Credit union employees, like many other professionals, may wonder if they qualify for student loan forgiveness programs. While credit unions are not-for-profit financial institutions, their employees typically do not fall under the Public Service Loan Forgiveness (PSLF) program unless the credit union is a government entity or a 501(c)(3) organization. However, some credit union employees might still be eligible for other forgiveness programs, such as income-driven repayment plans or state-specific initiatives, depending on their employment status, loan type, and repayment history. It’s essential for credit union employees to explore their options, review the specific requirements of each program, and consult with their loan servicer or a financial advisor to determine their eligibility for student loan forgiveness.

| Characteristics | Values |

|---|---|

| Eligibility for PSLF (Public Service Loan Forgiveness) | Credit union employees may be eligible if their employer is a qualifying non-profit or government organization. Most credit unions are not government entities but may qualify if they meet specific IRS 501(c)(3) criteria. |

| Employer Certification | Credit unions must be certified as qualifying employers under PSLF. Many credit unions do not meet this requirement unless they are non-profit or government-affiliated. |

| Loan Type Requirement | Only federal Direct Loans qualify for PSLF. Other loan types (e.g., FFEL, Perkins) must be consolidated into Direct Loans. |

| Payment Requirements | 120 qualifying payments (10 years) are required while working full-time for a qualifying employer. Payments must be made under an income-driven repayment plan. |

| Non-Profit Credit Unions | Employees of credit unions with 501(c)(3) status may qualify for PSLF. Most credit unions are not 501(c)(3) organizations. |

| Temporary Expanded PSLF (TEPSLF) | Credit union employees may benefit from TEPSLF if they have previously made payments under non-qualifying plans but meet other PSLF criteria. |

| State-Specific Programs | Some states offer student loan forgiveness programs for credit union employees, but these are rare and vary by location. |

| Federal Employment Status | Credit unions are generally not federal employers, so employees typically do not qualify for federal employee-specific forgiveness programs. |

| Income-Driven Repayment Plans | Required for PSLF eligibility. Credit union employees must enroll in an IDR plan to qualify. |

| Tax Implications | PSLF is tax-free, but forgiven amounts under other programs may be taxable depending on state and federal laws. |

| Recent Policy Changes | As of 2023, no specific changes have been made to include credit union employees broadly under PSLF, but waivers and expansions may apply in certain cases. |

Explore related products

What You'll Learn

![]()

