Income-based student loan forgiveness has become a critical topic for borrowers seeking relief from mounting educational debt. These programs, such as Income-Driven Repayment (IDR) plans, adjust monthly payments based on the borrower’s income and family size, offering a more manageable repayment structure. After a specified period, typically 20 to 25 years, any remaining balance may be forgiven, though borrowers may face tax implications on the forgiven amount. However, eligibility criteria, repayment terms, and the potential for policy changes under different administrations create complexities for borrowers navigating these options. As student debt continues to burden millions, understanding the nuances of income-based forgiveness programs is essential for those seeking financial stability and long-term relief.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Eligibility | Available after 20-25 years of qualifying payments under income-driven plans. |

| Income-Driven Repayment Plans | Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), Income-Contingent Repayment (ICR). |

| Forgiveness Tax Implications | Forgiveness amounts may be taxable as income (exceptions apply under certain plans). |

| Qualifying Payments | Payments must be made under an income-driven plan and count toward the 20-25 year requirement. |

| Public Service Loan Forgiveness (PSLF) | Separate program offering forgiveness after 10 years for public service employees. |

| Remaining Balance After Forgiveness | Any remaining balance is forgiven but may be taxed (except for PSLF). |

| Loan Type Eligibility | Only federal Direct Loans are eligible; FFEL or Perkins Loans must be consolidated. |

| Payment Amount | Payments are capped at 10-20% of discretionary income, depending on the plan. |

| Recertification Requirement | Income and family size must be recertified annually to maintain eligibility. |

| Recent Updates (2023-2024) | Temporary changes under the Biden administration may shorten forgiveness timelines or expand eligibility. |

Explore related products

What You'll Learn

- Eligibility Criteria: Income thresholds, repayment plans, and loan types for forgiveness

- Public Service Loan Forgiveness (PSLF): Requirements for public sector workers

- Income-Driven Repayment (IDR): Forgiveness after 20-25 years of payments

- Tax Implications: Forgiven amounts as taxable income

- Loan Consolidation: Impact on forgiveness eligibility and timelines

![]()

Eligibility Criteria: Income thresholds, repayment plans, and loan types for forgiveness

