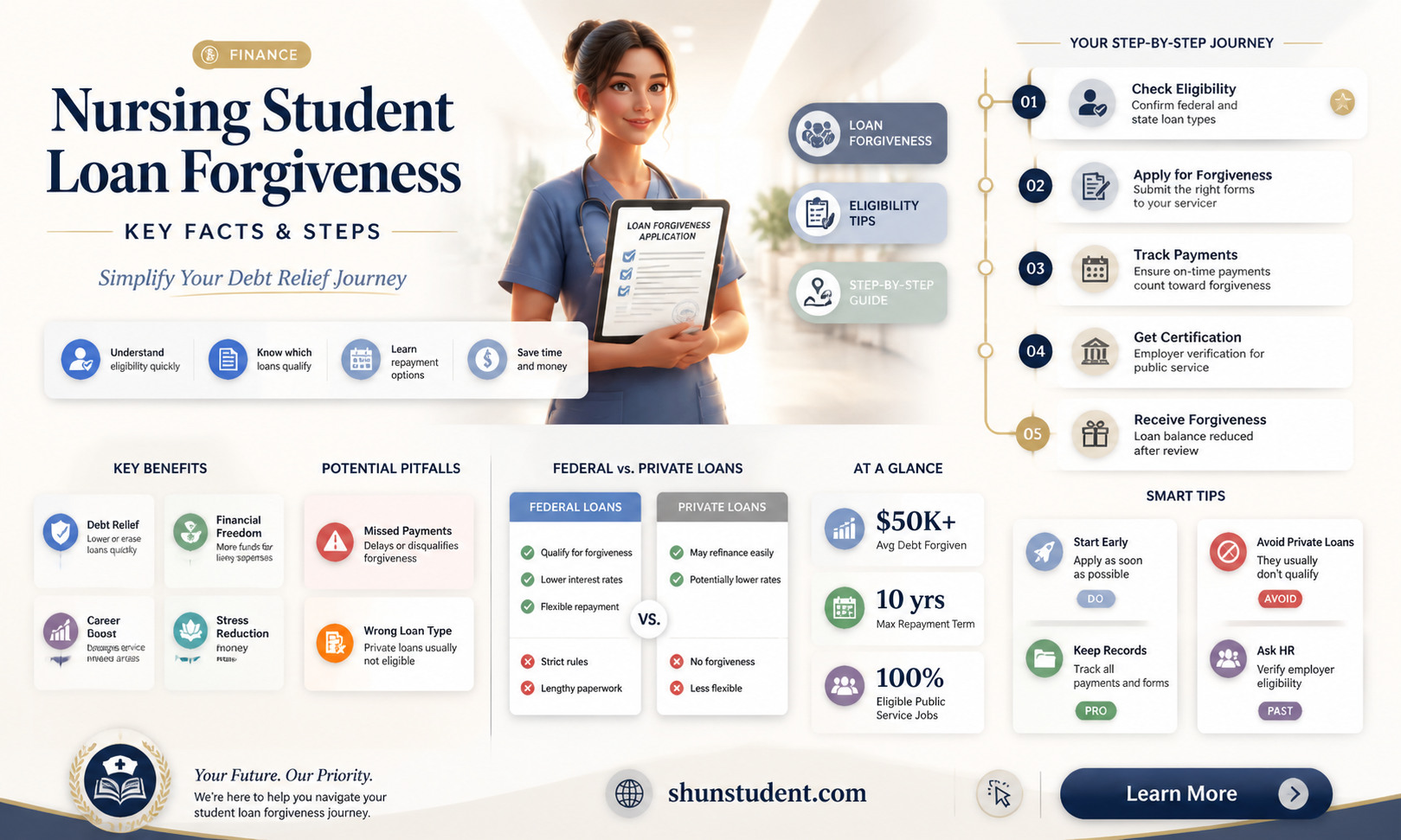

Nursing student loans are a significant concern for many aspiring healthcare professionals, and the question of whether these loans can be forgiven is a critical one. With the rising cost of education and the increasing demand for skilled nurses, many students rely on loans to finance their studies. Fortunately, there are several loan forgiveness programs available specifically for nurses, designed to alleviate financial burden and encourage service in underserved areas or high-need specialties. Programs like the Nurse Corps Loan Repayment Program, Public Service Loan Forgiveness (PSLF), and state-specific initiatives offer opportunities for partial or full loan forgiveness in exchange for a commitment to work in designated areas or facilities. Understanding the eligibility criteria, application processes, and obligations associated with these programs is essential for nursing students and graduates seeking financial relief.