Public Service Loan Forgiveness (PSLF) eligibility for credit union workers

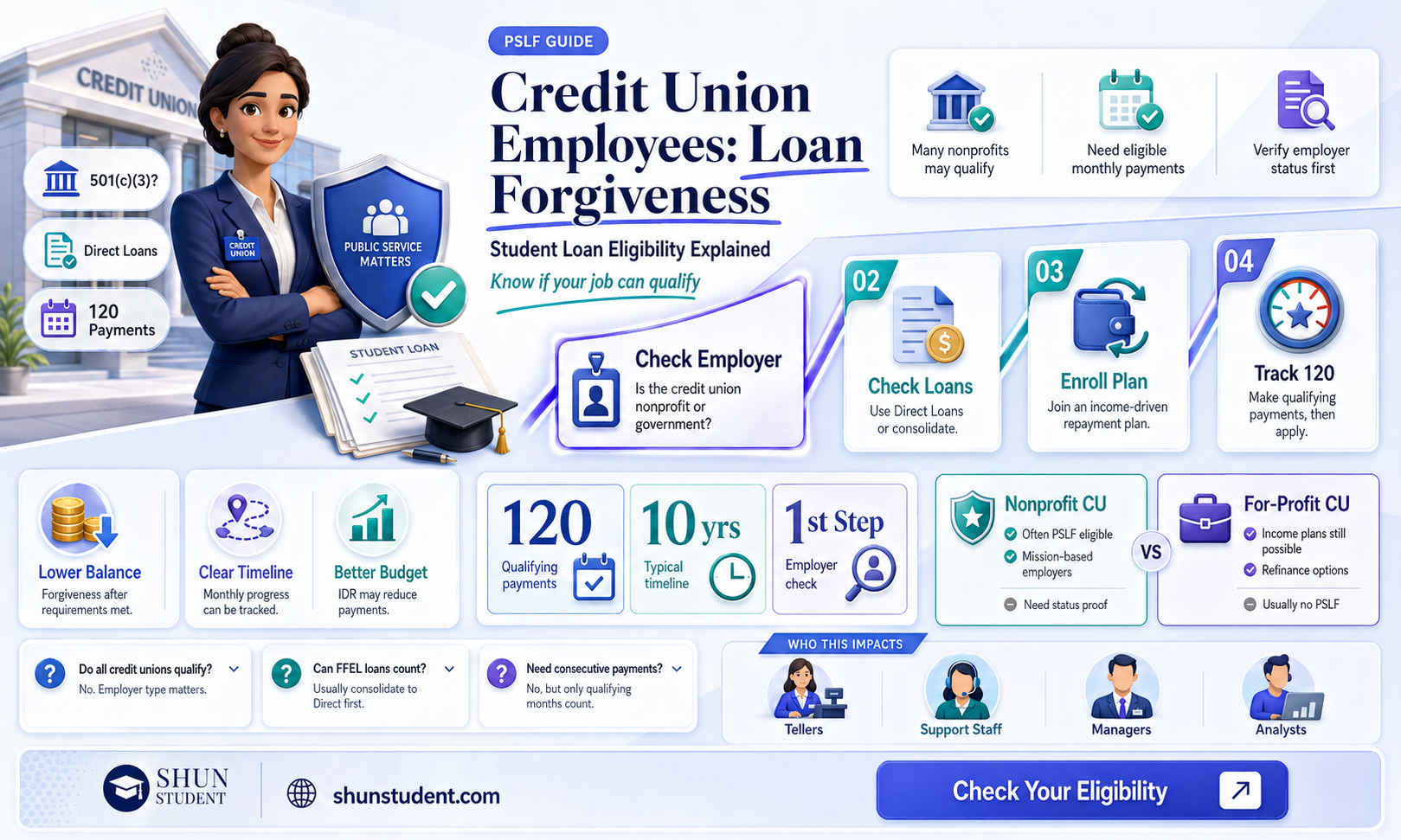

Credit union employees often wonder if their roles qualify them for Public Service Loan Forgiveness (PSLF), a federal program designed to forgive student debt after 120 qualifying payments. The key to eligibility lies in the employer’s classification, not the employee’s specific duties. Credit unions, as not-for-profit financial cooperatives, frequently meet the program’s requirement for tax-exempt status under Section 501(c)(3) of the Internal Revenue Code or as a government organization. This means most credit union workers are in a strong position to pursue PSLF, provided they follow the program’s strict guidelines.

To qualify, credit union employees must first ensure their loans are in the Direct Loan program, as only these loans are eligible for PSLF. If loans are in another federal program, such as FFEL or Perkins, consolidation into a Direct Consolidation Loan is necessary. Next, workers must enroll in an income-driven repayment (IDR) plan, which caps monthly payments at a percentage of discretionary income. Popular IDR plans include Revised Pay As You Earn (REPAYE) and Income-Based Repayment (IBR). Each payment made under an IDR plan while employed full-time by a qualifying employer counts toward the 120-payment requirement.

A critical but often overlooked step is submitting the Employment Certification Form (ECF) periodically. This form verifies that both the employer and the repayment plan meet PSLF criteria. Credit union employees should submit the ECF annually or when changing jobs to ensure payments are tracked accurately. Failure to certify employment can result in payments not counting toward forgiveness, even if all other criteria are met. The ECF also helps identify potential issues early, such as incorrect repayment plans or loan types.

One challenge for credit union workers is the program’s strict definition of full-time employment, which aligns with the employer’s definition or 30 hours per week, whichever is greater. Part-time employees, even if working for a qualifying employer, are not eligible for PSLF. Additionally, credit unions with for-profit subsidiaries or affiliations may complicate eligibility, as only the specific not-for-profit entity qualifies. Employees should verify their employer’s tax status using the IRS Tax Exempt Organization Search tool to confirm eligibility.

In conclusion, credit union employees have a unique advantage in pursuing PSLF due to their employers’ not-for-profit status. By consolidating loans into the Direct Loan program, enrolling in an IDR plan, and diligently certifying employment, workers can systematically work toward debt forgiveness. While the process requires attention to detail and adherence to strict guidelines, the potential to eliminate student debt after a decade of service makes PSLF a valuable opportunity for those in the credit union sector.

Combining Student Loan Forgiveness and Repayment: What You Need to Know

You may want to see also

Explore related products

![]()

Non-profit status of credit unions and loan forgiveness

Credit unions, often recognized for their member-focused approach, operate under a unique non-profit structure that sets them apart from traditional banks. This non-profit status is a critical factor when examining the eligibility of their employees for student loan forgiveness programs. Unlike for-profit institutions, credit unions are member-owned cooperatives, which means their primary goal is to serve their members rather than maximize profits. This distinction raises questions about how their employees fit into the criteria for loan forgiveness programs, particularly those designed for public service or non-profit workers.

