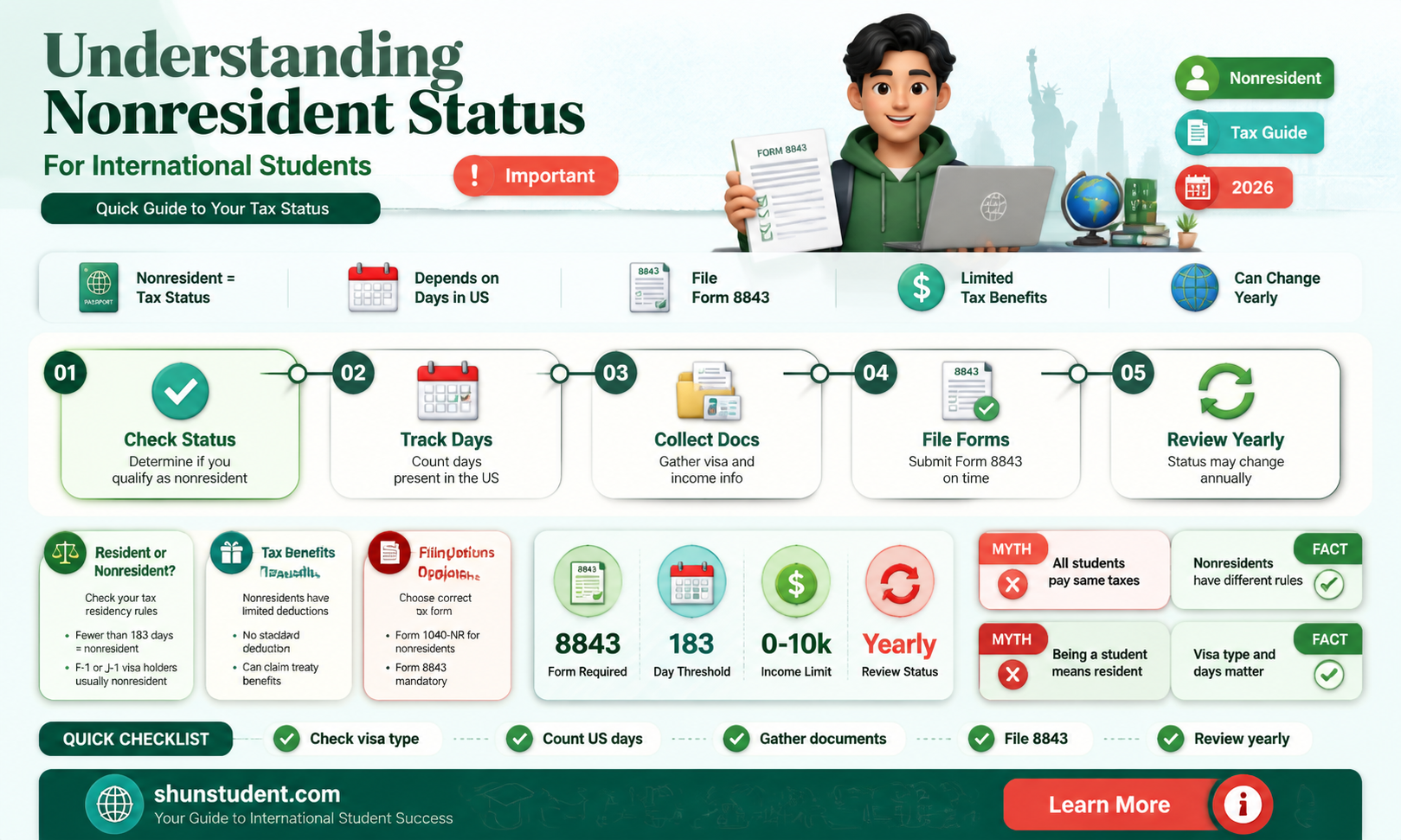

International students on F-1, J-1, or M-1 visas in the United States are generally considered nonresident aliens for tax purposes for their first five calendar years in the country. This status affects how they are taxed and which tax forms they need to fill out. After five years, they may become resident aliens for tax purposes, which is distinct from residency status for tuition or permanent residency purposes. Nonresident aliens are typically liable for Social Security and Medicare taxes on wages earned in the US, with some exceptions based on their nonimmigrant status.

| Characteristics | Values |

|---|---|

| Tax residency status | Nonresident alien for tax purposes for the first 5 calendar years |

| Tax form | 1040-NR |

| Tax treaty | The US has income tax treaties with 65 countries, which can reduce or eliminate US tax on pensions, interest, dividends, royalties, and capital gains |

| Social Security and Medicare taxes | Exempt for the first 5 calendar years |

| FICA taxes | Exempt for the first 5 calendar years |

| Substantial Presence Test | Required to pass to be considered a resident for tax purposes |

