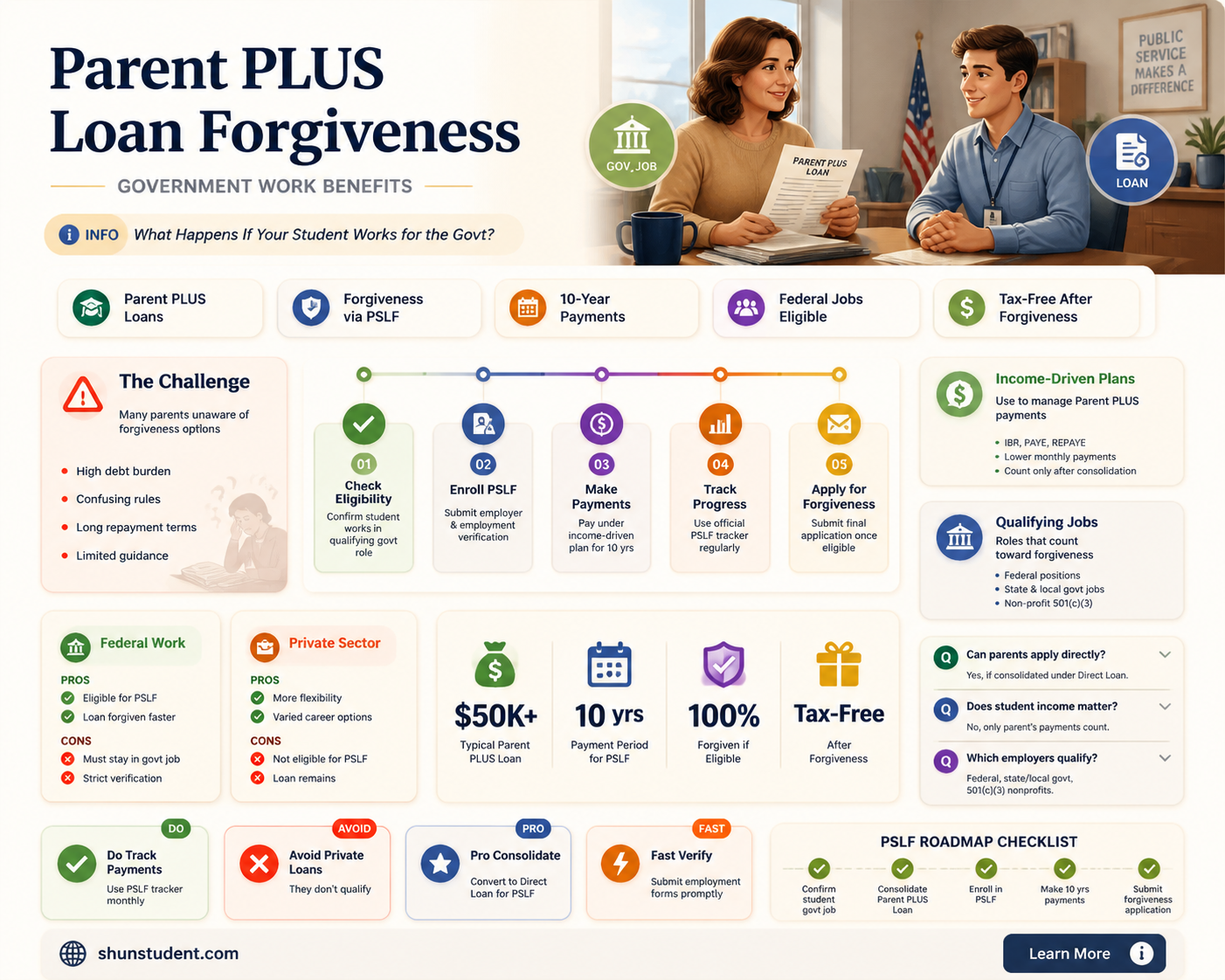

Parent PLUS loans, a federal student loan option for parents to finance their child's education, are not automatically forgiven if the student secures government employment. Unlike certain loan forgiveness programs tailored for specific professions or public service roles, Parent PLUS loans do not qualify for forgiveness based solely on the student's career path. However, parents may explore other forgiveness options, such as Public Service Loan Forgiveness (PSLF) if they work in qualifying public service jobs, or income-driven repayment plans that offer forgiveness after a set number of payments. It’s essential for borrowers to understand the terms and conditions of Parent PLUS loans and explore all available repayment and forgiveness strategies to manage their debt effectively.

