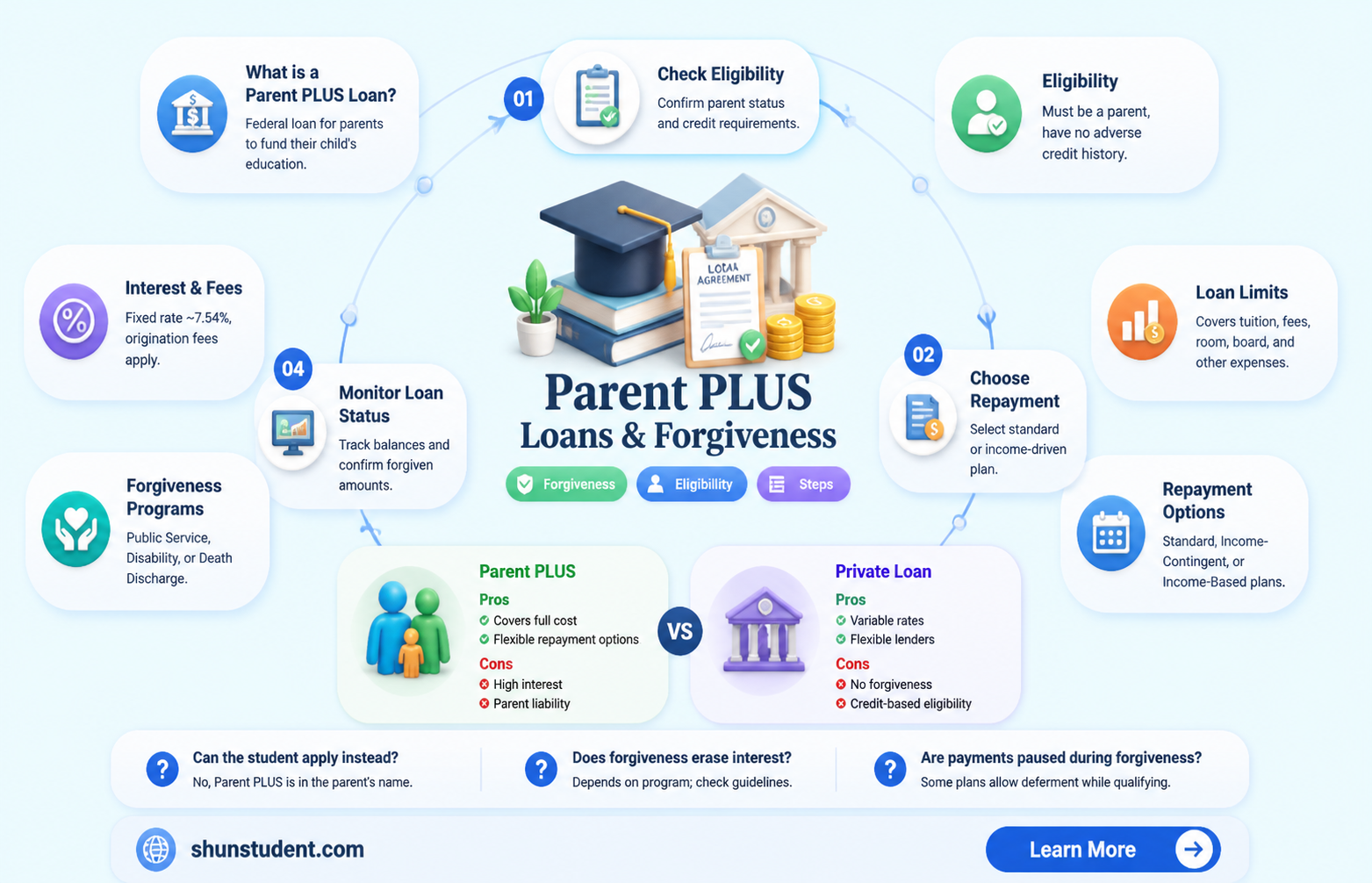

Parent PLUS loans are a federal loan option allowing parents to borrow money to cover their child’s educational expenses, but their inclusion in student loan forgiveness programs has been a topic of significant debate and confusion. Unlike traditional student loans taken out directly by students, Parent PLUS loans are held by the parent borrower, which complicates eligibility for forgiveness programs like Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) plans. While Parent PLUS loans can be consolidated into a Direct Consolidation Loan and potentially qualify for IDR plans, they are not automatically included in broad student loan forgiveness initiatives, such as those proposed or implemented by the federal government. Borrowers must carefully review program requirements and consider consolidation or repayment strategies to maximize their chances of benefiting from available forgiveness options.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Parent PLUS loans are eligible for forgiveness under specific programs. |

| Programs Including Parent PLUS Loans | Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) plans, and limited one-time adjustments (e.g., 2023 IDR Account Adjustment). |

| Requirements for PSLF | Borrower must make 120 qualifying payments while working full-time for a qualifying employer. Loan must be consolidated into a Direct Consolidation Loan. |

| Income-Driven Repayment (IDR) Forgiveness | Forgiveness after 20-25 years of qualifying payments, depending on the plan. Parent PLUS loans must be consolidated into a Direct Consolidation Loan and enrolled in an IDR plan. |

| One-Time Adjustments | Parent PLUS loans may benefit from temporary adjustments, such as the 2023 IDR Account Adjustment, which counts time in repayment toward forgiveness, even if payments were not previously qualifying. |

| Exclusion from Broad Forgiveness Plans | Parent PLUS loans are generally excluded from broad student loan forgiveness initiatives, such as the Biden administration's one-time cancellation (up to $20,000) for federal student loans. |

| Consolidation Requirement | Parent PLUS loans must be consolidated into a Direct Consolidation Loan to qualify for PSLF or IDR forgiveness. |