Explore related products

What You'll Learn

- International students with F-1, J-1, or M-1 visas are considered nonresident aliens for tax purposes for their first five calendar years in the US

- After five years, international students may become resident aliens for tax purposes

- Resident status for tax purposes does not equate to residency by other definitions

- Nonresident aliens are liable for Social Security and Medicare taxes on wages for services performed in the US

- Nonresident aliens can be exempt from US tax under tax treaties

![]()

International students with F-1, J-1, or M-1 visas are considered nonresident aliens for tax purposes for their first five calendar years in the US

The year an international student enters the US is counted as their first year, even if they were only in the country for part of that year. After five calendar years, international students with F-1, J-1, or M-1 visas may become resident aliens for tax purposes if they meet the "Substantial Presence Test." This test determines tax residency status and is based on physical presence in the US over a three-year period, including the current calendar year and the two preceding years.

It is important to note that being a "resident" for tax purposes does not equate to being a resident by other definitions, such as for tuition or immigration purposes. Additionally, certain exemptions may apply based on the student's nonimmigrant status and the services performed. For example, students employed by the school, college, or university where they are enrolled at least half-time may be exempt from Social Security and Medicare taxes, regardless of their tax residency status.

To confirm their tax residency status and ensure accurate tax filing, international students are advised to use tax preparation software or seek guidance from tax professionals. The specific tax obligations and exemptions may vary depending on individual circumstances and the specific terms of their visas.

In summary, international students with F-1, J-1, or M-1 visas are typically considered nonresident aliens for tax purposes during their first five calendar years in the US, after which their tax residency status may change based on their physical presence and other factors.

Understanding Tax Benefits: International Students and American Opportunity

You may want to see also

Explore related products

![]()

After five years, international students may become resident aliens for tax purposes

International students in the United States on F-1, J-1, or M-1 non-immigrant status are generally considered non-resident aliens for tax purposes for their first five calendar years in the country. This means that these students are exempt from Social Security Tax and Medicare Tax on wages paid to them for services performed within the United States. However, after five years of residing in the US, these students may become resident aliens for tax purposes and are then liable for Social Security and Medicare taxes.

It is important to note that the year an international student enters the US counts as their first year, even if they were only in the country for part of that year. To determine residency for tax purposes, international students can use resources such as the Internal Revenue Service (IRS) "Introduction to Residency Under US Tax Law" and IRS Publication 519. Additionally, the GLACIER Tax Prep program can help students determine their residency status for federal tax filing purposes.

If an international student is considered a non-resident alien for tax purposes, they can use specific tax preparation software, such as GLACIER Tax Prep, to complete their federal tax forms. On the other hand, resident aliens for tax purposes file taxes in the same manner as US citizens and residents, and they may take advantage of tax software for residents, such as TurboTax or H&R Block basic tax software. It is important to note that "resident for tax purposes" is solely a tax filing status and does not equate to residency by other definitions, such as for tuition purposes or as a US permanent resident.

In addition to the time-based criteria for determining tax residency, international students on F-1, J-1, or M-1 visas must also meet the "Substantial Presence Test" to be considered resident aliens for US tax purposes. This test considers the number of days an individual has been physically present in the US over a three-year period, including the current calendar year and the two preceding years. To meet this test, an individual must be present in the US for at least 183 days during this three-year period.

How International Students Can E-File Their Taxes

You may want to see also

Explore related products

![]()

Resident status for tax purposes does not equate to residency by other definitions

The concept of "resident status" for tax purposes is distinct from residency definitions in other contexts. While international students may be classified as "nonresident aliens" or "resident aliens" for taxation, this does not equate to residency for tuition or immigration purposes. This tax residency status solely determines taxation rates and the applicable tax forms to be completed.

International students on F-1, J-1, or M-1 visas are typically considered nonresident aliens for tax purposes during their first five calendar years in the United States. This classification exempts them from certain taxes, such as Social Security and Medicare taxes on wages earned for services performed within the country. However, they are still liable for taxes on income from US sources and may need to file specific tax forms, such as Form 1040-NR.

After five years, international students may become "resident aliens" for tax purposes, subject to meeting the “Substantial Presence Test." This change in tax residency status can impact their tax liabilities and the applicable tax forms. It's important to note that this shift in tax status does not grant students residency for other purposes, such as tuition or immigration.