| Characteristics | Values |

|---|---|

| Eligibility for Forgiveness | Parent PLUS loans are not automatically forgiven if the student gets a government job. However, forgiveness may be possible through specific programs like Public Service Loan Forgiveness (PSLF) if the parent meets eligibility criteria. |

| Public Service Loan Forgiveness (PSLF) | Parents can qualify for PSLF if they work full-time for a qualifying government or nonprofit organization and make 120 eligible payments under an income-driven repayment plan. |

| Income-Driven Repayment (IDR) Forgiveness | After 25 years of qualifying payments under an IDR plan, the remaining balance may be forgiven, but this is taxable as income. |

| Disability Discharge | If the parent or student borrower becomes totally and permanently disabled, the loan may be discharged. |

| Death Discharge | The loan is discharged if the parent or student borrower dies. |

| Closed School Discharge | If the student’s school closes while they are enrolled or shortly after withdrawal, the loan may be discharged. |

| Borrower Defense to Repayment | If the school misled the borrower or violated certain laws, the loan may be forgiven. |

| Tax Implications | Forgiveness through PSLF is tax-free, but forgiveness through IDR or other programs may be taxable. |

| Transfer of Loan to Student | Parent PLUS loans cannot be transferred to the student, limiting forgiveness options tied to the student’s employment or repayment status. |

| Government Job Impact | A student’s government job does not directly impact Parent PLUS loan forgiveness unless the parent qualifies independently through PSLF. |

Explore related products

What You'll Learn

![]()

Eligibility Criteria for Loan Forgiveness

Parent PLUS loans, unlike some federal student loans, are not automatically eligible for forgiveness if the student secures government employment. However, specific pathways exist for forgiveness under certain conditions. The Public Service Loan Forgiveness (PSLF) program is one such avenue, but it requires the parent borrower to consolidate the PLUS loan into a Direct Consolidation Loan and then make 120 qualifying payments while working full-time for a qualifying public service employer. This process is stringent, as payments must be made under an income-driven repayment plan, and the employer must be a government organization, 501(c)(3) not-for-profit, or other qualifying entities.

Another eligibility criterion involves income-driven repayment (IDR) plans, which can lead to loan forgiveness after 20–25 years of qualifying payments. For Parent PLUS loans, this requires consolidation into a Direct Consolidation Loan to access IDR plans like Income-Contingent Repayment (ICR). However, forgiveness under IDR is taxable as income, unlike PSLF, which is tax-free. Parents must carefully weigh the long-term financial implications of this route, as the forgiven amount could result in a significant tax liability.

A lesser-known option is Total and Permanent Disability (TPD) discharge, which forgives federal loans, including Parent PLUS loans, if the borrower or the student on whose behalf the loan was taken becomes permanently disabled. Documentation from a physician or the Social Security Administration is required to prove eligibility. This pathway is critical for families facing severe health challenges but requires thorough documentation and adherence to federal guidelines.

Lastly, closed school discharge and borrower defense to repayment are niche options for Parent PLUS loan forgiveness. The former applies if the student’s school closes while they are enrolled or shortly after withdrawal, while the latter requires proof that the school misled the borrower or violated state laws. These options are rare and situation-specific but highlight the importance of understanding all potential avenues for relief. Each eligibility criterion demands careful navigation of federal regulations, making it essential for borrowers to consult resources like the Department of Education’s Federal Student Aid website for precise guidance.