To understand the implications, consider the Public Service Loan Forgiveness (PSLF) program, which forgives federal student loans after 120 qualifying payments for those employed full-time by a government or non-profit organization. Credit unions, classified as 501(c)(14) organizations under the IRS tax code, generally qualify as non-profits. However, the devil is in the details. Employees must work directly for a 501(c)(3) organization or a government entity to be eligible for PSLF. While most credit unions fall under 501(c)(14), some may also hold a 501(c)(3) status if they meet additional criteria, such as providing low-income services. This dual classification complicates eligibility, as employees must verify their employer’s specific tax status to determine if their employment qualifies for PSLF.

For credit union employees, navigating these nuances requires proactive steps. First, verify the credit union’s tax classification by requesting a Determination Letter from the IRS or checking the IRS Tax Exempt Organization Search tool. If the credit union operates under 501(c)(14) alone, employees may not qualify for PSLF unless they work in a department that serves low-income populations and is separately classified as 501(c)(3). Second, ensure that loan payments are made under an income-driven repayment plan, as this is a requirement for PSLF. Third, submit an Employment Certification Form annually to confirm eligibility and track qualifying payments. These steps are essential to avoid the common pitfall of assuming non-profit status automatically qualifies for loan forgiveness.

While PSLF is a prominent program, credit union employees should also explore alternative forgiveness options. For instance, the Federal Perkins Loan Cancellation program offers forgiveness for certain public service roles, including those in non-profit organizations. Additionally, state-based loan repayment assistance programs (LRAPs) may provide relief for employees working in underserved communities. For example, New York’s “Get on Your Feet” LRAP targets recent graduates working in non-profit or public sector jobs, including credit unions serving low-income members. By broadening their search beyond PSLF, employees can uncover opportunities tailored to their specific circumstances.

In conclusion, the non-profit status of credit unions creates both opportunities and challenges for employees seeking student loan forgiveness. While their cooperative structure aligns with the spirit of many forgiveness programs, the specific tax classification and job role determine eligibility. By understanding these intricacies and taking proactive steps to verify qualifications, credit union employees can maximize their chances of benefiting from available programs. This approach not only alleviates financial burden but also reinforces the mission-driven nature of their work in serving communities.

Cancer and Student Loan Forgiveness: Exploring Options for Financial Relief

You may want to see also

Explore related products

![]()

Income-driven repayment plans for credit union employees

Credit union employees, like many other professionals, often seek ways to manage their student loan debt effectively. One viable option is enrolling in income-driven repayment (IDR) plans, which adjust monthly payments based on income and family size. These plans can significantly reduce financial strain, especially for those in the nonprofit or public sectors, including credit unions. However, understanding eligibility and the nuances of these plans is crucial to maximizing their benefits.

To qualify for an IDR plan, credit union employees must first have eligible federal student loans, such as Direct Loans or Federal Family Education Loans (FFEL) that are consolidated into a Direct Consolidation Loan. Once eligibility is confirmed, borrowers can choose from four main IDR plans: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Each plan calculates payments differently, typically capping them at 10-20% of discretionary income. For instance, REPAYE limits payments to 10% of discretionary income for all borrowers, while IBR caps payments at 10% or 15%, depending on when the first loan was disbursed.

A key advantage of IDR plans for credit union employees is the potential for loan forgiveness after 20-25 years of qualifying payments. This feature is particularly beneficial for those with high loan balances relative to their income. For example, a credit union employee earning $45,000 annually with $60,000 in student debt could see monthly payments drop from $600 under the Standard Repayment Plan to $200 under REPAYE, with forgiveness after 25 years. However, borrowers must recertify their income and family size annually to remain in the program, as payments adjust based on these factors.

While IDR plans offer relief, they are not without drawbacks. One significant consideration is tax implications. Any forgiven amount after 20-25 years may be treated as taxable income, potentially resulting in a substantial tax bill. Additionally, credit union employees should be aware that payments under IDR plans may not cover accruing interest, leading to loan balance growth over time. To mitigate this, borrowers can make extra payments toward the principal when financially feasible.

In conclusion, income-driven repayment plans provide a practical solution for credit union employees managing student loan debt. By carefully selecting the most suitable plan, staying on top of annual recertification, and planning for potential tax liabilities, borrowers can navigate their repayment journey more effectively. While not a one-size-fits-all solution, IDR plans offer a structured path toward financial stability and eventual loan forgiveness.

Accountants and Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Federal vs. private student loan forgiveness options

Credit union employees, like many other professionals, often seek student loan forgiveness as a means to alleviate financial burden. Understanding the differences between federal and private student loan forgiveness options is crucial, as eligibility, programs, and benefits vary significantly. Federal student loans offer a range of forgiveness programs tailored to specific careers, income levels, and repayment plans, whereas private loans typically lack standardized forgiveness options, relying instead on lender discretion or refinancing strategies.