| Interest Capitalization | Consolidation may trigger interest capitalization, increasing the loan balance. |

| Transferability to Student | Parent PLUS loans cannot be transferred to the student, limiting repayment options. |

| Current Policy (as of 2023) | Parent PLUS loans remain eligible for PSLF and IDR forgiveness but are excluded from most broad forgiveness initiatives. |

Explore related products

What You'll Learn

- Eligibility Criteria: Parent PLUS loans may qualify for forgiveness under specific programs like PSLF or IDR

- PSLF Requirements: Parent PLUS loans can be forgiven after 120 qualifying payments under PSLF

- Income-Driven Repayment: Forgiveness for Parent PLUS loans is possible through IDR plans after 20-25 years

- Consolidation Rules: Parent PLUS loans must be consolidated into a Direct Loan for IDR eligibility

- Biden Forgiveness Plan: Parent PLUS loans were not explicitly included in the 2022 forgiveness plan

![]()

Eligibility Criteria: Parent PLUS loans may qualify for forgiveness under specific programs like PSLF or IDR

Parent PLUS loans, often a lifeline for families funding higher education, can indeed be eligible for forgiveness under specific programs. However, the path to forgiveness is not automatic and requires careful navigation of eligibility criteria. Two primary programs stand out: the Public Service Loan Forgiveness (PSLF) program and Income-Driven Repayment (IDR) plans. Each has distinct requirements, but both offer a potential route to debt relief for Parent PLUS loan borrowers.

To qualify for PSLF, the borrower must work full-time for a qualifying employer, such as a government or not-for-profit organization, and make 120 eligible payments under a qualifying repayment plan. Here’s the catch: Parent PLUS loans are not eligible for PSLF unless they are consolidated into a Direct Consolidation Loan and repaid under an income-driven plan. This consolidation step is crucial, as it allows Parent PLUS loans to access IDR plans, which are otherwise unavailable to them. Once consolidated, the borrower can switch to an IDR plan like Income-Contingent Repayment (ICR), the only IDR plan available for consolidated Parent PLUS loans.

