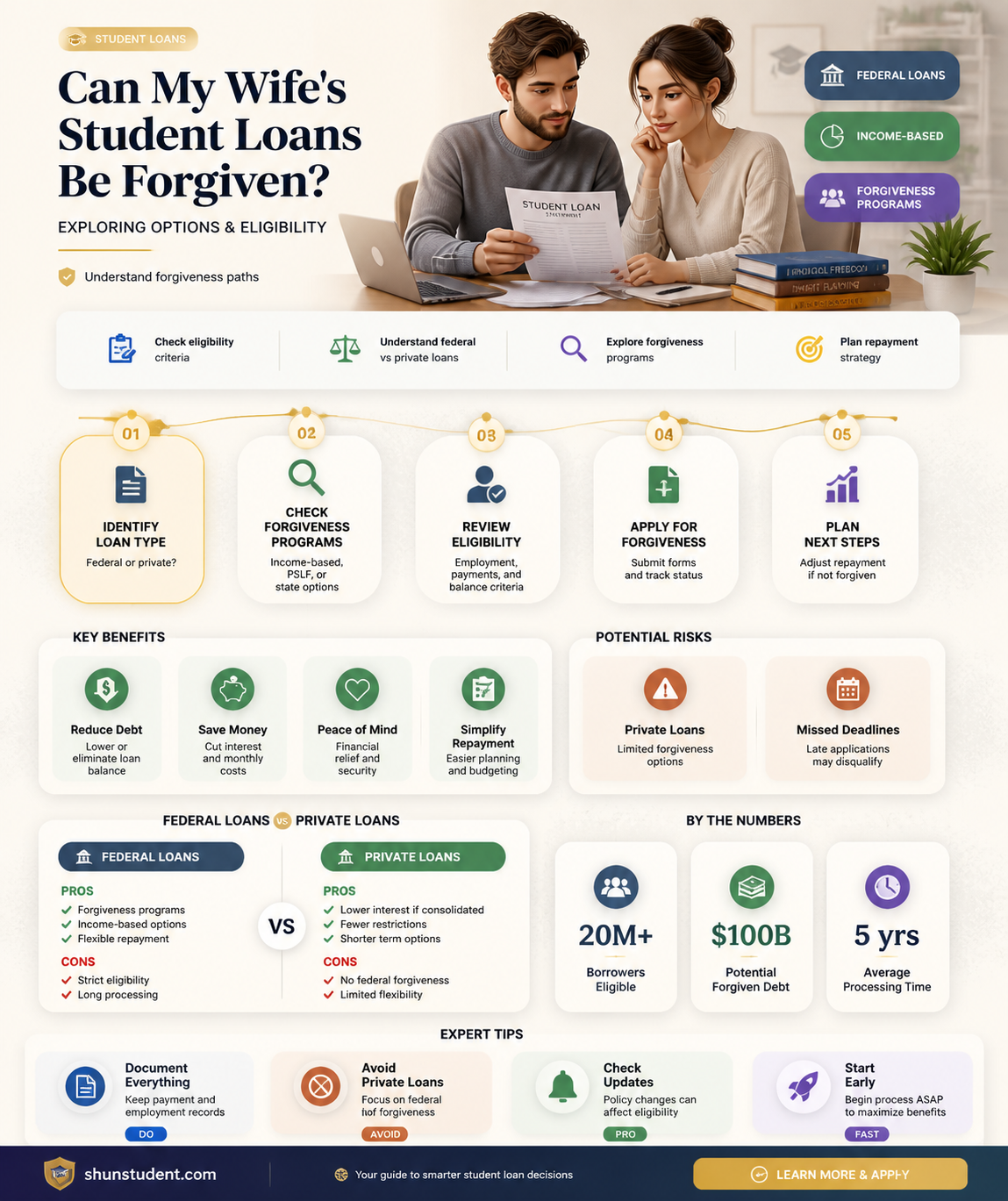

Navigating the complexities of student loan forgiveness can be overwhelming, especially when considering options for a spouse’s debt. Many borrowers wonder if their wife’s student loans qualify for forgiveness, and the answer depends on several factors, including the type of loans (federal or private), her employment status, and the repayment plan she’s enrolled in. Federal student loans, for instance, may be eligible for programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, or income-driven repayment (IDR) forgiveness, provided she meets specific criteria. Private loans, however, typically do not offer forgiveness options unless refinanced or settled. Understanding these distinctions and exploring available programs is crucial to determining whether your wife’s student loans can be forgiven.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Depends on loan type (federal or private), repayment plan, and profession. |

