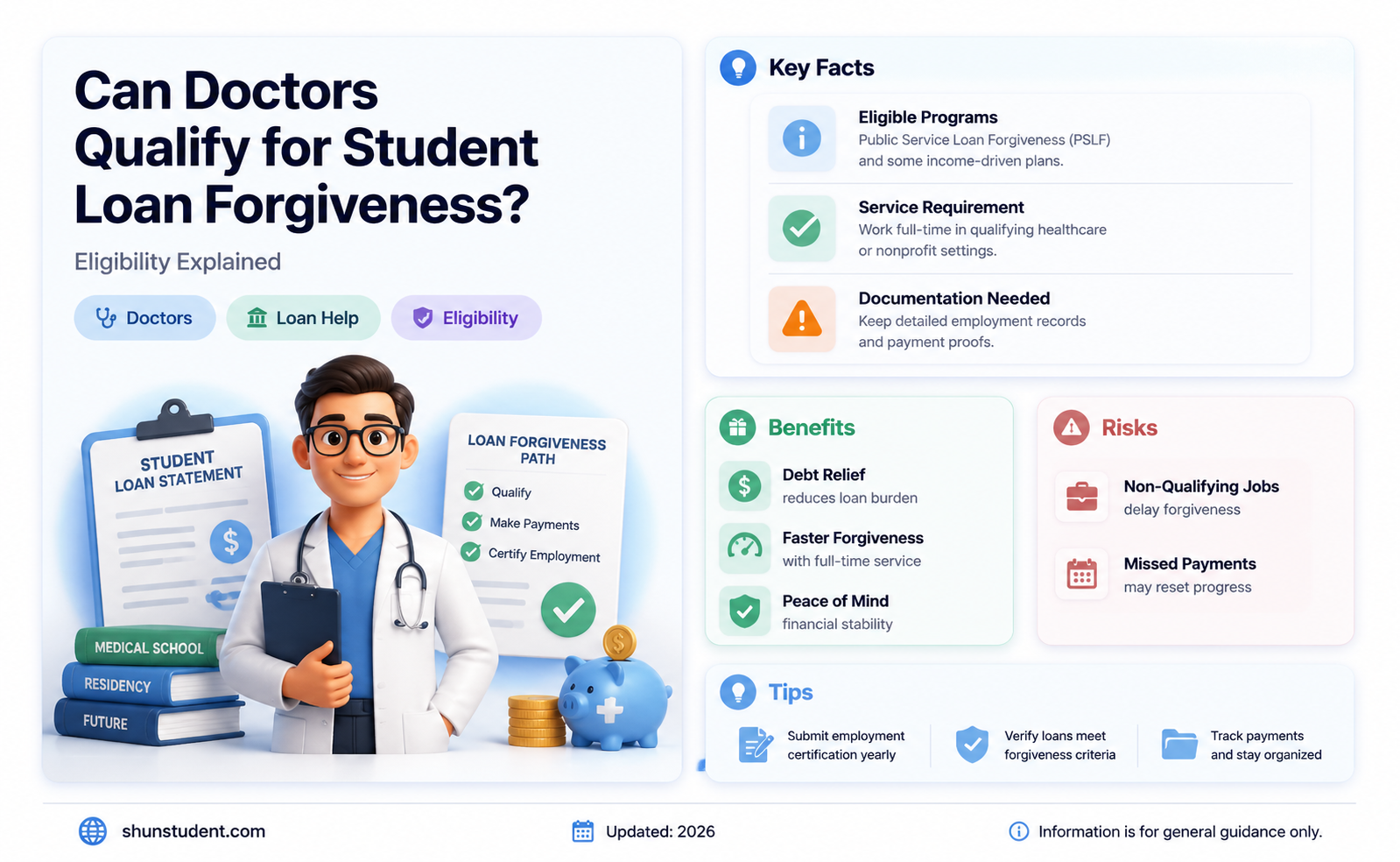

The topic of student loan forgiveness for doctors has gained significant attention in recent years, as many medical professionals face substantial debt after completing their education. With the high cost of medical school and the lengthy training required to become a physician, doctors often graduate with six-figure student loan balances. As a result, various programs and initiatives have been established to provide relief, raising the question: are doctors eligible for student loan forgiveness? Understanding the eligibility criteria, available programs, and potential benefits is crucial for medical professionals seeking to manage their debt and achieve financial stability in their careers.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness Programs | Yes, doctors are eligible for certain student loan forgiveness programs. |

| Public Service Loan Forgiveness (PSLF) | Eligible if employed full-time by a qualifying public service employer. |

| National Health Service Corps (NHSC) | Forgiveness for primary care providers working in Health Professional Shortage Areas (HPSAs). |

| State-Based Loan Repayment Programs | Varies by state; many states offer repayment assistance for doctors in underserved areas. |