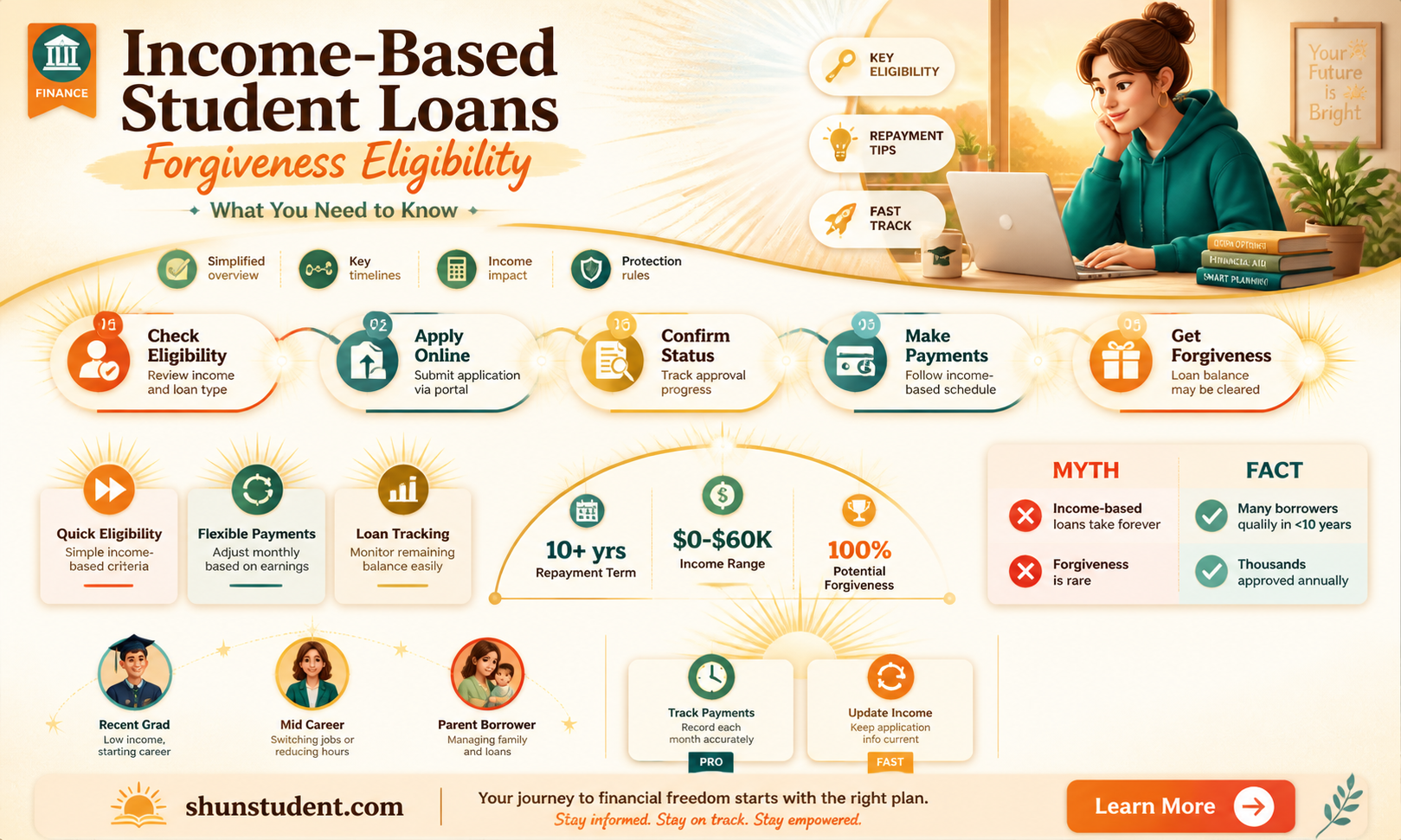

Income-driven repayment (IDR) plans are a lifeline for borrowers struggling to manage federal student loan payments, but forgiveness isn’t automatic. To qualify, you must meet specific income thresholds, enroll in an eligible repayment plan, and hold qualifying loan types. Here’s how it breaks down: income thresholds determine your monthly payment, typically capped at 10-20% of your discretionary income, depending on the plan. For example, if your annual income is $40,000 and your family size is two, your discretionary income might be calculated as the difference between your income and 150% of the federal poverty guideline, resulting in lower monthly payments. These reduced payments are a stepping stone to forgiveness, which typically occurs after 20-25 years of consistent payments, depending on the plan.

Repayment plans like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR) each have unique eligibility rules. For instance, REPAYE is available to all borrowers with eligible loans, while PAYE requires proof of partial financial hardship. Choosing the right plan is critical, as it affects both your monthly payment and the timeline for forgiveness. For example, if you’re pursuing Public Service Loan Forgiveness (PSLF), you must enroll in an IBR or PAYE plan and work full-time for a qualifying employer. Missteps here can delay or disqualify you from forgiveness, so careful selection is key.

Not all federal loans qualify for income-driven forgiveness. Direct Loans, including subsidized and unsubsidized Stafford Loans, PLUS Loans (for graduates and professionals), and consolidation loans, are eligible. However, Federal Family Education Loans (FFEL) and Perkins Loans must be consolidated into a Direct Consolidation Loan to qualify. Private loans are entirely ineligible, regardless of your income or repayment plan. For example, if you have a mix of Direct and FFEL loans, consolidating them into a Direct Consolidation Loan is a necessary step to access IDR forgiveness.