Analytical Perspective: Federal student loan forgiveness programs are designed with public service and financial need in mind. For instance, the Public Service Loan Forgiveness (PSLF) program forgives remaining balances after 120 qualifying payments for those working full-time in eligible public service jobs, including credit union roles if the employer qualifies as a nonprofit or government organization. In contrast, private lenders rarely offer forgiveness, focusing instead on profit. However, some credit unions may provide employer-assisted repayment benefits as part of their employee perks, bridging the gap between federal and private loan solutions.

Instructive Approach: To maximize forgiveness opportunities, credit union employees should first determine their loan type. Federal loans can be managed through income-driven repayment plans, which cap monthly payments at a percentage of discretionary income and offer forgiveness after 20–25 years, depending on the plan. For private loans, employees should explore refinancing options to lower interest rates or negotiate directly with lenders for hardship assistance. Additionally, leveraging employer benefits, such as tuition reimbursement or student loan contributions, can supplement limited private loan forgiveness options.

Comparative Analysis: Federal forgiveness programs provide clear pathways but require strict adherence to eligibility criteria. For example, PSLF demands consistent employment in qualifying roles and timely payments under an approved plan. Private loan forgiveness, while rare, may be achievable through refinancing with credit unions that offer special programs for members. However, refinancing federal loans into private ones eliminates access to federal forgiveness programs, making this a trade-off that requires careful consideration.

Practical Tips: Credit union employees should annually review their loan status and explore all available resources. Federal loan holders can use the Department of Education’s Loan Simulator to estimate forgiveness timelines under different plans. For private loans, employees should inquire about employer partnerships or credit union-specific refinancing deals. Keeping detailed records of payments and employment is essential for federal forgiveness applications, while maintaining a strong credit profile improves refinancing prospects for private loans.

By understanding these distinctions and taking proactive steps, credit union employees can navigate the complexities of student loan forgiveness, whether federal or private, to achieve financial stability.

Did Obama Pass a Law to Forgive Student Loans?

You may want to see also

Explore related products

![]()

Certification process for credit union employee forgiveness

Credit union employees seeking student loan forgiveness must navigate a certification process that hinges on their eligibility under specific federal programs, primarily the Public Service Loan Forgiveness (PSLF) program. Unlike direct government employment, credit union roles require careful documentation to prove their nonprofit or public service status. The first step involves confirming that the credit union is a qualifying employer, typically by verifying its 501(c)(1), 501(c)(3), or government-affiliated designation. Employees must submit an Employer Certification Form (ECF) annually or when switching jobs to ensure consistent eligibility tracking.

The ECF serves as the backbone of the certification process, requiring detailed employer information, including tax identification numbers and signatures from authorized officials. For credit union employees, this step is critical because misclassification of the employer’s status can derail forgiveness eligibility. For instance, while federal credit unions often qualify, state-chartered credit unions must prove their nonprofit status through IRS documentation. Employees should retain copies of submitted ECFs and follow up with their loan servicer to confirm receipt and processing, as delays or errors are common.

A lesser-known but equally important aspect is the role of the loan type and repayment plan. Only Direct Loans qualify for PSLF, so employees with FFEL or Perkins Loans must consolidate them into the Direct Loan program before applying for certification. Additionally, borrowers must enroll in an income-driven repayment (IDR) plan, such as PAYE or REPAYE, to ensure payments count toward forgiveness. Credit union employees should calculate their qualifying payments carefully, as partial or late payments do not count, and switching plans mid-repayment can reset the 120-payment counter.

One practical tip for streamlining the certification process is to maintain a personal record of all employment and payment history. This includes pay stubs, tax returns, and correspondence with loan servicers. Should disputes arise regarding employer eligibility or payment counts, this documentation can expedite resolution. Moreover, employees should monitor legislative changes, as expansions to PSLF or new forgiveness programs could simplify or alter the certification requirements in the future.

In conclusion, the certification process for credit union employee forgiveness demands meticulous attention to employer status, loan type, and repayment plan adherence. By proactively verifying eligibility, submitting accurate ECFs, and maintaining comprehensive records, employees can navigate this complex process effectively. While the steps may seem daunting, the potential for significant loan forgiveness makes the effort worthwhile for those committed to a career in public service through credit unions.

Student Loan Forgiveness Dates: What Borrowers Need to Know

You may want to see also

Frequently asked questions

Yes, credit union employees may be eligible for student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), if they meet the program’s requirements, including working full-time for a qualifying employer and making 120 eligible payments.

Credit union employees must work full-time for a qualifying employer (such as a nonprofit or government organization), have eligible federal student loans, and make 120 qualifying payments under an income-driven repayment plan to qualify for programs like PSLF.

No, credit union employees are generally not eligible for PSLF if their credit union is a for-profit organization. PSLF requires employment with a government organization, 501(c)(3) nonprofit, or other qualifying public service employer.