| Federal Student Loan Forgiveness | Available through programs like Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, Income-Driven Repayment (IDR) Forgiveness, and Temporary Expanded PSLF (TEPSLF). |

| Private Student Loan Forgiveness | Rarely available; some lenders offer forgiveness in cases of disability or death. |

| Public Service Loan Forgiveness (PSLF) | Requires 120 qualifying payments while working full-time for a government or nonprofit organization. |

| Teacher Loan Forgiveness | Up to $17,500 in forgiveness for eligible teachers working in low-income schools for 5 consecutive years. |

| Income-Driven Repayment (IDR) Forgiveness | Remaining balance forgiven after 20-25 years of qualifying payments, depending on the plan. |

| Disability Discharge | Total and Permanent Disability (TPD) discharge available for federal loans with proper documentation. |

| Death Discharge | Federal loans are discharged upon the borrower’s death; private loans vary by lender. |

| Bankruptcy Discharge | Extremely rare for student loans but possible in cases of undue hardship. |

| Temporary Expanded PSLF (TEPSLF) | Allows previously ineligible payments to count toward PSLF forgiveness. |

| Loan Type Impact | Federal loans have more forgiveness options than private loans. |

| Employment Requirements | Certain programs require specific employment (e.g., public service, teaching). |

| Repayment Plan Impact | IDR plans are required for IDR forgiveness; standard plans do not qualify. |

| Tax Implications | Some forgiven amounts may be taxable, depending on the program and circumstances. |

| Application Process | Requires submitting forms and documentation to the loan servicer or Department of Education. |

| Recent Updates | Changes to PSLF and IDR forgiveness rules under the Biden administration (e.g., limited PSLF waiver expired Oct. 31, 2022). |

Explore related products

What You'll Learn

- Income-Driven Repayment Plans: Lower payments based on income; forgiveness after 20-25 years

- Public Service Loan Forgiveness (PSLF): Forgiveness after 10 years of qualifying payments in public service

- Teacher Loan Forgiveness: Up to $17,500 for teachers in low-income schools after 5 years

- Disability Discharge: Loans forgiven if borrower has a permanent disability

- Closed School Discharge: Forgiveness if school closes while enrolled or soon after

![]()

Income-Driven Repayment Plans: Lower payments based on income; forgiveness after 20-25 years

For those grappling with the weight of student loan debt, income-driven repayment (IDR) plans offer a lifeline by recalibrating monthly payments to align with earnings. These plans, which include options like Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR), cap payments at 10-20% of discretionary income, ensuring affordability even during periods of low earnings. For instance, a borrower earning $40,000 annually with a family size of two might see payments drop from $500 to $200 per month under REPAYE, freeing up funds for other financial priorities.

The true allure of IDR plans, however, lies in their forgiveness component. After 20 to 25 years of consistent payments, any remaining balance is forgiven, though borrowers should be aware that the forgiven amount may be taxed as income. For example, a borrower on the IBR plan would qualify for forgiveness after 25 years, while someone on REPAYE could see forgiveness in as little as 20 years if all loans being repaid were for undergraduate study. This timeline shortens to 20-24 years for graduate studies, making IDR plans particularly beneficial for those with advanced degrees and higher debt loads.

Choosing the right IDR plan requires careful consideration of individual circumstances. REPAYE, for instance, is ideal for single borrowers or those with undergraduate loans due to its shorter forgiveness timeline and lower payment cap (10% of discretionary income). In contrast, IBR might suit married borrowers with higher incomes, as it considers spousal income differently depending on tax filing status. Borrowers should use the Federal Student Aid Loan Simulator to model payments and forgiveness timelines under each plan before committing.

One critical caveat is the annual recertification requirement for IDR plans. Failure to update income and family size information each year can result in a return to the standard repayment plan, potentially doubling or tripling monthly payments. Additionally, borrowers must remain vigilant about tax implications of forgiveness, as the forgiven amount could trigger a significant tax bill. Strategies like setting aside a portion of savings annually or exploring Public Service Loan Forgiveness (PSLF) in tandem with IDR can mitigate these risks.

In practice, IDR plans are not a one-size-fits-all solution but a strategic tool for managing long-term debt. For a 30-year-old borrower with $60,000 in loans and an entry-level salary of $45,000, switching to REPAYE could reduce monthly payments by 60% and lead to $20,000 in forgiveness after 20 years. By contrast, a 35-year-old with $100,000 in graduate school debt might opt for IBR, aiming for forgiveness after 25 years while maintaining manageable payments. Ultimately, IDR plans offer a pathway to financial stability, but maximizing their benefits requires proactive planning and informed decision-making.