| Characteristics | Values |

|---|---|

| Loan Forgiveness Programs | Public Service Loan Forgiveness (PSLF), Nurse Corps Loan Repayment Program, Perkins Loan Cancellation |

| Eligibility Requirements | Full-time employment in qualifying public service or nonprofit roles, working in underserved areas, meeting specific service obligations |

| Loan Types Covered | Federal Direct Loans (for PSLF), Stafford Loans, Perkins Loans, Nurse Corps Loans |

| Forgiveness Amount | Up to 100% of remaining loan balance after meeting program requirements |

| Service Obligation | 10 years of qualifying payments (PSLF), 2-4 years of service in underserved areas (Nurse Corps) |

| Tax Implications | PSLF forgiveness is tax-free; Nurse Corps repayment may be taxable |

| Application Process | Submit Employment Certification Form (PSLF), apply through Nurse Corps program website |

| Recent Updates (2023) | Temporary PSLF waiver expired Oct. 31, 2022; Nurse Corps funding increased |

| State-Specific Programs | Varies by state (e.g., New York State Nursing Faculty Loan Forgiveness) |

| Private Loan Forgiveness | Not eligible for federal forgiveness programs; rare exceptions exist |

| Income-Driven Repayment (IDR) | Can lead to loan forgiveness after 20-25 years, depending on plan |

Explore related products

What You'll Learn

![]()

Federal Loan Forgiveness Programs

Nursing students burdened by federal loans have several pathways to forgiveness, but understanding the nuances of each program is crucial. The Public Service Loan Forgiveness (PSLF) program stands out as a primary option. To qualify, nurses must work full-time for a qualifying employer—such as a government agency, nonprofit hospital, or eligible healthcare organization—and make 120 qualifying payments under an income-driven repayment plan. This program forgives the remaining loan balance after meeting these criteria, offering a clear, albeit structured, route to debt relief.

Another federal program tailored for healthcare professionals is the Nurse Corps Loan Repayment Program. This initiative repays up to 85% of unpaid nursing education debt for licensed nurses who commit to working at least two years in a Critical Shortage Facility or as nurse faculty at an eligible school of nursing. While not technically "forgiveness," this program effectively eliminates a significant portion of debt in exchange for service in high-need areas. Eligibility depends on factors like employment setting and financial need, making it a targeted solution for those willing to serve in underserved communities.

For nurses working in rural or underserved areas, the National Health Service Corps (NHSC) Loan Repayment Program offers substantial benefits. Participants can receive up to $50,000 in loan repayment for a two-year commitment to serve in a Health Professional Shortage Area (HPSA). This program is particularly appealing for nurses specializing in primary care, as it aligns debt relief with addressing critical healthcare gaps. However, applicants must commit to full-time service, and partial repayment options are available for half-time work.

Comparatively, the Federal Perkins Loan Cancellation Program provides forgiveness for nurses with Perkins Loans who serve in designated low-income schools or certain healthcare roles. Nurses can have up to 100% of their loans forgiven over five years, with incremental forgiveness starting at 20% after the first year. While this program is more limited due to the phaseout of Perkins Loans in 2017, existing borrowers can still benefit. It’s a straightforward option for those with eligible loans, though availability is shrinking.

In navigating these programs, nurses must remain vigilant about eligibility criteria and documentation. For instance, PSLF requires certification of employment annually or when switching jobs to ensure payments count toward forgiveness. Similarly, income-driven repayment plans, often a prerequisite for forgiveness, recalculate monthly payments based on income and family size, requiring annual recertification. Practical tips include keeping detailed records of employment and payments, consulting with loan servicers regularly, and exploring state-level loan repayment programs for additional support. By strategically aligning career choices with these federal programs, nurses can significantly reduce or eliminate their student loan burden.

Does Student Loan Forgiveness Extend to Dependent Borrowers?