Disabled Veterans: Do They Qualify for Student Loan Forgiveness?

You may want to see also

Explore related products

![]()

Government Employment Requirements for Forgiveness

Parent PLUS loans, unlike federal student loans held by the student, are not eligible for the Public Service Loan Forgiveness (PSLF) program based solely on the borrower’s employment in government. However, there is a pathway to forgiveness for Parent PLUS loans through consolidation into a Direct Consolidation Loan and subsequent enrollment in an income-driven repayment (IDR) plan. Once consolidated, the parent borrower can pursue forgiveness under the Income-Contingent Repayment (ICR) plan, which requires 25 years of qualifying payments. If the parent borrower works full-time for a government agency or qualifying nonprofit, these payments can count toward the 25-year threshold, effectively linking government employment to the forgiveness timeline.

To leverage government employment for Parent PLUS loan forgiveness, the parent borrower must first consolidate the loan into the Direct Loan program. This step is critical because Parent PLUS loans are not eligible for IDR plans in their original form. After consolidation, the borrower can apply for ICR, which caps monthly payments at 20% of discretionary income. For parents working in government roles, this process allows their employment to indirectly support forgiveness by maintaining manageable payments over the 25-year period. It’s essential to certify income annually and recertify the IDR plan to ensure continued eligibility.

A key consideration for parent borrowers is the tax implications of loan forgiveness. Under current law, forgiven amounts after 25 years of ICR payments are treated as taxable income. Parents should plan for this potential tax liability by consulting a financial advisor or tax professional. Additionally, while government employment itself does not accelerate forgiveness, it can provide job stability and consistent income, making it easier to maintain qualifying payments. Parents should also explore employer-based repayment assistance programs, which some government agencies offer to supplement loan repayment efforts.

Comparatively, the PSLF program offers faster forgiveness after 10 years for eligible borrowers, but Parent PLUS loans remain ineligible even if the student works in government. This distinction highlights the importance of understanding the specific requirements for each forgiveness program. For Parent PLUS loans, the focus must be on the 25-year ICR timeline, with government employment serving as a supportive factor rather than a direct qualifier. Parents should carefully track their payments and ensure they meet all IDR requirements to avoid setbacks in the forgiveness process.

In practice, parent borrowers should take proactive steps to maximize their chances of forgiveness. First, consolidate the Parent PLUS loan into the Direct Loan program as soon as possible. Second, enroll in ICR and ensure all payments are made on time and in full. Third, maintain full-time government employment to provide financial stability and consistent income for IDR payments. Finally, stay informed about changes to federal loan programs and tax laws that could impact forgiveness strategies. By combining these steps, parent borrowers can navigate the path to forgiveness effectively, even if their loans are not directly tied to government employment requirements.

Poverty's Role in Student Loan Forgiveness: A Path to Equity?

You may want to see also

Explore related products

![]()

Public Service Loan Forgiveness (PSLF) Rules

Parent PLUS loans, a federal loan option allowing parents to borrow for their child's education, are not automatically forgiven if the student secures government employment. However, there’s a pathway to forgiveness through the Public Service Loan Forgiveness (PSLF) program, which requires a strategic approach. To qualify, the *parent*—not the student—must consolidate the PLUS loan into a Direct Consolidation Loan and then enroll in an income-driven repayment (IDR) plan. This shifts the loan type from FFEL or Direct PLUS to a Direct Loan, making it eligible for PSLF. The parent must then make 120 qualifying payments while working full-time for a government or nonprofit 501(c)(3) organization. Payments made under the Standard Repayment Plan do not count unless they meet the IDR criteria, so switching to an IDR plan is crucial.

One critical detail often overlooked is the employment certification process. Parents should submit the Employment Certification Form annually or when changing employers to ensure payments are tracked correctly. This step is non-negotiable, as it verifies eligibility and prevents disputes later. For instance, a parent working as a teacher in a public school would qualify, but a part-time role or employment with a for-profit company would not. The PSLF rules are strict: payments must be made on time, in full, and under an IDR plan while maintaining eligible employment. Missing any of these criteria resets the 120-payment counter, delaying forgiveness.