Understanding the interplay between income thresholds, repayment plans, and loan types is essential for maximizing your chances of forgiveness. For instance, if your income is below 150% of the federal poverty guideline, your payment under IBR could be as low as $0, and these months still count toward forgiveness. However, beware of potential pitfalls: unpaid interest can capitalize under certain plans, increasing your balance, and forgiven amounts may be taxable unless you qualify for PSLF. Regularly recertifying your income and staying informed about policy changes, such as the recent IDR Account Adjustment, can help you navigate this complex process effectively.

In summary, eligibility for income-driven student loan forgiveness hinges on meeting income thresholds, enrolling in the right repayment plan, and holding qualifying loan types. By strategically aligning these factors, borrowers can reduce their monthly payments and work toward forgiveness. Practical steps include consolidating ineligible loans, choosing the optimal repayment plan, and staying vigilant about recertification deadlines. While the process is intricate, understanding these criteria empowers borrowers to take control of their financial future.

Understanding IDR Student Loan Forgiveness: A Comprehensive Guide to Eligibility

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Requirements for public sector workers

Public Service Loan Forgiveness (PSLF) offers a lifeline to public sector workers burdened by student debt, but qualifying isn’t automatic. To unlock this benefit, borrowers must meet specific criteria, starting with employment. You must work full-time for a qualifying employer, which includes government organizations at any level (federal, state, local), 501(c)(3) nonprofits, and some other nonprofit organizations that provide public services. Part-time workers can also qualify if they meet the employer’s definition of full-time or work at least 30 hours per week. This requirement underscores the program’s focus on rewarding long-term commitment to public service.

Next, your loan type matters. Only Direct Loans are eligible for PSLF. If you have Federal Family Education Loans (FFEL) or Perkins Loans, you’ll need to consolidate them into a Direct Consolidation Loan to qualify. Additionally, your repayment plan must be income-driven, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), or Revised Pay As You Earn (REPAYE). These plans tie your monthly payments to your income, making them manageable while you work toward forgiveness. Failure to enroll in an income-driven plan can disqualify you, even if you meet all other criteria.

The timeline is another critical factor. Borrowers must make 120 qualifying payments while employed full-time in public service. These payments must be made on time, in full, and under an eligible repayment plan. Periods of deferment, forbearance, or economic hardship typically don’t count toward the 120 payments. A practical tip: Submit the Employment Certification Form annually to ensure your payments are tracking correctly. This form also helps identify any issues early, such as an ineligible employer or repayment plan.

Despite its benefits, PSLF has a reputation for complexity and strict requirements. For instance, working for a nonprofit doesn’t automatically qualify you—the organization must meet specific criteria. Similarly, payments made under the wrong repayment plan or before consolidating ineligible loans won’t count. To navigate these pitfalls, borrowers should consult the Federal Student Aid website or a loan servicer specializing in PSLF. Persistence and attention to detail are key, as the program’s rules leave little room for error.

In conclusion, PSLF is a powerful tool for public sector workers, but it demands careful planning and adherence to specific rules. By focusing on eligible employment, loan types, repayment plans, and payment tracking, borrowers can position themselves to eliminate their student debt after a decade of service. While the process is rigorous, the reward—full loan forgiveness—is well worth the effort for those committed to a career in public service.

Missouri's Tax Rules on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment (IDR): Forgiveness after 20-25 years of payments

For borrowers grappling with federal student loan debt, Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income. What’s less understood is the forgiveness component: after 20–25 years of consistent payments, the remaining balance is erased. This isn’t a loophole—it’s a built-in feature designed to prevent lifelong debt servitude for low- and middle-income earners. However, the clock resets with certain actions, such as switching plans or missing payments, so borrowers must navigate this path with precision.

Consider the mechanics: IDR plans like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Based Repayment (IBR) calculate payments as 10–20% of discretionary income, depending on the plan and enrollment date. For instance, a borrower earning $40,000 annually with a family size of two might pay as little as $200 monthly under REPAYE. Over 20–25 years, this structured affordability ensures that payments align with income, not debt size. Yet, the trade-off is time—and potentially, a tax bill on the forgiven amount, though current law exempts IDR forgiveness from taxation through 2025.