| Income-Driven Repayment (IDR) Forgiveness | Eligible after 20–25 years of qualifying payments, depending on the plan. |

| Military Service Programs | Forgiveness options available for doctors serving in the military. |

| Employer-Based Forgiveness | Some hospitals or healthcare organizations offer loan repayment assistance. |

| Tax Implications | PSLF is tax-free; other programs may have taxable forgiven amounts. |

| Loan Type Requirement | Federal student loans (Direct Loans) are typically required for forgiveness. |

| Specialty Requirements | Some programs require primary care specialties (e.g., NHSC). |

| Service Commitment | Requires a commitment to serve in underserved or high-need areas. |

| Application Process | Requires documentation of employment and loan eligibility. |

| Recent Updates (2023) | Temporary PSLF waivers and expanded eligibility for IDR forgiveness. |

Explore related products

What You'll Learn

- Public Service Loan Forgiveness (PSLF) eligibility for medical professionals

- Income-driven repayment plans and loan forgiveness options for doctors

- National Health Service Corps (NHSC) loan repayment programs

- State-specific loan forgiveness programs for healthcare providers

- Military service loan repayment programs for medical officers

![]()

Public Service Loan Forgiveness (PSLF) eligibility for medical professionals

Medical professionals burdened by student loan debt often seek relief through Public Service Loan Forgiveness (PSLF), a federal program promising tax-free forgiveness after 120 qualifying payments. However, eligibility hinges on a strict set of criteria, and doctors must navigate a complex landscape to secure this benefit.

Unlike income-driven repayment plans, PSLF doesn't consider income level; instead, it rewards a decade of dedicated service in the public sector. This program is particularly appealing to physicians, whose educational debt often surpasses six figures.

Qualifying Employment: The Cornerstone of PSLF

The cornerstone of PSLF eligibility lies in qualifying employment. Doctors must work full-time for a qualifying employer, defined as a government organization at any level (federal, state, local, or tribal), a 501(c)(3) not-for-profit organization, or a not-for-profit organization providing certain types of public services. This encompasses a wide range of medical settings, including public hospitals, community health centers, academic medical centers affiliated with universities, and non-profit clinics serving underserved populations.

For example, a pediatrician working at a federally qualified health center or an emergency room physician employed by a county hospital would likely meet the employment criteria.

Loan Type and Repayment Plan: Crucial Details

Not all student loans are created equal when it comes to PSLF. Only Direct Loans, the most common type of federal student loan, qualify. If a doctor has Federal Family Education Loans (FFEL) or Perkins Loans, they must consolidate them into a Direct Consolidation Loan to be eligible.

Furthermore, borrowers must be enrolled in an income-driven repayment (IDR) plan. These plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE), cap monthly payments based on income and family size. This is crucial because PSLF requires 120 qualifying payments, and IDR plans often result in lower monthly payments, making it easier to fulfill the requirement.

Documentation and Vigilance: The Keys to Success

The PSLF application process demands meticulous documentation. Doctors should submit an Employment Certification Form (ECF) annually or whenever they change employers. This form verifies qualifying employment and ensures payments are counted towards forgiveness. Keeping detailed records of payments, employment history, and correspondence with loan servicers is essential. The PSLF program has faced criticism for its complex rules and past processing errors, making vigilance and proactive documentation crucial for a successful outcome.

A Path to Financial Freedom

While the PSLF program requires commitment and careful navigation, it offers a lifeline to doctors burdened by student loan debt. By understanding the eligibility criteria, choosing the right repayment plan, and maintaining meticulous records, medical professionals can leverage PSLF to achieve financial freedom and focus on their calling: providing quality healthcare.

Alabama Tax Benefits: Student Loan Forgiveness Explained for Borrowers

You may want to see also

Explore related products

![]()

Income-driven repayment plans and loan forgiveness options for doctors

Doctors burdened by six-figure student loan debt often overlook income-driven repayment (IDR) plans, assuming they’re only for low-income earners. This misconception is costly. While doctors’ salaries may seem high, IDR plans like Revised Pay As You Earn (REPAYE) and Pay As You Earn (PAYE) calculate payments based on discretionary income, factoring in high living expenses and family size. For instance, a doctor earning $200,000 with $300,000 in debt and a family of four could see monthly payments reduced by 30-50%, making these plans viable even for high earners.

The real game-changer for doctors lies in pairing IDR plans with Public Service Loan Forgiveness (PSLF). PSLF forgives remaining loan balances after 120 qualifying payments for those working full-time in nonprofit or government healthcare settings. For doctors in residency, fellowships, or employed by hospitals like Kaiser Permanente or Mayo Clinic, this combination can shave decades off repayment timelines. However, meticulous documentation is critical—each payment must be certified, and employment must be verified annually to qualify.