A common misconception is that the student’s government job directly impacts the parent’s loan forgiveness. In reality, the student’s employment is irrelevant; it’s the parent’s role that matters. For example, if a parent works for a federal agency while their child becomes a government employee, only the parent’s employment counts toward PSLF. This distinction is vital for families planning to leverage PSLF, as it requires the parent to commit to public service for at least 10 years. Additionally, parents should beware of payment pauses or forbearances, as these periods do not count toward the 120 payments unless they occurred during the COVID-19 administrative forbearance.

Finally, the PSLF program offers a clear but demanding route to forgiveness for Parent PLUS loans. Parents must navigate consolidation, IDR enrollment, and employment certification meticulously. While the process is complex, the reward—full loan forgiveness after 120 qualifying payments—can be life-changing. For those considering this path, consulting the Federal Student Aid website or a loan servicer for personalized guidance is highly recommended. PSLF is not a quick fix but a long-term commitment to public service, offering financial relief for parents who meet its stringent requirements.

Student Loan Forgiveness Update: Am I Still Eligible for Relief?

You may want to see also

Explore related products

![]()

Income-Driven Repayment Plan Options

Parent PLUS loans, unlike federal student loans held by the student, are not eligible for Public Service Loan Forgiveness (PSLF) or income-driven repayment (IDR) forgiveness programs in their original form. However, there’s a strategic workaround: consolidating Parent PLUS loans into a Direct Consolidation Loan, which then allows the parent borrower to access income-driven repayment plans. Among these, the Income-Contingent Repayment (ICR) plan is the only IDR option available for consolidated Parent PLUS loans. Under ICR, monthly payments are calculated as the lesser of 20% of discretionary income or the fixed payment over 12 years, adjusted for income. For instance, if a parent’s adjusted gross income (AGI) is $50,000 and their family size is 2, their discretionary income would be $10,000 (AGI minus 150% of the poverty guideline), and their monthly payment would be capped at $166.67. After 25 years of qualifying payments, any remaining balance is forgiven, though the forgiven amount may be taxed as income.

While ICR offers a pathway to forgiveness, it’s critical to weigh the trade-offs. Payments under ICR may be lower than the standard plan but can still accrue significant interest over time, potentially increasing the total repayment amount. For example, a $50,000 Parent PLUS loan at 7% interest could grow to over $80,000 after 25 years if payments don’t cover the interest. Parents should also consider the tax implications of forgiven debt, which could result in a substantial tax bill in the forgiveness year. To mitigate this, borrowers may want to consult a tax professional or set aside funds annually to prepare for this liability.

Another practical tip is to maximize deductions when calculating discretionary income. For instance, parents can lower their AGI by contributing to retirement accounts or claiming eligible deductions, which in turn reduces their monthly ICR payment. Additionally, if the student for whom the loan was taken becomes disabled or passes away, the Parent PLUS loan may be discharged, though this is a rare and unfortunate circumstance. Parents should also explore whether their employer offers student loan assistance programs, as some companies provide repayment benefits that can offset the burden.

Comparatively, income-driven plans like Revised Pay As You Earn (REPAYE) or Pay As You Earn (PAYE), which cap payments at 10% of discretionary income and forgive balances after 20–25 years, are not available for Parent PLUS loans even after consolidation. This makes ICR the sole, albeit imperfect, option for parents seeking relief. In contrast, if the student themselves takes out federal loans and enters public service, their loans could be forgiven after 10 years under PSLF, but this does not extend to Parent PLUS loans. This distinction underscores the importance of parents understanding their limited options and planning accordingly.

In conclusion, while Parent PLUS loans are not directly forgiven if the student enters government service, consolidating these loans and enrolling in the ICR plan can provide a path to forgiveness after 25 years. Parents must carefully evaluate the long-term financial implications, including interest accrual and tax consequences, and take proactive steps to minimize their repayment burden. By leveraging available tools and staying informed, parents can navigate this complex landscape more effectively.