While tax residency status is crucial for accurately filing taxes, it operates independently from other residency definitions. International students should be mindful of their tax obligations and consult reliable sources or professionals to understand their specific situation and ensure compliance with tax laws.

In summary, the term "resident status" in the context of taxation is unique to that domain and should not be conflated with residency definitions in other contexts, such as tuition or immigration. International students need to be aware of their tax residency status to fulfil their tax obligations correctly, but this status does not confer the same rights or benefits as residency in other contexts.

Work-Study Eligibility: International Students at CSUN

You may want to see also

![]()

Nonresident aliens are liable for Social Security and Medicare taxes on wages for services performed in the US

Whether an international student is a nonresident alien or a resident alien for tax purposes depends on their visa status and the length of their stay in the US. Students in F or J status are considered nonresident aliens for tax purposes for the first five calendar years of their stay in the US. Scholars in J status are considered nonresident aliens for the first two calendar years.

Nonresident aliens are generally liable for Social Security and Medicare taxes on wages for services performed in the US. However, there are certain exemptions based on their nonimmigrant status. For example, nonresident alien students in F-1, J-1, or M-1 status for less than five calendar years are exempt from Social Security and Medicare taxes on wages for services performed within the US. To qualify for this exemption, the services performed must be allowed by the United States Citizenship and Immigration Services (USCIS) for their nonimmigrant statuses and must be carried out to fulfil the purposes for which such visas were issued.

Similarly, NRA scholars, trainees, teachers, or researchers in J-1 or Q-1 status are exempt from Social Security and Medicare taxes on wages for services performed within the US. However, this exemption does not apply if they change to a nonimmigrant status other than J-1 or Q-1, in which case they become liable for these taxes from the day of the status change. Additionally, the spouses and dependents of NRA scholars, trainees, teachers, or researchers in J-2 status are not exempt and are fully liable for Social Security and Medicare taxes on any wages earned in the US.

Furthermore, under special exception rules, Social Security and Medicare taxes do not apply to services performed by students employed by a school, college, or university where the student is enrolled at least half-time. The student's on-campus employment must be incidental to and for the purpose of pursuing a course of study.

It is important to note that the term "resident" in the context of tax purposes does not equate to residency by other definitions. Being a "resident for tax purposes" is solely a tax filing status and is distinct from being a resident for tuition or permanent residency purposes.

International Students: Invest in US Stocks?

You may want to see also

![]()

Nonresident aliens can be exempt from US tax under tax treaties

International students on F, J, M, or Q visas in the US are typically considered nonresident aliens for tax purposes. This means that they are required to file a Form 1040-NR, U.S. Nonresident Alien Income Tax Return, if they have any income subject to US tax, such as wages, tips, scholarships, or fellowship grants.

Now, nonresident aliens can benefit from tax treaties, which are agreements between the US and foreign countries outlining how nonresidents will be taxed in each country. The US has tax treaties with 66 countries, and these treaties can provide significant tax relief for nonresident aliens. Under these treaties, nonresident aliens may be exempt from US income taxes on certain types of income or be taxed at a reduced rate.

For example, Canadian citizens who are in the US as international students are exempt from tax on any US income earned from activities related to education, training, or maintenance. Additionally, they can be exempt from up to $10,000 in personal services (such as OPT, teaching, and research) if their total income is less than or equal to $10,000. If their income exceeds this threshold, they become liable for US taxes on the entire amount.

Furthermore, nonresident aliens who are teachers or researchers in the US on an F-1 visa may not need to provide an 8233 for their income, which can be exempt under specific tax treaties, such as the Indian tax treaty. However, if they stay in the US for more than 24 months, they may lose these treaty benefits and become subject to taxes on income previously considered exempt.

To claim any tax treaty benefits, nonresident aliens must file a true and accurate income tax return within 16 months of the due date. They may also need to attach a completed Form 8833, Treaty-Based Return Position Disclosure, depending on their specific circumstances. It is important to note that tax treaties are reciprocal, so they apply to US citizens or residents earning income in the treaty countries as well.

International Students: Non-Resident Status in New York State

You may want to see also

Frequently asked questions

A resident alien is someone who is considered a resident for tax purposes. This is different from being a resident by other definitions, such as having a Green Card and being a US permanent resident.

You can use the GLACIER Tax Prep program or Sprintax software to determine your residency status. You can also refer to the IRS "Introduction to Residency Under U.S. Tax Law" page and IRS Publication 519.

International students with F-1 or J-1 visas are generally considered nonresident aliens for their first five calendar years in the US. After five years, they become resident aliens for tax purposes.