A critical caveat emerges in the details: not all payments count equally. Only payments made while enrolled in an IDR plan qualify toward the 20–25-year forgiveness threshold. Forbearance, deferment, or payments under the Standard plan do not advance the clock. For example, a borrower who pauses payments for 12 months due to economic hardship will extend their forgiveness timeline by a year. Similarly, consolidating loans can reset the payment count, so strategic planning is essential.

To maximize IDR forgiveness, borrowers should annually recertify their income and family size to ensure payments remain accurate. Tools like the Federal Student Aid website streamline this process, allowing updates to be submitted online. Additionally, tracking payment eligibility through loan servicer portals prevents surprises. For those nearing the forgiveness threshold, documenting every payment is crucial—errors in servicer records are not uncommon, and proof of eligibility can resolve disputes.

In practice, IDR forgiveness is a marathon, not a sprint. It demands patience, vigilance, and a proactive approach to managing debt. For borrowers earning modest incomes or pursuing public service careers, it’s a viable path to financial freedom. However, it’s not a one-size-fits-all solution—high-income earners may pay off their loans before reaching the forgiveness threshold, while others may find alternative strategies like Public Service Loan Forgiveness (PSLF) more advantageous. Understanding these nuances transforms IDR from a vague promise into a tactical tool for debt resolution.

Florida's Tax Rules on Student Loan Forgiveness: What You Need to Know

You may want to see also

Explore related products

![]()

Tax Implications: Forgiven amounts as taxable income

Forgiven student loan amounts can trigger unexpected tax bills, a consequence often overlooked by borrowers celebrating debt relief. The Internal Revenue Service (IRS) generally considers forgiven debt as taxable income, meaning the amount wiped away could resurface as a liability come tax season. This rule applies to income-driven repayment (IDR) plans, which promise loan forgiveness after 20–25 years of qualifying payments. For instance, a borrower with $50,000 forgiven under Pay As You Earn (PAYE) might face a tax bill as if they’d earned an extra $50,000 that year. Understanding this nuance is critical, as it can turn a financial windfall into a budgetary challenge.

The tax treatment of forgiven student loans hinges on the concept of "taxable cancellation of debt income." When a lender forgives a debt, the IRS views it as income received, subject to federal income tax. However, exceptions exist. The American Rescue Plan Act of 2021 temporarily exempts student loan forgiveness from federal taxation through 2025, a relief measure aimed at pandemic recovery. Yet, this exemption doesn’t apply to all forgiveness programs or state taxes. For example, Public Service Loan Forgiveness (PSLF) recipients are federally exempt, but borrowers in states like California or New York may still owe state taxes on forgiven amounts. Navigating these layers requires vigilance and often professional advice.

Strategic planning can mitigate the tax impact of forgiven student loans. One approach is to align forgiveness with a year of lower income, reducing the marginal tax bracket and, consequently, the tax burden. For instance, a borrower nearing retirement might time their forgiveness to coincide with reduced earnings. Another tactic is to explore tax credits or deductions, such as the Student Loan Interest Deduction, to offset taxable income. Additionally, consulting a tax professional can uncover state-specific exemptions or installment payment plans to ease the financial strain. Proactive measures transform a potential tax trap into a manageable financial event.

Comparing the tax implications of different forgiveness programs highlights the importance of informed decision-making. While IDR plans and PSLF offer pathways to forgiveness, their tax treatments differ. IDR forgiveness, outside the temporary exemption period, typically incurs taxes, whereas PSLF remains tax-free. Private loan forgiveness, often negotiated through settlement, is almost always taxable. Borrowers must weigh these differences against their financial goals and tax situations. For example, a borrower with high income might prioritize PSLF to avoid future tax liabilities, while another with fluctuating income could leverage the temporary exemption window. Each program’s tax profile demands careful consideration to maximize benefits and minimize surprises.