Is Student Loan Forgiveness a Real Possibility for Borrowers?

You may want to see also

Explore related products

![]()

Impact of Student’s Government Job on Forgiveness

Parent PLUS loans, a federal student loan option for parents to finance their child's education, often leave borrowers wondering about forgiveness opportunities, especially if their child secures a government job. The impact of a student's government employment on loan forgiveness is a nuanced aspect of this financial aid program, offering both potential benefits and limitations.

Understanding the Public Service Loan Forgiveness (PSLF) Program:

The PSLF program is a cornerstone of loan forgiveness discussions. It offers a pathway to debt relief for borrowers who work full-time in eligible public service jobs, including government positions. Here's the catch: the student's government job does not directly forgive the Parent PLUS loan. Instead, the parent borrower must consolidate the loan into a Direct Consolidation Loan and then make qualifying payments while working in an eligible public service role themselves. This means the parent, not the student, must be employed in a government or qualifying non-profit organization to benefit from PSLF.

Exploring Income-Driven Repayment (IDR) Plans:

IDR plans can provide an alternative route to loan forgiveness, albeit after a more extended period. These plans cap monthly payments at a percentage of the borrower's discretionary income and offer forgiveness of the remaining balance after 20-25 years of qualifying payments. If a parent borrower is on an IDR plan and their child secures a government job with a stable income, it could indirectly impact the parent's ability to manage loan payments. Higher income might result in higher monthly payments under the IDR plan, potentially delaying the forgiveness timeline.

Strategic Planning for Parents:

Parents considering Parent PLUS loans should carefully evaluate their long-term financial strategy. If there's a possibility of the student pursuing a government career, parents might explore other financing options or consider the potential benefits of PSLF. For instance, parents could opt for federal student loans in the student's name, which may qualify for PSLF if the student works in public service. This shift in borrowing strategy could significantly impact the family's overall financial health.

The Role of Student's Government Job in Repayment Assistance:

While a student's government job doesn't directly forgive Parent PLUS loans, it can still play a role in repayment strategies. Some government agencies offer loan repayment assistance programs as employee benefits. These programs may provide financial support to employees for their education debt, including Parent PLUS loans. Students with government jobs can explore such benefits, which could indirectly help their parents manage loan repayment. This assistance might come in the form of direct payments towards the loan or as a taxable benefit, providing parents with additional resources to tackle their debt.

In summary, the impact of a student's government job on Parent PLUS loan forgiveness is indirect and primarily influences repayment strategies rather than offering immediate forgiveness. Parents should carefully navigate the complexities of federal loan programs and consider the long-term implications of their borrowing decisions, especially when their children pursue careers in the public sector. Understanding the interplay between loan forgiveness programs and employment choices is crucial for effective financial planning.

Can You File for Student Loan Forgiveness? A Comprehensive Guide

You may want to see also

Frequently asked questions

Parent PLUS loans are not automatically forgiven if the student gets a government job. However, the parent borrower may qualify for Public Service Loan Forgiveness (PSLF) if they work full-time for a qualifying government or nonprofit employer and make 120 eligible payments.

Parent PLUS loans can be forgiven through the PSLF program if the parent borrower (not the student) works full-time for a qualifying federal government employer and meets all PSLF requirements, including 120 qualifying payments.

No, the student’s government employment does not directly affect Parent PLUS loan forgiveness. Forgiveness depends on the parent borrower’s employment and participation in programs like PSLF.

Yes, Parent PLUS loans are eligible for forgiveness under certain government programs, such as PSLF or income-driven repayment (IDR) plans after 240–300 qualifying payments, depending on the plan.

Parent PLUS loans are not forgiven if the student joins the military. However, the parent borrower may qualify for military-related benefits or deferment options, but forgiveness depends on the parent’s own employment or repayment plan.