IDR plans offer forgiveness after 20 or 25 years of qualifying payments, depending on the plan. For Parent PLUS loans under ICR, forgiveness occurs after 25 years. However, borrowers must remain in the plan and make payments based on their income and family size. It’s essential to recertify income and family size annually to ensure continued eligibility. A practical tip: keep detailed records of payments and employment, especially for PSLF, as documentation is critical for approval.

Comparing PSLF and IDR, PSLF offers faster forgiveness (10 years vs. 25 years) but requires public service employment. IDR, while slower, is more flexible and accessible to all borrowers, including those in the private sector. For Parent PLUS loan holders, the choice depends on career path and financial situation. For example, a parent working in public education might prioritize PSLF, while one in a lower-paying private sector job might lean toward IDR.

In conclusion, Parent PLUS loans can qualify for forgiveness, but the process demands proactive steps. Consolidation into a Direct Loan, enrollment in an IDR plan, and adherence to program requirements are non-negotiable. Whether pursuing PSLF or IDR, understanding the eligibility criteria and taking timely action can turn the possibility of forgiveness into a reality. For borrowers, the key takeaway is this: forgiveness is achievable, but it requires strategy and persistence.

Understanding Student Loan Forgiveness: Payments Required for Debt Relief

You may want to see also

Explore related products

![]()

PSLF Requirements: Parent PLUS loans can be forgiven after 120 qualifying payments under PSLF

Parent PLUS loans, often taken out by parents to fund their child's education, can indeed be forgiven under the Public Service Loan Forgiveness (PSLF) program. This is a critical piece of information for parents burdened by education debt, as it offers a pathway to financial relief. However, the process is not automatic and requires careful navigation of specific requirements. To qualify, the loan must be in the parent's name, and the parent must be employed full-time by a qualifying public service organization. This includes government entities, non-profit organizations with 501(c)(3) status, and certain other non-profits providing public services.

The first step is to ensure the Parent PLUS loan is consolidated into a Direct Consolidation Loan. Only Direct Loans are eligible for PSLF, and since Parent PLUS loans are originally issued as part of the Federal Family Education Loan (FFEL) Program or Direct Loan Program, consolidation is often necessary. After consolidation, the parent must enroll in an income-driven repayment (IDR) plan. This step is crucial because IDR plans cap monthly payments at a percentage of the borrower’s discretionary income, making it easier to manage payments while working in public service. Popular IDR plans include Income-Contingent Repayment (ICR), which is the only IDR plan available for Parent PLUS loans after consolidation.

Once enrolled in an IDR plan, the parent must make 120 qualifying payments. These payments must be made on time, in full, and while employed full-time by a qualifying employer. It’s essential to track these payments meticulously, as the Department of Education’s count may differ from the borrower’s records. Submitting the Employment Certification Form (ECF) annually or whenever switching employers can help ensure payments are accurately counted. This form verifies employment and payment eligibility, reducing the risk of disqualification later.

A common pitfall is assuming all non-profit employment qualifies. Only organizations with 501(c)(3) status or those providing specific public services, such as emergency management or public education, meet PSLF criteria. Parents should confirm their employer’s eligibility using the Department of Education’s Employer Search Tool. Additionally, part-time employment is not sufficient; the parent must work at least 30 hours per week for the qualifying employer. Combining part-time jobs to meet the hourly requirement is not allowed unless both employers are eligible.

Finally, after completing 120 qualifying payments, the parent must submit the PSLF application to receive forgiveness. This process can take several months, so it’s advisable to apply as soon as eligibility is met. Forgiveness under PSLF is tax-free, providing significant financial relief. However, parents should remain vigilant about maintaining their eligibility throughout the 10-year repayment period, as changes in employment or repayment plan can disrupt progress. With careful planning and adherence to these requirements, Parent PLUS loans can be forgiven, offering a lifeline to parents committed to public service.