You may want to see also

Explore related products

![]()

State-Specific Repayment Assistance

Nursing student loan forgiveness isn’t a one-size-fits-all solution, and state-specific repayment assistance programs highlight this diversity. Each state tailors its initiatives to address local healthcare workforce shortages, creating a patchwork of opportunities for nurses burdened by debt. For instance, California’s Bachelor of Science in Nursing Loan Repayment Program offers up to $10,000 annually for two years to nurses working in federally designated Health Professional Shortage Areas (HPSAs). In contrast, New York’s Nurse Loan Forgiveness Program provides up to $4,000 per year for four years to licensed nurses practicing in underserved communities. These programs demonstrate how states leverage financial incentives to retain nurses where they’re needed most.

To navigate these programs effectively, nurses must understand eligibility criteria, which vary widely. Most require a commitment to work in underserved areas or specific facilities, such as rural hospitals or public health clinics. For example, Texas’ Nurse Education Loan Repayment Program mandates a two-year service obligation in a critical shortage facility, while Florida’s Nursing Student Loan Forgiveness Program targets nurses working in state-funded nursing homes. Applicants should research their state’s Department of Health or Board of Nursing websites for detailed requirements and application deadlines. Pro tip: Keep meticulous records of your employment and loan details, as documentation is often a key component of the application process.

A comparative analysis reveals that state programs often complement federal initiatives like the Public Service Loan Forgiveness (PSLF) program. While PSLF requires 10 years of qualifying payments, state programs typically offer shorter-term relief, making them ideal for nurses seeking immediate financial assistance. However, some states, like Illinois, require recipients to enroll in income-driven repayment plans to qualify for their Health Professions Loan Repayment Program. This interplay between state and federal programs underscores the importance of strategic planning. Nurses should assess their long-term career goals and financial situation to determine which combination of programs maximizes their benefits.

Persuasively, state-specific repayment assistance isn’t just about debt relief—it’s a career accelerator. By committing to underserved areas, nurses gain invaluable experience in high-need specialties like geriatrics, mental health, or critical care. For example, Ohio’s Nurse Education Assistance Loan Program prioritizes applicants working in long-term care facilities, addressing the state’s aging population crisis. This dual benefit—financial relief and professional growth—makes these programs a win-win for both nurses and communities. Nurses considering these opportunities should view them as investments in their future, not just solutions to current debt.

Finally, a descriptive overview of application processes reveals common pitfalls to avoid. Many programs require detailed employment verification, tax documents, and loan statements, so disorganization can delay approval. Some states, like Washington, use a competitive scoring system based on factors like years of experience and facility type, making early application crucial. Additionally, nurses should be aware of tax implications; some states treat loan repayment as taxable income, while others offer tax exemptions. Practical tip: Set reminders for annual recertification deadlines, as failure to renew can result in forfeiture of benefits. By staying informed and proactive, nurses can fully capitalize on these state-specific opportunities.

Understanding Student Loan Forgiveness for Fully Disabled Borrowers: Timeline Explained

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF)

Nursing students burdened by loan debt often seek relief through Public Service Loan Forgiveness (PSLF), a federal program designed to incentivize careers in public service. This program offers a lifeline to those committed to serving their communities, but navigating its requirements demands careful attention.

Here's a breakdown:

Eligibility hinges on two key factors: employment and loan type. Full-time employment (at least 30 hours per week) in a qualifying public service organization is mandatory. This encompasses a wide range of roles, including nurses working in government agencies, non-profit hospitals, and community health clinics. Crucially, only Direct Loans are eligible for PSLF. Consolidating other federal loans into a Direct Consolidation Loan can make them eligible, but payments made prior to consolidation don't count towards the required 120 qualifying payments.

The path to forgiveness is a marathon, not a sprint. Borrowers must make 120 on-time, monthly payments under a qualifying repayment plan while employed full-time in public service. These payments don't need to be consecutive, but they must be made after October 1, 2007. Choosing an income-driven repayment plan can significantly lower monthly payments, making it easier to meet the 120-payment threshold.

Documentation is paramount. Submitting an Employment Certification Form (ECF) annually, or whenever changing employers, is crucial. This form verifies your employment and ensures your payments are counted towards PSLF. Keeping meticulous records of all payments and ECF submissions is essential for a smooth forgiveness process.

PSLF offers a substantial reward for dedication to public service. After fulfilling the 120-payment requirement, the remaining balance on your Direct Loans is forgiven tax-free. This can translate to significant savings, allowing nurses to focus on their patients and communities without the burden of overwhelming debt.

