to enforce collection through legal means, such as wage garnishment or asset seizure. However, federal student loans, which constitute the majority of educational debt, are not subject to state statutes of limitations. Instead, they operate under federal law, which imposes no time limit on collection efforts. This distinction highlights the importance of knowing whether your loans are federal or private, as private loans may eventually fall outside the statute of limitations, offering a pathway to forgiveness through legal expiration.

Analyzing the impact of the statute of limitations reveals a strategic opportunity for borrowers with private defaulted student loans. Once the statute expires, lenders cannot successfully sue to collect the debt, though they may still attempt voluntary repayment. Borrowers should be cautious, however, as making a payment or acknowledging the debt in writing can reset the clock in some states. To leverage this, borrowers should first verify the statute of limitations in their state and confirm whether it has expired. If it has, they can respond to collection attempts by sending a certified letter demanding proof of the debt and asserting that the statute has lapsed. This approach can effectively halt aggressive collection tactics and, in some cases, lead to settlement offers for a fraction of the owed amount, indirectly achieving a form of forgiveness.

For federal student loans, the absence of a statute of limitations means borrowers must explore alternative forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. However, the statute of limitations still plays a role in one critical area: tax debt resulting from loan forgiveness. Under the Tax Cuts and Jobs Act of 2017, forgiven student loan balances are treated as taxable income, but the statute of limitations for IRS collection is generally 10 years. Borrowers who strategically delay addressing defaulted federal loans until closer to this deadline may face reduced tax liability if the forgiven amount is eventually collected. This requires careful planning, as prolonged default damages credit and increases accrued interest, but it underscores how understanding limitations periods can mitigate long-term financial consequences.

A comparative perspective reveals how the statute of limitations interacts with bankruptcy, another potential avenue for student loan forgiveness. While discharging student loans through bankruptcy is notoriously difficult, private loans may be eligible if the borrower can prove undue hardship. Here, the statute of limitations becomes a double-edged sword: if the statute has expired, the lender’s claim is weaker, potentially strengthening the borrower’s case for discharge. Conversely, federal loans remain exempt from such limitations, making bankruptcy a less viable option. Borrowers must weigh the risks of prolonged default against the possibility of partial relief through bankruptcy, using the statute of limitations as a strategic factor in their decision-making process.

Instructively, borrowers should take proactive steps to document and track the statute of limitations for their defaulted loans. Start by requesting a detailed loan history from the lender or servicer, noting the date of last payment and any subsequent collection activity. For private loans, consult a state-specific legal guide or attorney to confirm the applicable statute and its expiration date. If the statute has lapsed, respond to collection efforts in writing, citing the legal time frame and demanding cessation of contact. For federal loans, focus on rehabilitation programs or forgiveness pathways, but remain aware of the 10-year tax collection limit for future planning. By mastering the statute of limitations, borrowers can transform a seemingly insurmountable debt into a manageable—or even forgivable—obligation.

Amazon's Student Loan Forgiveness: Fact or Fiction? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Total and Permanent Disability Discharge

For borrowers facing overwhelming financial strain due to severe health issues, the Total and Permanent Disability (TPD) discharge program offers a critical lifeline. This federal initiative allows individuals with qualifying disabilities to eliminate their federal student loan debt entirely, providing a fresh start when medical challenges make repayment impossible.

Qualifying for TPD Discharge: A Three-Pronged Approach

To secure TPD discharge, borrowers must prove their inability to engage in substantial gainful activity due to a physical or mental impairment. Documentation requirements vary: veterans can submit VA disability determinations, Social Security Disability Insurance (SSDI) recipients must provide benefit award notices, and others need physician certification. Notably, SSDI applicants must be approved for benefits for at least five consecutive months before applying, while physician certifications require a doctor’s statement affirming the disability’s permanence.

The Monitoring Period: A Temporary Tether

Approval isn’t the final step. Discharged borrowers enter a three-year monitoring period where they must meet annual requirements: submitting earnings documentation, notifying the government of income exceeding the poverty line, and refraining from further federal student borrowing. Failure to comply can reinstate the debt, though exceptions exist for borrowers whose earnings exceed limits due to temporary increases.

Practical Tips for a Smooth Application

Navigating TPD discharge requires precision. Applicants should gather all medical records beforehand, ensure physicians understand the permanence requirement when certifying, and double-check SSA or VA paperwork for accuracy. For SSDI recipients, applying during the five-month waiting period expedites the process. Additionally, borrowers should monitor their email and mail for government communications to avoid missing critical deadlines during the monitoring phase.

The Broader Impact: Relief Beyond Repayment

TPD discharge not only eliminates debt but also removes the defaulted status from credit reports, though the discharge itself may appear. This distinction can improve creditworthiness over time. Moreover, discharged loans become tax-free starting in 2026 under current law, easing the financial burden further. For those whose disabilities have upended their financial futures, TPD discharge represents more than policy—it’s a pathway to stability.

College Misconduct? How to Secure Student Loan Forgiveness for Improper Practices

You may want to see also

Frequently asked questions

Yes, defaulted student loans can be forgiven through programs like Public Service Loan Forgiveness (PSLF), Total and Permanent Disability (TPD) discharge, or bankruptcy (though bankruptcy is rare and requires proving undue hardship).

A: Loan rehabilitation can remove the default status from your credit report, but it does not forgive the loan. However, once rehabilitated, you may become eligible for forgiveness programs like income-driven repayment (IDR) forgiveness.

A: There is no specific time limit for forgiveness, but certain programs have requirements, such as making qualifying payments for 10 years under PSLF or 20–25 years under IDR plans.

A: Private student loans are not eligible for federal forgiveness programs. However, some private lenders may offer settlement options or discharge in cases of borrower death or disability.

A: No, defaulting does not automatically qualify you for forgiveness. You must actively pursue forgiveness through eligible programs and meet their specific requirements.