Student Loan Forgiveness: A Boost or Burden to National Debt?

You may want to see also

Explore related products

![]()

Income-Driven Repayment: Forgiveness for Parent PLUS loans is possible through IDR plans after 20-25 years

Parent PLUS loans, often a lifeline for families funding higher education, can feel like a financial albatross. But there’s a glimmer of hope: Income-Driven Repayment (IDR) plans offer a pathway to forgiveness after 20 to 25 years of qualifying payments. Unlike traditional repayment plans, IDR ties monthly payments to income and family size, making them more manageable for borrowers with limited cash flow. For parents who took out PLUS loans, this means the possibility of eventual forgiveness, though the journey is neither short nor simple.

To qualify for IDR forgiveness, Parent PLUS loans must first be consolidated into a Direct Consolidation Loan. This step is non-negotiable, as PLUS loans are ineligible for IDR plans in their original form. Once consolidated, borrowers can enroll in an IDR plan such as Income-Contingent Repayment (ICR), the only plan available for consolidated Parent PLUS loans. Under ICR, payments are calculated as 20% of discretionary income or the amount you’d pay on a fixed payment plan over 12 years, adjusted for income, whichever is less. This structure ensures payments remain proportional to earnings, a critical feature for parents with fluctuating or modest incomes.

The clock on forgiveness starts ticking once you’re in an IDR plan, but the timeline varies. For Parent PLUS loans consolidated under ICR, forgiveness occurs after 25 years of qualifying payments. While this may seem daunting, it’s a finite endpoint, unlike the indefinite repayment terms of standard plans. Borrowers must also be mindful of tax implications: forgiven amounts may be considered taxable income, though current laws offer temporary relief through 2025 under the American Rescue Plan. Consulting a tax professional can help navigate this potential financial hurdle.

Practical tips can smooth the path to forgiveness. First, recertify your income and family size annually to ensure payments remain aligned with your financial situation. Missing recertification can lead to higher payments or capitalization of interest. Second, track your qualifying payments meticulously; errors in payment counts are common and can delay forgiveness. Finally, consider making payments during periods of low income, as IDR plans can calculate payments as low as $0, which still count toward forgiveness. With patience and strategy, Parent PLUS loan forgiveness through IDR is not just possible—it’s a realistic goal.

Forgiveness Options for Stafford Student Loans Through Peace Corps Service

You may want to see also

Explore related products

![]()

Consolidation Rules: Parent PLUS loans must be consolidated into a Direct Loan for IDR eligibility

Parent PLUS loans, designed for parents to finance their child's education, often leave borrowers grappling with repayment options. Unlike traditional student loans, these loans aren't automatically eligible for Income-Driven Repayment (IDR) plans, which can cap monthly payments based on income and family size. This exclusion can be a significant hurdle for parents facing financial strain.

Here's the crucial rule: Parent PLUS loans must be consolidated into a Direct Consolidation Loan to become eligible for IDR plans. This consolidation process essentially transforms the PLUS loan into a new Direct Loan, opening the door to potentially lower monthly payments.

Think of it as a financial reshuffling. By consolidating, you're essentially creating a new loan with terms that allow for IDR plan enrollment. This can be a lifeline for parents struggling to meet the standard repayment requirements of Parent PLUS loans.

The Consolidation Process: A Step-by-Step Guide

- Eligibility Check: Ensure your Parent PLUS loans are in good standing (not in default).

- Application: Submit a Direct Consolidation Loan application through the Federal Student Aid website.

- Loan Selection: Carefully select the Parent PLUS loans you wish to consolidate.

- Repayment Plan Choice: During the application, choose an IDR plan that suits your financial situation. Options include Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR).

- Review and Submit: Double-check all information for accuracy before submitting your application.

Important Considerations:

- Interest Rates: Consolidation doesn't lower your interest rate; it's a weighted average of the rates on the loans being consolidated.