A lesser-known but equally valuable option is the National Health Service Corps (NHSC) Loan Repayment Program. Doctors committing to serve in Health Professional Shortage Areas (HPSAs) can receive up to $50,000 in loan repayment for a two-year commitment. For specialists like psychiatrists or OB-GYNs, this program not only alleviates debt but also addresses critical healthcare disparities. The NHSC’s State Loan Repayment Program (SLRP) offers additional funds, stacking with federal programs for maximum benefit.

While IDR and forgiveness programs offer relief, they’re not without pitfalls. REPAYE, for example, capitalizes unpaid interest annually, potentially increasing the principal balance. Doctors must also navigate tax implications of forgiven amounts, though the American Rescue Plan Act of 2021 temporarily exempts PSLF forgiveness from federal taxation through 2025. Strategic planning—such as switching to a lower-cost IDR plan during residency or maximizing PSLF eligibility—can mitigate these risks and optimize outcomes.

Ultimately, doctors have more pathways to student loan forgiveness than they realize, but success requires proactive, informed decision-making. By leveraging IDR plans, PSLF, and targeted repayment programs like NHSC, even doctors with staggering debt can achieve financial stability. The key is to act early, stay organized, and seek expert guidance to navigate the complexities of these programs effectively.

Stop Student Loan Forgiveness Calls: Effective Strategies to End Harassment

You may want to see also

Explore related products

![]()

National Health Service Corps (NHSC) loan repayment programs

Doctors burdened by student loan debt can find significant relief through the National Health Service Corps (NHSC) loan repayment programs. These initiatives, designed to address healthcare shortages in underserved areas, offer a compelling opportunity for eligible physicians. In exchange for a commitment to serve in Health Professional Shortage Areas (HPSAs), participants receive substantial financial assistance, effectively reducing or eliminating their educational debt.

The NHSC offers two primary repayment programs: the NHSC Loan Repayment Program (NHSC LRP) and the NHSC Substance Use Disorder (SUD) Workforce Loan Repayment Program. The NHSC LRP provides up to $50,000 in loan repayment for a two-year service commitment, with the possibility of additional awards for extended service. The SUD Workforce LRP, tailored to address the opioid crisis, offers up to $75,000 for a three-year commitment. Both programs prioritize primary care providers, including physicians, nurse practitioners, and physician assistants, working in federally designated HPSAs.

Eligibility for these programs hinges on several factors. Physicians must hold an unrestricted license to practice in their state and be employed or have an offer of employment at an NHSC-approved site. The application process is competitive, with priority given to those serving in areas with the greatest need. Applicants must also demonstrate a commitment to providing care to underserved populations, regardless of their ability to pay.

One of the most appealing aspects of the NHSC programs is their flexibility. Physicians can choose to serve in rural, urban, or tribal communities, depending on their interests and career goals. Additionally, the programs cover a wide range of specialties, including family medicine, internal medicine, pediatrics, and psychiatry. This inclusivity ensures that a diverse array of healthcare professionals can contribute to improving access to care while alleviating their financial burdens.

For doctors considering the NHSC loan repayment programs, careful planning is essential. Prospective applicants should research approved service sites early, as availability can vary by location and specialty. It’s also crucial to understand the tax implications of loan repayment awards, as they are considered taxable income. Finally, physicians should weigh the long-term benefits of serving in an underserved area against the immediate financial relief, ensuring alignment with their personal and professional aspirations. By leveraging these programs, doctors can make a meaningful impact on public health while achieving financial stability.

Are Current Students Eligible for Loan Forgiveness Programs?

You may want to see also

![]()

State-specific loan forgiveness programs for healthcare providers

Doctors burdened by student loan debt can find relief through state-specific loan forgiveness programs designed to attract and retain healthcare providers in underserved areas. These programs vary widely in eligibility criteria, award amounts, and service requirements, making it crucial for physicians to research options tailored to their location and specialty.

While federal programs like Public Service Loan Forgiveness (PSLF) offer broad eligibility, state programs often provide more targeted benefits, addressing specific healthcare shortages within their borders.

California's Solution: The Steven M. Thompson Loan Forgiveness Program

A standout example is California's Steven M. Thompson Loan Forgiveness Program, offering up to $106,000 in loan repayment assistance to primary care physicians, dentists, and mental health providers who commit to serving in federally designated Health Professional Shortage Areas (HPSAs) for two years. This program prioritizes providers working in medically underserved communities, ensuring access to care for vulnerable populations.

Key Takeaway: California's program demonstrates how states can incentivize healthcare professionals to address critical shortages by offering substantial financial relief tied to specific service commitments.

Practical Tip: Physicians interested in California's program should verify their practice location's HPSA designation and carefully review the application deadlines and required documentation.