Ultimately, the tax implications of forgiven student loans underscore the need for holistic financial planning. Borrowers must view forgiveness not as an endpoint but as one piece of a larger puzzle. Tools like tax-advantaged retirement accounts, charitable deductions, or even health savings accounts can offset taxable income from forgiveness. Staying informed about legislative changes, such as extensions to the tax exemption, is equally vital. By integrating tax strategy into their repayment plan, borrowers can turn the challenge of forgiven debt into an opportunity for financial optimization, ensuring relief today doesn’t become a burden tomorrow.

Did Obama Sign a Student Loan Forgiveness Program? Facts Revealed

You may want to see also

Explore related products

![]()

Loan Consolidation: Impact on forgiveness eligibility and timelines

Loan consolidation can reset the clock on your forgiveness timeline, potentially delaying the day you become debt-free. When you consolidate multiple federal student loans into a single Direct Consolidation Loan, any progress you’ve made toward income-driven repayment (IDR) forgiveness is erased. For example, if you’ve already made 5 years of qualifying payments under an IDR plan, consolidating will restart your forgiveness counter to zero. This is because the new consolidated loan is considered a single, new loan with its own repayment history. For borrowers pursuing Public Service Loan Forgiveness (PSLF), consolidation is particularly risky: only payments made *after* consolidation count toward the required 120 qualifying payments.

Consider this scenario: A teacher with $50,000 in federal loans has been making payments under the Revised Pay As You Earn (REPAYE) plan for 7 years, aiming for forgiveness after 20 years. If they consolidate to lower their monthly payment, those 7 years of progress vanish, and the forgiveness timeline extends another 20 years from the consolidation date. However, consolidation can sometimes simplify repayment by combining multiple loans into one, making it easier to manage and track payments. The key is to weigh the benefits of lower monthly payments against the cost of losing progress toward forgiveness.

To minimize the impact on forgiveness timelines, borrowers should consolidate strategically. First, ensure all loans eligible for IDR or PSLF are included in the consolidation. Second, time the consolidation carefully—ideally after reaching a significant milestone (e.g., 10 years of payments) or when switching to a more forgiving repayment plan. Third, use the Federal Student Aid Loan Simulator to model how consolidation affects your forgiveness timeline and total repayment amount. For PSLF borrowers, consolidating before submitting the PSLF form can disqualify prior payments, so consult with your loan servicer beforehand.

A cautionary note: Private loan consolidation (refinancing) is not the same as federal loan consolidation and typically eliminates access to IDR plans and forgiveness programs altogether. Always stick to federal consolidation if preserving forgiveness eligibility is a priority. Additionally, consolidating default loans can restart the clock on rehabilitation, but it won’t remove the default from your credit report. Borrowers over 50 may find consolidation less appealing, as extending the repayment timeline could push forgiveness into retirement years, potentially affecting tax liability.

In conclusion, loan consolidation is a double-edged sword for forgiveness seekers. While it can streamline repayment and lower monthly payments, it often comes at the cost of resetting forgiveness timelines. Borrowers must carefully evaluate their financial goals, repayment history, and eligibility for forgiveness programs before consolidating. For those nearing the forgiveness threshold, consolidation may do more harm than good. Conversely, borrowers with multiple loans and no significant progress toward forgiveness might find consolidation a practical way to simplify their repayment strategy. Always consult resources like the Department of Education’s Federal Student Aid website or a certified loan counselor to make an informed decision.

Biden's Student Loan Forgiveness: Duration and Long-Term Impact Explained

You may want to see also

Frequently asked questions

Yes, income-driven repayment (IDR) plans offer loan forgiveness after 20–25 years of qualifying payments, depending on the plan and type of loan.

To qualify for forgiveness, payments must be made consistently under an IDR plan. Inconsistent payments may not count toward the required 20–25 years.

Under current law, forgiven amounts under IDR plans may be taxed as income, unless you qualify for exceptions like Public Service Loan Forgiveness (PSLF).