Is Navient Forgiving Student Loans? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF): Forgiveness after 10 years of qualifying payments in public service

If your wife has been diligently working in public service while managing her student loans, she might be on the path to a significant financial milestone: Public Service Loan Forgiveness (PSLF). This federal program offers a clear, albeit stringent, route to erasing her debt after 10 years of qualifying payments. Here’s how it works: to be eligible, she must make 120 qualifying payments while employed full-time by a government or qualifying non-profit organization. These payments must be made under an income-driven repayment plan, ensuring they’re manageable based on her income and family size. The clock starts ticking from her first qualifying payment, so consistency is key.

One critical detail often overlooked is the type of loans eligible for PSLF. Only Direct Loans qualify, so if your wife has Federal Family Education Loans (FFEL) or Perkins Loans, she’ll need to consolidate them into a Direct Consolidation Loan to participate. This step is non-negotiable and can reset her payment count, so timing matters. For instance, if she’s already made 50 qualifying payments under FFEL, consolidating will restart her counter at zero. Planning this transition strategically can save years of effort.

Employer certification is another crucial step in the PSLF process. Your wife should submit the Employment Certification Form annually or whenever she changes jobs to ensure her payments are tracking correctly. This form verifies her employer’s eligibility and her full-time status, both of which are required for PSLF. Waiting until the 10-year mark to confirm eligibility could lead to costly surprises, so proactive documentation is essential. Think of it as building a paper trail that proves her compliance with the program’s rules.

Finally, the PSLF program isn’t without its challenges. Common pitfalls include missing payments, working for ineligible employers, or being on the wrong repayment plan. For example, if your wife switches to a standard repayment plan—even temporarily—those payments won’t count toward her 120. Similarly, part-time work or employment with a for-profit company, even if it’s in a public service role, disqualifies her during that period. Staying informed and vigilant can prevent these setbacks, ensuring she stays on track to achieve forgiveness.

In summary, PSLF offers a clear path to student loan forgiveness for those committed to public service, but it demands precision and persistence. By ensuring the right loan type, maintaining qualifying payments, certifying employment regularly, and avoiding common pitfalls, your wife can position herself to eliminate her debt after a decade of service. It’s a long-term commitment, but the payoff—financial freedom—is well worth the effort.

Do You Qualify for Student Loan Forgiveness? Key Eligibility Criteria Explained

You may want to see also

Explore related products

![]()

Teacher Loan Forgiveness: Up to $17,500 for teachers in low-income schools after 5 years

Teachers in low-income schools face unique challenges, but they also have access to a powerful financial incentive: the Teacher Loan Forgiveness program. This federal initiative offers up to $17,500 in student loan forgiveness after five consecutive years of full-time teaching in a designated low-income school. To qualify, your wife must meet specific criteria, including teaching in a school that serves students from low-income families, as determined by the federal government’s Title I guidelines. This program is particularly beneficial for secondary school teachers in math, science, or special education, who are eligible for the maximum $17,500, while other teachers can receive up to $5,000.

To navigate this opportunity, start by verifying the eligibility of your wife’s school through the Teacher Cancellation Low Income Directory. Next, ensure her loans qualify—only Direct Subsidized and Unsubsidized Loans are eligible, not Federal Family Education Loans (FFEL) or Perkins Loans, unless consolidated into a Direct Loan. After completing five years of teaching, she must submit the Teacher Loan Forgiveness Application to her loan servicer, along with certification from her school’s chief administrative officer. Keep detailed records of her teaching years, as documentation is critical for approval.

While the program is generous, it’s not without limitations. For instance, if your wife has both eligible and ineligible loans, payments may be applied to ineligible loans first, reducing the forgiveness amount. Additionally, the forgiven amount may be considered taxable income, though recent legislation has temporarily waived taxes on forgiven student loans through 2025. To maximize benefits, consider pairing this program with Public Service Loan Forgiveness (PSLF) if your wife plans to continue teaching in the public sector, as PSLF can forgive remaining balances after 10 years of qualifying payments.

Finally, timing and strategy are key. Encourage your wife to start tracking her eligible teaching years immediately and to consolidate ineligible loans if necessary. Regularly review her loan servicer’s communications to ensure payments are correctly applied. By understanding the nuances of the Teacher Loan Forgiveness program, your wife can take a significant step toward reducing her student loan burden while making a meaningful impact in a low-income school.