How to Check Your Student Loan Forgiveness Status: A Quick Guide

You may want to see also

Explore related products

![]()

Nurse Corps Loan Repayment

Nursing students burdened by loan debt have a powerful ally in the Nurse Corps Loan Repayment Program. This federal initiative, administered by the Health Resources and Services Administration (HRSA), offers substantial financial relief in exchange for a commitment to serve in areas with critical nursing shortages.

Imagine wiping out up to 85% of your qualifying nursing student loans in just three years. That's the potential reality for eligible nurses who participate in the Nurse Corps Loan Repayment Program.

Eligibility hinges on several key factors. Firstly, you must be a licensed registered nurse (RN) or advanced practice registered nurse (APRN) with qualifying federal student loans. Secondly, you must commit to working full-time for at least two years at an approved Critical Shortage Facility (CSF). These facilities include hospitals, clinics, and other healthcare settings located in Health Professional Shortage Areas (HPSAs) or Medically Underserved Areas/Populations (MUAs/MUPs).

The application process is competitive, requiring a detailed application, proof of licensure, loan documentation, and a commitment letter from your chosen CSF. It's crucial to research eligible facilities in your desired location and understand the specific needs of the population they serve.

While the Nurse Corps program offers significant benefits, it's not without its considerations. The commitment to work in a potentially challenging environment requires dedication and a genuine desire to serve underserved communities. Additionally, tax implications should be factored in, as the loan repayment is considered taxable income.

Despite these considerations, the Nurse Corps Loan Repayment Program presents a compelling opportunity for nurses seeking to alleviate their student loan burden while making a meaningful impact on healthcare access. It's a win-win situation: you gain financial freedom while contributing to the well-being of those in need.

Will Student Loans Be Forgiven After 20 Years? What You Need to Know

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plans

Nursing students often graduate with substantial loan debt, and the burden can feel overwhelming. Income-Driven Repayment (IDR) plans offer a lifeline by capping monthly payments at a percentage of discretionary income, typically 10-20%. For nurses, especially those in lower-paying roles or public service, this can mean significantly lower payments compared to standard plans.

Consider a new graduate nurse earning $50,000 annually with $100,000 in loans. Under a standard 10-year repayment plan, monthly payments would exceed $1,000. However, an IDR plan like Revised Pay As You Earn (REPAYE) could reduce this to around $300, freeing up funds for living expenses or other financial goals. The trade-off? A longer repayment term, often 20-25 years, with potential tax implications on forgiven balances.

Choosing the right IDR plan requires careful analysis. For instance, Pay As You Earn (PAYE) caps payments at 10% of discretionary income and forgives remaining debt after 20 years, but eligibility is limited to borrowers with loans from 2011 or later. In contrast, Income-Based Repayment (IBR) offers a 10% or 15% cap depending on loan type and forgives debt after 20 or 25 years. Nurses in public service, such as those working for nonprofit hospitals, may qualify for Public Service Loan Forgiveness (PSLF), which forgives remaining debt after 10 years of qualifying payments.

To maximize IDR benefits, nurses should annually recertify their income and family size, as changes can adjust payment amounts. Additionally, keeping detailed records of payments is crucial, especially for those pursuing PSLF. While IDR plans provide relief, they’re not a one-size-fits-all solution. Nurses must weigh the long-term costs of extended repayment against immediate financial stability.

In summary, Income-Driven Repayment plans can transform student loan management for nurses, offering lower monthly payments and pathways to forgiveness. By understanding plan specifics, staying organized, and aligning repayment strategies with career goals, nurses can navigate their debt more effectively and focus on what matters most—their patients.

Navigating Student Loan Forgiveness: A Step-by-Step Guide for Borrowers

You may want to see also

Frequently asked questions

Yes, nursing student loans may be eligible for forgiveness through programs like the Public Service Loan Forgiveness (PSLF) or the Nurse Corps Loan Repayment Program, depending on the borrower’s employment and eligibility criteria.

The Nurse Corps Loan Repayment Program offers up to 85% of unpaid nursing education debt in exchange for working at least two years in a Critical Shortage Facility or as a nurse faculty member at an eligible school of nursing.

Yes, nursing students can qualify for PSLF by working full-time for a qualifying employer (like a government or nonprofit organization) and making 120 eligible payments under an income-driven repayment plan.