A Patchwork of Opportunities: Exploring Regional Variations

Beyond California, a patchwork of state-specific programs exists, each with unique features. For instance, New York's Doctors Across New York program provides up to $20,000 annually for up to five years to physicians practicing in underserved areas, while Texas offers the Physician Education Loan Repayment Program, targeting primary care physicians and psychiatrists with awards up to $160,000 over four years. Comparative Analysis: While award amounts vary, most programs share common eligibility criteria, including practicing in designated shortage areas, committing to a minimum service period, and demonstrating financial need.

Navigating the Application Process: A Strategic Approach

Securing state loan forgiveness requires strategic planning. Steps: 1. Identify Relevant Programs: Research state-specific programs through government websites, professional associations, and loan forgiveness databases. 2. Assess Eligibility: Carefully review program criteria, ensuring your specialty, practice location, and financial situation align with requirements. 3. Prepare Documentation: Gather necessary documents, including loan statements, employment contracts, and proof of service in underserved areas. 4. Meet Deadlines: Submit applications well before deadlines, allowing time for review and potential follow-up. Caution: Be mindful of program-specific obligations, such as maintaining licensure and fulfilling service commitments, to avoid repayment penalties.

State-specific loan forgiveness programs offer a valuable lifeline for doctors struggling with student loan debt. By strategically targeting underserved areas, these programs not only alleviate financial burdens but also improve access to healthcare for communities in need. Physicians willing to commit to serving in these areas can significantly reduce their debt while making a meaningful impact on public health.

Dependent Students and Loan Forgiveness: Eligibility and Key Considerations

You may want to see also

![]()

Military service loan repayment programs for medical officers

Medical officers in the military often face significant student loan debt after years of rigorous education and training. Fortunately, the U.S. military offers robust loan repayment programs designed specifically for these professionals, providing a pathway to financial relief in exchange for service. These programs are not only a strategic recruitment tool but also a means to retain highly skilled medical personnel in critical roles. For doctors considering military service, understanding these programs can be a game-changer in managing educational debt.

One of the most prominent programs is the Financial Assistance Program (FAP) offered by the U.S. Army, Navy, and Air Force. Under FAP, medical officers can receive up to $40,000 annually for three years toward their student loans, totaling $120,000. This program is available to physicians, dentists, and other healthcare professionals who commit to active duty service. For example, a newly commissioned Army doctor could see a substantial portion of their $200,000+ medical school debt eliminated within the first few years of service. The repayment begins after completion of residency or internship, making it particularly appealing for early-career doctors.

Another key program is the Health Professions Loan Repayment Program (HPLRP), which offers up to $50,000 annually for three years, totaling $150,000, in exchange for a three-year service commitment. This program is available to physicians serving in underserved areas or in roles deemed critical by the military. Unlike FAP, HPLRP is often targeted at specific specialties, such as emergency medicine or psychiatry, where demand is high. For instance, a Navy psychiatrist stationed on a remote base could qualify for this program, significantly reducing their financial burden while serving their country.

While these programs offer substantial benefits, there are important considerations. First, the repayment amounts are taxable income, which reduces the net benefit. Second, service commitments typically range from three to four years, during which doctors must adhere to military standards and deployments. Lastly, eligibility often depends on factors like specialty, location, and current military needs. Prospective applicants should carefully review program requirements and consult with a military recruiter to ensure alignment with their career goals.

In conclusion, military service loan repayment programs provide a viable and lucrative option for medical officers seeking student loan forgiveness. By committing to serve in critical roles, doctors can significantly reduce or eliminate their debt while gaining unique professional experiences. These programs not only alleviate financial stress but also contribute to a sense of purpose and service, making them an attractive option for those willing to combine medicine with military life.

Unlocking Student Debt Forgiveness: A Step-by-Step Guide to Claiming Relief

You may want to see also

Frequently asked questions

Not all doctors are eligible for student loan forgiveness. Eligibility depends on factors such as the type of loan, repayment plan, employment (e.g., working in underserved areas or for nonprofit/government organizations), and participation in specific programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans.

Private student loans are generally not eligible for forgiveness programs. Forgiveness options typically apply only to federal student loans, such as Direct Loans, which are the most common type held by medical professionals.

Doctors can qualify for PSLF by making 120 qualifying payments while working full-time for a qualifying employer (e.g., government, nonprofit, or certain healthcare organizations) and being on an income-driven repayment plan. After meeting these requirements, the remaining federal loan balance may be forgiven tax-free.

Yes, programs like the National Health Service Corps (NHSC) Loan Repayment Program offer loan forgiveness for doctors who commit to serving in Health Professional Shortage Areas (HPSAs). The amount forgiven depends on the service commitment length and full-time or part-time status.

Yes, income-driven repayment plans (e.g., PAYE, REPAYE, IBR) can lead to loan forgiveness after 20–25 years of qualifying payments, depending on the plan. However, the forgiven amount may be taxed as income, unlike PSLF, which is tax-free.