Forgiving Student Loans for Disabled Borrowers: What You Need to Know

You may want to see also

Explore related products

![]()

Disability Discharge: Loans forgiven if borrower has a permanent disability

For borrowers facing permanent disability, the Total and Permanent Disability (TPD) Discharge program offers a lifeline to eliminate federal student loan debt. This provision, part of the Higher Education Act, recognizes that individuals with severe disabilities often face insurmountable financial barriers. To qualify, the borrower must provide documentation proving their inability to engage in substantial gainful activity due to a physical or mental impairment expected to last continuously for at least 60 months or result in death. Acceptable evidence includes a physician’s certification, Social Security Administration (SSA) notice of award for Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) based on disability, or documentation of a 100% disability rating from the U.S. Department of Veterans Affairs (VA).

The application process, while straightforward, requires vigilance. Once approved, the borrower enters a three-year monitoring period during which they must refrain from earning above the poverty line, taking out new federal loans, or receiving new federal education benefits. Failure to comply can result in loan reinstatement. Notably, discharged loans may be considered taxable income, though recent legislation has temporarily waived taxes on TPD discharges through 2025. Borrowers should consult a tax professional to understand potential liabilities.

Comparatively, private student loans rarely offer disability discharge options, underscoring the importance of federal loan forgiveness for this demographic. For spouses seeking relief for their partners, understanding the TPD process is critical. Proactive steps include gathering medical records, contacting loan servicers for application forms, and monitoring deadlines. Advocacy groups like the National Disability Rights Network can provide additional support.

A practical tip for applicants: keep detailed records of all communications with loan servicers and agencies. This documentation can resolve disputes and expedite the process. While the TPD discharge program is not widely publicized, it remains a vital tool for those whose disabilities prevent them from repaying student loans. By leveraging this provision, borrowers and their families can achieve financial stability during challenging times.

Does Aidvantage Qualify for Student Loan Forgiveness? What Borrowers Need to Know

You may want to see also

Explore related products

![]()

Closed School Discharge: Forgiveness if school closes while enrolled or soon after

If your wife’s school shut down while she was enrolled or shortly after she withdrew, she might qualify for Closed School Discharge, a federal program that wipes out student loans tied to the closed institution. This isn’t a loophole—it’s a safety net designed to protect borrowers from financial ruin when their education is abruptly cut short. To qualify, the closure must have occurred while she was enrolled, during an approved leave of absence, or within 120 days after withdrawal. If she transferred credits to another school, however, she’s likely ineligible, as this suggests she completed her program elsewhere.

The application process for Closed School Discharge is straightforward but requires attention to detail. Start by contacting your loan servicer to request the discharge application. Gather proof of enrollment dates, such as transcripts or enrollment records, as these will be critical in demonstrating eligibility. If your wife’s loans were private, the rules may differ, as private lenders aren’t bound by federal discharge programs. In such cases, consult the lender directly or seek legal advice to explore options.

One common pitfall borrowers face is assuming they automatically qualify because their school closed. Not all closures meet the federal criteria, and some schools may reopen under a different name, complicating eligibility. For instance, if the school closed due to accreditation issues but later merged with another institution, your wife’s loans might not qualify for discharge. Always verify the closure status with the Department of Education’s Closed School Discharge database to ensure accuracy.

Beyond the immediate relief of loan forgiveness, Closed School Discharge offers a fresh start but comes with nuances. For example, discharged loans are no longer taxable as of recent legislative changes, but any refunded amounts (e.g., tuition paid for the canceled period) must be returned to the lender. Additionally, if your wife attended a school that closed decades ago, she’s still eligible to apply—there’s no statute of limitations for this discharge. Practical tip: keep all loan and school-related documents in a single folder for easy access during the application process.

Finally, consider the broader impact of pursuing this discharge. While it eliminates the debt, it doesn’t restore the time or effort invested in the incomplete education. If your wife intends to continue her studies, research accredited institutions and inquire about credit transfers before enrolling. Closed School Discharge is a powerful tool, but it’s just one step in navigating the aftermath of a school closure. Pair it with proactive planning to rebuild educational and financial stability.

Discover If You Qualify for Student Loan Forgiveness: A Guide

You may want to see also

Frequently asked questions

Yes, if your wife works full-time for a qualifying public service employer (e.g., government, non-profit) and makes 120 eligible payments under an income-driven repayment plan, she may qualify for Public Service Loan Forgiveness (PSLF).

It depends on the specific program. For example, the one-time student loan forgiveness plan (up to $20,000 for Pell Grant recipients and $10,000 for others) applies to borrowers earning below certain income thresholds. Check if your wife meets the eligibility criteria.

Yes, if your wife has a permanent disability, she may qualify for Total and Permanent Disability (TPD) discharge. She’ll need to provide documentation of her disability to her loan servicer to apply for forgiveness.