- Forgiveness: While IDR plans offer forgiveness after a certain number of qualifying payments (typically 20-25 years), the forgiven amount may be taxable as income.

- Credit Impact: Consolidation can temporarily lower your credit score due to the new loan inquiry.

The Takeaway:

Consolidating Parent PLUS loans into a Direct Loan is a strategic move for parents seeking the benefits of IDR plans. It provides a pathway to more manageable monthly payments and potential loan forgiveness down the line. Remember, careful planning and understanding the implications are crucial before proceeding with consolidation.

Biden Student Loan Forgiveness: Step-by-Step Application Guide for Borrowers

You may want to see also

Explore related products

![]()

Biden Forgiveness Plan: Parent PLUS loans were not explicitly included in the 2022 forgiveness plan

The Biden administration's 2022 student loan forgiveness plan aimed to alleviate the financial burden on millions of borrowers, but it left many parents in a state of uncertainty. Parent PLUS loans, a federal loan program allowing parents to borrow for their child's education, were notably absent from the explicit provisions of this plan. This omission has sparked confusion and concern among families who had hoped for relief.

Understanding the Exclusion: The 2022 forgiveness plan primarily targeted borrowers with federal student loans held by the Department of Education, offering up to $20,000 in relief for Pell Grant recipients and $10,000 for others. However, the plan's language did not specifically mention Parent PLUS loans, which are technically held by the parent, not the student. This distinction is crucial, as it places these loans in a different category, potentially excluding them from the forgiveness criteria.

Impact on Borrowers: For parents who have taken on significant debt to support their child's education, this exclusion can be devastating. Parent PLUS loans often carry higher interest rates and less flexible repayment options compared to traditional student loans. Without explicit inclusion in forgiveness programs, these borrowers may continue to struggle with repayment, especially if they are nearing retirement age or facing financial hardships.

Advocacy and Potential Solutions: Advocacy groups and lawmakers have recognized this gap in the forgiveness plan. Some propose expanding the eligibility criteria to include Parent PLUS loans, arguing that these borrowers should not be penalized for supporting their children's education. Others suggest creating separate relief programs tailored to the unique circumstances of parent borrowers. As the debate continues, it is essential for affected parents to stay informed and engage with policymakers to ensure their voices are heard.

Practical Steps for Affected Parents: In the absence of immediate solutions, parents with PLUS loans can take proactive steps. First, explore income-contingent repayment plans, which can adjust monthly payments based on income and family size. Second, consider loan consolidation, which may provide access to additional repayment options. Lastly, stay updated on legislative developments and participate in advocacy efforts to push for inclusive student loan forgiveness policies. While the 2022 plan may not have addressed Parent PLUS loans, ongoing discussions offer hope for future relief.

Understanding Student Loan Forgiveness: Key Qualifications and Eligibility Criteria

You may want to see also

Frequently asked questions

Yes, Parent PLUS loans are eligible for certain student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) forgiveness, provided they meet the program’s specific requirements.

Yes, Parent PLUS loans can qualify for PSLF if the borrower works full-time for a qualifying public service employer and makes 120 eligible payments under a repayment plan like Income-Contingent Repayment (ICR).

Yes, Parent PLUS loans can be included in IDR forgiveness after consolidating them into a Direct Consolidation Loan and enrolling in the Income-Contingent Repayment (ICR) plan. Forgiveness typically occurs after 20–25 years of qualifying payments.

It depends on the specific program. For example, the 2022 one-time forgiveness program did not include Parent PLUS loans unless they were held by the Department of Education and met certain income criteria. Always check the program’s eligibility rules.

Yes, Parent PLUS loans are discharged if the student borrower dies or becomes permanently disabled. However, the loan is not discharged if the parent borrower dies or becomes disabled, unless the parent consolidates the loan into their own Direct Consolidation Loan.